Is Crypto Reporting ‘Impossible’ Under US Law? Experts Weigh In

Upon receiving $10,000 worth of cryptocurrency in a DeFi transaction, you must report the seller's name and social security number to the IRS.Crypto reporting in the US Is it impossible?

The United States Securities and Exchange Commission’s (SEC) approval of a spot Bitcoin (BTC) exchange-traded fund (ETF) could come any day now. And when it does, many believe that everything will change.

But is the United States ready for an onslaught of first-time crypto investors? Regarding tax compliance, maybe not.

Crypto investors will have to pay taxes on their profits just as investors do when they sell stocks, bonds, and real estate. That much is clear. But the whys and wherefores are still up in the air.

Jerry Brito, CEO of crypto lobbying group Coin Center, wrote in a blog post on Jan. 2 that it’s “virtually impossible to comply” with crypto tax reporting obligations as things stand now, particularly in light of a provision added a few years ago as part of the United States Infrastructure Investment and Jobs Act.

- BitGo Receives In-Principle Approval for Digital Payment Token Services License in Singapore 🇸🇬

- 🚨 Attention Crypto Lenders: Return the Money or Face the Music! 🎶

- Bitcoin ETF’s false start Was it a hack or a mistake by an SEC intern?

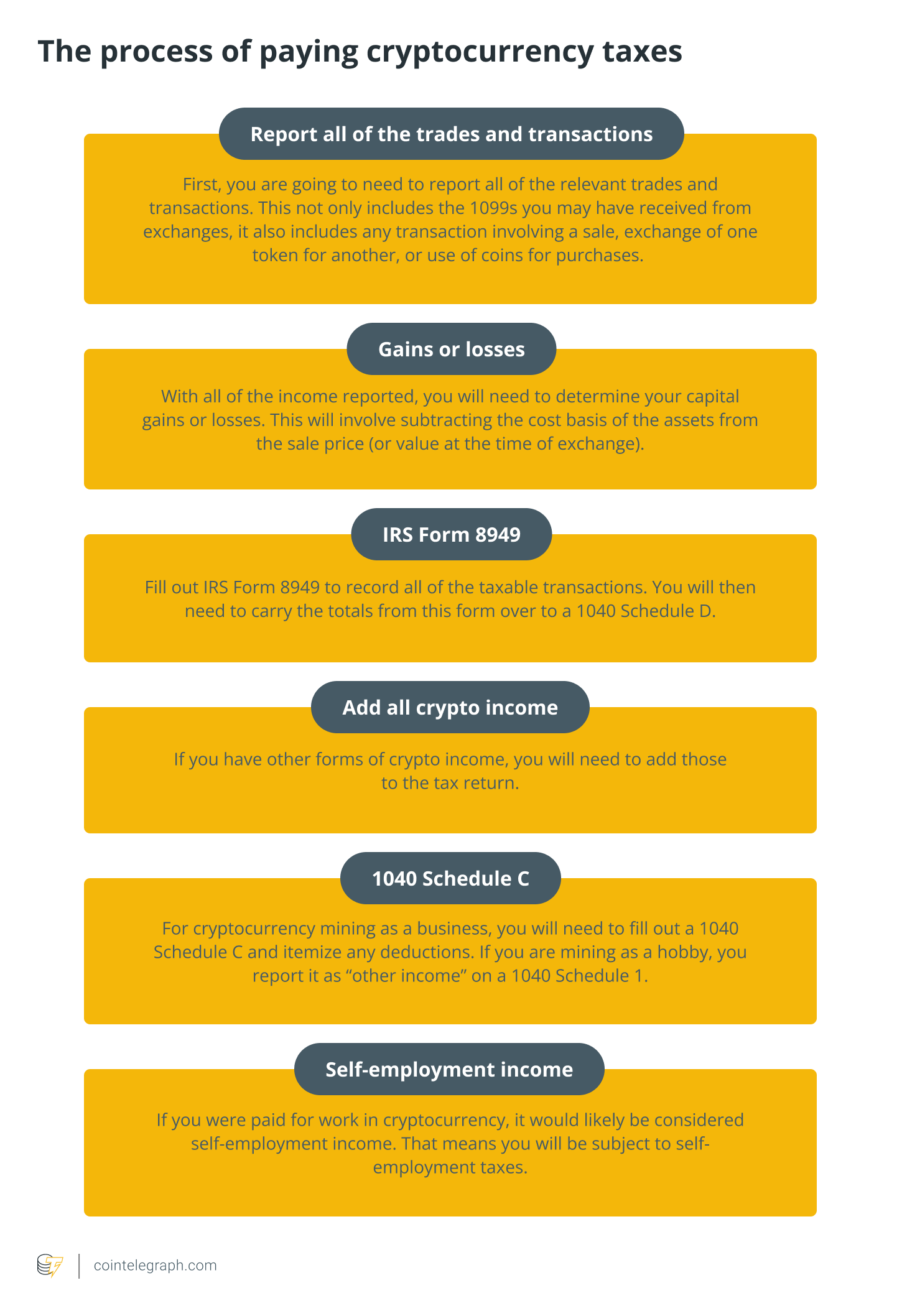

Reporting Requirements for Crypto Transactions

That provision, which took effect on Jan. 1, 2024, amends the U.S. tax code “to require anyone who receives $10,000 or more in cryptocurrency in the course of their trade or business to make a report to the IRS [the U.S. Internal Revenue Service] about that transaction,” Brito noted.

This might seem innocuous enough, but if, for example, a Bitcoin miner receives block rewards in excess of $10,000, then “whose name, address, and Social Security number do they report,” as now required by law, Brito asks.

Or say you “engage in an on-chain decentralized exchange of crypto for crypto and you, therefore, receive $10,000 in cryptocurrency, who do you report?” How does one even determine if the amount of crypto is equivalent to $10,000?

“The law is silent on this matter, and the IRS has not issued any guidance answering these and other questions,” wrote Brito.

Are the New Requirements Really Murky?

But are the new requirements really so murky? Will they inhibit would-be investors and set back crypto adoption in the U.S., as some warn? Maybe there are other tax frameworks that U.S. law and rule-makers should follow in anticipation of crypto going mainstream — like those in Switzerland, the United Kingdom, or Singapore, for instance.

When asked if it is indeed difficult for most investors to comply with existing U.S. tax laws regarding crypto, Omri Marian, professor of law and academic director of the Graduate Tax Program at the University of California, Irvine School of Law, disagreed with Brito’s characterization.

“The law only applies to payments over $10,000 in the context of a ‘trade of business,’ which is a term of art,” Marian told Blocking.net.

“If I am a car dealer, for example, and I sell a car for $10,000 in cash, I have to report the buyer to the IRS. And I can because I know who the buyer is. The law applies the same requirement to selling goods and services in exchange for crypto.”

If car dealers — or any other business owners — can comply in the cash sale context, then so can crypto buyers and sellers. “The medium of exchange makes no difference,” Marian says.

But what about Bitcoin miners, one of the specific examples cited by Brito? “In the absolute majority cases, miners will not be considered to be engaged in a ‘trade or business’ under current law,” said Marian, which means the requirement will not apply to them.

It’s also “extremely unlikely” that a Bitcoin miner will receive $10,000 or more from a single person whose transactions that miner validated, “so again, the law is not applicable,” he added.

Still, the IRS has yet to publish any guidance in this area, which doesn’t help.

“It’s a bit too early to conclude that it’s virtually impossible to comply,” Shehan Chandrasekera, head of tax strategy at CoinTracker, told Blocking.net. However, it will certainly be a challenge in the short term.

Even though the law went into effect on Jan. 1, the IRS has yet to issue any regulations or update its Form 8300 to report digital assets, noted Chandrasekera, adding:

“Until these regs are out, we can only speculate what exactly will need to be reported for digital assets.”

Only a Minority Will Be Impacted

Nathan Goldman, associate professor at North Carolina State University’s Poole College of Management, told Blocking.net that the new rule will not affect the majority of crypto traders simply because most transactions will not meet the $10,000 threshold.

However, investors who trade large amounts of crypto will likely be impacted by the seemingly vague provision.

For example: “If you sell somebody an entire Bitcoin, you will be over the $10,000 limit, and you will have to report the transaction to the IRS. If this is a routine transaction to somebody you know, it will still be somewhat obtrusive” because you need to get their name, address, social security number, among other things. “However, you can comply with the rule.”

“On the contrary, if this is to an unknown party, a crypto exchange company, or something else of that magnitude, it is unclear how this transaction can be documented.”

Again, there is no IRS guidance here, and it could be particularly worrisome for those who have already had a $10,000 transaction in 2024, especially in light of the 15-day period before the non-reporting of the transaction becomes a felony, Goldman added.

What About DeFi Transactions?

Still, doesn’t the unique decentralized nature of crypto render some reporting problematic? Take the decentralized finance (DeFi) transactions, which Brito cited above.

“At the moment, it is literally not possible to comply with the reporting requirement,” Miller Whitehouse-Levine, CEO at the DeFi Education Fund, told Blocking.net. What’s needed instead for the 60 million Americans who own digital assets today are “fit-for-purpose tax provisions” that basically regard crypto as a different sort of case.

Treating crypto as a special case with tailored rules would “improve tax compliance overall and provide the clarity necessary to foster domestic innovation,” continues Miller. There are even places where this approach is already being taken, he added:

“The United Kingdom is a good example of a model that the U.S. might follow, especially when it comes to the taxation of DeFi transactions.”

In 2023, the U.K. actually “issued a call for responses on how best to tax DeFi transactions,” Miller recalled, a recognition that the U.K. understood the novelty of the new technology and the fact that “a new framework that is tailored to digital asset transactions is needed.”

Others, however, take the view that crypto is more similar to than different from other financial transactions and, therefore, doesn’t need special legislation or rules.

“In the context of DeFi, if you choose to sell something to someone for $10,000 in crypto without knowing who this person is, so you can’t report that person, then you made a conscious choice to break the law. Similarly, if I choose to make an anonymous sale in cash to someone, I also break the law,” said Marian, adding:

“The bottom line is that in almost all cases, people can comply because they can, in fact, identify the buyer or because the reporting requirement doesn’t apply to them.”

What Changes Could Congress Make?

Still, let’s assume for the sake of argument that crypto is a special case and deserves its own particular tax framework. What sort of changes would Congress then need to make?

“Congress should consider adding a de minimis exemption — like the ones on foreign currency transactions — to limit the small and innocuous reporting requirements that could surround cryptocurrency,” said Goldman. This would allow taxpayers to avoid having to incur a tax liability every time they make crypto transactions.

Is Crypto Adoption at Risk?

If Congress does nothing, could that impact crypto adoption in the United States? “I believe it would,” answered Goldman. “However, I also believe that is not a bad thing at this time.”

Congress has been very careful about imposing too many — or too few — restrictions on cryptocurrency, he further explained. In some ways, the U.S., through its inaction, is letting crypto chart its own path.

While that might hinder short-term adoption, it shouldn’t prove an obstacle to widespread acceptance in the longer term, he suggested.

Marian, for his part, doesn’t believe Congressional inaction will harm crypto adoption in the United States. “To date, crypto has seen almost no formal tax guidance in the U.S. and has been operating essentially under the existing tax framework. Yet, ‘miraculously’ crypto is still on the rise in the U.S., and has been since its introduction,” he said.

Nor is there any empirical evidence that links market movements and U.S. tax guidance on cryptocurrencies, at least as far as Marian is aware. “If people do not more widely adopt crypto in the U.S., it has nothing to do with tax [treatment].”

One probably shouldn’t count on Congressional action on the crypto front these days — given all the other things happening in the world. Assuming things stand as they are now, at least in the short term, what is the single most important thing that retail investors should know about crypto tax reporting for 2024?

“Investors need to carefully document their transactions,” Goldman said. “As IRS attention toward cryptocurrency ramps up, it will become imperative that taxpayers can support their transactions. I expect this to be an area that the IRS increasingly applies pressure toward, and it will be imperative for investors to support their transactions if under audit.”

Q&A

Q: What are the current tax compliance requirements for crypto investors in the United States?

A: Crypto investors will have to pay taxes on their profits just like investors do when they sell stocks, bonds, and real estate. However, specific reporting obligations can be complex and unclear.

Q: What is the new provision added to the U.S. tax code regarding crypto tax reporting?

A: The provision, which took effect on January 1, 2024, requires anyone who receives $10,000 or more in cryptocurrency in the course of their trade or business to make a report to the IRS about that transaction.

Q: Are the new requirements for crypto tax reporting impossible to comply with?

A: Experts have different opinions on this matter. While some argue that compliance is difficult due to uncertainties and lack of IRS guidance, others believe that compliance is possible within the existing tax framework.

Q: How will the new tax reporting requirements impact crypto traders?

A: The majority of crypto traders will not be affected as most transactions will not meet the $10,000 threshold. However, investors who trade large amounts of crypto may be impacted and will need to report transactions to the IRS.

Q: What challenges arise from reporting decentralized finance (DeFi) transactions?

A: Reporting DeFi transactions can be problematic due to the unique decentralized nature of crypto. Some experts argue that tailored tax provisions for crypto transactions, like those in the United Kingdom, would improve tax compliance and foster domestic innovation.

Q: Should Congress make changes to the tax framework for crypto?

A: Some experts suggest that Congress should consider adding a de minimis exemption to limit reporting requirements for small and innocuous crypto transactions. This would provide relief to taxpayers and reduce the burden of tax compliance.

Q: Will Congressional inaction on the crypto tax framework hinder crypto adoption in the United States?

A: While Congressional inaction might hinder short-term adoption, experts believe it should not be an obstacle to widespread acceptance in the longer term. Crypto has been on the rise in the U.S. even without formal tax guidance.

Q: What should retail investors know about crypto tax reporting for 2024?

A: Retail investors should carefully document their transactions as IRS attention toward cryptocurrency increases. It will be imperative for investors to support their transactions if they come under audit.

Reference List

- Bitcoin Price Regains Strength: BTC Could Still Remain in Range until 2024

- Binance 2023 Report Reveals 40 Million New Users Added, Total Registered Users Reach 170 Million

- What Bitcoin ETF Approval Could Mean for Coinbase and MicroStrategy Stock

- Crypto Index Funds Simplify Investing but Challenge Blockchain Ethos

- A Taxing Obligation: Is Crypto Reporting ‘Impossible’ Under US Law?

Interact with us! What are your thoughts on the current crypto tax reporting requirements in the United States? Share your opinions and join the conversation on social media. 💬📲🌐

Image Source: Miximages

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- SEC Under Fire: Senators Call for Report on X Account Breach

- Lawyers and politicians are demanding an investigation of the SEC’s handling of the Bitcoin ETF post.

- SEC Investigation Won’t Stop Bitcoin ETF Decision, But Could There Be a Delay? 🕵️♂️

- Oops! SEC Twitter Account Hack Creates Bitcoin ETF Chaos

- The State Comptroller’s Concerns over NYDFS Management of BitLicense

- Blockchain Association takes on Sen. Warren’s criticism of crypto hiring

- How “Bitcoin Rodney” Scammed Millions With a Fake Investment Scheme 😱

{kind=link}