The so-called "Defi", how much do you go to the center?

Most of today's decentralized financial projects are built on Ethereum, and there are many components that collaborate and accumulate, such as:

1. Core consensus agreement;

2. Assets;

3. Smart contract agreement.

- Programmer Xiao Ge told: What is the experience of all the wages only bitcoin?

- Babbitt column | Shenzhen digital currency mobile payment pilot zone prequel

- Ethereum was “occupied” by USDT, with network utilization of 90%

Smart contracts make new crypto assets possible, and new assets can quickly become collateral, making more new assets possible, all based on the underlying core consensus agreement.

Therefore, 2) "assets" and 3) "smart contract agreements" actually rely on 1) "core consensus agreement", which means that the decentralization of "assets" and "smart contract agreements" cannot exceed the "core consensus agreement". The degree of decentralization.

In other words, since the "core consensus agreement" is the foundation layer on which the " asset" and "smart contract agreement" are built, the "core consensus agreement" determines the " asset" and "smart contract agreement" that can be achieved/maintained. The theoretical maximum decentralization level.

Developer thinking and design choices

Some assets and agreements are built on Ethereum and bear in mind the core principles of Ethereum, but others are not.

Uniswap was a decentralized exchange agreement published on the Ethereum mainline in November 2018 and funded by the Ethereum Foundation, which was founded by Hayden Adams. For design choices, Hayden Adams explained:

When I created Uniswap, what I really consciously did was to imitate the properties of Ethereum. I really care about some of the key attributes of Ethereum. Its processing efficiency and storage are not the most efficient. But it is the most decentralized programming method, and the most anti-review ability… It has all these features for untrusted execution. So these (characteristics) are also what I am trying to rebuild.

This passage by Hayden Adams touches on the "choice" problem faced by Ethernet, Bitcoin and other blockchain protocols: the scalability trilemma , the blockchain system is difficult to base. The layer does the following three things at the same time:

1. Decentralization;

2, scalability;

3. Security.

There is currently no blockchain that combines high performance decentralization, scalability, and security. Although Bitcoin and Ethereum's Work Proof (PoS) consensus algorithms are designed differently, both ultimately chose higher "decentralization" and "security" at a lower "extensibility". The "assets" and "smart contract agreements" based on Ethereum are also inherited from this design.

One thing to keep in mind is that there is no end to "decentralization." It is often a floating standard with subjective consciousness. Therefore, decentralization cannot be reached, it is just a goal that requires hard work. In addition, a thing built on the Ethereum does not mean that it has the same attributes as Ethereum.

assets

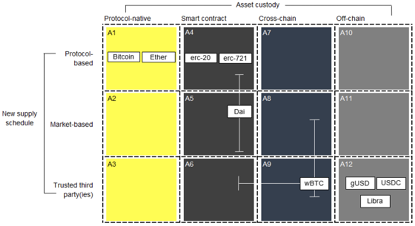

The basic framework of distinguishing different assets by two dimensions of hosting and supply

1. Bitcoin and Ethereum – both represent the “gold standard” of decentralization in all of the above assets. Both are protocol-level, which means that both hosting and new provisioning are handled at the protocol level, and both are transparent and open. The supply rules for Bitcoin and Ethereum are known (12.5 new bitcoins are generated every 10 minutes, 2 new Ethereums are generated every 15 seconds) and can be checked. Both are also programmatic anti-inflation assets, which exist for 10 years (bitcoin) and 4 years (Ethereum).

2, ERC-20, ERC-721 and other token standards – are audited smart contract standards, similar to Bitcoin and Ethernet, the way of hosting and new supply is open and transparent. However, these token standards have additional risks:

- Hosting and ownership are currently handled by smart contract code;

- The circulation of different tokens may vary greatly and needs to be checked at a reliable source. OnchainFx is a good source for checking supply (see "2050 Supply" and "Supply Snapshot")

3, DAI – Maker's stable currency DAI is a very interesting stable coin experiment, DAI retains many of the key attributes of Ethernet, but through the integration of multiple smart contracts and decentralized stakeholders, adds a lot of complexity Sex. DAI is an ERC-20 token that is managed by smart contracts, and the supply will vary depending on market conditions, depending on the creation of a net mortgage debt (CDP) .

4. Cross-chain assets – wrapped BTC (wBTC) is relatively new and small in number. It represents an innovative solution – the “wrapped assets framework” that enables bitcoin or other cross-chain assets. Enter the smart contract on the Ethereum. wBTC does have some transparent features that users can check, but it also brings various risks, such as: intermediary risk (including merchants and custodians), smart contract risk (ERC-20), mortgage risk.

5. Under-chain hosting – The risks include the extent to which intermediaries provide users with transparency and inspection in terms of hosting processes and security measures. (You can see again how parcel assets provide security measures)

Note: Many of the above assets are derivatives, and they all derive their value from the underlying assets (such as US dollars, Bitcoin or a basket of assets). As can be seen from the two-dimensional graph above, the supply of derivatives (such as wBTC) is different from the supply of its underlying assets (such as BTC).

protocol

Below is a brief list of the design features that I have observed to some extent at the expense of "decentralization":

1. Rent-seeking – rent-seeking may be made in two ways, one is the cost, that is, the gas fee is exceeded; the second is that a unique token must be used. In theory, if rent-seeking is released in open source code and the cost is built into the protocol in some way, then the protocol is easily forked and the cost-related code is removed in the forked chain. We have actually seen this situation, such as Zcash/Zclassic, Bancor/Uniswap.

2. Closed contributor collections—for example, in a Proof of Entitlement (PoS) system, if the verifier set is a closed “selected” verifier, or if the verifier's election process is not random, then trust is transferred. To the "ruling intermediary", decentralization is limited. Similarly, for smart contracts that rely on external data, a small, manipulated oracle (Oracle) collection introduces additional risk.

3, trapdoors – if a developer can temporarily lock, or permanently stop a function, then the code of this smart contract is not autonomous. Of course, it also needs to be divided into two. For example, when a smart contract finds a loophole, it is beneficial at this time.

The above mentioned are not comprehensive, just a few examples of the trade-offs I have observed in the design of the protocol. Often, you need to be very close to the code to understand exactly what you trust.

Don't confuse open finance with decentralized finance

Some smart contract agreements and assets do not show much decentralization, they are only open and can be used for free. In other words, we can say that some assets and agreements may be part of "open finance," but not "decentralized finance."

Of course, the line between open finance and decentralized finance is not clear, and there is a lot of overlap and mixing between the two. Not only that, but because of the lack of a clear definition, some terms are also easily misrepresented, resulting in a disconnection of trust.

- 2016: "Blockchain, not Bitcoin"

- 2017: The clichéd white paper dilutes the original meaning of blockchain terminology

- 2018: "Decentralized Finance / DeFi" and "Open Finance" emerged and used to promote a variety of projects with varying degrees of decentralization and openness.

- 2019: Libra tries to distort the meaning of "cryptocurrency"

How much decentralization is the so-called "decentralized finance"?

It varies significantly by protocol, asset, and application. There are even some decentralized things that come out in a centralized form because they are hosted on exchanges and other aggregation platforms.

Users need to constantly question the wording and feasibility of the various emerging financial instruments they use, and more importantly, who they trust (such as centralized agents) and what exactly they are (such as smart contract codes).

If an asset or an agreement has no good reason to deviate from the design principles of the base layer, then we have good reasons not to use these new financial instruments.

Written by: Aaron Hay

Source: Chain smell

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- BTC 徘徊 "万" word area long and short into the tug of war

- Getting Started with Blockchain | Opening the "Three Locks" for Bitcoin Smart Contracts

- 0.32 dollars to buy 40 bitcoins: the currency exchange will not work hard, the regular army will come

- Twitter Featured | 300 million Telegram users will be able to trade Bitcoin, Tether is blocking the Ethereum network

- The Ethereum Foundation funds $2.46 million to developers to advance Ethereum 2.0

- Heavy | China Telecom Releases 5G Era Blockchain Smartphone White Paper

- There are only two kinds of coins in the currency circle: community coins and "community coins"