Why is the "DAO + ICO" fundraising method proposed by Vitalik not working?

Written by: Hao Kai, Hashkey Capital Research

Source: Chain News

"DAICO" or "DAO + ICO" is a new fundraising method proposed by Ethereum founder Vitalik Buterin during the ICO boom in January 2018. He hopes to integrate the concept of the decentralized autonomous organization DAO into the ICO fundraising In the process of capital investment, to solve the problems existing in traditional ICO, so that the blockchain project parties can successfully raise funds, and the interests of investors can be protected.

However, we have studied the operation mechanism and practice of DAICO , and have come to a conclusion: DAICO cannot effectively solve the problems existing in traditional ICO .

- People's Posts and Telegraphs: Six possibilities for blockchain development in 2020

- Davos News | Ten-year journey, China Blockchain Industry Figure Contribution Awards announced

- Industrial blockchain enters the market, 2020 may usher in an inflection point

This conclusion is mainly based on our findings:

- The game between the investor and the project party cannot promote the project to always develop in a favorable direction;

- DAICO has not been recognized and adopted by the mainstream blockchain market;

- Many people have proposed improvement plans for DAICO design, but the specific effects need to be tested in practice.

So, for now, DAICO is not a successful way to raise funds.

What are the disadvantages of ICO?

To illustrate our conclusions, let's start with the ICO boom.

In 2017, due to the high return on investment of some digital currencies, the initial coin offering (ICO, Initial Coin Offering), a fundraising model, quickly became popular. The following figure shows the fundraising situation of digital currency projects through ICO in 2017 and 2018 calculated by CoinSchedule. The statistics of different institutions may not be completely consistent, but the trends are generally the same. At the beginning of 2018, the project owner can raise billions of dollars from the market through ICO every month.

Figure 1 ICO funds raised in 2017 and 2018, data source: CoinSchedule

Figure 1 ICO funds raised in 2017 and 2018, data source: CoinSchedule

Although the ICO has promoted the popularity and development of the blockchain to a certain extent, on the whole, the ICO market has shown a chaotic and lack of supervision. Many criminals use the name of ICO to commit fraud. The main disadvantages of ICOs include:

- The project party does not promise any guarantee

The risk of investors participating in the ICO is very high. One of the important reasons is that the project party will not provide any guarantee for investment returns and development progress. After the project parties easily raise tens or even hundreds of millions of dollars, it is difficult to guarantee that they will continue to treat investors as a community of interests.

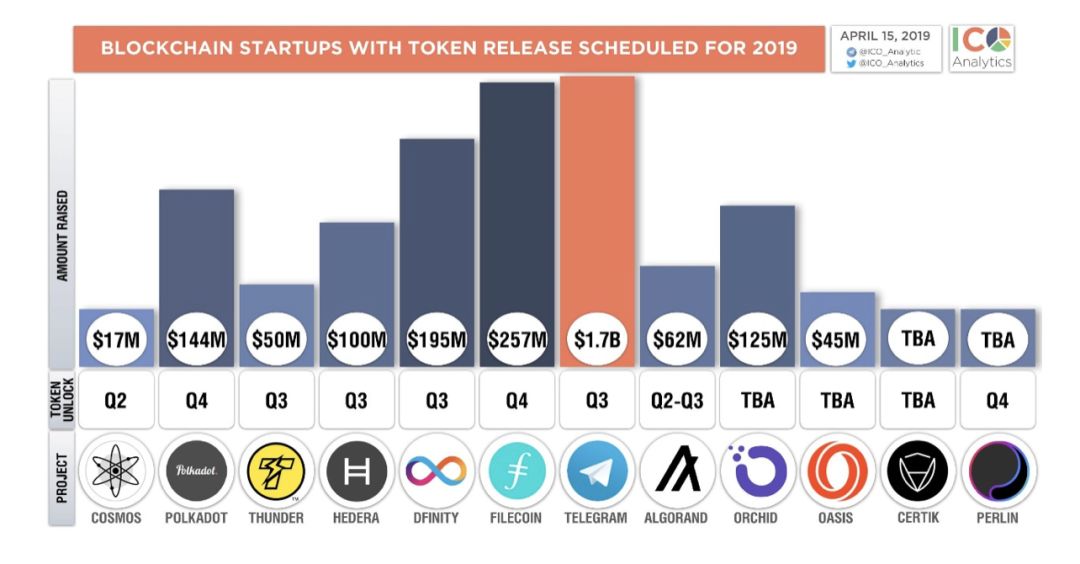

The following figure is a part of the ICO Analytics statistics that may launch and issue tokens on the mainnet in 2019 . As can be seen from the figure, well-known projects such as Telegram, Filecoin and Dfinity have raised a lot of funds, but their development progress is not satisfactory, and so far (January 2020) has not yet been launched on the main network.

Figure 2 Some projects that may be launched in 2019, source: ICO Analytics

Figure 2 Some projects that may be launched in 2019, source: ICO Analytics

- The project party has complete discretion over the funds raised

After the end of the ICO, the project party can get all the funds immediately and can freely dispose. Investors have no way to intervene in the use of funds, and investors' rights have not been protected in any way. For example, in October 2018, the Rchain project exploded in cash flow problems. However, in the official financial information provided by Rchain, the board's salary has increased, which is obviously not in the interest of investors.

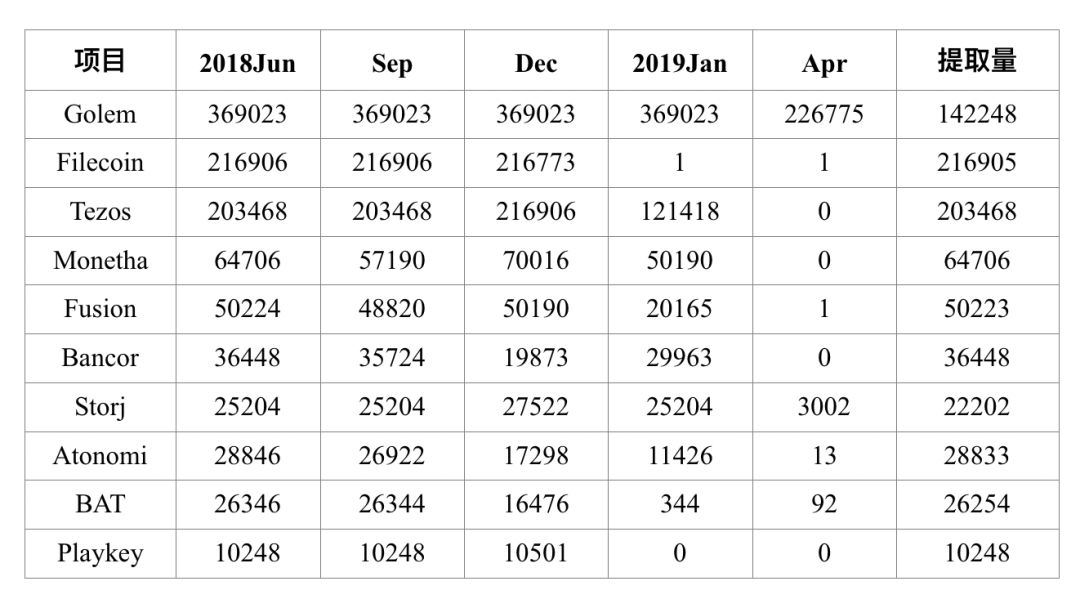

The following table shows the changes in the ETH balance raised by some project parties in April 2019. As can be seen from the table, most project parties will choose to take out all ETH within a short period of time, and there is no detailed description and plan for the use of funds.

Table 1 ETH balance raised by the project party, data source: diar

Table 1 ETH balance raised by the project party, data source: diar

- It is difficult to hold the project party accountable

Because digital currencies have the characteristics of natural cross-borders, investors from all over the world can participate in ICOs. Once the project party commits fraud, it is difficult for investors to recover the loss of funds through legal channels . Therefore, China's supervision of ICOs is very strict. The Announcement on Preventing the Risk of Token Offering and Fundraising (2017) and related documents have repeatedly emphasized that issuing digital currency to domestic residents to raise bitcoin and ether is illegal securities. activity.

What is the operation mechanism of DAICO?

In view of the shortcomings of the above ICO, the blockchain field needs a more reasonable way of raising funds. In January 2018 , Ethereum founder Vitalik Buterin proposed a fundraising method called DAICO , which aims to solve the problems existing in traditional ICOs . While the project party can successfully raise funds, the interests of investors can also be protected.

DAICO stands for DAO (Distributed Autonomous Organization) + ICO, and integrates the concept of DAO into the ICO fundraising process. Based on the traditional ICO, DAICO adds a smart contract between the investor and the project party. After the fundraising is over, the smart contract will continue to track the development progress of the project and conditionally release the raised funds conditionally.

May wish to briefly introduce the operation mechanism of DAICO:

- DAICO process

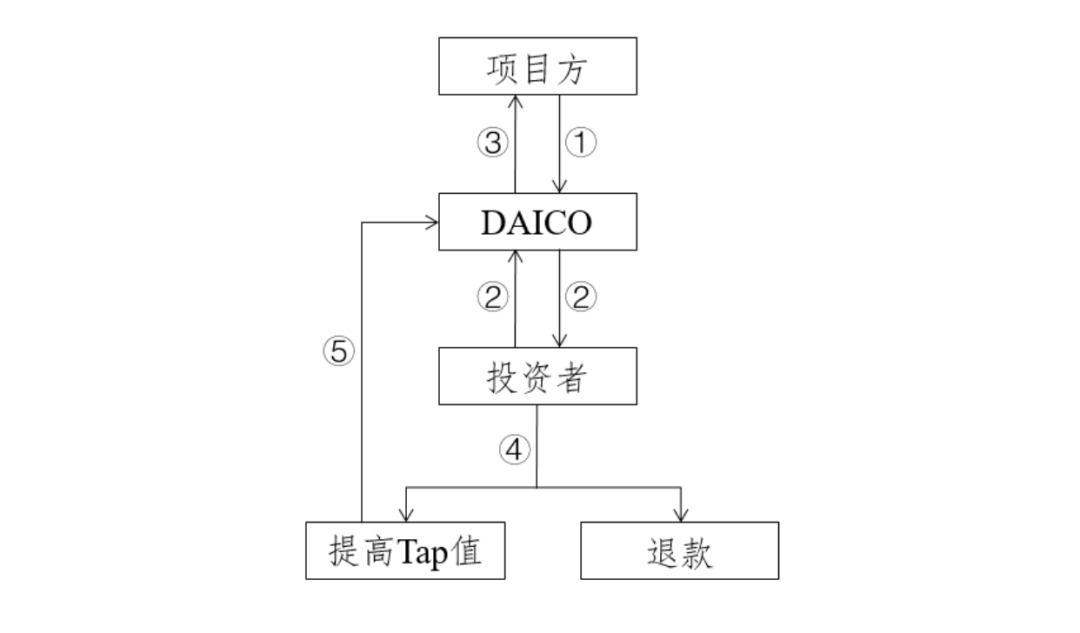

The project fundraising process through DAICO is shown in the following figure.

Figure 3 DAICO process

Figure 3 DAICO process

- Project party initiates DAICO contract

- Investors contribute ETH to the DAICO contract and obtain ERC20 tokens, which is no different from traditional ICO;

- After the end of the contribution period, a new state variable Tap will appear in the contract. The project party withdraws ETH from the contract according to the Tap value. The Tap value determines the speed at which the project party takes ETH from the smart contract;

- Token holders can choose to "tap value" or "refund" by voting according to the progress of the project. If token holders vote for a "refund", the process ends;

- If the token holders vote for "Tap Increase", then the Tap value in DAICO will increase, and the project party will withdraw the ETH with the new Tap. You can continue to vote to "increase the Tap value" before voting is completed through "refund" or ETH is withdrawn.

- What DAICO can solve

The funds raised through DAICO are not issued to the project party in one go, but are gradually released through smart contracts and voting mechanisms. If the project party wants to get all the raised funds, then the project must be continuously developed. DAICO can effectively overcome the incentive problems of traditional ICOs, keep the interests of the project party and investors consistent, and greatly reduce the risk of project party fraud.

At the same time, investors can also intervene in the process of issuing funds. For outstanding project parties, investors can vote to increase the Tap value, speed up the unlocking of funds, and help the project party accelerate the development progress. If investors are not satisfied with the progress of the project, investors can vote for a refund and recover the remaining ETH in proportion. . It should be noted that investors cannot vote to lower the Tap value, but project parties can vote to lower the Tap value voluntarily.

- Game Theory of DAICO

The original design of DAICO is to allow investors to decide whether to continue to support this project based on the performance of the project party and the development of the project. However, it should be noted that the purpose of investors and project participants participating in DAICO is to obtain the maximum possible income, so the income will largely determine the voting choices of investors and project parties.

According to the price of the secondary market, when the exchange rate of ERC20 tokens issued by the project party to ETH is higher than the initial exchange rate, that is, when the value of ERC20 tokens relative to ETH increases, even if developers abuse funds and delay project progress, rational investment They will not choose to vote for a refund, they will choose to sell ERC20 tokens in the secondary market to get higher returns. At the same time, there may be some project parties who value short-term benefits want a refund, because the remaining ETH value in the raised funds is lower than the ERC20 token value issued to investors.

Similarly, according to the price of the secondary market, when the exchange rate of ERC20 tokens issued by the project party to ETH is lower than the initial exchange rate, that is, when the value of ERC20 tokens relative to ETH decreases, even if the project party continues to develop, the project will be carried out smoothly. Some investors will still choose to refund to reduce investment losses.

It should also be noted that the fund raised by the project party is ETH, and ETH is easily affected by the overall digital currency market, and the price fluctuations are very large. The violent fluctuation of ETH price will affect the incentive mechanism in DAICO. For example, when ETH is in a downward trend, the project party hopes to unlock and sell all ETH as soon as possible to avoid suffering greater losses. At this time, regardless of the actual progress of the project, the project party will increase the Tap value by voting. Therefore, using ETH for fundraising is not the best option.

On the whole, the voting mechanism designed by DAICO cannot effectively motivate excellent projects and eliminate bad projects, and the game between investors and project parties cannot always promote the project to develop in a favorable direction.

DAICO is not effective in practice

Abyss, a distributed game publishing platform, is the first project to raise funds through DAICO. In May 2018, Abyss raised more than 15 million US dollars through DAICO. Abyss gives specific requirements for each voting time, voting weight, and percentage of voting.

The following picture shows the voting status listed on the Abyss website. As can be seen from the figure, Abyss has conducted a total of 5 votes, 4 of which increased the Tap value and passed the vote, and 1 decreased the Tap value and failed. Since November 2018, Abyss has never voted again. During this period, no votes were cast on refunds.

Figure 4 Abyss vote

Figure 4 Abyss vote

According to CoinMarketCap data, the token price of the Abyss project has performed poorly, and has fallen by almost 90% relative to the price at the time of issue, and has fallen by about 50% relative to the price of ETH.

According to the previous analysis, in this case, a rational investor should ask for a refund, but actually did not vote for a refund. There are two reasons for this phenomenon. One is that investors are full of confidence in the Abyss project and believe that poor price performance is only a short-term phenomenon; the second is that investors have already sold their ERC20 tokens and do not care about the development of the project at all. We think the second possibility is even greater.

In addition to Abyss, projects such as BitGame and Tokedo also use DAICO to raise funds, but the popularity of these projects is generally low, which shows that DAICO has not been accepted by the mainstream blockchain market.

Reflections on DAICO Fundraising Model

DAICO integrates the idea of DAO into the ICO fund-raising process to balance the rights of investors and project parties to a certain extent. It is designed to allow investors to decide whether to continue to support the project based on the performance of the project party and the development of the project. .

However, DAICO cannot effectively solve the problems existing in traditional ICO.

First, many investors are more concerned about their short-term income and are not concerned about the future development of the project. They will not vote based on the actual development of the project. In addition, some investors do not even participate in voting, so the project party still has a decisive influence on the voting results.

Second, the voting result is directly related to the number of tokens. If the project party holds most of the tokens through reservations, purchases from the secondary market, or even conspiracy, then it is equivalent to the project party being able to act according to their wishes, and the voting mechanism designed by DAICO will be directly invalidated.

Third, it can be seen from the acceptance of the blockchain market that DAICO has not been recognized and adopted by the mainstream blockchain market. This model is not highly attractive to project parties and investors.

There are also many people who have proposed improvements to DAICO design:

- It is fundraising using stable coins like DAI . The price of stablecoins does not fluctuate and is not easily affected by the entire digital currency market. This can reduce the impact of price factors on investors and project parties to a certain extent during voting. However, it should be noted that the token prices given by most digital currencies during the fundraising stage have not been subjected to rigorous valuation calculations. Therefore, the prices of these tokens will still fluctuate greatly in the secondary market. Fundraising does not fundamentally solve this problem.

- After the fundraising is completed, ERC20 tokens will not be issued to investors, but will be issued after the project has achieved phased results (such as the main online line). Prior to this, investors participating in DAICO had only voting rights, but could not trade ERC20 tokens on the secondary market, and the token price would not change. By adopting such an issuance mechanism and adopting a stablecoin fundraising design, investors and project parties can vote independently of the price factor and based on the progress of the project. However, this method prevents investors from realizing cash quickly, and may reduce the enthusiasm of some investors for participation.

- Based on the DAICO model, an " agent " agency can be introduced to objectively judge the actual progress of the project and solve the problem of the bad project being overvalued and the good project being killed by mistake. But before that, you need to find a completely objective agency and solve the problem of agency fees. This part of the cost can be paid by investors, just like the "investment consulting fee" in reality.

- It is the specific requirements for the voting weight of each address in the DAICO model, the proportion of participation in voting, and voting incentives to increase the voting participation of investors and reduce the possibility of the project owner being the only one.

In summary, DAICO cannot effectively solve the problems existing in traditional ICO, and this model has not been adopted by the mainstream blockchain market. Although others have proposed improvements to DAICO, the specific effects need to be tested in practice. At the moment, DAICO is not a successful fundraising design.

Review: Dr. Zou Chuanwei, Chief Economist of Wanxiang Blockchain, PlatON

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Holding money or saving money for Chinese New Year this year? We looked at the data for the last ten years

- New Year's Eve Survey: Nearly 90% of professionals believe that blockchain iconic applications will emerge this year

- Digital currencies have now become part of the global financial system

- Bakkt's consumer application launches this year and will be more like PayPal

- CME Group's bitcoin options trading volume surges 200%. Can Wall Street's capital barriers be completely broken?

- Long Baitao | Digital Asset Research Institute Digital Currency Weekly Report (2020/1/19)

- British Telecom giant withdraws from Libra Association! But there are 1,500 companies waiting to join