2019 stablecoin research report: why is the current use scenario restricted and how to adapt to the mainstream payment environment?

Overview

We usually do not associate the stability of financial assets with cryptocurrencies. After all, we have seen a lot of events such as "hundred times coins" and "return to zero coins" in just a few years. Bitcoin, as its representative, did not inherit the price stability of major fiat currencies when it inherited the payment function of fiat currencies. As a brand new digital asset, it has no connection or support with other stable financial assets or legal systems. However, most people will buy Bitcoin as an investment.

However, as a digital cash, Bitcoin solves the problem of a payment mechanism that bypasses censorship, that is, "allow online payments to be sent directly from one party to another without going through a financial institution." This is a new payment instrument that is not affiliated with any institution, and it largely exceeds (or even attempts to challenge) the existing regulated financial system. Therefore, in order to have a value standard that is more acceptable to most people, stablecoins came into being.

This article will introduce the classification of existing stablecoins, and discuss whether stablecoins will eventually break through the closed-loop cryptocurrency world and enter our wider financial system. In addition, possible application scenarios for stablecoins in existing payment systems. And conclude whether stablecoins will expand into more common business interaction and payment scenarios.

- Weekly development of industrial blockchain 丨 Many governments have stated that they will vigorously develop blockchain in 2020

- If Bitcoin prices skyrocket, it could make this country the richest country

- Opinion: The biggest opportunity for blockchain 2.0 is "regulatory technology"

Report

What is stablecoin

Stablecoins are blockchain-based payment tools designed to achieve the price stability required by end users. Some stablecoins use fiat currencies as collateral assets. Others use a range of other non-statutory types of mortgage assets. There are also attempts to use algorithms to achieve price stability without collateral at all.

The stablecoin solves the problem of price instability in the cryptocurrency ecosystem. The stablecoin USDT, which has the largest circulation, now has a market value of USD 4.64 billion. However, all of these stablecoins are experimental, and the current range of practical use is limited to cryptocurrency exchanges, issuers, and speculators.

Application scenarios of stablecoin

Stablecoins have begun to attract attention in the cryptocurrency ecosystem. Specifically, they are popular among existing cryptocurrency traders, miners, and users. The three main functions that dominate current stablecoin use are:

- Locking in profits: Cryptocurrency speculators and traders often convert cryptocurrencies into stablecoins to temporarily "lock in" profits, thereby transferring risk exposure to relatively stable assets. This is especially useful on exchanges that do not have a fiat currency equivalent. Similarly, cryptocurrency miners convert their cryptocurrencies into stablecoins to reduce their directional risk to the mined cryptocurrencies.

- Stable tax haven: In the financial system, transfers and transactions may require service providers to charge fees or tax authorities to collect income taxes, and reporting is required. Stablecoins can avoid the reintroduction of funds into the regulated financial system, thus avoiding taxes.

- Out-of-bank payment: Some miners, speculators or users may not have a commercial bank account in a particular jurisdiction. Stablecoins allow digital access to fiat currencies worldwide. For example, the U.S. dollar stablecoin allows "digital dollars" outside the U.S. without requiring the user to have a domestic bank account within the U.S. In addition, since the stablecoin is open 24/7, when the ACH (Automatic Clearing Center), wire transfer system or other payment infrastructure is closed, the stablecoin can play the role of legal currency value transfer during these times.

In addition, the use of stablecoins can avoid potential friction caused by blockages or temporary holdings of funds that may occur when the KYC program re-introduces funds into the traditional financial system. For example, cryptocurrency trading companies or hedge funds often choose to use stablecoins to implement value between different countries in a more flexible way.

Classification of stablecoins

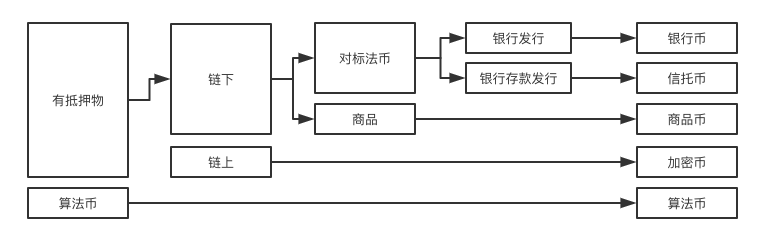

This section describes several methods used by stablecoin issuers to achieve relative price stability, and how they have evolved over time. Figure 1 outlines five types of stablecoins. Figure 2 shows some standard stablecoins.

Figure 1: Stablecoin classification map

Figure 2: Mainstream stablecoins

Stablecoins, backed by fiat currencies, currently dominate the market. Fiat currencies are divided into three types: physical cash, central bank reserves and commercial bank deposits. Currently, commercial bank deposits are most likely to be used as collateral for stablecoins.

- Physical cash: In order for stablecoins to use physical cash as collateral, a warehouse is required to store US dollar banknotes, and a trust or custodian supervises and guarantees that the digital currency issued corresponds to the US dollar. For many reasons, it is impractical to pledge stablecoins with physical cash. Not to mention how difficult it is to keep and transport, the annual cost it pays is an unbearable figure.

- Central bank digital currencies: Some central banks such as China and the European Union have reviewed the digital currency (CBDC) issued by the central bank. Often central bank digital currencies are planning to try to use M0 as collateral. Because this method requires more extensive and elaborate regulatory and economic changes to the existing financial market system, the time to market for these plans is significantly longer, and there are currently no specific cases, so they are outside the scope of this article, but in practice In China, this method may eventually bring the biggest benefits or restraints to domestic consumers.

- Commercial bank deposits: Currently, the stablecoin collateral is usually commercial bank deposits. This article refers to the two sub-categories as "bank currency" and "trust currency" according to their nature.

Bank currency

Banking institutions can use their reputation, existing compliance measures, AML / KYC practices, and auditing measures to issue their own stablecoins. This type of stablecoin can replace traditional bank deposits with local banks because it is issued directly by the bank. Each coin, like a bank deposit, is backed by the portfolio of that particular issuing bank and is subject to the bank's default risk.

However, this method differs from traditional bank deposits because the blockchain itself is a clear record of ownership. This is different from traditional bank accounts. In traditional bank accounts, commercial banks adjust their customer account balances on their own accounts through bookkeeping adjustments or interbank payment systems. This subtle difference means that commercial banks may need to maintain a comprehensive account of all deposits issued on the blockchain system to avoid inconsistent legal ownership between the blockchain ledger and the internal ledger of the commercial bank.

Although Silvergate Bank has only recently begun to provide this service, this type of stablecoin currently seems to be a success. Silvergate is the first bank to issue and redeem stablecoins to facilitate real-time peer-to-peer payments. Payments to the Silvergate Network (SEN) can only be made directly between the issuing commercial banks' own customer networks. Other "challenger" banks that have already established relationships with cryptocurrency companies may follow. The experience of these initial banks can provide important lessons for major mainstream banks to use stablecoins as market opportunities.

Outside of Silvergate, the best known is JPM Coin, a program designed to target payments between businesses with accounts in JP Morgan. Despite some progress, JPM Coin is still a prototype and the actual implementation of mass production may take several years.

Trust currency

Despite the similar characteristics of trust coins and commercial bank accounts, the operation mode of trust coins is more similar to the Venmo, TransferWise or PayPal model: third parties issue stable coins using funds held in their own bank accounts. In this model, there is an additional intermediary (trust or third party), which is different from the bank currency mentioned earlier.

End-user collateral is usually kept separate from all other funds of a third-party trust or company. In addition, a trust or third-party issuer does not always use a bank account held by a commercial bank, but instead uses multiple accounts from multiple banks. This is the most commonly used and most widely used method of stablecoins today.

Tether is a good example of such a product. It occupies the vast majority of the market, with daily transaction volume exceeding 95% of all stablecoins. Tether was launched in 2014 and has issued a token USDT with a 1: 1 USD anchor. The company insisted that the USDT issuance was secured by equivalent bank deposits held in banks.

There are two sources of risk in the Tether model. The first source is the solvency of the banks that Tether uses to hold collateral. The second source is the credibility of Tether itself, especially the company's claim to maintain a banking relationship and to fund it with a USDT issuance amount of 1: 1. Suspicion of Tether collateral has caused the value of USDT to fall below $ 1.

In October 2018, many companies started to launch stablecoins one after another, hoping to grab a share of the tether scandal. Gemini, Paxos and Circle all issued stablecoins, backed by collateral held by commercial banks.

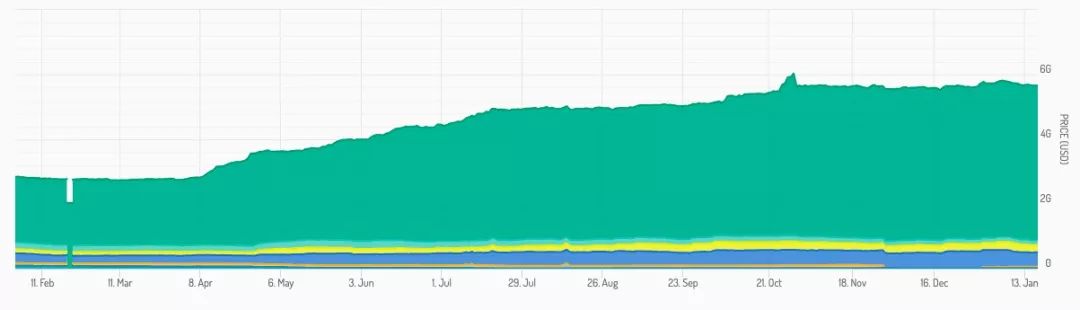

Although the transaction volume of other stablecoins is much smaller than Tether, they are growing rapidly. Figure 3 shows the market value of stablecoins for 2019-2020. During this period, the average number of stablecoins in this category has reportedly increased, although it should be noted that laundering transactions may overstate the exact number. As of March 2019, USDC (Circle), Paxos Tokens and Gemini Tokens, and True USD, their total daily trading volume exceeds USD 138 million. That's about 90% of Venmo's average daily income of $ 158 million. In comparison, the average daily transaction volume of Tether during the same period is about 7 billion to 8 billion US dollars.

Figure 3: Market Cap of Stablecoin

This new set of trust coins has diversified their banking operations and established a collateral reserve relationship with more reputable banks. These include better bank records in the United States than banks designated to hold Tether dollar reserves. This has also led to the strengthening of third-party audit relationships-although still not a "Big Four" company, at least close to the top 50 auditing companies are willing to audit them

Importantly, these startups are portraying compliance by seeking permission to provide a level of credit similar to that of a banking entity. However, no agreement has yet been reached on which licenses consider stablecoins to be properly regulated.

Commodity currency

A stablecoin can be linked to a non-statutory asset or a basket of assets (such as cash securities or commodities). There are many types of assets that can support this type of coin, each with its own characteristics. For example, commodity coins can be backed by Treasury bills, high-quality liquid assets, or traditional tangible goods. However, this method will always involve a trusted custodian regardless of the asset. One example is Digix Global, which issues GDX tokens that can be converted into one ounce of gold.

Cryptocurrency

These are tied to the value of crypto assets or a basket of crypto assets. Since collateral supporting stablecoins is held on-chain, cryptocurrency issuers claim to reduce their reliance on third parties.

However, due to the volatility and risk of the base currency, this method is essentially speculative. Long-term price stability may be compromised, and the high correlation of cryptocurrency prices limits the benefits of a basket of coin diversification.

Cryptocurrency company Maker issued a significant stablecoin of this variety. The company issued a stablecoin DAI, which was later changed to SAI. DAI is an ERC-20 token, meaning it exists on the Ethereum network. The currency is collateralized by the Ethereum cryptocurrency. In order to deal with the risks of Ethereum, DAI must be over-collateralized. Although over-collateralization and hedging strategies can partially offset some of these risks, huge cryptocurrency price drops may still break this link.

Therefore, although this method is very creative, it ultimately failed the cryptocurrency fluctuation impact test.

Algorithm Coin

Algorithmically controlled stablecoins do not depend on collateral held elsewhere. Instead, they try to achieve stability by hard-coding a set of rules into the stablecoin itself, such as adjusting the supply of stablecoins to meet demand. In this way, the system is theoretically self-sufficient and does not need to establish links with existing monetary systems, assets and even other cryptocurrencies. This is a tool used by the central bank to manage sovereign currencies.

Basis attempts to maintain a 1: 1 USD exchange rate for Basecoin using a unique method that involves issuing three separate tools to motivate investors to purchase Base Share (when the price of Basecoin is too high) or Base Bond (when the price is too high) Too high).

Although some people still believe that algorithmically controlled stablecoins are a viable option to reduce the risk of counterparty or cryptocurrency assets in trust coins, bank coins and commodity coins, others are skeptical. It turns out that it is difficult, if not impossible, to eliminate risk.

However, the collapse of Basis has proven the fickle nature of creating currencies and maintaining their prices. Generally, this approach is highly speculative and raises questions about fair practices on how to ensure value, price stability and control.

Status of stablecoin

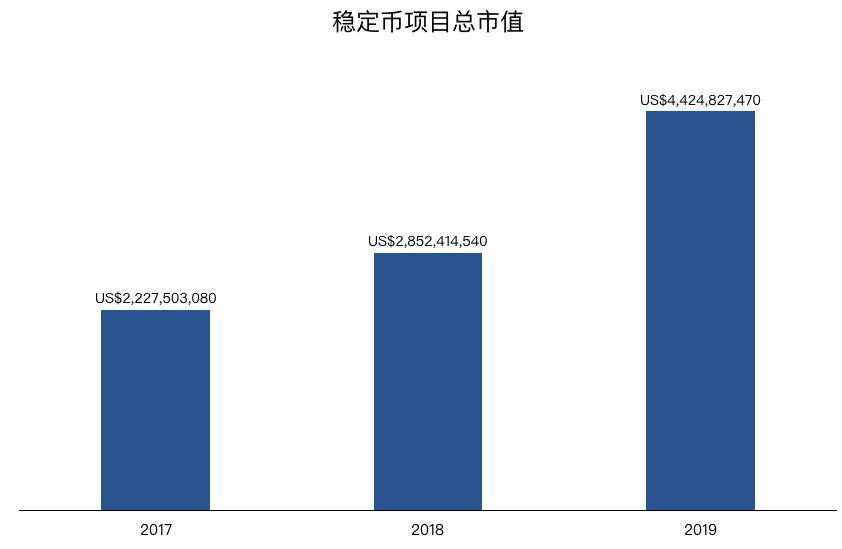

Since the emergence of stablecoins, the market size has expanded rapidly, with the total market value rising from around US $ 2.2 billion in 2017 to US $ 4.4 billion in 2019. Market value doubled.

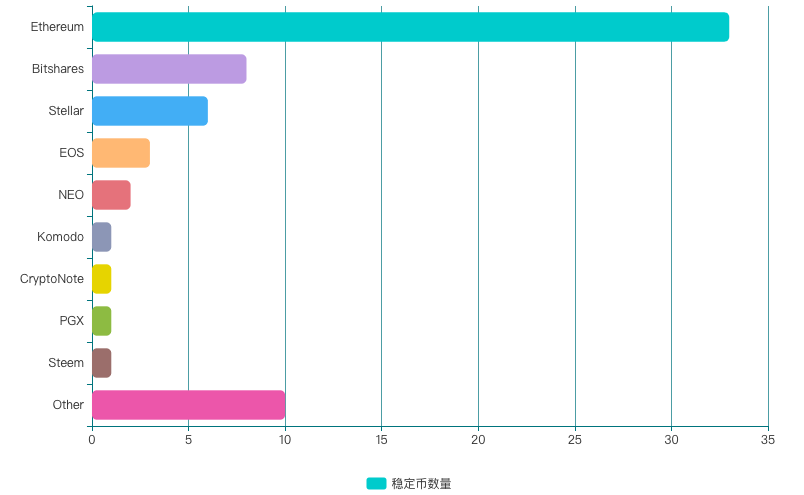

During the three years from 2017 to 2019, various stablecoins began to emerge, and the market entered a period of rapid development. Currently, there are 33 stablecoins in the Ethereum network, and Bitshares has become the second largest stablecoin platform, with 8 stablecoins in its network.

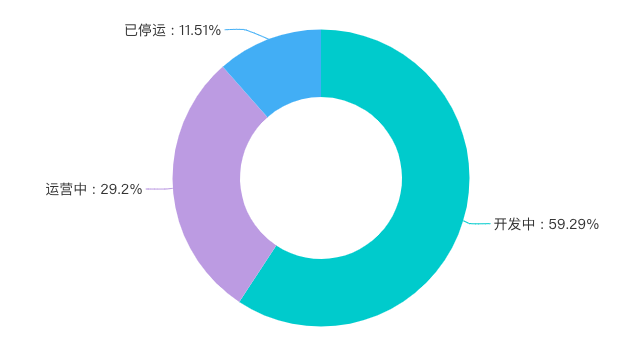

Although many corporate entities have announced stablecoin projects, as of the end of the third quarter of 2019, only 66 stablecoins have been listed, accounting for 29.2% of all stablecoins. There are 134 stablecoins under development, accounting for 59.29% of all stablecoins. Among them, well-known stablecoins launched by Basis have been discontinued, accounting for 11.51% of all stablecoins.

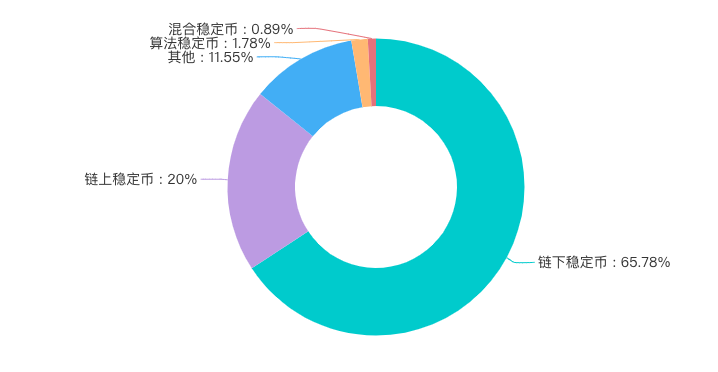

Of all the listed stablecoins, the off-chain stablecoins account for the vast majority, 65.78%.

Future trends

Stablecoins have found a suitable market in the cryptocurrency ecosystem. Specifically, they have been used to lock in gains made on the speculative cryptocurrency market, circumvent taxes and make certain payments without a bank account. Trust coins like USDT are the most commonly used. However, bank coins may soon compete with these coins. Bank coins have larger and wider application scenarios, and they also bring their own compliance and volume and gain some natural advantages.

First, this section considers some possible explanations to explain why the current use of stablecoins outside the closed-loop cryptocurrency ecosystem is relatively limited. The second part of this section looks at the applicability of stablecoins to established payment systems. To this end, we provide an overview of various existing payment systems. Third, we explore the situation where stablecoins can be improved on one of these systems or fill markets where the system is currently unable to reach, and identify issues that stablecoin issuers will face in the future.

Why is the current usage scenario restricted

There are various functional and non-functional considerations for business transactions that stable transactions cannot meet in the current implementation. It is worth noting that stablecoin's methods in terms of identity, privacy, and compliance are still immature, and many lack a reliable review process.

Immature regulatory approach: Regulated companies will not use cryptocurrencies or stablecoins as a settlement mechanism without considering the regulatory system or structure. Compliance with existing regulations is key. Although certain issuers have obtained specific regulatory permits, coverage is far from adequate. Ensuring the security of stablecoin transfers also means taking steps to screen individual participants and taking financial flow measures to detect and block suspicious activities, especially fraudulent activities.

No audit company endorsement: mainstream audit companies believe that the current stablecoin issuers are too risky to evaluate, so this task falls to the audit companies with poor reputation. The method of ensuring proof of collateral and reserves is still uncertain, and an audit report covering that information may not have the legality to provide a guarantee. In addition, Tether's choice to keep its financial statements private has made its funds more questionable. Collateral is often held by multiple decentralized entities, making it less reliable than the dollar reserves of large banks. These issues have led investors to question the legitimacy of funds custody and their ability to prove sufficient reserves.

Stablecoins issued by banks have clear advantages, as these institutions have adopted strong auditing measures to ensure proof of reserves in addition to their history of compliance and anti-money laundering practices. It is not too risky for legitimate third-party auditors, and current audits can be tailored in a very straightforward manner to these institutions that deal with stablecoins.

Lack of a formal institutional perspective: Issuers must understand how to use stablecoins to optimize designs for corporate or retail transactions. Existing payment systems are flexible enough to handle both cases, but the governance and execution of transactions differ based on who is using the network and for what purpose.

Private transactions are another area where retail and institutional customers have different requirements, because you can't ask companies to see transactions made public to all on-chain participants. A network that broadcasts all information to all parties is not suitable for business transactions, but this is an inherent characteristic of the public chain established by most current stablecoins.

In addition, financial institutions will strictly require KYC, and anonymity is a feature of cryptocurrencies. For most stablecoins, a legal identity is not required to be directly associated with the receiving address before sending funds. The architecture and supported platforms inherit the legal identity methods used by companies and financial institutions that are not regulated, and making changes to the architecture after the fact brings complexity.

How stablecoins adapt to the mainstream payment environment

Enterprises and financial institutions need blockchain-based payment systems to settle transactions they make on these networks. If stablecoins are to seize this opportunity, they must be consistent with the payment systems currently in use.

Currently, there are five main payment methods that we use daily: cash, credit card, ACH and wire transfer. Consumers and companies' preferences in terms of payment methods may vary greatly from country to country, but they are basically the same.

Although there are many factors to consider when looking at payment systems, this section will focus on who uses the payment system, its purpose, and the higher-level functions of the payment value chain. The applicability of the blockchain will depend on these factors and therefore will vary between payment systems. For example, wire transfers with large and small systems are most relevant to the blockchainization of digital payment services, and cash and credit cards are areas where blockchain is almost impossible to enable.

The difference between push and pull transactions is an extremely important perspective for viewing payment systems in the context of stablecoins, because stablecoins are a push payment system. Push transactions mean that the payment is initiated by the sender. Think about how your friends will give you the ownership of the money when they transfer it to you. On the other hand, the pull transaction is initiated by the receiver. Think of check transactions, where ownership depends on what you tell your bank to withdraw funds from the sender's account into the account.

Cash as a bearer, physical cash is the simplest form of push. However, unlike the cryptocurrency or stablecoin currently on the market, the issuance is controlled by the central bank under the government.

The central bank has conducted research on the retail-centric central bank digital currency, and if privatized and widely distributed, it has the potential to serve as a digital version of cash. However, such systems are currently under development.

Although there is no fiat currency support or denomination in fiat currency, digital currencies like Bitcoin are like cash and they are all secret assets. Similarly, neither system can be thoroughly reviewed, and no custodian intervention is required to prove ownership, redemption, or initiate payment. Libra's founder David Marcus once said that stablecoins can replace cash by solving the problem of Bitcoin's volatility, but this is unlikely because the existing stablecoins of fiat currencies exist as liabilities of companies or banks. are different.

card

Despite the wide variety of cards, all card networks are connected to a two-way value chain involving banks that help issue (customer) and obtain (commercial) payments.

Cards are not widely used in payments between businesses. At present, the most destructive enterprise blockchain application for traditional card payments will be a tokenized point model, which can be similar to a closed-loop network debit card payment. However, there are no successful cases of such a system, so it is not significant.

Small Amount Bulk Payment System (BEPS) + Large Amount Real-time Payment System (HVPS)

First, the Central Bank ’s large-value real-time payment system (HVPS) was put into operation in 2002. Its role is to process large-scale credits between the same city, remote places, and inter-banks of commercial banks (including a certain amount in the bank). Payment instructions are sent in real time, one by one, in full Liquidation of funds.

In 2005, the Central Bank ’s small batch payment system (BEPS) was put into operation. It is used to process debit payment services intercepted by paper vouchers in the same city and other places, and small credit payment services where each amount is below the prescribed amount. The net clearing fund mainly provides low-cost, large-business payment and clearing services for the society.

The transfer into and out of the bilateral current accounts held by each other's banks directly transfer funds; the two parties open an account in a third-party bank and the transfer is performed by the third party; the two parties transfer the funds through a reserve account opened in the central bank.

The complete payment process also includes three aspects: payment, settlement and settlement. The payment takes place between the payee, payer, and the bank that opened the account. The payer's book balance decreases and the payee's book balance increases; clearing is the process by which the receiving and paying banks exchange payment information and calculate the difference between the debit and credit according to the payment instruction; The account-opening bank and central bank involved in the payee's payer shall use the central bank to transfer the reserve account to settle the debt and debt relationship.

Settlement is the operation process of calculating, classifying and transmitting payment instructions, and funds have not been substantially transferred at this time. The settlement after the liquidation is the actual transfer of funds between accounts based on the liquidation results.

wire transfer

Financial institutions typically use wire transfers in situations such as settlement securities delivery or foreign exchange markets. Wire transfers are also used for international payments. The telegraphic transfer system is enhancing remittance capabilities to penetrate the supplier payment market. In some cases, individuals use wire transfers.

There are two wire transfer systems in the United States-Fedwire operated by the Federal Reserve Bank (Fedwire) and privately owned CHIPS. They function similarly and are initiated by the payer, who instructs the bank to irreversibly transfer the money to another account. However, they use different settlement methods, which has an impact on the risk and liquidity provided by each system. Fedwire is an RTGS (Real-Time Gross Settlement) system, which means that every transaction is settled as it happens and the balance is updated in real time. This greatly reduces the risk of bank failures in the system. On the other hand, CHIPS facilitates network connections between banks between 9 am and 5 pm. The CHIPS multilateral net settlement provides the market with more liquidity during the day, while the remaining funds are settled through Fedwire at the end of the day.

Development requirements for stablecoins

Since most transactions between companies are conducted through the central clearing house or wire transfer of the People's Bank of China, the stablecoin design must meet users' requirements for one or both of these two systems. There are two dimensions of adoption: the risk profile of stablecoins and how they integrate into existing (or new blockchain-based) payment scenarios.

Integration into payment solutions

There are various potential uses for stablecoins in each payment system. Below we provide a hypothetical example for each example.

Large and Small Amount System (HVPS + BEPS) Considering the existing use of large and small Amount systems as a means of payment between enterprises, large and small Amount systems are very important when considering the solution of blockchain applications (especially those involving physical transfer) . Companies with complex supply chains have conducted blockchain trials to manage shared transaction processes. In this case, stablecoins can eliminate the need to resolve off-chain through large and small systems. For example, a smart contract can be established that begins payment upon confirmation that delivery meets mutually agreed terms.

wire transfer

Stablecoins are often discussed as a substitute for wire transfers within financial institutions. In the cryptocurrency ecosystem, stablecoins help to instantly settle cryptocurrencies into fiat currencies. The connection is made via wire transfer, which is used in the area of regulated financial services to settle stock and foreign exchange transactions. Stablecoin offers a new feature-transfer assets 24 hours a day. However, functionality needs to come from weighing trade-offs, not simply slap your head. For example, a strictly set trading window is a feature of the CHIEFS architecture, not a loophole, enabling the system to focus liquidity during the day.

Risks of stablecoin

Future stablecoins also face some unresolved issues:

- Will future bank tokens continue to exist in isolation in issuing commercial banks? For example, JPM Coin and Silvergate Network: Coins can only be sent to account holders of the same bank.

- If banks issue and transfer stablecoins between them, how will they deal with directional risk exposure to competitors?

Conclusion

Just as multiple old payment systems coexist, there will not be a situation where "one stable currency applies to all countries and scenarios". One tool cannot solve all scenarios of global settlement. Instead, the method of mortgage and regulatory structure will depend on the specific use. Stablecoins may find value in a regulated financial system by providing a new niche market-providing value for blockchain-based applications.

In other words, they do not strictly provide value from the payment link, but bring benefits from the form of the ledger of the benefits (such as reducing friction, time costs, legal restrictions), or providing an additional payment in exchange for any other asset the way. Certain types of payments made with stablecoins may eventually have inherent advantages and disadvantages.

For example, a tokenized capital market ecosystem will prevent double spending from being separated from useful services (such as payments) provided by the custodian. This will reduce third-party bottlenecks and potentially enable new services. The stablecoin that will have the greatest success will help make payments across one or more blockchain scenarios that transfer a large amount of value.

Eventually, they may be designed to run on hosted applications and users' blockchain systems. Significant progress has been made in the stablecoin field. It is worth noting that stablecoins have paid more attention to regulatory and compliance measures. In addition, existing financial institutions are beginning to think about how these assets can enhance their existing products. I believe that the development of stablecoin features will continue and provide a series of products to support the various needs of trading parties.

risk warning:

- Beware of illegal financial activities under the banner of blockchain and new technologies. The standard consensus firmly resists the use of blockchain for illegal fundraising, online pyramid schemes, ICOs, various variants, and dissemination of bad information.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Viewpoint: Bitcoin gold has been attacked by double spending again, and nearly 7,500 coins have been lost. Is Bitcoin still safe?

- Assisting Wuhan, what can the blockchain do for public welfare?

- U.S. ambassador to Iraq hit, bitcoin surges over 4%

- Chengdu has 35 companies with blockchain technology research as the core and 298 related companies

- Financial institutions join the stablecoin trend: 2020 will be the year of the real stablecoin

- What can the blockchain do? What can't you do? | Back to common sense

- Deutsche Bank: Digital RMB will weaken US dollar's dominance in global financial system