Application and Research of Blockchain Technology in Cross-Border Payment

Introduction

Cross-border payment is an increasingly hot field in China's economy. With the continuous development of domestic consumption and domestic enterprises, cross-border payment has become an important opportunity for China's economic activity and development.

Current cross-border payments come in many forms, typically through cross-border transfers between banks and banks, through cross-border payments through Visa and UnionPay, and through third-party payment agencies such as Alipay. However, cross-border payment currently faces many problems, including high cost, high risk, high probability of risk interception by the payment institution, and long arrival period. These issues have been plagued by merchants and consumers, so the industry has long been exploring an effective solution until blockchain technology emerges.

The blockchain is a distributed data storage technology under a peer-to-peer network. The core of the blockchain is to achieve data consistency between nodes in a peer-to-peer network without third-party and centralized mediation. In layman's terms, in the absence of third-party notarization, participants in the network provide witnesses to the transaction and quickly announce to the entire network, which proves the truthfulness and validity of the transaction record.

The decentralization of the blockchain, the value of the original chain, and the nature of natural liquidation actually match the needs of the cross-border payment field. It is an important technology that can fully meet the needs of cross-border payment and realize the transformation of cross-border payment.

- Indian regulators have procrastination? The cryptocurrency ban has not been lifted, and the people took to the streets four times to protest

- Sound | The Treasure of the Crossing of the Bulls

- Babbitt column | Blockchain + Medical: A bridge to restore trust? (under)

Based on this idea, this paper constructs a cross-border consumption scenario, in which customers use French currency to purchase digital currency and transfer it to their digital currency wallet, paying the payment to overseas merchants through cross-border payment institutions, and the payment institution will quickly turn the customer's digital currency in the middle. Converted to the merchant's local currency and paid to the merchant. This process no longer relies on banks and card organizations, there is no high processing fee, there is no risk of being blocked by the risk of trading, and there is no risk of fraud, even real-time accounting, and there is no foreign exchange management. Government constraints such as mandatory foreign exchange settlement and foreign exchange exchange limits can solve the dilemma faced by the current cross-border payment industry.

In order to fully verify this idea, the author designed a complete implementation plan and implemented it to implement a cross-border payment platform based on blockchain technology, and will soon be put on the market.

This paper analyzes and demonstrates the status quo of cross-border payment, deeply studies the technical characteristics of blockchain, and combines the two to achieve a perfect solution for cross-border consumption scenarios from the perspectives of business logic, business scenarios, and technology implementation. Cross-border payment products based on blockchain technology for various problems.

Chapter One Introduction

Cross-border payment is an area that is becoming hotter and hotter after China's economic development has reached a certain level. With the promotion of domestic consumption and the promotion of domestic enterprises, and the continuous deepening and expansion of the “Belt and Road”, the Chinese economy External relations are bound to become closer and closer, economic and financial exchanges are becoming more frequent, and the internationalization of the RMB continues to advance. The field of cross-border payment has increasingly become an important opportunity for China's economic activity and development.

Cross-border payment is the action of domestic organizations and individuals to make payments abroad, involving domestic and foreign liquidation and settlement, and involves the conversion between different currencies. Cross-border payment includes cross-border receipts, cross-border remittances, settlement and sale of foreign exchange, etc., covering consumers from overseas “haitao”, Chinese products are sold overseas, and Chinese consumers are spending overseas.

This paper mainly analyzes the status quo and problems of cross-border payment, clarifies the types of existing cross-border payments, proposes the crux of improvement, and introduces the popular technology of blockchain to study its application value in the field of cross-border payment. And the meaning of the industry, the formation of effective solutions to the current problems and solutions, and the construction of a practical cross-border payment technology platform and business products based on blockchain technology, to achieve the default results.

Section 1.1 Cross-border payment overview and main issues

Cross-border payment has become an important financial field in the context of China's economic development. The market scale is huge, and the in-depth development of the “Belt and Road” is bound to further expand this scale. Faced with this inevitable trend, superimposing the development model of the Internet industry, just as traditional banks are challenged by Internet third-party payment, the traditional cross-border payment market is undergoing subversive changes, and Internet gameplay has joined this field. Bringing great challenges and changes to the traditional model. The rise of blockchain technology has further stirred up the industry and brought unprecedented changes, which will surely become a challenger in the future and shocking the field.

There are various forms of cross-border payment, ranging from inter-bank institutions to card organizations, as well as third-party payment agencies, such as:

● Cross-border transfers through channels between banks and banks;

● Cross-border payment through Visa, UnionPay and other card organizations;

● Pay through third-party payment institutions such as Alipay;

● Pay through third-party cross-border payment agencies such as pingpong.

At present, cross-border payment industry also has many problems due to insufficient competition and technical restrictions, including:

● High cost, even up to 3%;

● High risk and vulnerable to malicious fraud;

● The probability of being intercepted by the paid institution is high;

● The arrival period is long.

Section 1.2 Application Value of Blockchain Technology in Cross-Border Payment

The blockchain is a distributed data storage technology under a peer-to-peer network. The core of the blockchain is to achieve data consistency between nodes in a peer-to-peer network without third-party and centralized mediation. In layman's terms, in the absence of third-party notarization, participants in the network provide witnesses to the transaction, and quickly announce to the entire network, the entire network proves the truthfulness and validity of the transaction record, thus constructing technology. A rigidly guaranteed trust environment.

This technology was born with the popularity of Bitcoin. It does not require the characteristics of a third-party witness to ensure that no individual or organization can control the network, just to serve this kind of virtual currency that is not controlled by a third party. Produced and distributed. Although this technology provides the advantages of third-party mediation, technical rigidity guarantee, data cannot be falsified, and so on, there are also problems of low performance, huge resource consumption, 51% attack, and fork.

Specifically, Bitcoin allocates billing rights in the form of POW, which is proof of workload. By randomly selecting numbers to calculate hash values and requiring hash values to meet specific rule requirements, this completely random violence calculation can be guaranteed. Fair and random distribution of billing rights, while the cost of fairness, openness, and fairness is dependent on violent calculations, while competing with each other makes it more difficult to obtain billing rights and requires more computing power. In addition, this kind of violent calculation is not perfect to ensure that there is no possibility of obtaining the billing right at the same time, that is, two nodes may obtain the billing right by satisfying the system rules at the same time by random selection, which makes the concurrent billing happen, thus bringing The fork of the blockchain, and the subsequent abandonment of one of the chains in accordance with the bitcoin mechanism, resulting in the loss of all accounting information in this chain, and this defect directly led to the organization of more than 51% of the computing power It is possible to control the fork and discard the fork to launch the attack, which is also the main defect of the original blockchain public chain.

The industry has discovered the huge potential of the blockchain and has continuously improved its defects. On the one hand, this technology has gradually developed into a chain of alliances, multi-centered and manageable, and has made great progress in performance. It has become possible, on the other hand, the public chain and even around Bitcoin itself are constantly improving to avoid existing problems.

When this technology collides with the cross-border payment field, we can find that the decentralization of this technology, the value of the native chain, and the nature of natural liquidation perfectly match the application of this field, so the blockchain technology is An important technology that can fully meet the needs of cross-border payment and realize the transformation of cross-border payment.

Section 1.3 Implementing a cross-border payment product based on blockchain technology

Imagine a cross-border consumption scenario where customers use French currency to purchase digital currency, transfer it to their digital currency wallet, and pay the payment to the overseas merchant through a cross-border payment institution. The payment institution quickly converts the customer's digital currency into the legal currency of the merchant's location and pays it to the merchant. Merchant. Since it is not a legal currency, the network does not access the foreign exchange administration or other official institutions (trying to use the US dollar, RMB, etc. settlement, it is necessary to carry out through the US government or Chinese government-controlled payment channels, which is why the United States can swing the sanctions stick Because all international dollar payments are subject to control, such payments and transfers are completely outside the control of the state, government, and organization.

Therefore, this process no longer depends on banks and card organizations, there is no high processing fee, there is no risk of being blocked by the risk of trading, no political interference, no malicious refusal to commit fraud, or even Real-time accounting reduces the pressure on merchants' funds, and there are no government constraints such as foreign exchange management, mandatory foreign exchange settlement, foreign exchange exchange limits, and political risks. It is the best choice for consumers and merchants.

In addition, exchange risk can be minimized or even completely neglected through real-time legal currency exchange or acceptance of digital currency, which is also very attractive for merchants who often influence the exchange rate fluctuations.

The realization of all of this depends on the cross-border payment platform based on blockchain technology. This paper analyzes and demonstrates the status quo of cross-border payment field, deeply studies the technical characteristics of blockchain, and combines the two to achieve a perfect solution. A cross-border payment product based on blockchain technology for various problems encountered in cross-border consumption scenarios.

Chapter II Summary of the Status Quo of Cross-Border Payments

Cross-border payment is a hot area in the new era, so let's first understand what cross-border payments are, what types of cross-border payments, and what are the problems with cross-border payments that trigger us to change, thus forming a brand new technology and product. form. The core is between two or more countries and regions, because of the transfer of funds required by trade and investment with certain tools and payment systems [1].

Section 2.1 What is cross-border payment?

Cross-border payment is the transfer between domestic and foreign customers, and the payment between domestic and foreign customers. Because of the different currency and clearing house, it is necessary to use different settlement payment instruments in the same country to realize the transfer and liquidation of funds between the two places. , settlement, to complete a cross-border commodity transaction and currency payment, which can include the exchange of currency.

A typical case:

1. Domestic customers purchase goods at the foreign currency website according to the foreign currency price, and at the same time, pay the converted RMB amount through some payment institutions, and the domestic cooperative bank of the payment institution conducts the purchase of foreign exchange and conducts corresponding operations of the SAFE;

2. The overseas merchants confirm the payment success message of the payment institution and deliver the goods to the country through international logistics;

3. The customer confirms the receipt of the goods and sends a liquidation order to the payment institution. The payment institution will transfer the money to the merchant through the cooperative bank in accordance with the settlement agreement with the overseas merchant, in the form of the corresponding foreign currency.

Of course, this process is reversed. It is the same logic that overseas customers purchase goods from domestic merchants and pay for the payment of goods.

It can be said that cross-border payment has become increasingly important with the development of China's economy and is becoming an inevitable trend of China's economic development [2].

Section 2.2 Classification of cross-border payments

The domestic cross-border payment market can be divided into three categories according to the participants: bank cross-border payment, card organization, and third-party payment institutions.

Banks have long been the main agency for cross-border payment settlement, targeting individuals, businesses, and mainly cross-border remittances between individuals, through SWIFT (Global Interbank Financial Telecommunications Association) to handle cross-border payment settlement services. SWIFT is a privately held organization that has achieved a centralized cross-border payment capability by incorporating global banks into its network and was once in an absolute monopoly. SWIFT is characterized by high commission rate and low payment efficiency. It can only be remitted to payment within 3-5 days. On the other hand, it also has many advantages. First, it has high reputation and reliable quality. At the same time, there is a cap on the fee, which is suitable for large remittances. With payment. Due to its monopoly position, the world's major cross-border payments have relied on SWIFT for a long time, which has made the institution's high costs and self-renovation slow.

Card organization is the main cross-border payment institution, mainly for merchants and individuals. It is the main cross-border payment method in the consumer market. The rate is high, often more than 3%, and due to various fraud risks, card organizations often adopt monitoring and control. Means, but on the one hand, it is still impossible to avoid fraudulent cases, stolen and malicious refusal, but on the other hand, many normal transactions are affected by systematic errors.

Third-party payment institutions such as Alipay, WeChat Pay, Paypal, etc. are new forces in this industry. Due to different gameplay, they quickly occupy a considerable market share in a few years through low cost and attractive service.

We have analyzed and summarized the tools and methods of cross-border payment in recent years, and basically can divide the existing cross-border payment models into the following categories [3][4][5].

(1) Bank

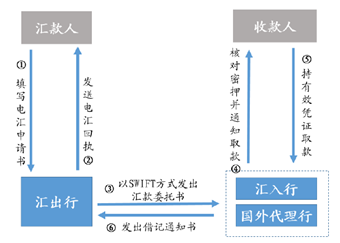

Banks primarily implement cross-border payments and settlements via wire transfers. The remitter is handled at the remittance bank, and the bank sends a message to the adversary bank by means of a telegraph, telex, SWIFT, etc., and the adversary bank pays the payee according to the content of the message [6][7].

The domestic application is more SWIFT channels. SWIFT is a cross-border payment and settlement institution between international banks. It has more than 4,000 member banks around the world. After applying for joining the institution, each bank will receive a SWIFT Code as its id for participating in the relevant cross-border payment settlement activities of the organization after the corresponding joint test and evaluation and board evaluation. The id is the unique identifier of the financial institution.

Due to its large organization and numerous members, SWIFT has gradually formed a large enterprise disease. On the one hand, the efficiency is extremely low. The specific performance is in applying for membership and remittance action. A new institution applies to become a member. From the application calculation, it includes interface development. Coordination test, acceptance assessment and other technical aspects of work, and then need to wait for the SWIFT high-level meeting approval, just waiting for the meeting time can be up to a month, and the sum of all working hours can exceed two and a half months. After that, you need to purchase a dedicated front-end hardware device to communicate with SWIFT. It usually takes more than 2 weeks for the equipment to arrive, for a total of 3 months. And specific to each business, it usually takes more than 24 hours to reach the other party's account. On the other hand, the cost is high, a cross-border remittance of 100,000 yuan, the cost of various calculations often requires more than 200 yuan, which makes the experience of such business through the bank is quite low.

Figure 2.1 SWIFT process

(2) Card organization

Card organization is the closest cross-border payment and payment institution for individual customers and merchants. Whether it is VISA, MasterCard, UnionPay, American Express, JCB, etc., there are always a few cards in the hands of individual customers. In Haitao and other scenarios, buyers often need to use these cards to pay the amount of consumption, and the merchants get the payment from the buyer through the clearing and settlement of the card organization. Cross-border payment through card issued by the card organization can be said to be the most important means and mode of cross-border payment between consumers and merchants [8][9].

The biggest convenience of the card organization is to support almost all banks and merchants. On the one hand, the card organization unites almost all banks. As long as the buyer has a bank account and handles the bank card, the card organization can make payment and settlement through the corresponding card organization. On the one hand, the card organization also lays out the acquiring network under the merchant lines, and supports the merchants' ability to accept bank card payment through pos and other equipment, thus achieving full coverage on the C and B sides.

Card organizations also have many problems, including high rates, high failure rates, and high fraud rates, which are elaborated in the next section.

(3) Third-party payment company

Third-party payments are emerging payment settlement agencies in the last decade, in a form similar to card organizations with customer accounts. After obtaining the payment license and cross-border foreign exchange payment license of the local regulatory agency, the third-party payment institution can legally carry out cross-border business such as payment, receipt, clearing and settlement [10][11][12].

The advantage of third-party payment institutions is that the cost is extremely low. For merchants, even pos tools can be used, and the handling fee is greatly reduced. For customers, the convenience of payment tools has also become an important selling point.

The main problem of third-party payment institutions is that the coverage of overseas offline merchants is still not high. Compared with the traditional card organization for decades of operation and expansion, the full coverage of third-party organizations has been completed for quite some time.

Figure 2.2 Process of a third-party payment institution:

Section 2.3 Major Issues in Cross-Border Payments

As mentioned above, traditional cross-border payment has always been realized mainly through banks and card organizations, especially for consumer scenarios. Currently, it is mainly implemented through card organizations, such as visa, mastercard, American Express, UnionPay, JCB, etc., and has maintained for a long time. Relatively stable situation. These names are familiar to the C-end consumers, and even because they can often get the wool from inside, they feel like they are happy and talked about it. In fact, the wool is on the sheep, the B-end customers bear the high cost, and of course they are passed on to C. On the client.

Traditional cross-border payment has solved many problems in cross-border consumption scenarios, but there have been many criticisms, mainly the following [13][14][15][16]:

1. High transaction costs. The transaction fee charged by the card organization is about 1.8%, and even higher than 3%. This rate is a very large cost for the retail industry, but it can only be accepted for a long time because of no choice. Generally speaking, the cost of card organization will be very high, but with the emergence of third-party payment and payment institutions, this rate has begun to decline. In fact, the rate of domestic payment has been very low, almost no profit. Space, which is also a direct result of the rapid development of domestic third-party payment. In the cross-border payment field, due to insufficient competition, this rate still has a relatively high profit margin. At present, with the emergence of Alipay, pingpong, etc., the initial form of price war has been presented, and there will be more and more Institutions join this competition, so adopting new technologies to reduce costs and increase efficiency becomes an inevitable choice.

2. The fraud rate and the rate of refusal are high. International credit cards have a 180-day refusal period. There is a risk of malicious refusal for merchants. Specifically, some individuals and groups can use this rule to purchase goods as consumers and maliciously after receiving the goods. The complaint, falsely claiming that the credit card was stolen, etc., refused to pay. At the same time, the card organization and the bank often favored the support of the customer in the general case handling, so that the merchant could not receive the loss of the payment. In fact, at present, there are indeed groups that use this rule to defraud the goods and then maliciously refuse to pay. The cross-border e-commerce is also frequently recruited. The success rate of appeals and arbitration is extremely low. Lost, this is a factor that is increasingly being considered by merchants when making cross-border payment options.

3. The transaction success rate is low. Due to factors such as supervision and anti-fraud, banks and card organizations in cross-border payment often set strict risk control mechanisms, such as requests from high-risk areas, suspicious multiple transactions within a single day, large transactions, etc. The transaction may be banned, and the payment institution further uses expert rules, machine learning, etc. to further enrich the risk rules. Once these rules are matched, a cross-border payment transaction is forcibly suspended. This is from the original meaning of good intentions, but in practice, due to technical reasons, business rules and other factors, it is often the case that a normal transaction is misjudged as a risky transaction and the situation is suspended, and the proportion of such errors is not low. In some cases, it is really irritating but helpless.

4. The return period is long. At present, the card organization has a mechanism of separation of transactions and clearing. The clearing and settlement of cross-border payment may take several days or even weeks, which directly leads to the inability of merchants to return money in real time, and the capital turnover rate is not high.

These problems are difficult to solve and break through under traditional technical conditions, because third-party organizations want to intervene in this field, there is a problem of customer trust, which serves as a technical and business threshold, and builds a wall for traditional institutions, only Alipay and other large Third-party payment companies have the ability to intervene in this area. However, with the emergence of blockchain technology, great changes have taken place in trust relationships, value circulation capabilities, and clearing efficiency. These technical and business barriers have gradually collapsed, bringing real meaning to the entire cross-border payment industry. The vibration on it.

Chapter III Blockchain and Its Business Application Value

Blockchain is a hot new technology application. After analyzing the characteristics, attributes and application scenarios of this technology, this technology is actually very applicable to various application fields in the financial industry, including cross-border payment.

Section 3.1 Overview of Blockchain Technology

The blockchain is a distributed data storage technology under a peer-to-peer network. The core of the blockchain is to achieve data consistency between nodes in a peer-to-peer network without third-party and centralized mediation. In layman's terms, in the absence of third-party notarization, participants in the network provide witnesses to the transaction, and quickly announce to the entire network, the entire network proves the truthfulness and validity of the transaction record, thus providing technical rigidity. A guaranteed trust environment.

This technology was born with the popularity of Bitcoin. It does not require the characteristics of a third-party witness to ensure that no individual or organization can control the network, just to serve this kind of virtual currency that is not controlled by a third party. Produced and distributed. Although this technology provides the advantages of third-party mediation, technical rigidity guarantee, data cannot be falsified, and so on, there are also problems of low performance, huge resource consumption, 51% attack, and fork.

3.1.1 Blockchain core mechanism

The technical core of the blockchain includes the following three aspects:

1, encryption system

The blockchain realizes data encryption in public situations through mathematically proven asymmetric encryption systems that are safe and reliable.

Asymmetric encryption is a kind of mathematical algorithm. By constructing a pair of data in a certain way, they are called public key and private key respectively. By calculating a string of characters through a private key, the digital signature of the string of characters can be obtained. The public key can decrypt the signature and verify if it is calculated by the corresponding private key.

The characteristic of this system is that anyone who does not have a private key cannot sign the text in any way and is unlocked by the corresponding public key, so in the case where the owner publishes his public key and keeps the private key properly, The digital signature calculated by the private key represents the owner's own recognition, and there is no possibility of forgery in mathematics.

This system is a technical guarantee that the transactions in the blockchain are not undeniable and cannot be falsified. The security system and trusted mechanism of the blockchain, especially the mechanism of tamper-proof and non-repudiation, are guaranteed by this algorithm. But at the same time, it must be pointed out that this is an encryption algorithm that is less efficient than symmetric encryption algorithms.

2, peer-to-peer communication

The biggest feature of the blockchain distinguishing from the traditional system is that it does not depend on the centralized system. Therefore, peer-to-peer communication constitutes the core of the blockchain communication mechanism.

In the traditional centralized service system, although the Internet and the LAN can completely exchange information in a peer-to-peer manner, they are all individual behaviors, as a public service such as news release, product transaction, payment accounting, etc. It is usually done on one or more central server nodes, and the client needs to connect to the central server to operate, thus forming a centralized star system.

Figure 3.1 Traditional Centralized System Architecture

The blockchain no longer has a service center, but all participants participate in an equal capacity, so a peer-to-peer communication method is adopted in the message communication.

Figure 3.2 Decentralized system structure

In this way of organization, a mesh-like communication structure is actually formed, which avoids the authoritative rule of the centralized node to the message, but enables the message to be quickly distributed in a point-to-point, decentralized manner at a geometric progression rate.

3. Consensus mechanism

The consensus mechanism is the core mechanism by which all participants can consistently record data under such a mechanism with no centrality and no authority. In layman's terms, in the blockchain system, in the absence of a middleman or a third party, a mechanism or algorithm can be used to achieve a consensus for all participants to jointly record the same data.

In the public chain system such as Bitcoin, the POW (workload proof) method is usually used, that is, the privilege calculation problem is used to obtain the accounting authority (these are the meanings of the three words "workload"), and then the whole network The broadcast is recorded by each node, and each node is ensured to be consistent, and some nodes that are maliciously falsified can be identified. In the alliance chain system, the consensus mechanism is generally implemented by the Byzantine algorithm. Since this article is not a technical article, it does not discuss the strong mathematical and logical proof of Byzantine algorithm, and the reader can verify it by himself.

3.1.2 Development of blockchain

Because there are many drawbacks in the public chain similar to Bitcoin, including the possibility that there will be forks and some records are legally discarded, it may be because some people master 51% of the computing power and deliberately create a fork to attack the blockchain platform, and Very certain non-environmental features with high power consumption, but also due to its own mechanism problems, there are defects in low accounting efficiency: 7 bills per second, 10 minutes delay, these are not directly applicable to business scenarios. the elements of. Therefore, the blockchain gradually evolved into a system of alliance chains. Compared with the public chain, the alliance chain adopted a completely different consensus mechanism and access mechanism, which completely solved the bifurcation problem and solved the 51% attack problem. The high energy consumption, while the performance is greatly improved to record 100 million records per second, the delay is less than 0.3 seconds, which makes the application of the blockchain in the industry possible.

Therefore, the blockchain is now developing in two directions. First, it is aimed at the huge potential of the blockchain, and its defects have been continuously improved, making this technology gradually develop into a chain of alliances, multi-centered, and manageable, and The performance has made great progress, making commercialization possible, and has become a part of reality; the other is to further improve the traditional public chain. After all, the public chain is the original form of the blockchain, and its open feature is the alliance chain. What is not available, so the public chain is also constantly developing to meet market demand, such as Bitcoin Improvement Proposal (BIP), so that digital currency such as Bitcoin can support more applications and have more Good characteristics, producing industry application value.

The above two developments are actually of great significance to the development of the topic described in this article, namely cross-border payment:

1. The development of the alliance chain is the basic technical form of some cross-border payment institutions, including, for example, R3 of most major banks in the world;

2. The continuous development of the public chain technology itself makes the use of digital currency as an intermediary for the efficiency and security of cross-border payment, which makes the digital money carrier used in this scheme practical in commercial scenarios.

It can be said that the continuous development of different forms and systems of blockchain makes cross-border payment really technically ready.

Section 3.2 Overview of Digital Currency

Speaking of the blockchain, I have to say digital currency, because the blockchain technology itself was born to build digital currency. At that time, in order to design and implement a currency that was not controlled by the centralized government and institutions, Zhong Bencong invented such a new technology application model that combines many traditional technologies, namely blockchain technology, and based on this technology creation. The world's first digital currency, bitcoin, has gained wide acceptance on a global scale because it is not controlled by any organization or individual.

As a technology to support currency, the blockchain must solve at least two major problems of bitcoin issuance and payment circulation. Here are several key links:

(1) Bitcoin account

The Bitcoin account is a string of characters corresponding to the public key address in the public-private key pair. It is used to express an account. Payment and collection are performed through this string. The payment information recorded in the blockchain book is Contact information between two accounts. Correspondingly, the private key corresponding to the public key is held by the account owner and is used to operate the account.

(2) Bitcoin circulation

When Bitcoin is paid, the payer will pay a certain amount of Bitcoin from the account to the other party's account. This action is signed by the private key held by the payer and broadcasted to the blockchain network, and the accountant record is obtained. , dissemination, and network-wide confirmation to achieve the end of a payment. In order to implement the mechanism of going to the third-party intermediary, the blockchain network does not have a central node to record this payment action. Therefore, the landing record of this payment needs to be temporarily selected by the blockchain network to record a node record, and broadcast and synchronize to all. node.

At this time, the miners appeared. The so-called miners are actually the nodes responsible for recording in the blockchain network, but because the accounting of which node is temporarily determined, the miners need to obtain the accounting authority through competition. The way to compete is very simple, is to generate a random number according to the rules, this random number requires that several bits before the hash value be 0. Since the Hash algorithm is a one-way algorithm, the number A can be hashed by the number A, but the reverse is not able to push A from A'. Therefore, the generation of this random number is completely dependent on the blind guessing and calculation of the computer, that is, only violence. Calculations, the calculation process is very painful, so it is unpredictable who gets it in the end. Firstly, the node that obtains the required random number will obtain the accounting authority, and pack and record several transaction information waiting for the record into the block, mount it to the end of the blockchain, broadcast to all nodes to synchronize through the P2P mechanism, and obtain several After the node responds to the confirmation, it is considered that the record is successful, and then the whole network waits for the birth of the next accounting node. This mechanism is called a consensus mechanism.

Because this kind of accounting is very time-consuming and power-consuming, the blockchain platform gives a few bitcoin rewards to the accounting work of the accounting node, which is also the source of the term miner, just like the hardworking miner has dug the mine. .

(3) Bitcoin generation

Finally, Bitcoin is generated because Bitcoin is generated in the circulation, which is the reward of miners when mining. Except for the first bitcoin issued by the creation block itself, all other bitcoins are derived from the blockchain system rewards at the time of billing.

The total number of bitcoins is limited, at around 21 million, which is guaranteed by a mathematical approach by continually reducing the production halving mechanism. As a kind of virtual asset with a limited amount, it is the first thing that it is not suitable as a legal tender, because the first law must have a rhythm controllable, which can reflect economic policies, and the second must match the production of social goods, avoid inflation and deflation. The mechanism for the limited amount of bitcoin is obviously not in line with it. But as a general equivalent exchange, or bulk commodities, Bitcoin is still fully competent. Therefore, in cross-border payments, Bitcoin is a basically qualified exchange symbol.

Section 3.3 Application Advantages of Blockchain

Based on the above mechanisms, blockchain technology provides a trusted network that does not require third-party central accounting and has the following characteristics:

(1) All transaction information is recorded by the temporary selection node of the blockchain network, without a third-party center, and is not controlled by individuals or organizations;

(2) The data of all nodes can be synchronized, and the failure of individual nodes does not affect the whole system, and all data can be recovered from the system at any time;

(3) All transactions are signed and cannot be tampered with.

Cross-border payments under blockchain technology abandon transit banks, enabling point-to-point fast and low-cost cross-border payments. Bypassing the intermediary bank can realize all-weather payment and instant payment, and save a lot of handling fees while accelerating the transaction progress. In addition, the de-centralization of blockchain, the inability to tamper with information, and anonymity have strengthened the security, transparency and low-risk nature of cross-border payments. The blockchain is not only an idea, but also gradually moving towards reality. Blockchain technology has different levels of cross-border payment solutions. It is small enough to use digital currency as an intermediary for foreign exchange, and to provide a decentralized global remittance system by providing technical support and underlying agreements to banks to replace the traditional costly SWIFT channel. The blockchain is not only an idea, but also gradually moving towards reality.

In summary, the blockchain provides features such as decentralization, trustworthiness, non-tampering, traceability, etc. As a financial industry application, it is more appropriate to use it in a scenario where no authority is a middleman.

Section 3.4 Application areas of blockchain

The blockchain is now widely used in various industries, as shown in the following figure:

Payment field: The transfer of funds through blockchain technology, especially in the cross-border payment business, the outstanding advantages, the establishment of direct interaction between multinational payers, simplify the process, real-time settlement, improve transaction efficiency, reduce business cost. In this area, for example, in the aforementioned R3 Alliance, a large number of global banks have established a cross-border inter-bank transfer remittance platform; for example, China Merchants Bank, the construction of cross-border payments before the port.

Supply Chain: Blockchain technology helps to improve the efficiency of supply chain management. As data is transparently transparent among the parties to the transaction, a complete and smooth flow of information is formed throughout the supply chain, thereby enhancing the overall supply chain management. effectiveness. The supply chain is currently a hot area, and banks have joined this field to extend traditional advantages, such as the Zheshang Bank's receivables chain, which is used to open up receivables between upstream and downstream of the supply chain, and to pass the credit of core enterprises; Internet companies For example, Lianyi Rong also joined this blue ocean and used blockchain technology to build a supply chain platform to solve the problems of high cost of financing risks, high operating costs and high efficiency costs.

Securities: Integrate equity into the blockchain and become a digital asset. It is possible to initiate transactions without intermediaries. Assets can be issued in a confidential or public manner as needed. The NYSE began experimenting with blockchain technology in securities trading as early as 2015. On the other hand, the ICO, which emerged in 2017, is using Ethereum to build a virtual digital token platform to issue its own shares (ie securities). . Of course, ICO proved to be a failure in China, but for the technology itself, it can be said to be a fairly successful application scenario and case.

Figure 3.3 Blockchain application overview icon

Bill financing: Based on the blockchain technology architecture, a new digital ticket business model is established. With distributed high fault tolerance and asymmetric encryption algorithms, the decentralized transmission of bill value can be realized, and the dependence on the bill trading center in the traditional business model can be reduced. degree. At present, many domestic banks and third parties have publicly exhibited blockchain bill financing businesses, such as Zheshang Bank, Weizhong Bank and other banking institutions, such as Shenzhen Qianhailian Yirong and other Internet companies.

Copyright protection: Using blockchain technology to integrate all links in the cultural industry chain, accelerate circulation, effectively shorten the value creation cycle, and authenticate the works through blockchain technology to prove the existence of works such as text, video and audio. To ensure the true uniqueness of the ownership. At present, micro-copyrights, original treasures and other products are online.

Trading: In the real estate trading market, there is a lack of transparency, cumbersome procedures, fraud risks, errors in public records, and the application of blockchain technology to record the loss of liens on land ownership during the trading period and post-trade processes. And tracking and ensuring the accuracy and verifiability of relevant documents. For example, the Swedish Land Registry has begun to use the blockchain for land registration, and the “four network interoperability” project in Hunan, China has adopted the same approach.

Health: Healthcare organizations face the problem of not being able to share data securely across platforms. Establishing good data collaboration among healthcare providers can help improve diagnostic accuracy, improve treatment outcomes, and reduce healthcare costs. For example, MIT's MedRec project, Ali Health is also working on similar projects in the country.

Traceability: The data stored in the blockchain is highly reliable and cannot be tampered with, and is naturally suitable for use in social welfare scenarios. Relevant information in the public welfare process, such as donation projects, fundraising details, fund flow, and feedback from recipients, can be stored in the blockchain to help the healthy development of social welfare. There are also many applications in this area, including the safe traceability of Jingdong's food sold on its own platform, and the traceability of Haitao's products by Tmall International.

Government affairs: “Using blockchain technology for data management and linkage, allowing relevant departments to directly query relevant data in real time, and then through process optimization to achieve data linkage and improve the efficiency of government processes. In government affairs, blockchain is due to its credit value. It has been closely integrated with the “running up to once” advocated by the Chinese government, and is currently being piloted in Hangzhou and Foshan.

Section 3.5 Blockchain and Cross-Border Payments

3.5.1 What does the blockchain bring to cross-border payments?

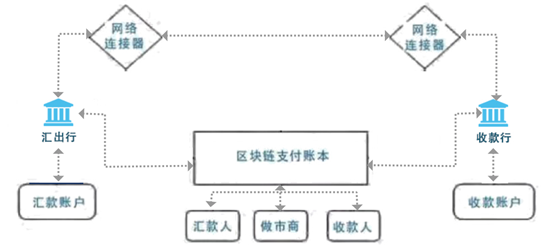

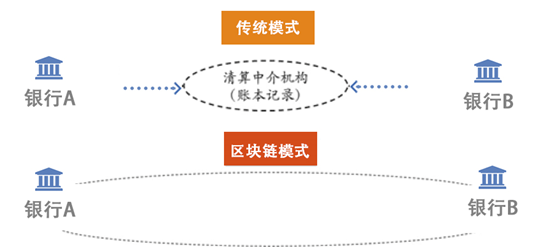

Current cross-border payment settlement As mentioned above, many links need to be implemented by a centralized organization, and there must be a trusted organization. At the same time, it takes a long period of time, high procedure costs, frequent fraud, and high rejection rate. For example, according to different regional remittance periods, it can be as long as 3 days, which is quite high for the cost of capital use. The application of blockchain technology can jointly build a cross-border payment system for banks, foreign exchange dealers and payment institutions into a blockchain cross-border payment system, forming a decentralized natural trust and value transfer platform, which can completely eliminate the need for intermediaries, trust institutions, and third parties. A cross-border payment system is implemented in the organization's scenario.

3.5.2 How digital currency combines cross-border payments

With the advent of digital currency and blockchain technologies such as Bitcoin, cross-border payment based on blockchain can link the flow of digital assets on the blockchain with the legal currency in reality, and convert legal currency into blockchain. The digital assets, and thus complete the cross-border flow of funds and value.

With digital currency or legal currency as the medium of exchange, the current cross-border payment application of blockchain has the following exploration paths: First, the decentralized payment and clearing organization represented by R3 will realize the alliance organization among banks and realize the inter-bank organization. The second is the Ripple, based on the original digital currency to build a cross-border payment alliance chain network; the third is based on SWIFT, based on the original centralized network and member base for the blockchain model transformation; The third-party payment represented by Alipay blockchain project; the fifth is the financial institution represented by China Merchants Bank and VISA, which builds a cross-border payment alliance chain network. The latter two models use French currency as the settlement tool and no digital currency. As a medium of exchange.

3.5.3 Application Mode 1: R3

The R3 project is by far the largest international inter-bank blockchain alliance, with support from dozens of financial institutions and millions of dollars in financing. R3's contribution to the blockchain application comes from bringing together a number of financial institutions and providing a mechanism for mutual cooperation, while creating the infrastructure, the blockchain bottom-level platform, the Corda project. Corda announced open source on November 30, 2016, and all participants can build their own blockchain applications based on this platform.

It is conceivable that with the participation of financial institutions, the Corda platform will more support financial applications, and cross-border payment is actually one of the most popular applications.

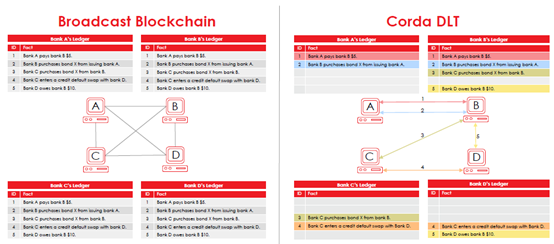

Corda is built according to the concept of "distributed ledger", which is a distributed database with decentralization and trust. The difference between this and the simple distributed database is that distributed database is only the storage mechanism of data is distributed. Its ability to control, ownership, add, delete, and change is still completed by a centralized organization or organization. The main solution is the parallel access, high availability, and high reliability of data. The distributed ledger is transformed from the ownership and use rights of the data. The data of each node is completely consistent, but the owner is different. Each node is a private database. The data is realized by the consensus mechanism between the database and the database. Mechanisms such as consistency, trust relationships, error detection and correction. Therefore, the two are fundamentally different, which is the core or most important technical contribution of R3 in the whole project.

There are of course many implementations of distributed ledgers. Blockchain is just one of them, and it will not be the best one. The best will always be tomorrow, and there will be more implementation technologies in the future. But for now, blockchain technology is still a popular and generally accepted method.

Corda was born to meet the financial institution's trading scenarios. Its system includes account-based state design. For example, Ethereum and other platforms also adopt this design idea. The so-called transaction-based state design is actually a link that constructs a transaction with a directed acyclic graph (DAG) to form a specific data structure. The transaction and the transaction are connected in series by input and output to become a transaction chain. This structure is different from the bitcoin data structure of the classical blockchain theory. There is no "chain" structure of "blocks", but in fact, its decentralized characteristics are still guaranteed. This is also a model for realizing the value of blockchain in a non-blockchain technology in a strict sense.

Notary is the core mechanism for verifying and confirming changes, or a quasi-consensus mechanism that replaces the normal blockchain model: a non-completely trusted or semi-developed network, where participants and nodes are not joined as if they were randomly connected to the Bitcoin network. Rather, it requires review and licensing and constitutes an independent "chain" that is not linked to each other, so it targets the transaction across accounts.

Figure 3.4 Corda basic logic

The basic goal of Corda is to establish a “decentralized” database, and to improve the concept and mechanism of the traditional blockchain system. It is to combine its own goals, make corresponding choices, improvements and innovations, and at the same time realize the appropriateness of information. Visibility, high system performance and connectivity to the real world.

The common blockchain consensus and broadcast process are as shown on the left. All nodes hold the same data. Each node contains every transaction data. Corda only keeps the data related to its own participants, and does not retain the full amount of data.

Figure 3.5 Schematic diagram of a typical transaction of Corda

The above picture is a typical transaction based on Corda. Participants use the smart contract to realize transaction registration, transaction registration public key, status and other elements.

Section 3.5.4 Application Mode 2: Ripple

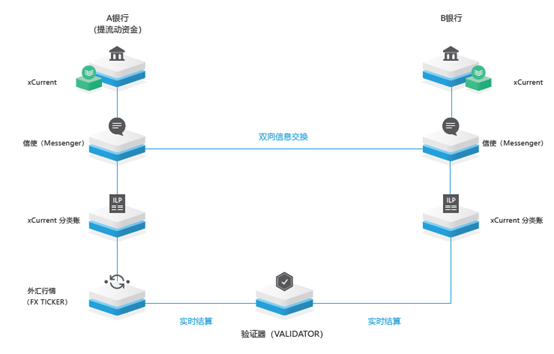

Founded in 2012, Ripple has built a blockchain technology to achieve cross-border payment and remittance capabilities, and has built itself into a financial services company that stands at the forefront of the blockchain. The company's cross-border payment remittance is characterized by a decentralized mechanism of blockchain, implemented in a centralized clearing manner.

Ripple's cross-border payment network mainly involves market makers and banks. The market maker declares the transaction price to Ripple, and the bank's collection terminal submits the information, price, terms and period of the transaction to Ripple. Ripple automatically combines the bank to the best-priced foreign exchange market maker, and the market maker is responsible for the transaction. Exchange and settlement between the two currencies. Ripple's business goal is to become a cross-border payment remittance organization led by blockchain technology.

Ripple is also a distributed, decentralized exchange mechanism. By establishing a distributed ledger and a digital currency XRP based on this blockchain system, a centralized exchange established by decentralization mechanism is constructed.

Figure 3.6 Ripple basic logic

Messenger is a messaging middleware that connects to the receiving bank, encapsulates messages, transmits information, prices, terms and cycles, and provides high transparency for transaction costs. Under this mechanism, both parties to the transaction can find errors in the message, thereby reducing the failure rate of transaction information transmission and transaction processing.

Each payment has a payment ID that can be used to query the payment status at any time during the payment execution, including during or after the funds settlement, to more effectively troubleshoot failed or delayed payments. Payment data exchanged with Messenger can be used to meet specific regulatory needs and other enhanced services in jurisdictions. Messenger utilizes Transport Layer Security (TLS) v1.2 for secure communication with existing banking systems, partner Messenger, and xCurrent's ILP components.

A validator is a component that confirms the success or failure of a transaction. It coordinates the flow of funds on the xCurrent ledger by eliminating all settlement risks and minimizing settlement delays.

The xCurrent ledger is the ledger of the transaction. The role of xCurrent is to continuously verify transaction information and to ensure transactional integrity of transactions.

FX Ticker is a release component of the price of foreign exchange transactions, mainly to ensure that the price data is really reliable.

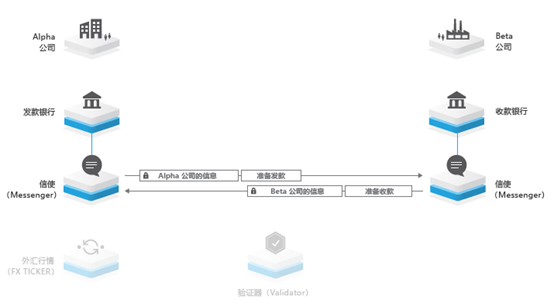

Cross-border payment case study: Alpha pays a cross-border payment of 100 Euros to Beta. Alpha has an account with a bank in country A, and Beta has an account with a bank in country B.

Figure 3.7 Ripple's typical transaction diagram 1

1. The payer initiates the process by providing information about the payment in the bank client application (which may be part of the existing online banking system). This information must include at least the following: payer, payee, payer amount/currency, payee amount/currency, etc.

2. The payment bank sends the request for quotation to the receiving bank to receive the portion of its payment that belongs to it, including its fee and empty fields, indicating any additional information required by the receiving bank to process the payment.

3. The payment bank obtains the foreign exchange rate issued by the liquidity provider from the foreign exchange market component.

4. The payment bank derives its portion of the payment, including its cost (in the example, $5).

5. The payment bank receives a response to its request for quotation and passes the quotation to the initial payer to determine the payment terms (including the fees of the receiving bank and the paying bank and the foreign exchange rate) are acceptable.

6. If the terms and additional payment information are acceptable, the receiving bank will issue a request to lock the quote. A locked offer indicates that the parties intend to process the payment and deliver the funds as described in the Payment Contract field. The contract field cannot be changed after the quotation is locked.

7. The payment bank receives the notification that the payment is now locked and updates the payment status in its database to reflect the new status.

Figure 3.8 Ripple's typical transaction diagram 2

After the two banks accept the offer, the paying bank can initiate an end-to-end payment, which consists of three sub-payments:

● Send payment: The internal bank transfer of the payment bank. The paying bank deducts the money from the payer's account and deposits it into its own separate account. In this transfer, any fees charged by the paying bank are deducted from the payer's account.

● Settlement Payment: The transfer funds are transferred from the payment bank's trading account (its xCurrent ledger) to the receiving bank's trading account by cross-bending this agreement. When the paying bank issues a sub-payment request, the transfer is automatically initiated. Performing a settlement payment does not require the payment bank to take any other action.

● Receive payment: The internal bank transfer of the receiving bank. The receiving bank lends its own separate account and credits the payee's account. In this transfer, any fees charged by the receiving bank are deducted from the payee's account.

Performing end-to-end payments involves the following steps:

1. The payment bank performs an internal book transfer, deducting the funds from the payer's account. In the example above, $125 was deducted: $120 for payment and $5 for payment bank charges.

2. The payment bank sends a request for payment to Ripple to confirm that the funds have been deducted from the payer. Requests to Ripple do not affect the bank's internal systems.

3. The payment bank notifies the receiving bank that the funds have been deducted.

4. Submit a payment request to initiate settlement payment, and transfer funds from the payment bank's ledger to the receiving bank's ledger by cross-accounting this agreement.

5. The payment bank notifies the receiving bank that payment has been made.

6. The receiving bank confirms that the transfer has been verified by the Validator and has been internally cleared, and the funds are settled to the payee.

7. The receiving bank submits a payment request to change the status of the payment to success.

8. The receiving bank informs the payment bank that the funds have been delivered to the payee's account.

9. The payment bank will change the status of the payment to success.

At this time, both parties believe that the payment is completed. Alpha remitted $125 and 100 euros was remitted to Beta's account.

Figure 3.9 Ripple's typical transaction diagram 3

3.5.5 Application Mode 3: SWIFT

At present, most countries and most banks in the world use SWIFT (Global Financial Inter-Telecommunication Association) to achieve cross-border settlement. In July 2017, SWIFT launched the Blockchain Proof of Concept (POC), a new standard for cross-border payments. The purpose of the blockchain test was to enable banks to adjust their international accounts in real time.

Figure 3.10 SWIFT basic logic

According to the assumption, blockchain technology can realize real-time capital account entry, rate reduction, reliable status inquiry and transmission of various types of information, real-time monitoring of current account circulation, and forecasting customer capital requirements. The blockchain platform developed by SWIFT combines HYPERLEDGER FABRIC 1.0 and “KEY SWIFT ASSETS” to design access rights for cooperative financial institutions to ensure reliable and secure data. At present, more than 20 banks have participated in the testing of this project, and Bank of China and Industrial and Commercial Bank of China have also participated in related work.

3.5.6 Application Mode 4: Alipay Blockchain Project

The Hong Kong version of Alipay Alipayay is based on the e-wallet-based blockchain cross-border remittance service, and its users can transfer money to GCash users in the Philippines through blockchain technology. The main process is as follows:

(1) AlipayHK users transfer money to GCash users in the Philippines via mobile app. The currency is Philippine peso (currently the minimum limit is 500 pesos), and the Hong Kong dollar purchase is made through Standard Chartered Bank Hong Kong. After successful purchase, the transfer order is registered to the blockchain. Node, after the consensus is successful, synchronize to all nodes;

(2) GCash polling obtains the latest block number of the blockchain, finds that the transaction details are read after the update, updates the GCash database, and pushes the account information through the app or SMS;

Figure 3.11 Alipay basic logic

(3) After receiving the credit information, the GCash user can use the GCash wallet to purchase or withdraw it at the ATM;

(4) AlipayHK performs two blockchain reconciliations at 12 o'clock and 24 o'clock every day, and registers the unregistered transactions in the blockchain to be registered, and synchronizes all nodes in the blockchain through the consensus mechanism;

(5) Standard Chartered Bank Hong Kong exchange funds after the regular exchange with the Standard Chartered Bank Philippines for cross-border liquidation, after the completion of the funds into the GCash reserve.

According to statistics, Ant Financial has applied for 90 blockchain patents, accounting for 10% of the current global blockchain related patents.

3.5.7 Application Mode 5: China Merchants Bank

China Merchants Bank also began to use cross-border payment remittances by using blockchain technology. With its advantage of having Hong Kong's wholly-owned subsidiary Wing Lung Bank, it has realized common-sense application of cross-border payment between the Mainland and Hong Kong.

On February 24, 2017, China Merchants Bank announced that it has applied blockchain technology to cross-border direct settlement, global account unified view and cross-border capital collection in the global cash management (Global Cash Management) field. Scenes.

In June 2016, China Merchants Bank adopted the POC experiment of cross-border direct-link clearing business, and took the lead in implementing the blockchain technology in the core system of the bank. After half a year of stable operation in the simulated environment, China Merchants Bank plans to be in the head office, Hong Kong branch and Wing Lung Bank recently. Cross-border direct-link clearing business through the blockchain technology transformation between the three sides of the strait will be officially commercialized.

Figure 3.12 Basic Logic of China Merchants Bank

3.6 Main challenges and countermeasures

3.6.1 Digital asset storage

Digital assets currently mainly refer to digital currencies based on public chains, such as Bitcoin and Ethereum.

Digital assets currently generally have two forms of preservation:

1. Use a digital currency wallet. At present, mainstream mainstream such as ImToken, AToken, etc., this wallet is actually a tool to help manage private keys and display, the biggest advantage is that the digital assets can be completely controlled in their own hands, without any outside control. Of course, due to the characteristics of digital currency and public chain, this method of preservation requires that the private key be fully managed. If it is leaked, it will be stolen by others, and no one can help to retrieve it. On the other hand, lost and forgotten the private key. These digital assets will be completely lost and can no longer be manipulated, and no organization or individual can help find them. So if you can manage the private key effectively, then using the wallet is a very safe and reliable way, otherwise it will be vulnerable.

2. Keep it on the exchange. Almost all digital currency exchanges support the introduction of digital currency, which is to keep digital currency on the platform. For trusted platforms, it will help customers to register, keep digital assets, and have the means to retrieve their logins and passwords, but for unreliable platforms, the digital currency that customers are entering will also pose a significant risk. In addition, theft of exchanges has also occurred frequently.

So in general, there is no perfect way to preserve digital money, especially in the digital world where government power cannot be intervened. The cost of digital assets not being controlled by the government is also not protected by the government. For many users, this is a major challenge, and in fact, it is also a problem that is currently not circumvented.

Therefore, this problem can be effectively managed mainly by using the mnemonic, exporting and keeping the private key, and using the wallet reasonably and correctly. Of course, it does not rule out that there will be better ways to help customers keep digital assets.

3.6.2 Digital asset price fluctuations

Digital assets as a tool in the payment process, its currency value is also the stability of the price is of great significance.

As a cross-border payment institution, using digital currency for cross-border asset circulation, what impact will it have if price fluctuations occur during this circulation? As a general understanding, digital currency is only an intermediate tool, why it has an impact. In fact, for digital currency such as Bitcoin, the confirmation process in the payment process takes several minutes (usually around 10 minutes), and these minutes are often It will be accompanied by currency fluctuations and even large fluctuations.

For example, a customer needs to remit 100,000 yuan to the foreign exchange, assuming 0.1% of the handling fee, and can also charge a service fee of 100 yuan for cross-border payment. Using bitcoin as a payment instrument, the following possibilities may exist:

1. If the value of the Bitcoin remains stable during the payment process, the net income of the transaction is 100 yuan, excluding various operating costs.

2. If the value of the Bitcoin appreciates by x% during the payment process, the net income of the transaction is 100+100000*x%, excluding various operating costs.

3. If the value of the Bitcoin value drops by x% during the payment process, the net income of the transaction is 100-100000*x%, excluding various operating costs. Obviously, if x>=0.1, the deal will not only have no money to make, but also lose money.

Figure 3.13 Bitcoin fluctuations

This is the bitcoin 1-minute K-line on the morning of September 13, 2018. It can be seen that the fluctuation of Bitcoin is quite fierce. The issue of currency value is an important issue in reality, and it is related to whether the payment institution will suffer significant losses.

To this end, a DCC mechanism is introduced. DCC, which is a dynamic currency conversion, is widely used in the cross-border payment industry. It is a mechanism provided by DCC to convert the price of commodity foreign currency into the price of the local currency. It provides the customer with the local currency price of the commodity directly, and collects a certain fee from it. When exchange rate prices fluctuate drastically, DCC companies are required to bear the corresponding risks. When exchange rate prices remain stable, DCC companies will benefit from them.

Through this mechanism, it is possible to show the customer a stable currency value, that is, the final price, and solve the problem of currency fluctuation of the client. On the other hand, the payment institution itself needs to adopt a series of means to avoid its own risk. Payment agencies can use the following means to solve the problem:

First, to obtain accurate and real-time quotes as much as possible, you can take the first way to obtain real-time quotes from multiple exchanges, such as the top ten exchanges, and eliminate the exchange quotes that have experienced large price fluctuations, thus obtaining relatively smooth and accurate. Price; the second upgrade quote refresh rate, refresh the price according to the frequency of 1 second, get the latest quote information as much as possible.

The second is to speed up the confirmation of the transaction. If the transaction confirmation can be completed in an instant, then the fluctuation can be ignored. The application can be improved by applying BIP or Bitcoin. This improved protocol is supported by policy support for additional messages, allowing for quasi-real-time bitcoin payment confirmation, a strategy that would greatly alleviate the risk of currency fluctuations within minutes. The mechanism and application of BIP will be described in detail later in this paper.

The third is to rationally set the price. The commonly used scheme takes the weighted average of the real-time exchange rate of the target exchange, and can also eliminate the highest and lowest quotations, and then take the weighted average.

Fourth, when accepting the customer's order, the reverse operation is performed in the manner of guaranteeing each transaction, that is, the currency received from the customer or the currency paid for the purchase is locked, thereby locking the price of the currency.

3.6.3 Bitcoin's own risk

Bitcoin itself has specific risks, including the aforementioned forks, 51% attacks, etc. Usually, this special scenario does not occur, but it also exists for a certain period of time at special times such as the global submarine cable break caused by network fragmentation. The corresponding possibility.

At the same time, the future bookkeeping rewards of Bitcoin will no longer come from mining but from both sides of the transaction, the friction costs will also rise.

These problems will not pose challenges to the program in the short to medium term, but in the long run, it is also necessary to effectively prepare by selecting a diversified digital money carrier.

3.6.4 Performance bottleneck risk

Due to the inefficient consensus mechanism and the need to broadcast and reach consensus on the whole network, the payment efficiency of Bitcoin has always been a major problem that plagues the industry. According to estimates, the current TPS (bits per second) of Bitcoin is about 3-7, compared to tens of thousands of TPS in general banking core business processing capacity. The industry has been exploring various options to mitigate this bottleneck.

One type of method is to increase the transaction capacity of each block by expanding the block. For example, BCH currently uses 8 times capacity expansion. From the economic point of view, it can achieve lower handling fee and higher TPS, which is more suitable as a The currency of the payment instrument, which can be actively adopted and accelerated to the actual scene. The second is the segregation witness, SegWit. By separating the witness data from the transaction data, the transaction data is more carried in the block capacity, and the number of transactions packaged in each block generation cycle is expanded, which can improve the efficiency at 1.7. Between -2.5 times, this mechanism depends on the deployment progress of the entire network. The third type is lightning trading, which means that by opening a lightning payment channel under the chain, the final record is only found in the chain to seek consensus when there is a dispute or need to close the channel. In fact, every transaction is avoided in daily use. Inefficient operation of the blockchain consensus, which depends on the deployment progress of the entire network. The combination of the above means can further improve efficiency.

Chapter IV Cross-border Payment Service Solution Using Blockchain Technology

Section 4.1 Overview

Before the blockchain, the traditional card organization as a centralized organization, its status is difficult to shake, and the role of the decoupling, trust, and natural liquidation of blockchain technology has been fully demonstrated in the field of payment and liquidation. As a bearer, real-time, low-cost value circulation becomes a reality. On the other hand, the trust of the technical guarantee of the blockchain enables third-party companies to quickly gain user trust and start to establish between C-side customers and B-side merchants. Ecology.

At present, the use of blockchain technology to achieve cross-border payment is mainly for both single-ended and card-issuing modes. In fact, it is aimed at different scenarios, perfectly solving various problems encountered in the traditional mode, and quickly opening up cross-border A new situation of payment.

Section 4.2 Ideas and Design

The cross-border payment of the consumption scenario can actually be further divided into the acquirer and the issuer. By introducing the blockchain technology and the digital currency (token), without changing the usage habits of the C-side customer and the B-side merchant, And to minimize the transformation of the merchant side and the laying of tools, to achieve clearing and settlement of cross-border payments.

4.2.1 Analysis of the role of digital currency

The basic concepts of digital currency have been introduced in the previous section, and the role of digital currency in the entire payment flow process will be explained here.

The core value of digital currency is to ensure that assets are credible and reliable. Through the decentralization, de-trust, and non-tamperability of the blockchain, digital currency has also been given the characteristics of being controlled by third parties and witnessing collective accounts. Therefore, holding digital currency will not be forcibly frozen and transferred by third parties. . For example, there will be no incident in which the card organization forcibly transfers funds to fraudulent gangs after accepting malicious refusal.

Digital currency is characterized by rapid real-time circulation and support for natural clearing settlement on the chain. The digital currency realized by the blockchain itself has value, which is different from the traditional bank and the electronic money paid by the third party, not only the currency symbol, but also the value itself. In the traditional clearing and settlement process, funds need to be liquidated and then settled. This is also an important reason for the delay in the cross-border payment scenario. The integration of digital currency clearing and settlement, real-time completion, will realize real-time funds. Arrived.

Since the flow of digital currency is completely based on specific applications on the Internet, there is no national border, no centralized management organization, no intermediate links established by government supervision and private organizations, so it is not regulated, not subject to foreign exchange control, and freely available on a global scale. Circulation. Of course, this also brings some risks. For example, it is necessary to take full responsibility for the custody of the digital wallet. For the case where the digital currency is stolen, the key is lost, and the digital currency is lost, it is impossible to obtain help from government agencies or private organizations. At the same time, the fluctuation of digital currency is large, real-time exchange is acceptable, and long-term holding is subject to large price fluctuations.

4.2.2 Recruitment and design of the receiving end

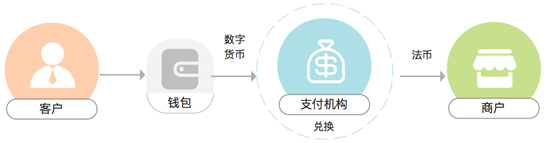

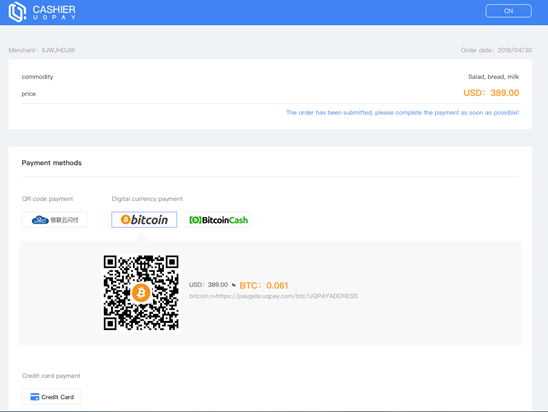

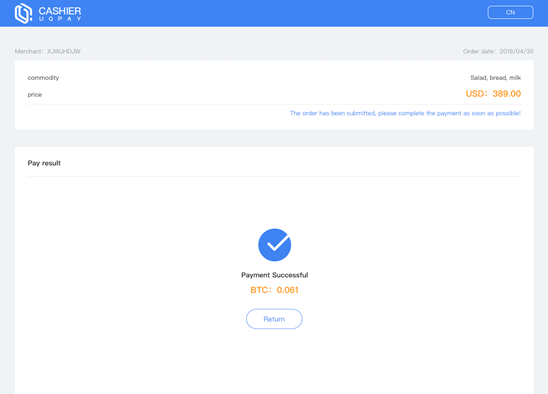

The basic process of acquiring the receipt: the receiving end is a payment product for the merchant to receive the order, which is divided into two scenarios: in-web in-app and in-store. Customers use digital currency for payment, while merchants receive the required fiat currency in real time, and the payment company acts as a third party for payment and redemption.

Figure 4.1 Schematic diagram of the receipt of the program

The customer can directly pay the digital currency to the merchant through the digital wallet compatible with the payment agreement, and the payment institution immediately sells the corresponding digital currency according to the current price after receiving the request, ensuring that there is no loss in the exchange, and the converted currency is paid. To the merchant.

This model can provide a new market expansion mechanism for major card organization organizations around the world, and can be widely applied to offline and online payment and e-commerce scenarios, including collection apps used by offline stores, and smart Pos. Machines, as well as online e-commerce payment APIs, payment gateways, and MPI (Malls Plug-in).

MPI is a payment plug-in for e-commerce websites that provides online billing solutions, including payment processes, security certification, and fraud prevention. By providing a reliable payment infrastructure, the cryptocurrency payment model is promoted globally to meet the easy access, convenience and customer-facing needs of merchants and their customers. This mechanism can bridge the gap between cryptocurrency owners and merchants. Encrypted money owners buy goods and services in their own currency, and merchants can easily exploit the benefits of blockchain to grow their business. By adopting this mechanism, the e-commerce website does not need to specifically develop the payment interface, and the payment capability can be realized by simply referring to the plug-in and performing account binding. The current mainstream MPI includes WooCommerce, Magento, Opencart, osCommerce and more.

Offline merchants use the smart collection POS application, which can directly install the smart collection app to any connected smart terminal device, including mobile device Android, iOS and PC device Windows, Mac, without purchasing special POS tools, this lightweight The solution can greatly reduce the deployment cost of the merchant's cryptocurrency receipt and increase the deployment speed. After simply inputting the local currency in the application, the system can obtain the converted cryptocurrency list through the system DCC, and then can select and implement Quick payment and receipt. At the same time, the system provides an open API for smart collection POS applications, allowing merchants to access the existing MIS cash register system to the smart pos application to solve the problem of integrated collection.

4.2.3 Idea and design of card issuance