How much decentralization is “decentralized finance”?

Foreword: Since 2018, the terminology of DeFi, open finance, and decentralized finance has become popular, and people often mix it. Are they the same? Is open finance equal to decentralized finance? How decentralized is decentralized finance? In the current decentralized finance, there are many centralized participations. How will these explorations develop? Is this a good or a bad thing? What do you think? The author of this article is Aaron Hay, translated by the "DL" of the "Blue Fox Notes" community.

Today's decentralized finance is mainly based on Ethereum, and has a lot of collaborative stack components:

Core consensus agreement

2. Assets

- Telegram blockchain network will be compatible with Ethereum

- EU Commission confirms preliminary antitrust investigation of Facebook's Libra

- Vitalik Buterin: The dawn of the hybrid Layer 2 protocol

3 smart contract agreement

Smart contracts support new assets, new assets serve as collateral to support other new assets, and all assets are backed by underlying core consensus agreements.

Points 2 and 3 depend on point 1, so they cannot achieve greater decentralization than point 1. That is to say, since the first point sets the theoretical maximum level of decentralization, then this is the upper limit of the decentralization level that can be achieved and maintained by points 2 and 3.

Developer Method / Design Tradeoff

Although some assets and agreements are built on Ethereum, other assets and agreements may not be considered, taking into account the core principles of Ethereum.

“When I created Uniswap, one thing I really realized was trying to mimic the properties of Ethereum itself. Therefore, Ethereum has some key attributes that I really care about. It is not the most efficient treatment, it is not the most Efficient storage. It is the most decentralized programming method, it is the most anti-censorship… You have this kind of trust-executing execution, it has all these attributes. So these attributes are what I am trying to rebuild. (From Wyre's interview with Hayswana's founder Hayden Adams)

The above citations refer to the trade-offs faced by Ethereum, Bitcoin, and other blockchain protocols: the trilemma of scalability. (Blue Fox notes: refers to decentralization, security and efficiency can not have both). The trivial theory of scalability points out that the blockchain system is difficult to have the following three at the same time in the base layer:

l Decentralization

l scalability

l Security

Today, there is no blockchain with high performance decentralization, scalability, and security. Bitcoin and Ethereum's PoW have different designs, but both have chosen higher decentralization and security, and sacrificed scalability. The same trade-offs exist for assets and smart contract agreements built on Ethereum.

Note that for decentralization, there is no finish line, and decentralization is more of a float, which is usually subjective. Decentralization cannot be reached, and efforts can only be made in this direction. Building on Ethereum does not mean that it must have the same attributes.

Not everything needs to be decentralized, but some things should be decentralized.

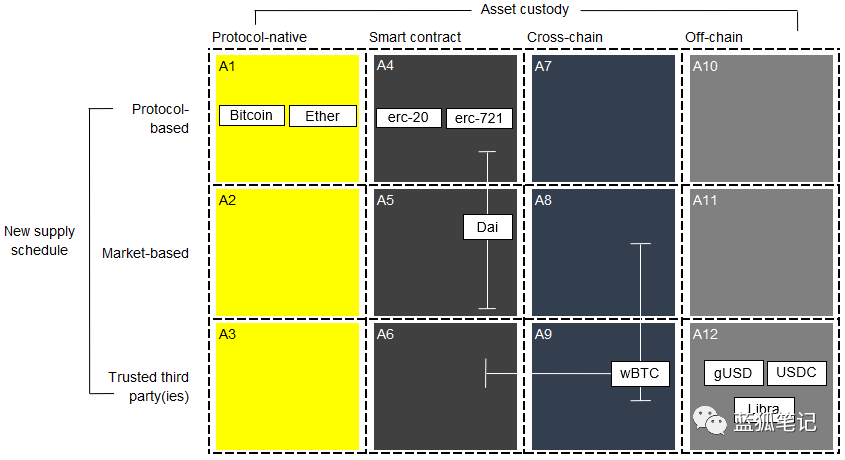

assets

The basic framework for mapping assets through hosting and provisioning capabilities

The basic framework for mapping assets through hosting and provisioning capabilities

1. Bitcoin and Ethereum

Among the other assets mentioned above, Bitcoin and Ethereum represent a decentralized “gold standard”. Both are protocol-originated, which means that both hosting and new offerings occur at the protocol level, both transparent and open. Each has a known supply rule, which is identifiable. Both are programmable deflation assets, with more than a decade (BTC) and more than four years (ETH).

2.erc-20, erc-721 and other token standards

They are audited smart contract standards, similar to Bitcoin and Ethereum, that support transparent and publicly hosted and processed new token offerings.

However, there are additional risks here:

1) Hosting and ownership are now handled by the code of the smart contract

2) The issue may vary greatly depending on the token and should be verified at a reliable source. Check the supply amount by onchainFX, etc.

3.Dai

Dai of MakerDAO is a very interesting stable coin experiment. Dai maintains many key aspects of ether, but adds considerable complexity because it requires the coordination of multiple smart contracts and decentralized stakeholders. Dai is an er-20 token, hosted by a smart contract, and the supply is variable and based on market demand, depending on the net creation of CDP.

4. Cross-chain assets

wBTC is a relatively new asset and is not large, but it proposes an innovative solution, a framework for waged assets, which enables Bitcoin or other cross-chain assets to access smart contracts on Ethereum. wBTC still presents a variety of risks, including broker risk (from merchants and custodians), smart contract risk (erc-20), and mortgage risk.

5. Out-of-chain hosting

It has risks from middlemen and how much they provide user checks and transparency for managed programs and security measures.

Note: Many of the above assets are derivatives, that is, their value is supported by the underlying assets, such as USD, BTC, or a basket of assets. As mentioned above, the supply of derivatives and the supply of its underlying assets (such as BTC) will change.

Note: All of the above assets are at risk of centralized hosting when owned by a centralized exchange. For example, ether is on an exchange, which is an A1 asset for an exchange, but for an exchange user who owns the asset, it is an A10 asset. Similarly, when ether moves into a smart contract, it becomes an A4 asset for the user of the asset. (Blue Fox notes: that is, the native token A1 asset that is controlled by the individual becomes the native token A4 asset controlled by the smart contract code.)

protocol

Here are some of the design features that I observed to sacrifice decentralization in some way:

Rent-seeking

Rent-seeking can be explicitly stated by fee (beyond the prescribed gas fee) or by using a specific token. In theory, if open source code is released, it has rent-seeking, and in some way the cost is built into the agreement, the protocol is easily forked, and the cost-related code is removed.

We have begun to see this in reality, see Zcash/Zclassic, Bancor/Uniswap.

2. Closed contributor group

For example, in a PoS system, if the verifier group is closed to a "selected" verifier, or the verifier selection process is not random, decentralization is limited to placing trust in the governance intermediary. Similarly, smart contracts that rely on external data, small and well-predicted machine sets pose additional risks.

3. Trap door

If the developer can temporarily lock or permanently stop the feature, then the smart contract code is not autonomous. However, trapdoors may prove to be beneficial when a vulnerability is discovered.

The above list is not comprehensive, just some examples of common protocol design tradeoffs. Often, you need to be very close to the code to accurately understand what you trust, or the messaging needs to be clear and transparent.

Information transfer

Some smart contract agreements and assets do not show more decentralization, but they are open and free to use. In other words, some assets and agreements are part of “open finance,” but not “decentralized finance.”

However, this line is not clear, and open finance and decentralized finance often overlap and mix. Because of the lack of a clear definition, terms are easily misrepresented and form a disconnect between perceived trust and actual trust.

l 2016: “The blockchain is not bitcoin”.

l 2017: White papers full of buzzwords dilute the original meaning of blockchain-specific terms.

l 2018: “Decentralized finance/defi” and “open finance” emerged, which were used to promote various projects and measures with varying degrees of decentralization and openness.

l 2019: Libra tries to change the original meaning of "cryptocurrency"

So, how decentralized decentralized finance is?

Every protocol, asset, and application is different, and even decentralized things can be centralized through hosted exchanges and other aggregators.

Users should often question the news and feasibility of the new financial instruments they are using, and more importantly, they need to have a clear understanding of who they trust (centralized middlemen) or what (smart contract code). (Blue Fox Notes: In reality, the vast majority of reading users have neither the ability nor the energy to understand the code and security of a smart contract.)

If an asset or agreement has no good reason to deviate from its underlying design principles, there are good reasons not to use these new financial instruments.

——

Risk Warning : All articles in Blue Fox Notes can not be used as investment suggestions or recommendations . Investment is risky . Investment should consider individual risk tolerance . It is recommended to conduct in-depth inspections of the project and carefully make your own investment decisions.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- 80% of ETH addresses are at a loss, but BTC addresses are 70% profitable

- Encrypted domain name is being squatted, sold, illegally possessed

- Lightning network has security risks, users need to update the client as soon as possible

- Perspectives | Incomplete Contracts and Blockchain Expansion

- Futures positions are bullish, bull market is not over yet?

- Thai Customs will use IBM and Maersk's blockchain platform to streamline cargo tracking processes

- "False" gold disrupts the market, BTC or demand soars