How should the banking industry use blockchain technology?

Disclaimer: This article was compiled by the BITKER project team. The BITKER project team focuses on the theoretical research of the blockchain industry, cutting-edge technologies, and secondary markets.

The modern banking system dates back to Italy in the 13th century, when the most famous bank in Europe was the Medici Bank. Their main innovation is the combination of banking and accounting systems to record double-entry accounting data in the general ledger. The banker's job is to track borrowers and lenders, or to handle deposits and withdrawals for clients. They must ensure that the books are placed in a safe place and that funds are secured. Trust and talent are among the most important factors for bank success at the time and in the coming decades.

For centuries, some of the world's largest companies and the highest salaries have come from the banking industry. However, during the 2008 financial crisis, this trust between banks and customers was hit, and many banks managed poor client funds. It is time to take some new measures. Many startups have entered the field, offering mobile-first, UI- and UX-friendly banking solutions. But the problem still exists, human error, corruption, transcripts and paper records, and poor transaction management, which will not disappear with the current system.

- Counterfeit currency attacks on the currency circle: how to prevent it effectively?

- Babbitt column | Dovey Wan: Bitcoin is not a safe haven, yet

- Weekends are rising? Since May, 40% of BTC's rising prices have occurred on weekends.

It was at this time that a new technology was born. This technology allows third parties to track transactions in public ledgers, transfer value globally at a faster rate, and manage pseudonym status online without the need for a central entity. This technology is called Bitcoin and was introduced by Satoshi Nakamoto. Bitcoin unwittingly introduced a three-way accounting system that banks can use to improve existing infrastructure.

Bank research blockchain technology

Bitcoin may now be created to diversify the power of the current banking system, but this will not prevent banks from conducting research and attempting to use this infrastructure to develop their own systems. Managing personal bank accounts may not be suitable for everyone, even if Bitcoin promotes the use of this tool, even for 2.2 billion non-bank accounts worldwide. The blockchain reduces the infrastructure costs of bank operations, which may help banks (or other startups) to absorb this huge bank accountless population.

Mike Bodson, CEO of DTCC, said:

"Assuming the US stock market has $65 billion, in five to seven years, I think that $65 billion will be reduced to $48 billion, so the cost pressure is high. In the past few years, all Wall Street companies are doing The same thing, they all try to modernize, but they don't use old technology, but outsource their business and send it overseas. They do all sorts of things and try to reduce costs, but at the same time, they also face The pressure of compliance and regulation has increased costs."

DTCC spends $1.4 billion a year, 50% on technology ($700 million) and deals $1.8 trillion a year.

2. Long-term opportunities

Every bank is focused on reducing costs, and blockchain technology may just help them achieve some of their goals. They can move critical operations, risk and financial systems to the blockchain platform.

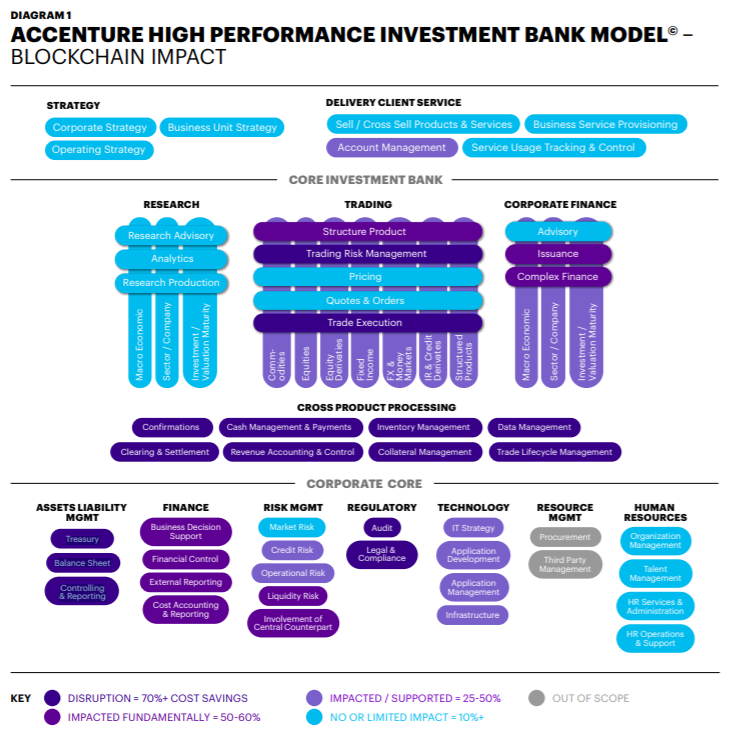

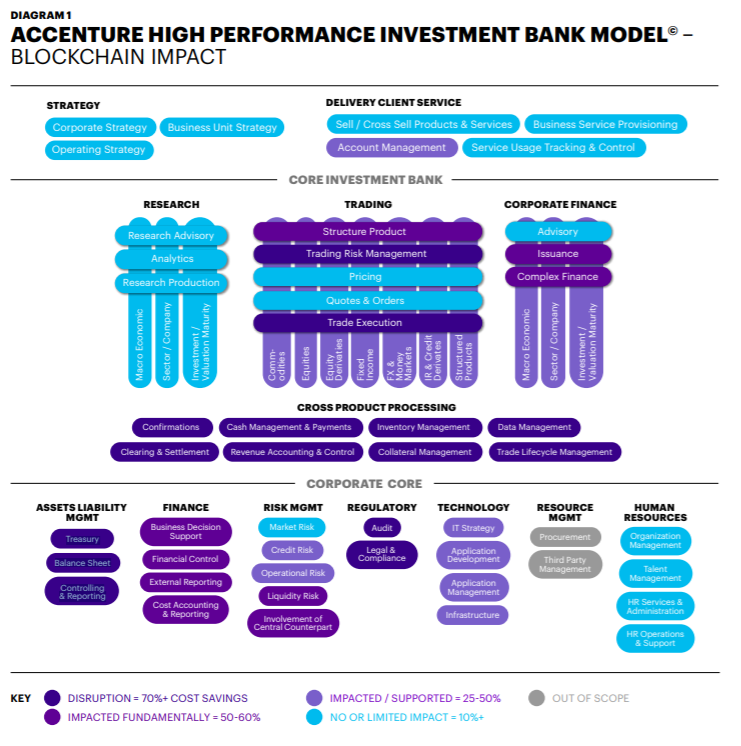

Accenture has published a report on which areas of the blockchain have benefited the most.

figure 1

Some of these areas may be affected by 70% damage due to their ease of automation. Imagine that all transactions are in a database, and anyone can audit its history and update the current transaction in real time. Because all transactions are digital, people no longer worry, if the storm comes, it will destroy the place where these transactions are stored, and waste valuable time to re-notify the network. In addition, because blockchains are stored in distributed networks for transactions, no one can hack, tamper with, or destroy past information (unless they have 51% of computing power, which is another matter).

Accenture finally completed the report. The report says that if the system is upgraded, the blockchain can help save about $8 billion.

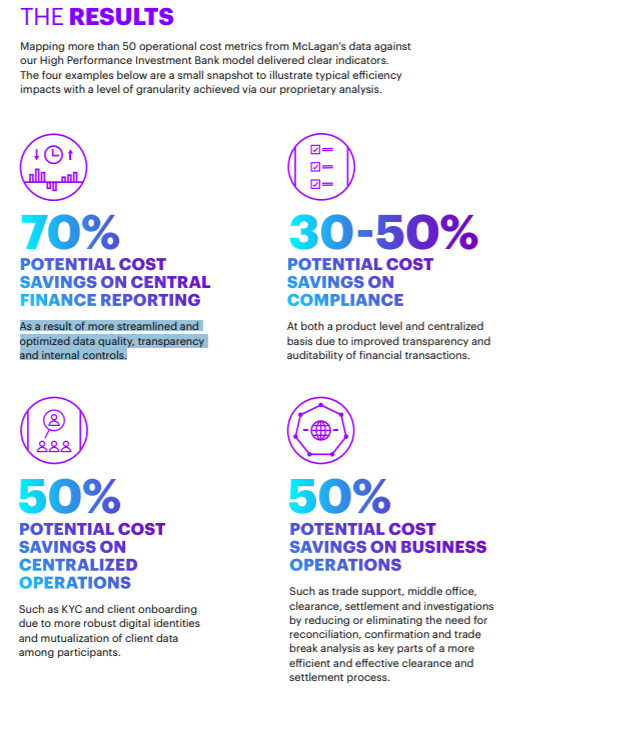

figure 2

3. Current blockchain solutions for central banks

Since 2014, central banks have been investigating the applicability of digital ledger technology in various bank debts, and currently about 40 central banks are investigating. As with any new technology, the blockchain is full of unknowns. Experiments and research have shown that central banks have significant advantages in adopting CBDCs (commercial bank digital currency) and DLT (distributed ledger technology). In the World Economic Forum white paper, ten use cases were proposed:

(1) Retail CBDC uses similar physical cash or alternative bank deposits for consumers.

(2) Commercial interbank lending rate (cbdc) wholesale settlement.

(3) Inter-bank securities settlement allows simultaneous peer-to-peer asset transactions.

(4) Primary or backup payment systems in domestic emergencies.

(5) Sovereign bonds issued and managed by the countries acting as nodes.

(6) Financial tracking of “anti-money laundering”/KYC information as a unified information channel.

(7) An information sharing site between public and private entities for financial data streams.

(8) Issue trade finance on distributed ledgers to increase domestic and global efficiency.

(9) Cash flow supply training tracks and analyzes the large amount of cash flow between commercial banks and central banks.

(10) The blockchain database is the EU Environmental Protection Agency credit system to improve the overall efficiency among member states.

3.1. Retail CBDC uses similar physical cash for consumers

In the future, when consumers use less cash, it is crucial for a country to introduce a good CBDC. Especially in countries where commercial banks are unstable and deposit insurance is not available. CBDC can be a program for inclusive finance, especially in the case of 52% mobile phone penetration.

3.2. Commercial Interbank Offered Rate (CBDC) Wholesale Settlement

Central banks from emerging countries have benefited the most from instant transactions, and central banks with efficient systems (such as the Danish Central Bank) can create a major or alternate domestic payment system in an emergency.

The intersection of emerging countries and developed banks may allow everyone to stand on the same side. Therefore, if the Bank of Denmark uses the blockchain as a backup and the Bank of Argentina as the primary backup, then it may be necessary to use the same technology to settle the transaction.

4. Blockchain bond issuance

Société Générale issued 100 million euros of guaranteed bonds in the Ethereum (ETH) blockchain as a securities-type token known as “habitat debt” or OFH. The bond was rated AA/Aaa by Moody's and Fitch and is part of the internal start-up project for the FinTech. The blockchain allows Société Générale to explore a more efficient bond issuance process in real time. Blockchain bonds reduce time to market, increase transparency, and enable faster transfer and settlement. Smart contracts automate the entire process.

Afghanistan, Tunisia and Uzbekistan have been testing blockchain sovereign bonds to help key sectors of the economy get out of trouble and increase market confidence. Afghanistan wants to issue a metal-linked bond, especially for the country’s $3 trillion lithium industry. Uzbekistan intends to issue blockchain bonds for its cotton industry, and Tunisia will issue bitcoin-based sovereign bonds. (Asia Times)

"Anti-money laundering as a unified information channel" / financial tracking of KYC information

According to Marouane El Abassi, governor of the Central Bank of Tunisia, blockchain bonds can combat money laundering, manage remittances, combat cross-border terrorism and limit the gray economy. (Asia Times).

5. The bank is already testing or using blockchain technology

5.1. New York Mellon Bank – blockchain-based US Treasury settlement

The Bank of New York Mellon is a global banking and financial services holding company headquartered in New York that manages $1.8 trillion in assets. They focus on providing a full range of foreign exchange, securities financing, collateral management and segregation, capital markets and prime brokerage services, as well as custody and wealth management. As early as 2016, they launched the BDS360, a US Treasury settlement system with blockchain technology, as a backup record for their systems. This blockchain reduces the bond's 3-5 day settlement time to 1-10 minutes in a safe, transparent, low-cost and instant manner. The back end bypasses distrustful intermediaries and outdated infrastructure by cleaning up and verifying the authenticity of bonds in the blockchain.

5.2. Santander Bank – Cross-border transactions

Banco Santander is a Spanish multinational commercial banking and financial services company headquartered in Santander, Spain, with revenues of $54 billion in 2017. The services of Banco Santander and blockchain technology are spread all over the world, and because of the instant cross-border transactions provided by the technology, the two can be described as a match. Together with Ripple's service Xcurrent, Santander launched One pay FX in 2018 and launched a distributed application (Dapp) to provide day-to-day international trading services to customers in Brazil, Spain, the UK and Poland. The traditional system takes 3 – 5 days and charges an average of $25 (or more than 3%-7% of the $25) to the customer based on the bank's completion of the international transaction.

5.3. Members of the ING-Zero Knowledge Set

ING is a Dutch multinational banking and financial services company headquartered in Amsterdam. Its main businesses are retail banking, direct banking, commercial banking, investment banking, asset management and insurance services, with 37 million customers worldwide. They tested blockchain technology and used Zero Knowledge Scope Proof (ZKRP) solutions to increase the confidentiality of public ledgers. Tests developed internally by the team show significant improvements in efficiency to protect customers' private information. A “zero knowledge certificate” allows a party to verify the accuracy of a statement without passing the actual information in the statement. Zcash is one of the largest cryptocurrencies using the ZKRP model.

6. Way of cooperation

6.1. Public chain

The public chain (unlicensed blockchain) allows anyone to interact with the network and run the node. Blockchain networks such as BTC, ETH, LTC and EOS are public chains. The benefits of an unlicensed blockchain are the more fundamental, more transparent, and unchanging components.

Banks may be less interested in getting everyone involved in the network. Unlicensed blockchains like Monero, Zcash, and Grin are using zero-knowledge proof algorithms to focus technology on more proprietary components.

The Aztec protocol provides a privacy component built on top of the Ethereum blockchain.

6.2. Private chain

The private chain (licensed blockchain) only allows authorized parties to participate in the network, check transactions, and audit information flows. There are currently consortiums that are setting up to bring together all banks and study private blockchains without revealing key data that should not be disclosed.

Ripple, Stellar, Quorum and R3 are some of the largest private chains or consortia.

7. Conclusion

In addition to opening a cryptocurrency trading counter, banks have many scenarios to study blockchain technology. The blockchain is currently beyond the testing phase of the banking industry, and banks want to know how the blockchain will work for them.

Author: Menajem Benchimol (. Blocktren founder Hackernoon columnist)

Article source: https://hackernoon.com/how-banks-are-leveraging-blockchain-technology-4bc8143f359f

Compilation: Bitker Research Institute

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Where is the development bottleneck of DeFi? What is the opportunity?

- Reddit will accept cryptocurrency rewards, this time without robots

- Coinbase: Bitcoin is becoming mainstream in the US, and nearly half of institutional investors are considering holding cryptocurrencies

- Encrypted Currency and Stratum Crossing (1): Bitcoin is your only chance to "slap the table"

- Quote analysis: BTC weekly line receives super big Yinxian, the long market is over?

- How do programmers view Libra source code? More doubts on GitHub

- In-depth interpretation of the first reading of PlatON cloud map economic blue book