Pivot: Will halving really lead to a rise in the price of the currency?

“Bitcoin prices have rebounded after the decline during the Libra hearing,” Forbes wrote. A "mystery order" (Translator's Note: an order for 20,000 bitcoins on Coinbase, Kraken and Bitstamp on April 2) opened the curtain of the 2019 bull market, Reuters reported. Tether's additional stable currency is a supporting factor for the recent rebound in bitcoin prices, QUARTZ said.

However, even a phenomenon with a logical basis may not have a causal relationship. Encrypted currency advocates generally believe that the reduction in block rewards causes prices to rise. And, this logic is reliable. If the miner earns less tokens, the selling pressure is reduced. The decrease in the supply side will cause the price of the relevant token to rise.

Litecoin has recently brought this narrative into mainstream attention. From the low of $22 in December 2018 to July of this year, it rose by 480% – one of the few assets to outperform Bitcoin during the bull market. Public publications, including CryptoSlate, attribute the rise in prices to the upcoming cuts.

- lCO six years of concise history: genius, scam and myth

- Bloomberg: Bitcoin is not an ideal safe-haven asset

- Charlie Lee: Litecoin needs more substitutability and privacy to make a bigger breakthrough in market capitalization

However, research by Nico Cordeiro and Ava Masucci from Seattle startup Strx Levlathan (the company) proves that the narrative of the mainstream media is wrong. The company specializes in designing and operating trading algorithms for the cryptocurrency market, which challenges people's belief that production cuts have a significant impact on token prices.

01 report text

- We found no evidence that the yield of crypto assets that experienced a reduction in production outperformed the market within six months of the decline in miners' rewards.

- The yield of a cryptocurrency asset for six months before and after the production cut is statistically higher than the rate of return for other periods, which shows that there is no evidence to support the change in supply and demand mode resulting in price anomalies.

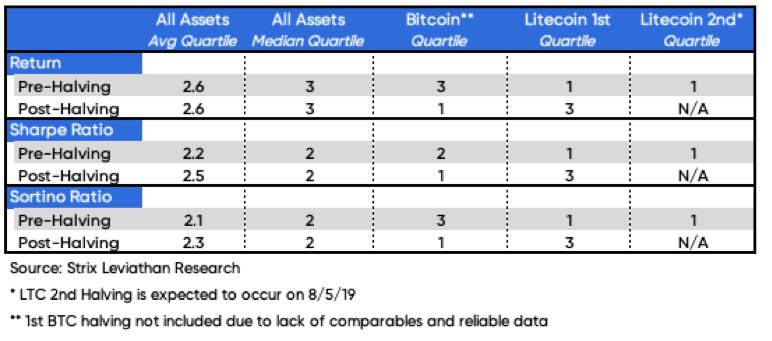

- In the few months before the two production cuts, the Wright currency outperformed the market, but after the first production cut, its price performance fell to 25% at the bottom of the market.

- Bitcoin presents an extreme counter-example of Litecoin, which has a poorer yield before the cut, but a stronger yield after the cut.

The reduction in mining incentives has reduced the selling pressure from miners, which has created an imbalance between supply and demand, which in turn has facilitated price adjustments.

Limited examples and historical data make it difficult to verify any narrative in the cryptocurrency field. Therefore, in order to examine the supply and demand theory that underpins this widely accepted narrative, we collected 32 production cuts of 24 assets (all of which experienced a reduction in miners' rewards according to a preset timetable), and another 320 The market is used for horizontal comparison.

Then we divided the above data into the period of 1, 3, and 6 months before the production cut, the time period of 1, 3, and 6 months after the production reduction, and the period of the non-reduction period, and then carried out the following analysis:

- For the same period of time, the price performance of the cryptocurrency that experienced the decline in mining incentives is reverse tested with the price performance of the cryptocurrency that has not been experienced, and then the performance data of each asset is converted into quartiles.

- Statistical analysis is used to determine whether there is a statistical difference between the distribution of yields during the period of reduced production of crypto assets and the distribution of yields during periods of reduced production.

- Before discussing the final results, it is necessary to understand the two implicit assumptions we have discovered if there is a fundamental change in the supply and demand relationship:

- The sudden change in the relationship between supply and demand of an asset represents that it has just experienced a reduction in production.

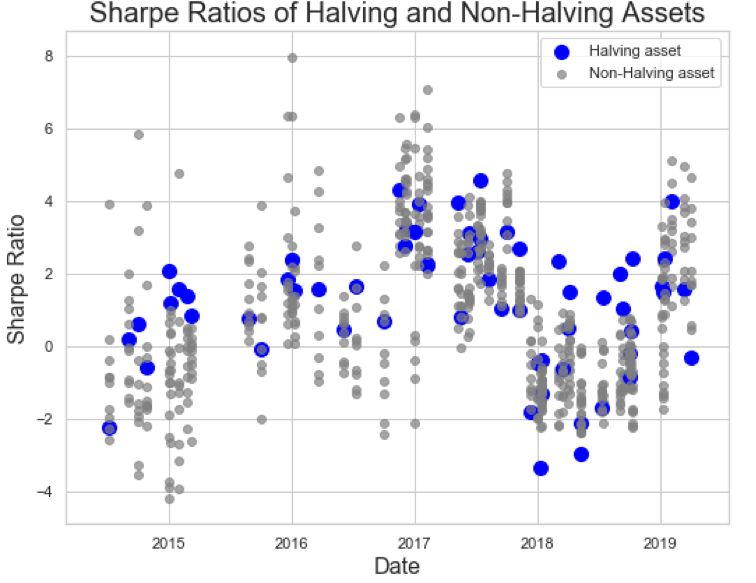

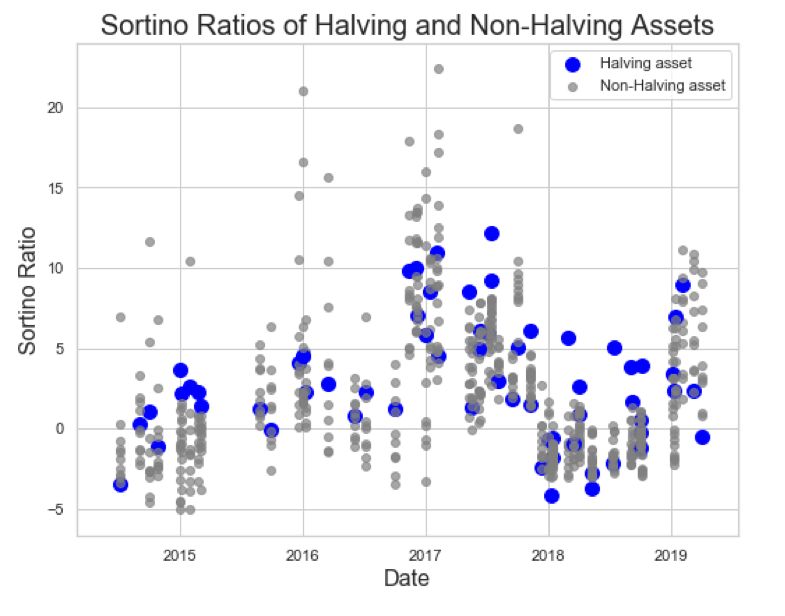

After the analysis is completed, we find that the impact of production cuts on the performance of cryptocurrency prices is limited. Through a review of the total return, Sharpe ratios and Sortino ratios, we found that the crypto assets that experienced a reduction in production before or after the decline did not perform better than the rest of the market. Part is good.

In terms of the two most influential cryptocurrencies in the production narrative, Bitcoin and Litecoin, we see a set of opposing extreme performance. Before the production of the Litecoin, its price performance outperformed the market twice, and its price fell to 25% at the bottom of the market in the six months after the production cut. In terms of Bitcoin, its price was weaker than the market as a whole before the production cut, but its price performance ranked the top 25% of the market after the last production cut. The difference before and after this reduction in production and the seemingly random results show that the supporting factor driving price increases is not the change in supply and demand dynamics.

By analyzing the time series of each asset and comparing it to the asset itself, further evidence showing that the production event is limited to market prices can be found. What we have found is that the return on an asset during the production cut is statistically the same as the return on the non-reduction period, which is statistically the same at 99% confidence level. In other words, we have not found that the production cuts cause abnormal fluctuations in prices, and we are faced with an indirect illusion.

In a broader sense, especially for Bitcoin (which performed better than the market after the last round of production cuts), what does this mean? From a more ambitious perspective, there is little evidence in these data. It shows that the income before and after an asset is reduced is caused by factors other than broader market sentiment. As far as Bitcoin is concerned, the reason it may outperform the market is the widespread belief in cryptocurrency fans. In addition, we do not recommend speculating the overall market with a single market sample.

Financial markets are full of thousands of mature, logically complete theories, but they are rarely feasible in reality. The same is true of the theory of supply and demand that supports production cuts. In reality, it is more likely that the gains in the front, middle and late stages of production cuts will be brought about by the rise in speculative levels rather than the pressure of selling pressure.

[Note] The assets analyzed include: BTC, LTC, XVG, FTC, MONA, NMC, FLO, POT, ABY, CURE, NYC, MOON, VTC, EMC2, IOP, MEME, COLX, ONION, DIME, LINDA , UNO, TRC, ANC, and SXC

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- China and the United States upgrade each other, BTC welcomes golden moments

- Supermarket giant Wal-Mart's "money war", want to bitcoin, Libra to the world?

- Why do you even hold some bitcoins even if you don't like it?

- US SEC Commissioner: The United States can learn from these countries for cryptocurrency policy

- Blockchain Weekly | In July, there were many security incidents in the exchanges and wallets. What happened to the market after the Litecoin was halved?

- The central bank accelerates the study of digital currency and sees how the progress of CBDC in various countries

- Global “City Currency” Inventory: These 13 countries and regions plan to “enclosure” currency