Stable Currency 3.0 Report | New Historical Mission and Competitive Landscape

Stabilized currency refers to the general equivalent of a "currency" that is relatively stable with the exchange ratio of the legal currency. Because the exchange ratio between legal currency and goods and services is relatively stable, the ultimate anchor for stable coins is goods and services, which is the actual purchasing power.

First, the digital currency market has developed at a high speed, and the stable currency has undergone three changes in identity and value.

Stabilizing Coin 1.0 : As a “deposit channel” and “preservation medium” for Token investment, it is likely to become a transitional product in a special historical stage.

- I survived the collapse of Lehman and survived the financial crisis. See how he built the "Golden Surplus"

- Taiwan has included STO in regulatory scope | Standard Consensus

- 14 BTC, the highest donation in the history of Bitcoin.org

The number of stable coins that have been developed since the end of 2018 , the main value is concentrated in the "input channel" and "value-keeping media". Their starting point is to solve the problem of Token investment. From this point of view, a good "stabilized currency" not only needs to have a reliable stability mechanism, but also maintains the stability of the "coin price". It also needs to exert influence in the majority of investors and provide convenient purchasing channels, especially with The major Token trading platforms have reached a cooperation, and there are enough stable currency trading areas and trading pairs on the line.

Fundamentally, the stable currency of the 1.0 period is the product of a rapidly developing Token investment demand, and the contradiction between regulatory restrictions on the entry of legal currency, which is a product of a special historical stage. The greater the price fluctuations of various Tokens such as Bitcoin and Ethereum, the more valuable the existence of stable coins. We have reason to predict that when countries around the world regulate the liberalization of “funded currency” transactions, or when mainstream currencies such as Bitcoin enter a mature stage of development and tend to “stable”, the above two values of “stable currency” will cease to exist. Of course, at present, this may take a long time to go.

Stabilizing Coin 2.0 : An efficient payment settlement tool within the banking system is essentially a “digital legal currency” that relies on commercial bank credit rather than government central bank credit.

At the beginning of 2019 , JP Morgan Chase and Japan Mizuho issued "stable coins" to bring a new wave of blockchain digital asset investment. But in fact, the stable currency layout of the two world-renowned commercial banks can neither bring new users to the blockchain digital asset world nor bring new funds. Because in essence, they only use blockchain technology to do the payment tools of the bank's inherent “storage”, “loan” and “sink”.

Blockchain technology has tremendous transformation value in the field of payment settlement, especially payment settlement between entities. The “stabilized coins” issued by the two banking giants are essentially using a convenient and efficient settlement network based on blockchain technology. The more financial institutions and customer groups that join this network, the greater the value of the settlement network. The “coin” here is called “stabilized currency”. It is better to call it “bank acceptance bill” on the inter-bank blockchain alliance chain, or “digital legal currency” based on commercial bank's own credit rather than government central bank credit.

However, it should be noted here that if the issuers of financial institutions such as banks comply with the 1:1 full amount of legal currency deposit mortgages, the stable currency is a settlement tool for them. If the issuer is not fully prepared, the stable currency it issues becomes a financing tool that involves the issue of “currency creation” and “money coinage”.

Stabilizing Currency 3.0 : "Currency" within the new blockchain finance and business ecosystem

In recent months, Defi ( Decentralized Financial ) has become one of the most concerned topics in the blockchain industry and even the traditional financial industry. If Bitcoin represents the idea of “non-state free competition currency”, Then behind Defi is the idea of “going to banking and self-financing”. This will have a huge impact on the business model and organizational structure of the traditional financial industry.

With the further development of infrastructure such as the public chain, the bottleneck of high-performance technology is breaking through, and various applications and financial services in the chain have also developed rapidly. Whether it is the consumption behavior of various DAPP goods and services such as "games", "entertainment", "social", "education", or the various types of "savings", "borrowing", "funds" and other financial assets based on digital assets. Behavior requires a value scale with stable purchasing power and a trading medium – stable currency.

Although it also has the function of “preserving value”, compared with the stable currency of the 1.0 period, the more important value of the stable currency in the new era is to construct a closed loop of value in a commercial and financial system. Based on the closed-loop value of a public-chain infrastructure, it is necessary to assume a large number of DApp goods and services and the pricing and payment functions of various financial services by a stable currency with sufficient value ( DApp internal tokens to fulfill more governance rights and incentives) Function). Before the basic token of the public chain itself has not completed sufficient value growth and stability, a safe and reliable stable currency is crucial to the development of the public chain ecology.

Since 2019 , the stable currency application Maker DAO has played a vital role in the ecology of ETH , greatly promoting the development of ETH financial ecology, but because it is an independent DApp endogenous stability mechanism, it is safe and reliable. Sexuality needs to be further fully verified, which limits its growth rate to some extent.

Second, the three major models of stable currency comparison, the short-term "funded currency mortgage" model has the greatest chance

Stable currency classification

Depending on the stability mechanism, stable currencies can be divided into two categories, one is asset-backed issuance, which is essentially similar to the gold standard system in the traditional international monetary system—issuing money through reserve gold; the other is imitation of the central bank. Supply and demand regulation, in essence, refers to the issue of currency and the stability of the currency price through the estimation of market demand and the dynamic adjustment of supply and demand in the currency-deficient system. In addition, in the asset-backed issuance model, it can be further divided into two categories based on whether the mortgage is a “funded asset” or a “blockchain digital asset”.

The first category: the legal currency asset mortgage issuance model

Such as: USDT, TrueUSD, GUSD, PAX, USDC, USDK, etc., issued with the US dollar 1:1 mortgage

The second category: mortgage issue on the blockchain digital asset chain

Such as: BitUSD, DAI

The third category: imitation of central bank supply and demand regulation

• Imitation of the central bank “bond repo” model: Basecoin

• Imitation of the central bank “adjust interest rate” model: NuBits

• Imitation of the central bank “selling foreign exchange to buy local currency” mode: Reserve, Terra

2. The main weaknesses of various types of stable coins

The core value of the stable currency and its main task is to maintain the relative stability of the price (in French currency). There are obvious defects and weaknesses in several existing stabilization mechanisms:

• The core risk of the Mortgage Mortgage model is the issue of the credit of the issuer's principal – how to ensure that the issuer reserves the full amount of the French currency and will not spam and run.

• In the blockchain digital asset mortgage model, the most important factor that will lead to the failure of the stability mechanism is the uncontrollable nature of the mortgage asset's own price, which is difficult in the current stage of the development of the blockchain digital asset market. avoid.

• Imitation of the central bank “bond repurchase” model and “interest rate adjustment” model, the core challenge is how to prevent investors from long-term bearish when the price of stable currency falls, refuse to accept the use of stable currency to buy “bonds” or increase stable currency savings. The essential problem is that the “bonds” and the “interests” of savings are not supported by themselves, and they are consistent with the overall system of stable coins.

• The biggest problem in the imitation of the central bank's “selling foreign exchange to buy local currency” model is that there is not enough “foreign exchange” reserves, that is, the stable currency issuer does not have enough funds to buy back a large amount of stable currency from the secondary market.

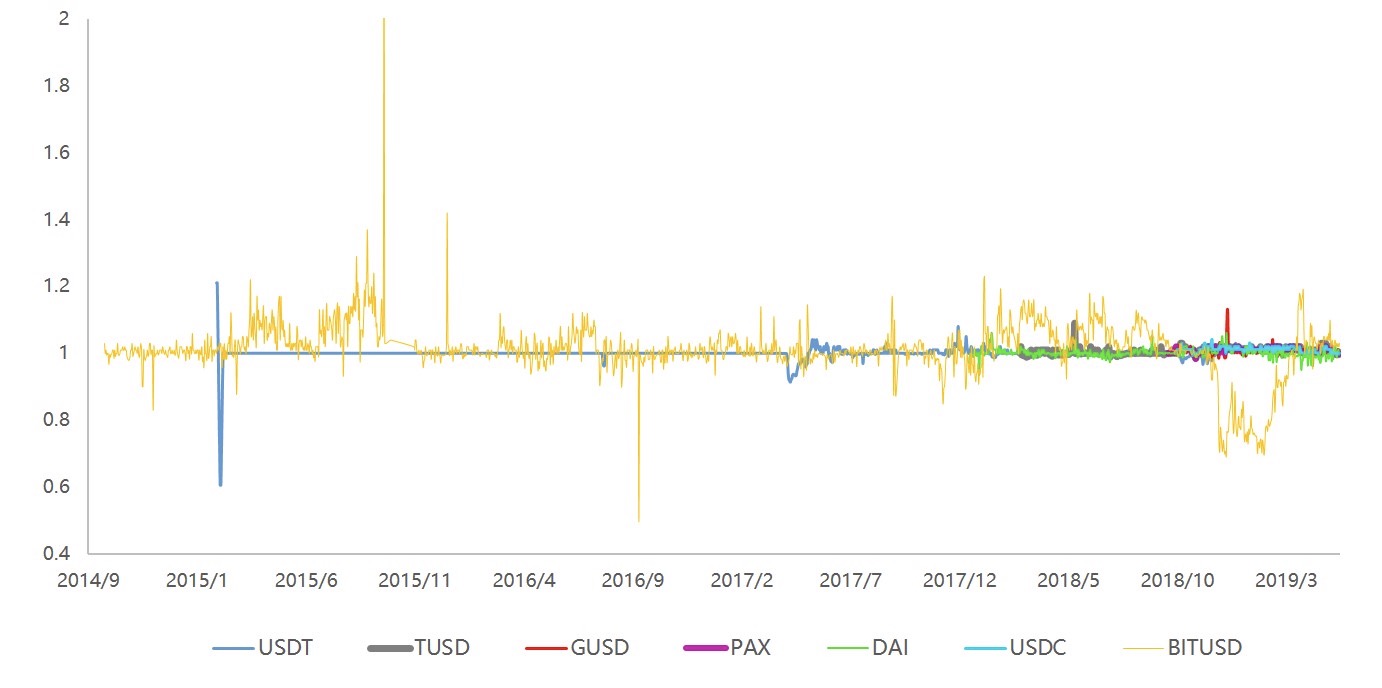

3 . Historical "stability" performance of various types of stable coins

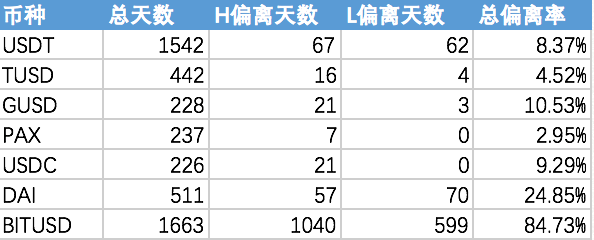

We have calculated the historical prices of stable coins that have been online in the various stable currency model representatives, including: USDT, TureUSD, GUSD, PAX, DAI, USDC, BitUSD.

According to the historical price performance of each stable currency, the stable currency of the “French Mortgage” model has the best stability. Among them, PAX has a price deviation (>3%) in the past 237 days, accounting for 2.95%; TUSD is in 442 days. The price deviation accounted for 4.52%; USDT in the past 1542 days, the price deviation accounted for 8.37%; USDC in the past 226 days, the price deviation accounted for 9.29%; GUSD deviation in the 228 days accounted for 10.53 %.

The stability of the “Digital Assets Mortgage Chain” model is significantly worse. DAI has accounted for 24.58% of the past 511 days; BitUSD has a deviation of 84.73% in 1663 days, which is basically unstable.

In the "imitation of central bank regulation" mode, the only NuBits currently on the line has collapsed and completely bid farewell to "stability."

On the whole, the stability of the legal currency mortgage model is the best, and with the addition of the emerging compliance dollar stable currency, its stability is gradually improved, and the credit risk of the issuer is expected to be effectively controlled. In addition, because the blockchain digital assets are extremely difficult to quickly get rid of the historical stage defects of “price fluctuations” and “insufficient liquidity”, and the value identification and adjustment of digital assets , the stability of the legal currency mortgage model is the best. And with the addition of the emerging compliant US dollar stable currency, its stability has gradually increased, and the credit risk of the issuer is expected to be effectively controlled. In addition, because blockchain digital assets are extremely difficult to quickly get rid of the historical stage defects of “price fluctuations” and “insufficient liquidity”, and the value identification of digital assets and the design of regulatory models may need to go through a relatively long development period. The blockchain asset collateral model and the stable currency that mimics the central bank's regulation mode are difficult to make breakthroughs in the short term.

At least in the next 2-3 years, the stable currency of the legal currency mortgage model will remain the main force in the stable currency market and have the greatest development opportunities.

Third, in the new round of competition for the French currency mortgage stable currency, compliance and ecological application will become the two major conditions for victory.

After the USDT, various types of legal currency mortgage model stable currencies are actively developing towards regulatory compliance and audit transparency. In particular, with the recent attempt by Bitfinex to misappropriate USDT's US dollar reserve funds to fill the deficit, the confidence of digital asset investors in stabilizing the currency has been greatly affected. Achieving security and credibility under regulatory compliance has become the primary issue that needs to be addressed in the current stable currency.

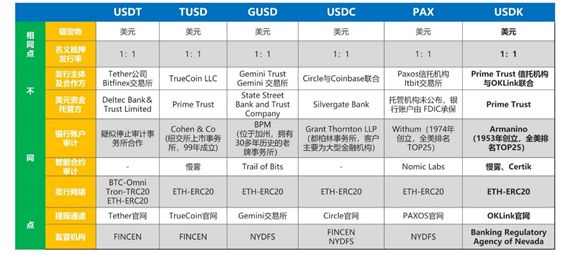

We conducted a tracking comparison analysis of the current major currency mortgage model stable currencies:

From the perspective of the custody of reserve US dollar assets, both TUSD and USDK are independently funded by the well-known US custodian PrimeTrust, which is more reliable than other custodians that are not explicitly disclosed or small custodians.

From the perspective of bank account auditing, in addition to the USDT suspected to stop auditing firm cooperation and long-term unpublished audit reports, several other stable currency bank account auditing institutions are well-known brands.

From the perspective of regulatory support, USDT's issuer Tether completed the FiNCEN registration in November last year after “streaking” for more than four years; several other issuers completed FinCEN in the early days of the launch of the stable currency. The registration of the Financial Crimes Inspection Bureau has either obtained the bitlicense of the NYDFS (New York Financial Services Authority) or has a banking license, and the compliance of the business entity is equivalent.

*Note: FinCEN is the Financial Crimes Inspection Bureau of the US Treasury Department. It is responsible for organizing, analyzing and restricting the dissemination of financial crimes, especially drug money laundering activities. According to the Bank of America Secrecy Act BSA, all money service business MSBs must be registered at FinCEN. FinCEN stipulates that Bitcoin trading websites and Bitcoin miners should be registered as money service companies and comply with anti-money laundering regulations.

The New York Financial Services Authority is the financial regulator of New York State. In 2015, the State of New York issued the Virtual Money Management Act, requiring all virtual currency companies to apply for the New York Financial Services Authority license bitlicense, and Ripple, Coinbase, Bitpay and other companies to obtain bitlicense.

Along with the acceleration of the stable currency 3.0 layout, a new round of financial ecological competition officially began.

Author: OK Research. Babbitt Information has carried out a deletion that does not affect the original intention. Original address

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Meet San Francisco in August, the second in 2019 than the original global developer contest

- How does decentralized MakerDAO make an "interest rate adjustment" decision?

- BM's "social" road

- Who is paving the way for big institutions? Scan the ecological landscape of the asset escrow industry

- Crazy BSV, and the logic behind it

- V God's proposed 99% fault-tolerant consensus: only 1% of honest nodes?

- Buy and buy, bitcoin "geek whale" accumulated 450,000 bitcoins in less than 9 months