The new pattern of staking: exchanges enter the market to explore the boundary, the pledge amount of service providers is not proportional to the income provided

Analyst | Carol Editor | Bi Tongtong | PANews

At this time last year, Staking was all the rage, and many players "run" to enter. In the past year, as more and more PoS public chains went online, the Staking market is becoming wider and wider. There are even voices in the market that this year may be the year of Staking.

Unlike the PoW mining market giants, which have high asset thresholds, Staking is regarded as a “new blue ocean” by mining pools, node service providers, and wallets. It is also an excellent opportunity to share mining dividends.

Above, PAData sorted out the expected annualized fiat currency returns of the 15 most valuable assets in the Staking market. And this article will take stock of the current status of the business of Staking suppliers, in order to fully show the development of Staking over the past year, and review the new changes after the current entry of the exchange.

- Eat Reason Rationally | Who is the real winner of the Steem incident?

- Comprehensive comparison of Chainlink, NEST, MakerDao oracles

- Wanxiang Blockchain Public Welfare Hackathon is coming to an end, Station B will broadcast the final road show live throughout

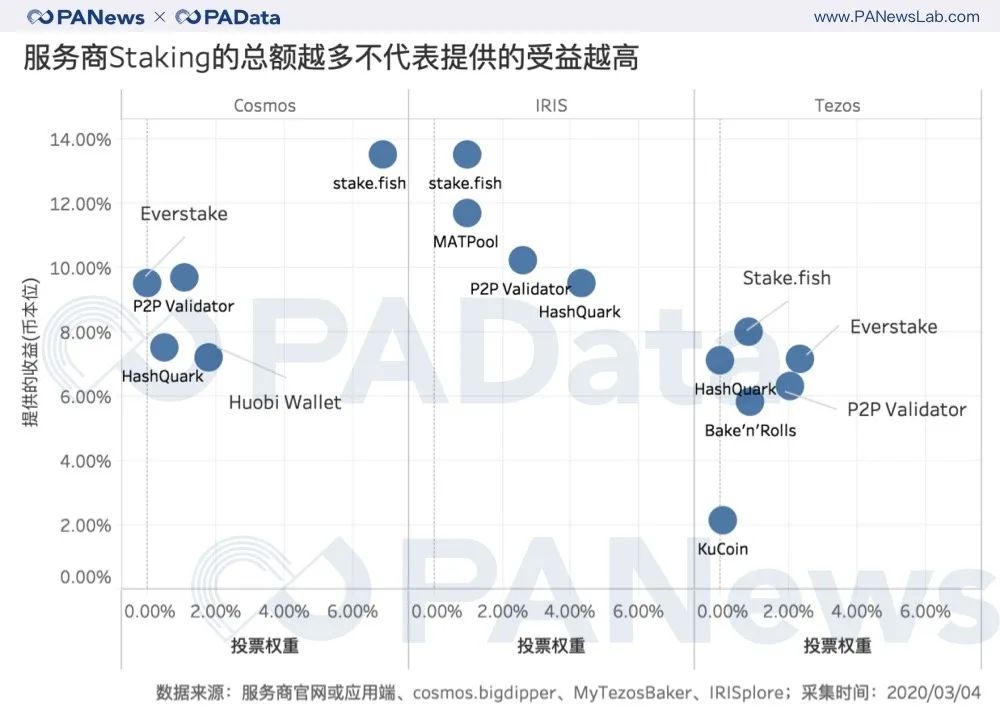

The more service providers Staking does not mean the higher the benefits provided

At present, Staking Rewards includes 82 Staking suppliers. PAData has selected 12 of them for in-depth analysis. These 12 suppliers cover the current major supplier types, including professional node service providers / mine pools, wallets. And exchanges.

In terms of business scale, My Cointainer is the largest Staking supplier, providing a total of 44 types of assets for Staking services, with an average currency standard return of up to 40.74%. However, from the perspective of specific asset nature, it mainly operates the Staking business for long tail assets. Therefore, the annualized income is much higher than other suppliers.

Most of the other suppliers can currently provide Staking services for 10-20 assets. Among them, the average annualized return of all assets with a higher currency standard is P2P Validator. The average return of 8 assets is 18.10%. The average return of 18 assets provided by HashQuark At 16.23%, the average return of the eight assets provided by OKEx Pool is 15.85%.

Compared with half a year ago, most suppliers have expanded their business scale. For example, My Cointainer increased the staking assets from 25 to 44, HashQuark from 10 to 18, and Cobo from 6 to 14. The expansion of business scale means that most service providers are still optimistic about the future development of Staking.

However, the total amount of Staking by the service provider, that is, the assets obtained from the user, is not directly proportional to the annualized income of Staking provided to the user.

PAData analyzed the relationship between the voting weight (pledged weight) of the three types of assets with a higher total amount of staking and more service providers (ATOM, IRIS, and Tezos) and the annualized returns of the currency standard. Businesses do not necessarily provide users with higher revenue.

For example, in ATOM's Staking, the voting weights of nodes operated by Huobi Wallet and HashQuark are higher than Everstake, but the latter provides higher revenue to users. Similarly, XTZ's Staking, Everstake's voting weight is higher than stake.fish, but the latter provides higher revenue to users. This situation is more obvious in IRIS Staking. HashQuark's voting weight is much higher than stake.fish, but it is also the latter that provides higher revenue to users.

Of course, the observation of local cases has limitations, but it still illustrates to some extent the fact that the voting weight of nodes is not related to the revenue provided by the service provider to users. The possible reason behind this is that the mechanism of staking makes the number of pledged tokens and mining income non-linearly related, but the number of pledged tokens is positively related to the probability of obtaining mining opportunities, so even if there are many tokens pledged by service providers, " "Luck" is not good, then the mining revenue will also be affected, and the revenue provided to users will naturally be affected.

Another possible reason is that the benefits provided are related to the cost of operating the nodes of the service provider. If the votes that become the nodes come from users and the service provider's self-delegation rate is 0, then its net income will be relatively higher and can be provided to users. The revenue may also be increased, but if the service provider's self-delegation rate is high, the cost is also relatively high, and the revenue that can be provided to users will naturally be affected.

Exchange entry expands staking boundaries

After a year of development, the player role of Staking has changed, and the exchange has entered the market. As a "gathering place" for asset flows, Staking by the exchange has a natural advantage. Currently, Coinbase, Kraken, Binance, Bitfinex, Coinone, Gate.io, OKEx, KuCoin, and MXC have all opened Staking services.

Among them, Coinbase and Kraken have become the two nodes with the highest total pledges on Tezos, exceeding 58.07 million XTZ and 28.61 million XTZ respectively, with voting weights of approximately 9.46% and 4.66%. Binance is the fourth largest node of Tezos, pledged 24.64 million XTZ, and the voting weight is about 4.01%. In addition, Binance is also the fifth largest node of Cosmos, pledged more than 9.06 million ATOM, and the voting weight is about 4.96%. And three of the top 6 nodes on EOS's pledge rate are related to the exchange: eosuobipool, okcapitalbp1, and bitfinexeos1, with voting weights of 3.03%, 2.97%, and 2.95%, respectively. Although the exchange ended late, it has quickly occupied an important position.

The exchange has also extended a new boundary for Staking, treating wealth management products that hold currency as interest and interest on leveraged borrowing as Staking, and has also broken through the requirements for lock-up voting with its own liquidity advantage.

For example, the Soft Staking product displayed on Kucoin's official website covers DAI, but DAI is not derived from mining. It is only after the Maker completes the upgrade that it integrates the DSR function, which makes DAI have the function of generating interest by holding coins. In the business introduction of the mining pool, leveraged lending and the "USDT Matcha Po" currency-bearing interest-generating business are listed as PoS mining types. Binance's official website has made the Staking business a "return on holding positions" and has broken the requirement for hedging of products such as Cosmos that require hedging of Staking. However, it should be pointed out that this operation is undoubtedly potentially risky, and the exchange's description of the position rebate product does not explicitly entrust the authorization relationship.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Viewpoint | Blockchain technology has become a new impetus for the development of "new infrastructure"

- How to use threshold signatures to generate random beacons?

- Swiss Crypto Valley Association Chairman: Central bank digital currency is the next stage in the development of decentralized finance

- Perspectives | Why Should You Hold Bitcoin?

- Babbitt Column | Pan Chao: Automated Market Maker DEX Economics

- Bitcoin Secret History: How Dorian Nakamoto became Satoshi Nakamoto?

- India's central bank plans to file review of Supreme Court's crypto ruling