Editor's note: This article has been deleted without changing the original intention of the author.

DeFi has become one of the key growth areas of Ethereum since 2019. Other competitive public chains are also building DeFi products, but they are much slower. The number of DeFi clients based on Ethereum is still very small, with an average of more than 40,000 users per month, of which 90% of users are using decentralized exchanges.

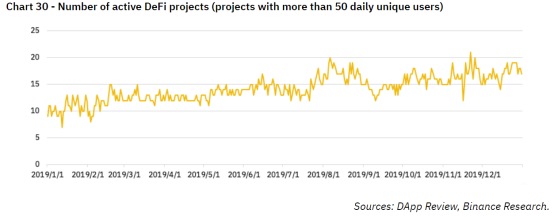

At the same time, as more and more developers are developing new products and establishing new services, the number of active projects with more than 50 daily users almost doubled in 2019.

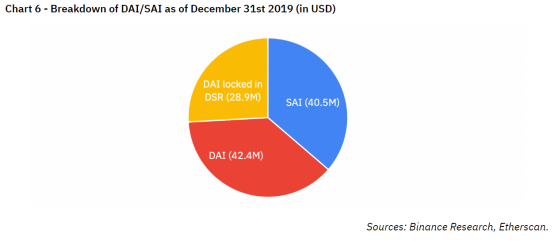

Since its establishment, the field of DeFi has been dominated by SAI / DAI. SAI / DAI is a decentralized stablecoin generated in the MakerDAO ecosystem, and its MCD (Multiple Collateral DAI) was released in November 2019. Since then, the migration between SAI and DAI has occurred quickly. As of December 31, 2019, it is estimated that 64% of the supply has been converted.

The inclusion of USDC into multiple DeFi platforms poses challenges to DAI due to factors such as a richer supply of USDC, different dynamics of interest rates, and stronger anchor price stability.

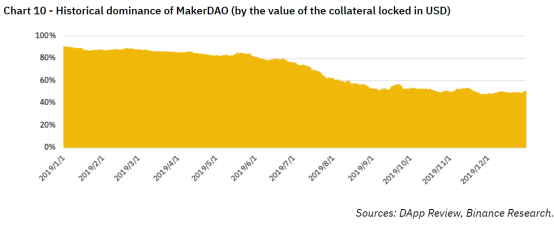

Measured by the total value of DeFi-locked collateral, lending platforms like Compound are increasingly challenging Maker's dominance.

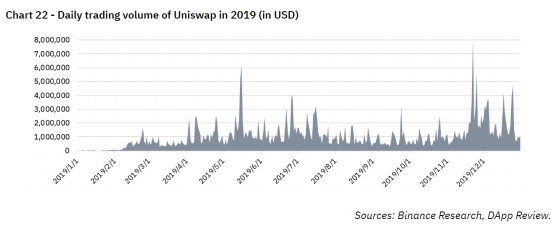

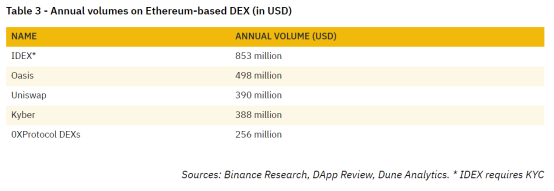

The trading volume of the "2.0" decentralized exchange also increased. Uniswap has over 19,000 users and an annual transaction volume of $ 390 million. Similarly, Kyber has more than 35,000 users and an annual transaction value of $ 387 million.

In 2020, we expect that new developments in Ethereum-based DeFi (such as derivatives, under-secured initiatives, the addition of ERC-20 USDT, etc.) will become a basic component of DeFi. Moreover, more Defi projects will be assisted by more outstanding cross-chain interoperability solutions.

DeFi (Decentralized Finance) has become one of the most important areas of Ethereum, with more than 100 projects and teams building applications and protocols for it in 2019. Binance Research began writing a series of reports on decentralized finance in June (the "DeFi Series"); this third report discusses the latest developments and key narratives in the DeFi field, focusing primarily on Ethereum, while also considering other districts Block chain. Most of the data used in this report is provided by DApp.Review, a new member of the Binance ecosystem.

DeFi's growing importance in Ethereum

As we stated in our report on the tokenized world, Ethereum has a wider range of applications than other blockchains. However, as we discussed earlier in the Ethereum-based DeFi report, its main focus has shifted to exchanges and financial applications.

DeFi includes (decentralized) exchange services and financial applications such as lending markets, asset management services, and payment solutions.

In 2019, the price of Ethereum fluctuated between $ 100 and $ 350, with a median price of $ 173. Regardless of the price, so far most decentralized financial ecosystems are built on Ethereum.

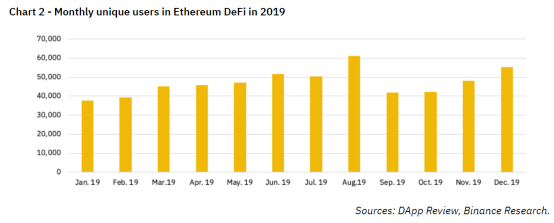

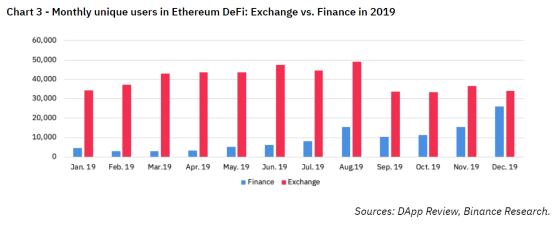

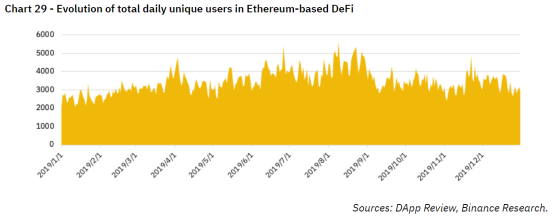

In 2019, the number of independent DeFi users per month is between 40,000 and 60,000. However, there are significant differences between the number of users of financial applications (e.g., lending platforms) and exchange services (e.g., currency trading platforms).

In January 2019, the number of unique users per month for decentralized exchanges was 34,244, while the number of unique users for financial applications was 4,649. During 2019, the number of DEX users increased and reached a peak of 48,934 in August 2019, before falling back to near the original level, with 34,033 users in December. On the other hand, the number of users of financial applications has continued to grow since January. In August, its monthly user number exceeded 10,000. In December, the number of unique users of decentralized financial applications on Ethereum reached 25,925.

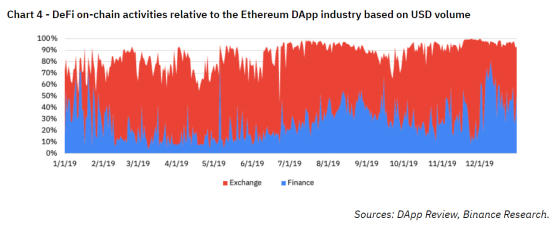

This chart represents all on-chain activity, which may include some exchanges that are not fully decentralized (e.g. IDEX). As shown in the figure above, more than 90% of the on-chain transaction volume in Ethereum-based DApps comes from DeFi-related applications. From a user's perspective, DeFi is the growth highlight of Ethereum in 2019. In short, Ethereum and DeFi have become a two-headed monster, each further developed and driven by the other. The main characteristics of their interaction will be defined in the next section.

Explore the interior of Ethereum DeFi

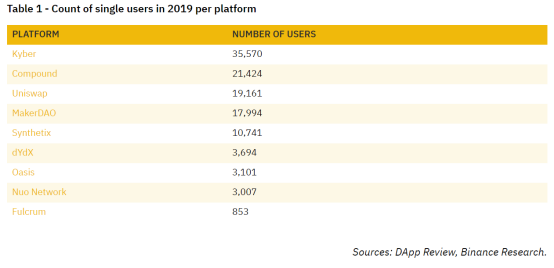

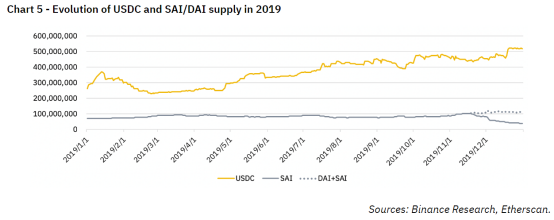

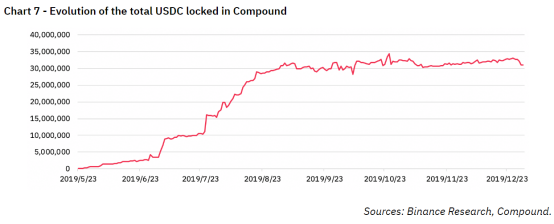

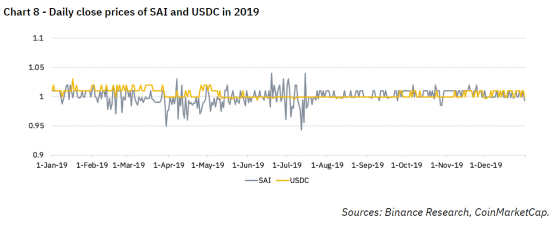

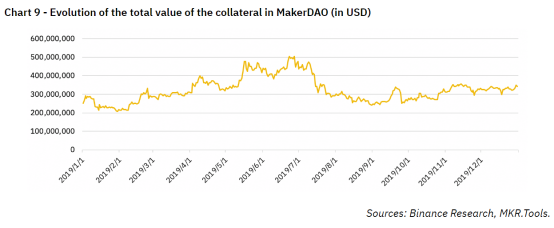

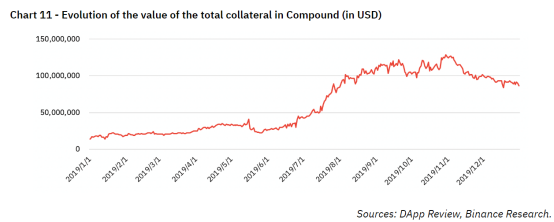

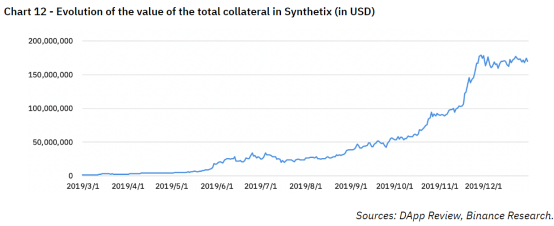

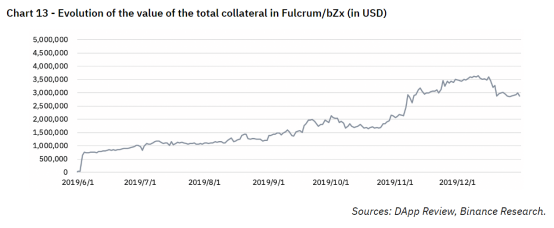

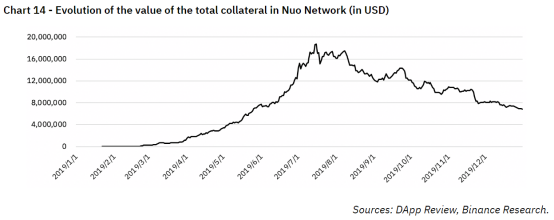

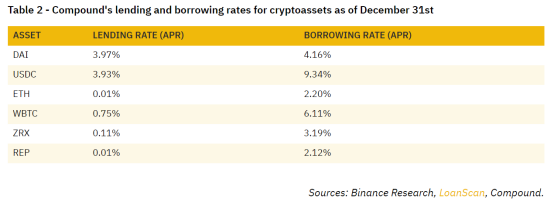

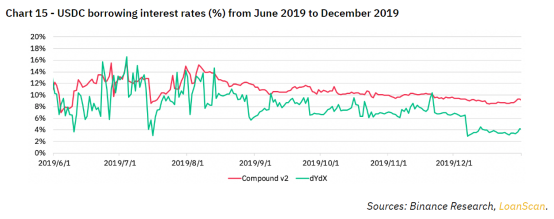

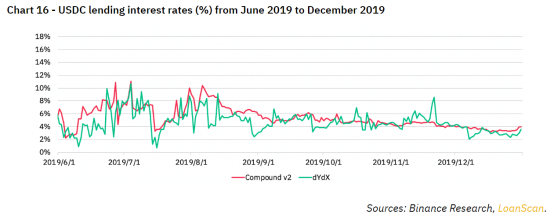

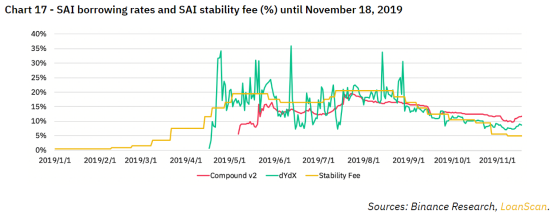

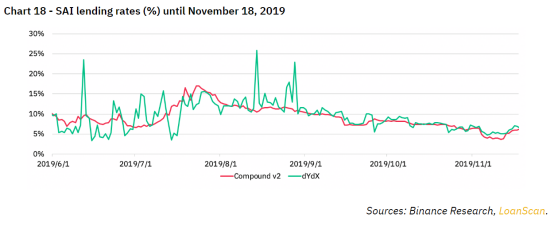

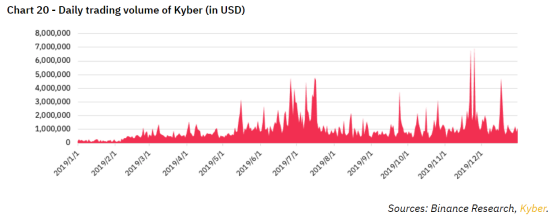

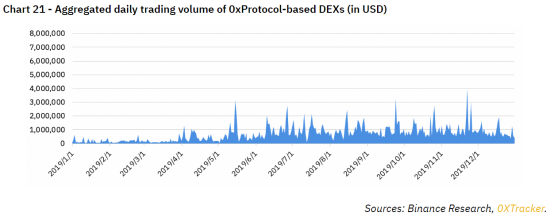

As shown in Table 1, the total number of independent users for each platform varies greatly in 2019. Kyber is the project with the largest number of users in DeFi, with a total of 35,570 unique users in 2019. In DeFi, Compound is the second most popular project and leads the way in the "financial" sub-category. However, these figures do not necessarily indicate the overall use of these underlying assets supported by the agreement. For example, DAI coins can be used without interacting with MakerDAO smart contracts (e.g., transactions, payments). Similarly, ctoken (Compound) and iTokens & ptoken (Fulcrum) can be exchanged outside the protocol. As tokens become more widely available, the statistics we need to pay close attention to are their average daily transaction volume and the number of active addresses that hold them. 2.1 USDC: The nemesis of DAI On the basis of DeFi, the decentralized stable coin-DAI generated from the MakerDAO protocol has been the core of DeFi in history. However, in 2019, the statutory mortgage stablecoin issued by the Centre Consortium-USD Coin (USDC)-became its nemesis. As shown in Table 5, the total supply gap between USDC and DAI is accelerating in 2019. Part of the reason is that the DAI of a single collateral is limited by a 100 million supply cap (as the debt ceiling of the Maker ecosystem). However, the agreement did not vote until November to increase the supply cap to 120 million. This is the first increase in the supply cap since 2018, when the supply cap was raised from 50 million to 100 million. At the same time, the supply of USDC increased from 261.3 million to 518.5 million in 2019, an increase of 98.4%. In contrast, the total supply of SAI and DAI increased by only 60.4% year-on-year, from 69.6 million to 111.6 million. With the increase of USDC's total market value, the use of USDC as collateral has also steadily increased in 2019. As of December 31, the USDC provided to the Compound agreement alone exceeded 30 million, accounting for more than 25% of the total value of all DAI / SAI in circulation. On May 23, Compound increased its support for USDC. In September, the amount of USDC provided to the Compound agreement increased rapidly, with the total amount of USDC pledged exceeding 30 million. Since then, the number of mortgages has remained at this level. However, increasing the total supply of USDC is not necessarily the only reason, but USDC is becoming increasingly popular in the DeFi world. As shown, the price stability of USDC is also higher than DAI in 2019. Finally, increasing the supply of DAI results in variable borrowing costs (stabilization fees paid by MKR holders), while increasing the supply of USDC generates only negligible costs (available from Centre). Stability costs are discussed in depth in Section 2.3. 2.2 Lending platforms like Compound and Synthetix are increasingly challenging Maker's dominance As the supply of DAI continues to increase (see 2.1), Maker's own collateral value has also shown a positive net increase. In the first half of 2019, the total value of collateral in MakerDAO increased due to the rise in ETH prices. Similarly, this ratio declined in the second half of 2019. However, more ETH was added to the platform, and the supply of SAI (then SAI + DAI) also increased. Therefore, by 2019, the total value of MakerDAO's collateral increased from $ 249 million to $ 342 million, a 37% increase. At the same time, the price of ETH fell by 2% in 2019. However, despite the increase in the total amount of collateral locked by MakerDAO, its "DeFi advantage" declined in 2019, from about 90% in January 2019 to less than 50% in December. Specifically, MakerDAO will be challenged by two major platforms in 2019: Compound and Synthetix. The value of Coumpound collateral, denominated in U.S. dollars, increased from $ 13.4 million at the beginning of the year to $ 86.3 million at the end of the year, an increase of 541%. Even more impressive is that Synthetix's total collateral value rose from $ 1.6 million on March 1 to over $ 160 million (EOY) due to the rapid rise in SNX prices. So far, the main asset generated in the Synthetic ecosystem is sUSD (Synthetic USD), which is mainly supported by SNX tokens. As of December 31, its supply was about 11 million. However, SNX's liquidity (based on orderbook data) is not as good as digital assets like BAT and ETH, which are two eligible collaterals in the MakerDAO ecosystem. Therefore, it remains to be seen how the system will perform under the highly volatile SNX price. Although the price of ETH is relatively lagging (see Table 1), the total collateral value of other small DeFi platforms will also increase significantly in 2019. We use Fulcrum and Nuo Network as examples to illustrate trends throughout the year. bZx showed a modest and steady increase in the total value of collateral locked on the platform. Starting from June 2019, the value of its collateral has rapidly increased to $ 2.7 million in just 6 months without a dedicated collateral. The total collateral of the decentralized margin trading platform Nuo Network grew rapidly in the first six months, reaching a peak of more than 17 million in July and August. Since then, the total amount of collateral it has locked has steadily declined, in part because of the decline in the price of the locked assets. 2.3 High volatility and spreads in the DeFi interest rate market According to the table below, interest rates for different assets vary widely. For example, 0x token (ZRX), Augur (REP), and Ethereum (ETH) have the lowest average annual interest rates. In contrast, only ETH and REP have the lowest borrowing rates (2.20% and 2.12%) because ZRX has a much larger spread. The stablecoin lending rates like DAI and USDC are the highest. Parity interest rate parity suggests that ETH and other digital assets may be undervalued. On the other hand, sometimes it is cheaper to implement specific trading strategies for ETH and BTC (via WBTC) than on many centralized exchanges such as Binance. However, the liquidity (book depth, trading volume) of centralized exchanges is still much higher than that of decentralized exchanges. Since June 2019, USDC's borrowing rates have fallen. Although the interest rate of dYdX fluctuates greatly, its borrowing rate on USDC is almost always lower than that of Compound. Since June 2019, USDC's lending rates have been steadily and slowly falling. Although the spread between Compound and dYdX is much lower than the borrowing rate, the volatility of the dYdX USDC loan rate is again higher than that of Compound. The stability fee set by MakerDAO is mostly higher than the market borrowing rates of Compound and dYdX. Until mid-September, the compound borrowing rate has been lower than the stabilization fee. At the same time, due to the emergence of more sensitive interest rate formulas, dYdX shows higher lending rates. This stabilization fee premium can be explained in a number of ways. First of all, the stable fee rate is regularly raised (government voting every week), and the interest rates of Compound and dYdX are always real-time, reflecting the real-time market dynamics. Therefore, users must price the volatility they may face in an open loan pool. In addition, as more smart contract insurance platforms such as Nexus Mutual and derivative protocols such as UMA Protocol gradually grow, users may have more options in the future to accurately price this risk. However, with the introduction of multi-collateral DAI (MCD), stabilization fees quickly fell below the opening prices of Compound and dYdX. In addition, arbitrage opportunities exist, similar to those described in our previous report. Specifically, ETH coin holders can borrow DAI from dYdX and deposit it to earn a DAI deposit interest rate higher than the borrowing rate (for example, through Oasis). Although the scope of DeFi is expanding, its market size is still small. Therefore, the interest rate fluctuations of DeFi are highly dependent on the specific factors of the platform (such as different lending market environment, fee structure, etc.). 2.4 Development of the "2.0 Decentralized Exchange" In 2019, the daily trading volume of many decentralized exchanges has grown rapidly. Kyber's trading volume has increased in 2019, peaking from June to July and late November (the daily trading volume reaches a maximum of $ 7 million). At the same time, the total value of the collateral it locks in is also growing rapidly. By January 1, 2019, it was worth about $ 500,000. By the end of 2019, the total value locked in Kyber is about $ 3.4 million. It is worth noting that 0X Protocol-DEX includes Raday Relay, DDEX, imToken (ex-TokenIon), Paradex and DeversiFi. Since early 2019, the total transaction volume of 0xprotocol-based DEX has been increasing. In 2019, their average daily transaction volume reached $ 702,000. The total value of Uniswap-locked collateral has also experienced an alarming increase. By January 1, 2019, it was worth about $ 500,000. By the end of 2019, the total value locked by Uniswap is approximately $ 28 million. Despite the impressive growth patterns of Uniswap and Kyber in 2019, their annual turnover is still lower than the two oldest Ethereum decentralized exchanges, Oasis (operated by Maker) and IDEX (requires KYC). Although Ethereum is the main platform for DeFi builders, "non-Ethereum" blockchain developers are also working on developing and researching DeFi applications and protocols.

Alternative DeFi (Alt-DeFi): heterogeneous but mostly lagging

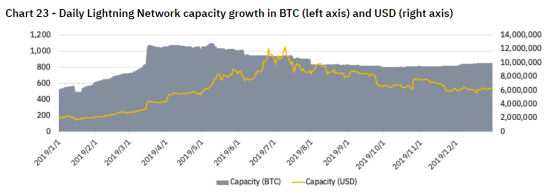

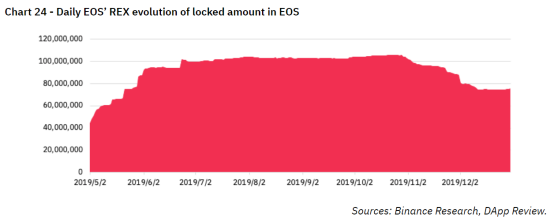

In this section, we will explore what we define as "Alt-DeFi": an alternative to DeFi outside of Ethereum. Alt-DeFi applications run on various blockchains, such as EOS, Binance Chain, Bitcoin, Cosmos, etc. Regarding the current status of DeFi's BTC, its main application is related to payment. Specifically, some solutions have been developed to improve the scalability of BTC for small payments. The most prominent example of this is the Lightning Network, which operates as the second layer of BTC. Lightning Network's data is difficult to get accurate estimates. However, due to its total capacity of approximately 854 BTC (ie, $ 6.2 million), it is more difficult to adopt. So far, only one important exchange (Bitfinex) has adopted Lightning Netword for BTC deposits and withdrawals. On the other hand, EOS has also shown market participants' interest in the business. First, EOSREX, the lending platform for computing resources in the EOS ecosystem, went online in April. Since its creation, this application has shown a significant increase in the resources available to the platform. However, since more resources are provided than borrowed resources, there is a serious imbalance in the dynamics of supply and demand. However, in the fourth quarter (as of December 31, 2019), the total amount of EOS provided decreased from a maximum of 105 million EOS to 75.6 million EOS. In addition, although the Kyber network is very popular in Ethereum, its team has also implemented Ethereum-based KyberSwap on other blockchains:

EOS: YoloSwap

TomoChain: TomoSwap

ETH / EOS cross-chain: Waterloo (not yet implemented)

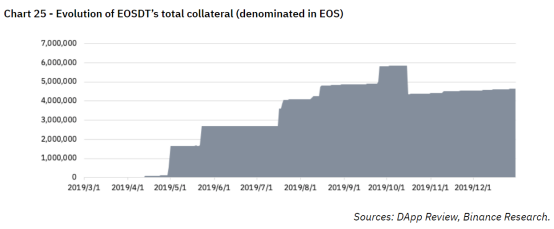

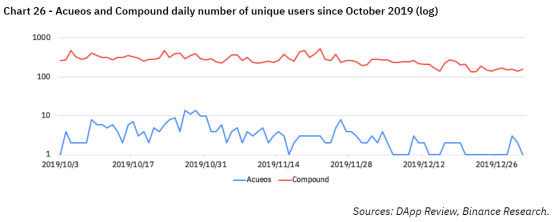

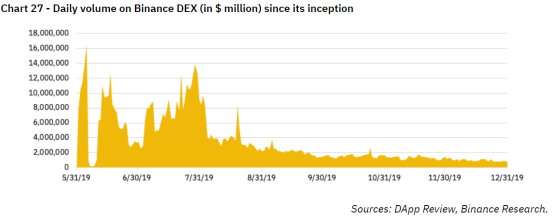

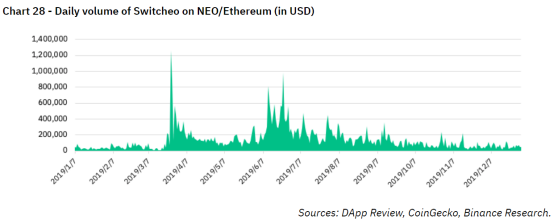

Similarly, the success of MakerDAO and Compound in the Ethereum field has led to the creation of similar platforms on competing blockchains. In the EOS ecosystem, the Equilibrium protocol works similarly to MakerDAO. The corresponding currency of DAI is called EOSDT, and the eligible collateral is EOS. However, Equilibrium's mortgage requirement is 130%, which is slightly lower than Maker's 150%. Since its creation, EOSDT has shown significant growth. As of December 31, 2019, the total value of the collateral it locked was estimated at more than 4 million EOS. However, its total market value is still relatively small, about 1.8 million EOSDT. Similarly, Acueos is an EOS implementation of the Compound protocol. Unfortunately, it has not been as widespread as Compound, as shown in the table below. In addition, Cosmos also has a similar project (like Maker), focusing on crypto-linked stablecoin supported by fiat currencies: Kava. On October 23, Kava successfully raised funds on Binance Launchpad. At the same time, NEO also has its own project similar to MakerDAO, called Alchemint. In this project, SDUSDs are generated by staking NEO. As of December 31, 2019, there were less than 60,000 SDUSDs issued on the Alchemint platform. PEG Network also launched its own MakerDAO-style debt-collateralized smart contract that allows users to deposit Bancor Tokens (available on the Ethereum and EOS chains) to print USDB. It is also worth noting that many traditional decentralized exchanges exist on many blockchains, such as Binance Chain (Binance DEX), NEO (such as Switcheo), EOS (such as NewDEX), and Tron (such as PoloniDEX). For example, Binance DEX was launched on March 23, 2019. Since June 2019, its average daily trading volume has been gradually decreasing. For most of this year, its trading volume has remained above $ 1 million. In the first nine months, the total transaction volume of Binance DEX was $ 755 million. Switcheo provides a decentralized exchange with full interoperability between the two blockchains on NEO and Ethereum. In 2019, Switcheo's total transactions for the year totaled $ 49.5 million. Other exchanges with cross-chain interoperability include Bancor Network (EOS / Ethereum) and other ongoing projects such as Thorchain. It runs its own IDO on Binance DEX. In addition to other blockchain interoperability DeFi applications, Loom Network has been working to introduce DeFi to alternative large market blockchains such as Tron and Binance Chain.

DeFi Paradox and 2020 Perspective

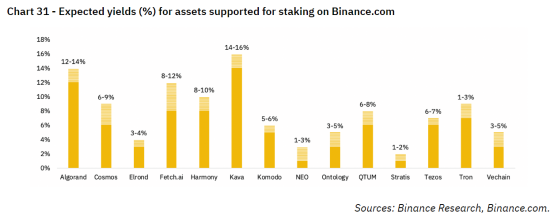

4.1 DeFi: a small and dynamic ecosystem Although DeFi represents a small part of the crypto industry, it is one of the most dynamic areas. On average, the Ethereum-based DeFi platform showed the number of daily unique users of 3456 users in 2019. The number of active projects (projects with more than 50 independent users per day today) has nearly doubled from 2019. However, this number is still small in absolute numbers, as fewer than 20 items are used. In addition, DeFi is still only a small part of the encrypted space. For example, locked collateral is worth about $ 6 billion, more than five times the total DeFi collateral. Finally, the size of DeFi is still insignificant compared to the (traditional) fixed income market. A recent estimate of the size of the debt market in 2019 is about $ 250 trillion. In the United States alone, consumer loans in 2019 are estimated to be as high as $ 1.6 trillion. 4.2 Staking growth Unlike borrowing, staking is performed at the protocol level. Users lock funds to ensure network security and then receive staking rewards. This is discussed in depth in our report on the rise of Staking. Since Staking is performed on the first layer of the blockchain, any rational digital currency holder should trust the Staking protocol. Therefore, we expect more and more investors and long-term investors to participate in on-chain management and other activities. According to StakingRewards.com, as of December 31, the cumulative market value locked in the Staking agreement is estimated to be $ 6 billion. This number will increase significantly by 2020, as more Staking-based protocols will launch their main networks, and Ethereum will switch from PoW to PoS. However, due to promised higher lending rates, loans may be replaced by staking. However, as of December 31, the funds locked in DeFi were worth about $ 670 million to Ethereum and about $ 200 million to EOS (mainly from EOSREX). We also look forward to merging into large-scale Staking services provided by digital currency exchanges (such as the Staking services of Binance, Coinbase, and KuCoin) and specialized providers. Will staking lead to centralization through economies of scale? However, as our recent institutional report shows, large traders and institutional investors believe that staking is not yet one of the key growth drivers for the crypto industry. Is the launch of the Ethereum beacon chain expected to shake the industry? 4.3 DeFi on Ethereum In 2020, we expect the following trends in Ethereum-based DeFi:

The end of Maker's dominance: We expect that Compound will take over from Maker in 2020, both in terms of output and number of locked positions. In addition, Synthetix may challenge Maker because it provides greater flexibility for assets that can be linked to Synths, such as Silver Ounce / sXAG or inverse BNB / iBNB. However, the collateral used by Synthetix is still linked to illiquid assets (SNX), raising concerns. In contrast, all assets used as collateral in Maker are highly liquid.

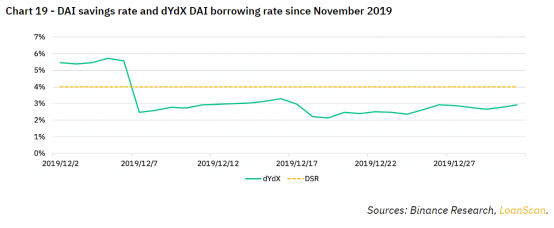

Maker's DSR integration: Although we expect that Maker's dominance may be challenged, it will still be one of the core products of the DeFi industry. Although new collateral (such as BAT) has received most of the attention, the Dai Savings Rate (DSR) may become one of the most important interest rates in the DeFi space. For example, Fulcrum has integrated DSR into its platform. Exchanges that include DAI in trading will also continue to include DAI savings rates in exchanges.

The hazards of less or even less- mortgaged solutions: As we discussed in our first report on DeFi, over-guaranteeing will not help people without funds. We are considering new solutions such as social capital recovery, credit scoring, zero-knowledge proof and credit market DAO. We also look forward to further leveraging the time value of monetary relationships, allowing users to borrow on future promised cash flow commitments. Sablier's experiments may pave the way for dedicated protocols. In early 2020, Aave (LEND) will transfer its lending market from the current test network to the main network.

DeFi derivatives are released on the Ethereum mainnet: The Convexity protocol and other protocols (such as the UMA protocol) are likely to bring new trading opportunities to the DeFi space. However, from the perspective of option underwriters, people remain skeptical about how to manage risks and returns. In addition, hedging solutions for DAI price risk, such as SwanDai, may also be deployed on the mainnet.

USDT is integrated into some DeFi protocols: As most of the circulating supply of USD Tether migrates to Ethereum, it is likely to be integrated into some DeFi protocols in the near future. For example, the Compound protocol will include USD Tether.

Growth of "one-stop" solutions: Platforms like Zerion and InstaDApp are designed to provide a better user experience and simplify the use of DeFi. Specifically, these single UIs allow interaction with various platforms. In addition, protocol aggregators like DeFiZap and Dex.ag deserve attention. Because they usually allow users to minimize gas costs and avoid the risks of specific platforms.

4.4 Alt-DeFi Extensions We look forward to some developments on non-Ethereum DeFi from the perspective of other blockchains, such as: BTC may play a more important role in DeFi, either in Ethereum or as a standalone solution.

BTC as collateral: BTC is the largest digital asset by market value, and may be added as collateral in MakerDAO (such as tBTC, WBTC), and further adopted in established Ethereum-based DeFi applications. SODA also allows the borrowing of ERC-20 tokens with BTC as collateral.

BTC side chain: DeFi on the BTC side chain may also cause more attention and research. Platforms like Money On Chain serve this purpose.

Binance Chain: Due to the existence of BEP-3, DeFi on Binance Chain may attract the attention of crypto participants. Loom Network's early initiatives demonstrate the growing interest in DeFi from third-party donors.

EOS: Should have greater synergy with Ethereum (e.g. Bancor, Kyber). Also, as mentioned in the previous section, it is developing its own DeFi ecosystem.

NEO: NEO has SDUSD minted in the Alchemint ecosystem, and the Switcheo exchange running on both the ETH and NEO blockchains. We expect to implement more DeFi solutions in 2020.

Cosmos: Kava is expected to be used in 2020, which may mark the birth of Cosmos' first decentralized stablecoin. Kava plans to include collateral such as XRP and BNB.

Tezos: DeFi was explicitly added to the new RFP by the Tezos Foundation for ecosystem grants in September 2019.

Algorand: The Algorand Foundation specifically mentioned its interest in the "DeFi movement" in a statement issued in November 2019.

Ontology: By adding support for PAX in its network, its goal is to develop DeFi use cases on the chain, as announced in August 2019.

Although the Alt-DeFi space may grow in 2020, it remains to be seen whether most users will be willing to use these services.

4.5 Summary

In this report, not all platforms and protocols are discussed. Because the scope of this industry is too broad to analyze in one report. For example, asset management platforms (such as Set Protocol and Melon) and repeaters (such as Loopring) were not included in the discussion.

We believe that DeFi is expected to further attract the attention of industry participants. However, so far, most use cases have been confined to the existing crypto community.

In addition, this report also includes decentralized exchange applications as part of DeFi, but the scope of DEX is usually beyond the field of DeFi.

In the future, once some technical and legal challenges are resolved, we expect that the decentralized financial industry will develop rapidly and may attract individuals and capital beyond the existing crypto industry.

In summary, the rapid development of DeFi has spawned an active and creative global community, laying the first step to challenge traditional financial platforms.

Is the world ready for the borderless state of DeFi?

We will continue to update Blocking; if you have any questions or suggestions, please contact us!