After the new SEC regulations, the cryptocurrency change geometry?

With the further consumption of market stocks, the market will eventually face adjustments, and the release of regulatory details will eventually lead to a return to value or constitute an obstacle? Clearer regulatory standards and more stringent regulatory boundaries are often one step away.

In the bear market, the currency circle was ruined for nearly a year, and it suddenly attracted a strong increase last week. So far, bitcoin prices have been difficult to stand up to the $4,200 shock rate, and have experienced rapid straight-line and sustained heavy volume gains. The highest bitcoin price has once stood at $5,400.

Regarding the factors that promote the rise in the price of this round of currency, the current industry has a high degree of recognition. There are two main sporadic factors. One is due to the fact that on the day of April Fool’s Day in the United States, the foreign media released an entertainment only. The "US Securities and Exchange Commission (SEC) accidentally announced the approval of the listing of two Bitcoin exchange-traded funds (ETFs)." Another reason was that the mystery buyer bought 20,000 bitcoins (worth $100 million) in three exchanges on Coinbase, Kraken and Bitstamp on the same day, which triggered a large number of quantitative trading orders.

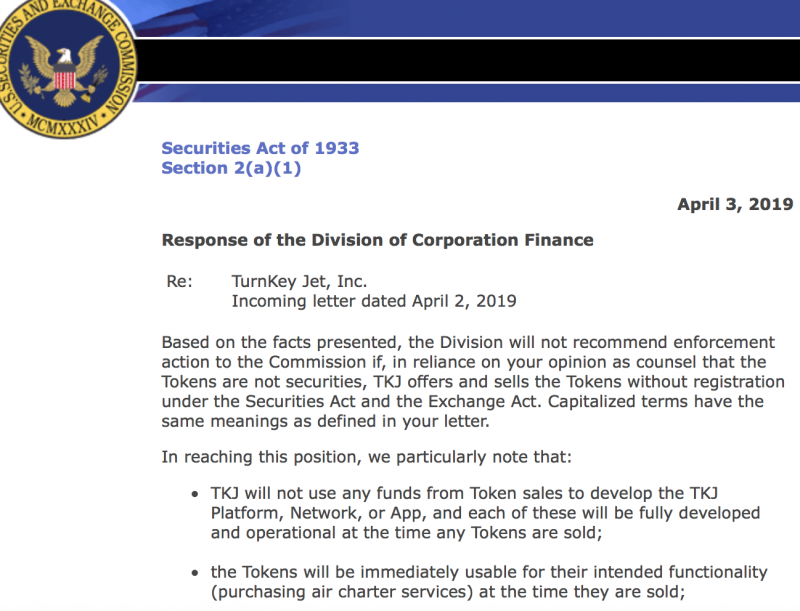

Immediately after the evening of April 3, the US Securities and Exchange Commission (SEC) issued a "Framework for "Investment Contract" Analysis of Digital Assets". In this note, the SEC provides a framework for analyzing whether a digital asset has a particular type of security feature (ie, an “investment contract”), as well as an ICO inquiry submitted by the former business travel startup TurnKey Jet on April 2, 2019. The letter responded.

- Why did the USDT at the time of the big rise suddenly increase by 300 million?

- Who is Hodlonaut? CSW is looking for him, the Bitcoin community is protecting him.

- How does the virtual currency mine circle respond to the “elimination” crisis?

The reason why this regulatory guide is regarded as a good news level is that this is the first time that the SEC has issued an investigative report on the DAO incident since July 2017, and determined that the DAO token is a securities subject to federal law. A “no objection” letter was issued for the sale of tokens for specific conditions, and it was determined that the token TKJ issued by TurnKey Jet was not a security.

In this regard, some insiders told the financial network that this is not a good news, and if it is only for TurnKey Jet to issue a Token through regulatory approval, it is more like an example. There is not much for other cryptocurrencies. Reference value.

Looking back on the past week, this round of rising prices is not seen by most industry insiders as a signal that the market is really warming up. As of press time, the BTC continued to pull back, and the price has fallen successively, falling below $5,000. After the release of the new SEC regulations, in addition to the previous blind optimism and the subsequent over-interpretation, what else is worth looking forward to in the cryptocurrency market?

After the heat, the TurnKey Jet was quickly forgotten by the market.

According to a recent report by Crypto Insider, Taylor Monahan, CEO of blockchain wallet tool MyCrypto, believes that the SEC's guidance framework and “no-action” letter provide little new information, Monahan commented: “This is for the encryption ecosystem. The system is not important, because no one will deploy tokens that are essentially a peculiar gift card, arcade game currency or membership plan."

This type of evaluation of TurnKey Jet tokens has almost become an industry consensus. The industry generally believes that this case does not really touch the core issue of token distribution, and therefore, there is not much reference value for other projects that want to be approved to issue tokens.

This mainly reflects the gap between market expectations and actual regulatory processes. What is the revelation of TurnKey Jet's token distribution to the industry?

Looking back at the SEC, it is determined that the conditions under which TurnKey Jet is not subject to the securities of the wholesale bank are:

1. The money sold by the token will not be used to develop the company platform, network, or APP;

2. Tokens can be used immediately for the intended function (purchase charter service);

3. The token can only be transferred to the company's own TKJ Wallets wallet, not the wallet outside the platform;

4. Each token is sold at a price of one dollar and each token represents the charter service that the company must provide equivalent;

5. Repurchase tokens must be repurchased at a discount of the face value of the token, unless the court in the US orders the company to liquidate the token

6. TurnKey Jet cannot claim that the market value of its tokens may increase.

Judging from the above restrictions on tokens, TurnKey Jet won the token of the wholesale bank. The main feature is that, first of all, the funds raised by the token sales cannot be used for development, and can only be used for the specific services of the company. Secondly, the price is fixed at $1 and there is no possibility of adding value; in addition, there are strict and detailed restrictions on token repurchase and storage.

Judging from the use of this token, Zhang Jin, a lawyer at Beijing Jincheng Tongda (Shanghai) Law Firm, told Finance Network that if the token cannot be used for project development, it cannot promise to bring in profits, then this time it will It is not a securities in our traditional sense, it does not have investment properties, so it certainly cannot be managed as a security. The token at this time is not a token in the usual sense. For other cryptocurrencies, there is not much reference.

What is more noteworthy is the restriction on the price and transferability of the token. TurnKey Jet lost all the value-added space in the wholesale token, and lost the most attractive value of the cryptocurrency. Imagination.

Li Lianxuan, a senior researcher at the OK Group's research department, told Finance Network that the token is more like Q coins. It mainly provides airlines' point services. He further explained: "If the future digital currency is issued like this, it will cost $1. The fixed price, the funds can not be used for project development, the repurchase can only be based on the first denomination price, then the coin is not developed as a digital currency, which will at least disappoint half of the investors and developers, there is no selling point at all. There is no room for appreciation. If the subsequent currency is based on this standard, why should it be issued?"

So, why does TurnKey Jet have to implement the functions that the previous points can achieve by issuing digital currency? As can be seen from TurnKey Jet's official website business, this is an American interstate airline leasing company for private airline charter services, with its target users concentrated in high-income groups. Finance columnist Xiao Lei recently issued a message saying that TurnKey Jet users need to wire transfer when booking a private jet, so they will be limited by the banking hours. For this group of people, the traditional financial channel may take too long, if any This problem can be solved with a cryptocurrency that runs 24 hours and does not require any financial intermediation. So he believes that it is the limitations of the traditional banking industry that prompted the company to seek another option through the SEC.

So for TurnKey Jet, it's about the traits of digital currency that are more flexible than points and traditional banking, rather than the full functionality of real digital currencies (especially those that involve market capitalization potential). It reduces the value-added possibility and the token of investment property. It also means that the risk of cryptocurrency and the complexity of the token issuance project are largely eliminated. It can only be said that it is more in line with the current controllability and safety of investment products. The requirements, which are fundamentally different from the regulatory cases expected by the encryption market, can neither meet the current market demand nor provoke project compliance enthusiasm.

This is also doomed, after a brief heat, TurnKey Jet will soon be forgotten by the market. Beijing University of Aeronautics and Astronautics, the national "Thousand Talents Program" special professor Cai Weide believes that it can be said in a word, the SEC only shows that the securities token can make money, other tokens are points, if it is points, do not want to make money on it.

Looking at the regulatory logic from the SEC reply details

The SEC's reply is a non-legally binding regulatory guidance. What is the point of this reply that does not constitute any legal opinion?

The SEC made it clear that the guidelines are not a detailed overview of the law and do not constitute any legal advice. According to the statement, the guidance framework was issued by the SEC's Center for Innovation and Financial Technology Strategy (FinHub). It only represents FinHub members' opinions and is not a SEC rule, regulation or statement. The committee has neither approved nor objected. Its content.

As early as six months ago, SEC Chief Financial Officer William Hinman had claimed to develop a new encryption guidance framework. William Hinman said: "We want to give startups an example of identifying cryptocurrencies as securities, and also provide them with an example of identifying cryptocurrencies as not securities. However, the SEC does not focus on the analysis process. An independent factor, but a comprehensive consideration in many aspects."

For half a year, using TurnKey Jet as an example, the SEC's regulatory guidelines include an example of identifying that the cryptocurrency is not a security. The regulatory guide is positioned as an analytical tool that helps market participants assess whether federal securities laws apply to the issuance, sale, or transfer of a particular digital asset in a more accessible language.

In a reply to TurnKey Jet, Jonathan Ingram, chief legal counsel of the SEC Corporate Finance Department, made it clear that the situation mentioned in the advisory letter from TurnKey Jet, James P. Curry, was true. TurnKey Jet's Token is not a security, so there is no need to register, you can provide and sell tokens under the Securities Act and the Trading Act, and Jonathan indicates that the SEC's position is based on the facts that TurnKey Jet stated in the letter, if that fact Any change will lead to different regulatory outcomes.

Lawyer Zhang Wei told Finance Network that the SEC's supervisory logic is that the lawyers of the project will specifically inform the SEC about the project and ask if they need to register with the ICO. According to their lawyers, the SEC will be based on the substance of the token. Use and the rights and obligations or risks of the investor and the project party to review whether the token is a security and then reply. Zhang Wei said: "Because US regulatory lawyers have to bear a lot of legal responsibility if they are perjury, I believe they should be truthful, and their projects will follow this path."

In order to minimize the regulatory uncertainty, the SEC has a lot of preconditions for the case of the token issuance. From its regulatory logic and review ideas, it is not enough at this stage. It constitutes a complete logic of judgment clauses, and is more inclined to operate under the exclusion method of specific analysis.

At the same time, according to the rules of the SEC, the “Staff guidance” issued by the SEC members is important, but it is far less effective than the SEC's official statement, so that the SEC can stay in the actual regulatory operation. There is room for flexibility.

"As a case, TurnKey Jet may mean to tell you from the opposite side, under what circumstances the token issuance is not a security," said Zhang Wei.

For the regulation itself, the actual case of borrowing TurnKey Jet to explain the regulatory requirements is a useful attempt. Previously, the SEC has repeatedly voiced a clearer and easier-to-understand regulatory guidance in the field of cryptocurrencies, although the part of the case itself that seems to be available for reference seems very limited, and even under such a token framework, it may More restrictions have been added to future token issuance.

Reiterate Howey Test

Li Lianxuan believes that the guide issued with TurnKey Jet is more valuable and can guide you to the extent that you can use the attributes of digital assets without violating US securities laws. This is a reflection of US legislative attitudes. In the case of points, the digital currency has no value.

In September 2018, when the District Court in the Eastern District of New York approved a case involving suspected ICO fraud, it was clear that the ICO was under the jurisdiction of the SEC, and the jury could reasonably judge whether the token issued by the ICO was a security under the Howie test.

The Howey Test was issued by the US Supreme Court in 1946 and is the basis for the SEC to determine whether a cryptocurrency is a security. For the vast majority of cryptographic assets and projects, the so-called blockchain project "passes the Howie test" in order to avoid a series of controls that are judged to be fabrics after the securities and penalties for possible refunds of principals, indemnities, etc. It means that the scores of the specific four test indicators are not high, because they will not be recognized as the test results of the securities.

Regulatory delays have not occurred, and there are many opponents who have proposed whether to use other rules or even create a new one to replace the “Hay Test” as a basis for more appropriate judgment of whether digital assets are securities. In response, SEC Chairman Jay Clayton made it clear earlier that he did not intend to update the standard to cater to the digital currency.

This regulatory guidance has once again reaffirmed and refined how the framework of the Howie test can be applied to digital assets. Li Lianxuan said that although the Howe test gave four judgment conditions, it also left a lot of space for consideration. The SEC's supervision guide is also to further define and indicate the direction of the fuzzy space.

In the four dimensions of Howie's test, the SEC talked about the "money-marked after investment" and "targeted common cause" that could not be avoided for cryptocurrency, and would "make profit for the investment." The “expectations” and “the source of profit from the promoters or third parties” are combined into a “reasonable expectation of the profits of others' efforts”.

According to the specific framework content, it can be concluded that if a project token is to pass the Howie test, it needs to be done:

1. To achieve a decentralized network, there needs to be independent and decentralized community users and developers. The project itself needs to implement open source, and after open source, this open mechanism can continue to drive the decentralized network.

2. Developers or active participants (APs) need to stay away from any commitments that can be traded or value added for future projects, and remain as separate as possible.

3. The cryptocurrency should also provide users with some valuable features.

Moreover, the guidelines also take into account the form in which tokens whose nature changes as the project development and network development process are evaluated and regulated.

It can be seen that in this guideline, the SEC intends to guide the project to strengthen its decentralization and function, while leaving room for the development of the project, while trying to dilute the industry's excessive attention to the future appreciation of the project token. .

Li Lianxuan added: For the prospect of Token appreciation, there may be financial attributes, but to what extent this attribute is strong depends on whether the official can approve it. This part still has controversial definition space and degree of vagueness, which needs further discussion.

Compared to the TurnKey Jet token, although neither BTC nor ETH are recognized as securities, their implementation paths are quite different. So far, BTC and ETH can still be said to be the only two decentralized digital assets that are regulated and expressly exempted from securities laws. Whether this "only nature" can be broken is not known. For most of the remaining projects that are facing regulatory challenges, whether they are ultimately certified as securities or completely close to TurnKey Jet's tokens, they seem to be faced with an embarrassing situation that runs counter to the original intention of digital currency innovation.

On the one hand, there are still many obstacles to catering to regulations that still have many uncertainties. According to Cointelegraph, John Berlau, a senior researcher at the Competitive Enterprise Institute of the US liberal think tank, said in a report titled "Encrypted Currency and SEC's Unlimited Power Competition: Why Speculative Consumer Goods Are Not "Securities"", Blockchain Technology and cryptocurrency are transformative innovations whose potential has been hampered by “heavy regulation.” The government’s suppression of these technologies has prevented entrepreneurs from trying new methods and applications.

On the other hand, at the same time, in the space that has not been touched by more detailed supervision, the concept of model currency is rampant, and IEO succeeds ICO to copy the next round of financing frenzy. Under the new speculative psychology and high market sentiment, the market is profitable. At the same time as the selling pressure, the funds flocked to major exchanges to try to find new opportunities for skyrocketing. The market is about to face the next round of adjustments.

Securities lawyer Zach Fallon said in an interview with Bloomberg that IEO completely copied the ICO model and made the situation worse. Fallon said that forcing investors to use platform coins makes regulators more skeptical about IEO. Since IEO tokens are immediately placed on the exchange and sold in the secondary market, the SEC is more likely to treat it as a security. And Bencamp CEO Nejc Kofric said: "Before we enter this market, the industry needs to be better regulated. Of course, there are still some exchanges entering this field, which I think is short-sighted."

Jiang Lilong, a senior analyst at TLAB, told Caijing.com that many investors' investment projects in the market at this stage are more concerned with the future appreciation of the project tokens than the quality of the projects. In the long run, the project side will be more inclined to invest more energy in the secondary market operations than the development of the project itself. This is not good for the long-term development of blockchain technology. From this perspective, the threshold for Token is at least at this stage beneficial to the healthy development of the blockchain secondary market.

In terms of the SEC's restrictions on TrunKey Jet, Jiang Xiaolong believes that the Tokens issued by many companies at this stage do not meet their requirements. The consideration of the actual functions of Tokens in the future will be an important consideration for the company's issuance of Tokens.

With the further consumption of market stocks, the market will eventually face adjustments, and the nature of gameplay and compliance issues will gradually emerge. Short-term market shocks are not enough to disrupt the pace of regulatory implementation.

Will the release of regulatory details lead to a return to value or constitute an obstacle? Clearer regulatory standards and more stringent regulatory boundaries are often one step away.

This article Source: Finance and Economics Network on the financial

Author: Xi breeze

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- The Brexit delay in the United Kingdom is a big blow to the BTC "back pot"? Things have to start from the previous big rise

- After many times of theft, the Korean exchange Bithumb lost $180 million last year.

- Well-known investment institution Polychain: Manage assets from $1 billion to near waist

- Hardcore bitcoiner development guide

- May heavy doubles! Hangzhou teamed up with Sanya to launch the "one-stop" blockchain summit

- Take you "understand Bitcoin": How to become a Bitcoin super user?

- Interpretation of the SEC "Digital Assets" Investment Contract "Framework Analysis" (with full text translation)