Barbarians at the Door of the Blockchain: Understanding the Crypto Industry M & A

Since 2013, the blockchain industry has had 350 mergers and acquisitions, with a cumulative transaction value of $ 4 billion, but compared to the value of the cryptocurrency network, or compared with mergers and acquisitions in other fields, the number and amount are still small. The cryptocurrency field is still a relatively young industry, and mergers and acquisitions are a symbol of the upgrading and iteration of crypto companies and a strategic tool.

Source: Chain News

Written by: Ricky Tan, founder of blockchain data and consulting firm TokenData

Compilation: Perry

- Urban rail two-dimensional code interconnection and interoperability realized from "1" to "11" in one year. Blockchain technology increased the "pass" capacity expansion

- Free and Easy Weekly Review 丨 Can't Blockchain Privacy Protection and Regulation Have Both? Actually!

- Security Monthly Report | 16 security incidents occurred in November, with losses of nearly US $ 56 million

Although the cryptocurrency industry is still in its infancy, mergers and acquisitions involving crypto companies are increasing. However, apart from rumors, media news and high-level summaries, there has been no relevant thorough analysis and forward-looking predictions. This article hopes to change this situation and provide a reference analysis and summary.

Trading behavior

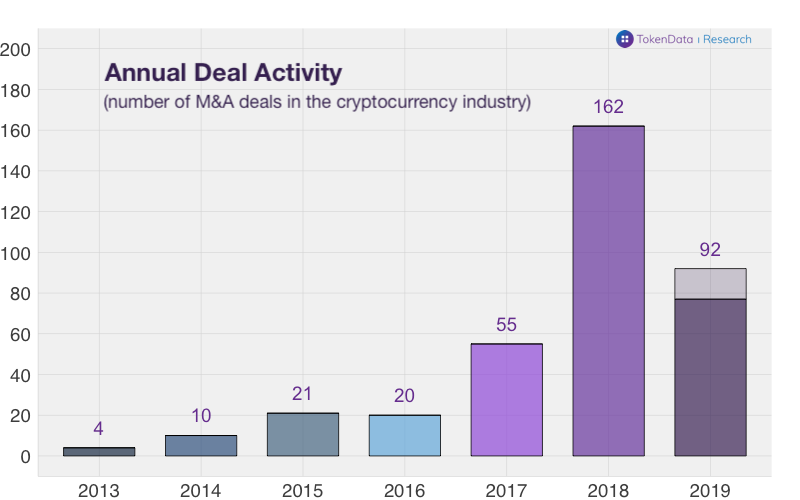

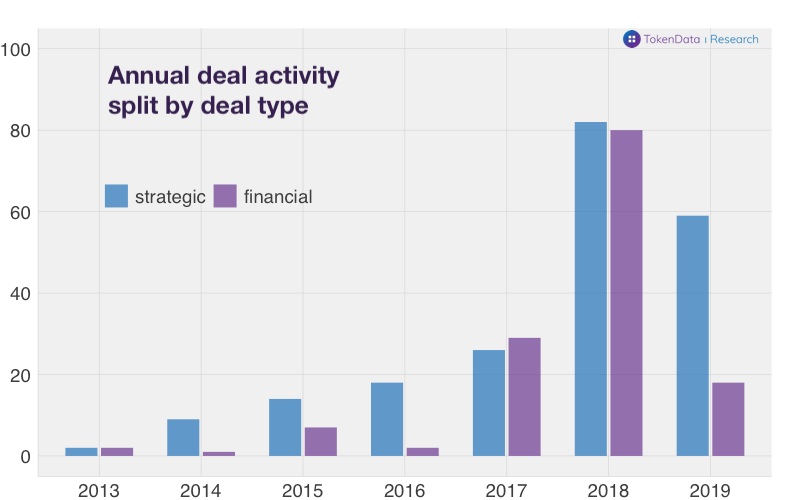

Since 2013, there have been 350 mergers and acquisitions involving cryptocurrency and blockchain companies. 2018 is the most active year for M & A activity, with more than 160 M & A transactions. We estimate that there will be approximately 90-100 transactions in 2019.

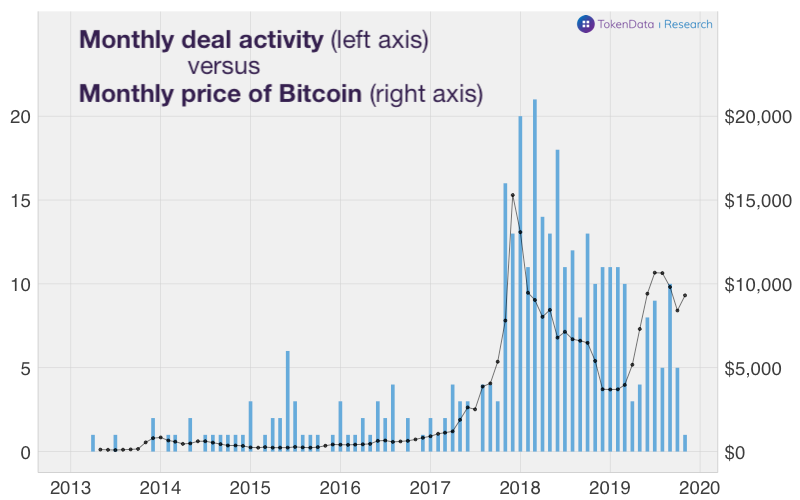

M & A activity is very ups and downs, and it seems to be positively related to cryptocurrency prices and industry sentiment. M & A activity on a monthly basis peaked in early 2018, when it was also the pinnacle of cryptocurrency prices and attention.

Amount of the transaction

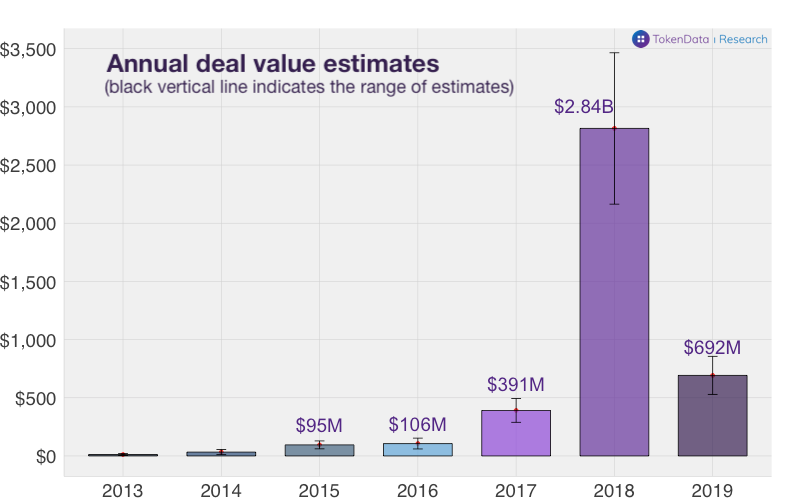

We estimate that the total value of relevant M & A transactions since 2013 is approximately US $ 4 billion, of which approximately US $ 2.8 billion in 2018 and US $ 700 million in 2019.

These numbers sound good, but they are still small compared to the overall network value (over $ 200 billion) of each cryptocurrency network. However, if you consider the early stages of the entire industry, this situation is reasonable: most companies have not been established for more than 5 years, and it seems that it will take a few years for the industry to have a remarkable IPO.

If you take a closer look at those interesting and interesting transactions, you will find that only one transaction in 2019 was worth more than $ 100 million, compared to five in 2018. However, notable deals in 2019 include: Facebook's acquisition of its Libra project, integration of the crypto asset custody industry (Coinbase-Xapo custody), and the first token merger.

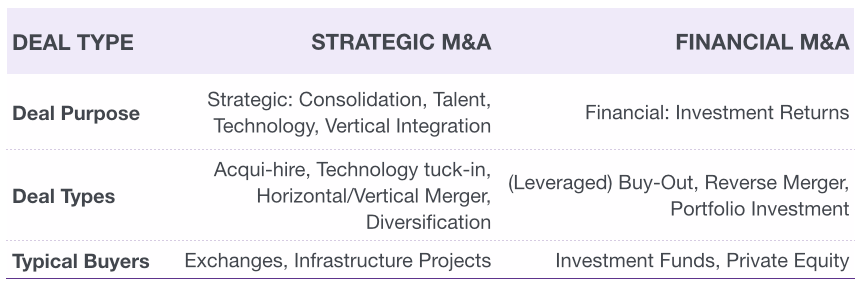

Financial M & S vs Strategic M & A: Not all M & As have the same value

We can divide these M & A transactions into two categories: financial M & A and strategic M & A, as described below:

2018: Motives for financial M & A are not clear. The chart below shows that there were more financial M & As in 2017 than strategic M & As, and in 2018 the numbers were basically the same. A closer look at financial M & A activity reveals that many acquisitions fall into two categories:

- a) Non-cryptographic enterprises that have failed to function and become crypto investment enterprises (such as Long Island Blockchain) through the acquisition of small cryptocurrency startups;

- b) Reverse merger, in which case a private crypto company acquires a listed shell company.

2019: Strategic M & A continues to be strong. When the cryptocurrency market was revised in 2018, opportunistic and unclear financial mergers and acquisitions disappeared, and it will be completely absent by 2019. Strategic M & As have maintained a good momentum, with approximately 70 transactions expected in 2019.

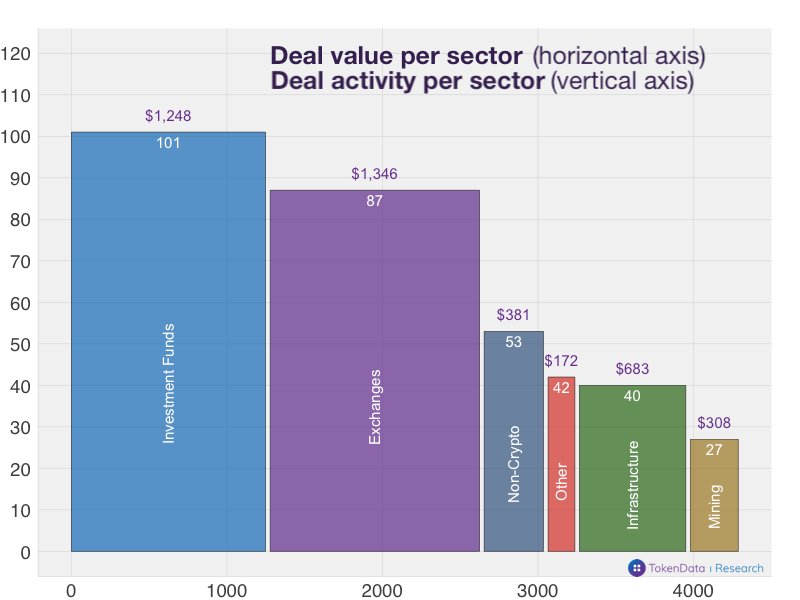

Sector: Funds and exchanges are at the forefront of acquisitions

More than 50% of M & A transactions are completed by investment funds and exchanges: Investment funds and cryptocurrency exchanges are the most active acquirers. Adding the two together accounts for more than half of the total amount and amount of all transactions.

The exchange is a strategic acquirer that is frequently hit: transactions and speculation are the first killer applications in the crypto industry, which allows transactions to have all the sufficient cash reserves and network resources for acquisitions.

"Pay Entry": Non-crypto companies have been expanding their presence in the industry by acquiring cryptocurrency startups. Most of these deals are aimed at bringing in the talent of startups. For example, Facebook acquired two startups (Chainspace and Servicefriend) to supplement development capabilities for its Libra and Calibra projects.

Crypto Infrastructure and Mining : Related acquisitions involving development teams of crypto infrastructure companies, protocols, and decentralized applications (DApps) were also active, with 40 transactions. Before the cryptocurrency market price correction in 2018, mining companies were very active, but in 2019 there are almost no signs of disappearance.

Exchange: Coinbase is a big M & A

Exchanges and trading-related companies are the most active strategic buyers. Which companies are the most active in this field?

Coinbase is the largest giant of strategic mergers and acquisitions, with a total of 16 acquisitions. The company's M & A strategy mainly focuses on talent and technology tuck-in (Note: Tuck-in M & A generally refers to the acquisition of the acquisition target into the acquirer and directly becomes a department, so that it is easier to obtain relevant technologies and advantages, compared to the cost of establishing and developing it Lower. ) Coinbase also made two heavyweight acquisitions: $ 100 million for Earn and $ 55 million for Xapo 's hosting business.

Kraken and Coinsquare follow Coinbase. Kraken has 7 transactions and Coinsquare has 5 transactions. One heavyweight deal was Kraken's $ 100 million acquisition of Cryptofacilities , a UK-based compliant cryptocurrency derivatives exchange.

So, what about Binance? Despite its high scale, speed, and product richness , Binance has so far made "only" 3 public acquisitions (Trustwallet, JEX, and Wazirx) . However, Binance has invested heavily in other cryptocurrency companies and partners, which in fact has similar strategic effects to mergers and acquisitions.

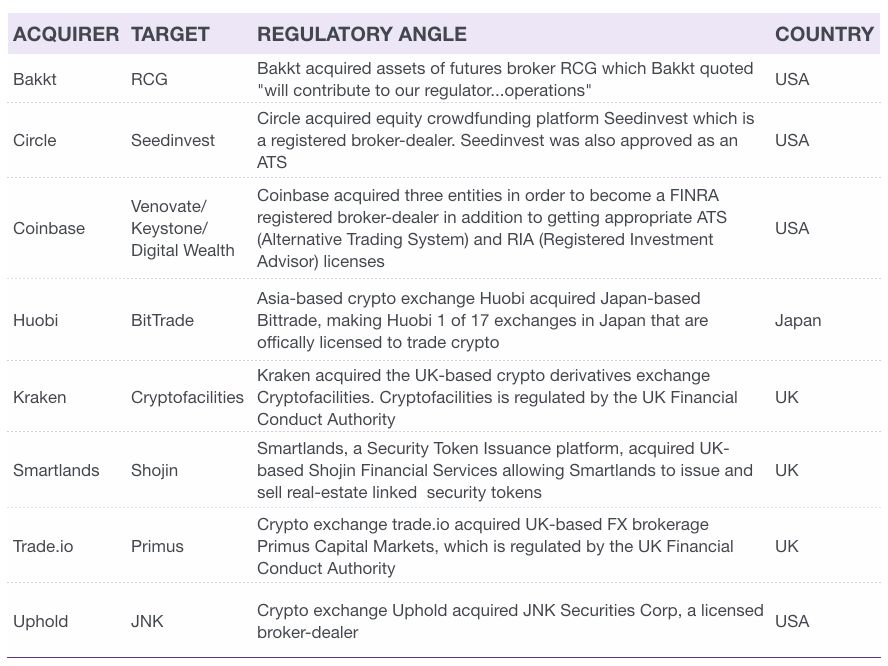

M & A is also used as a means to circumvent regulatory obstacles: Cryptocurrency exchanges use M & A as a strategic tool to facilitate regulatory approval in certain jurisdictions or certain products. They do this by acquiring companies that already have relevant regulatory licenses. We found that since 2018, 15 transactions (examples below) have explicitly mentioned in the announcement that regulatory issues are important considerations for their acquisitions.

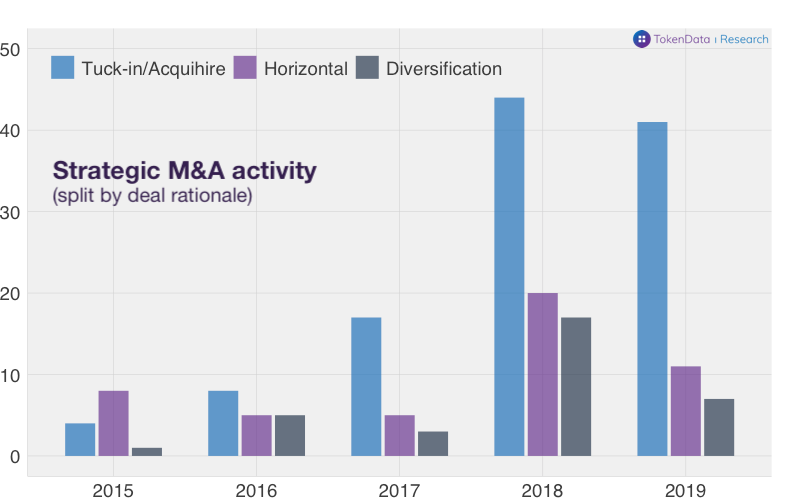

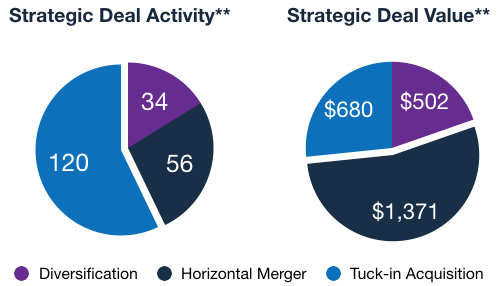

Talent- and technology-tuck-in is an important driver of strategic mergers and acquisitions

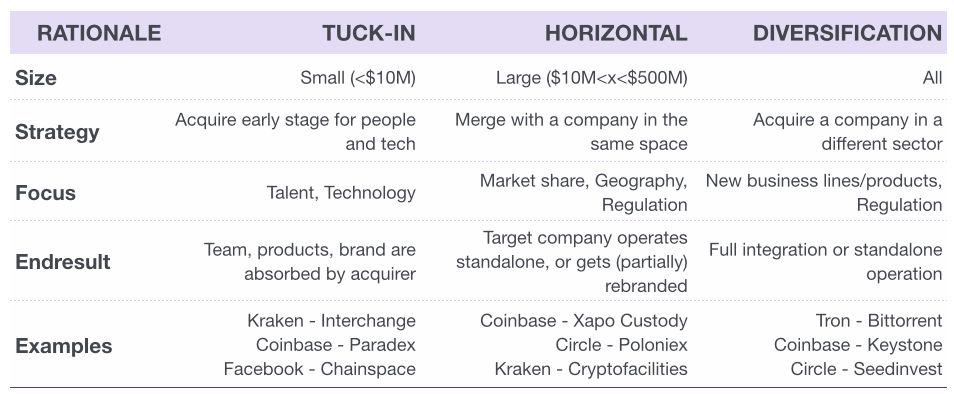

To understand the motivation of each M & A, we first divide all M & A into three categories: tuck-in, horizontal acquisitions and diversification.

Tuck-in * for talent and technology is currently the most common motivation for strategic mergers and acquisitions in the cryptocurrency space, and such mergers and acquisitions have maintained a steady momentum from 2018 to 2019. Focusing on the acquisition of talents and the acquisition of early technologies is in line with the characteristics of this industry's infancy.

* The word Tuck-in is quoted from Coinbase's Chief Operating Officer Emilie Choi, who used it in various interviews involving mergers and acquisitions in the cryptocurrency space:

- https://www.theblockcrypto.com/post/25055/emilie-choi-coinbase

- https://www.businessinsider.com/coinbase-crypto-bitcoin-acquisition-strategy-emilie-choi-2018-4?international=true&r=US&IR=T

Horizontal mergers: It accounts for only about a quarter of all strategic M & A transactions. However, it accounts for more than half of the transaction amount, because it represents the integration of larger and more mature companies.

Diversified transactions: This is a broad category that mixes multiple situations. It includes both cryptocurrency companies acquiring traditional financial institutions to obtain their compliance licenses (such as Coinbase, Bakkt, and Kraken) , and cryptocurrency agreements to acquire non-cryptographic companies to acquire their existing user base (such as TRON's acquisition of Bittorrent) .

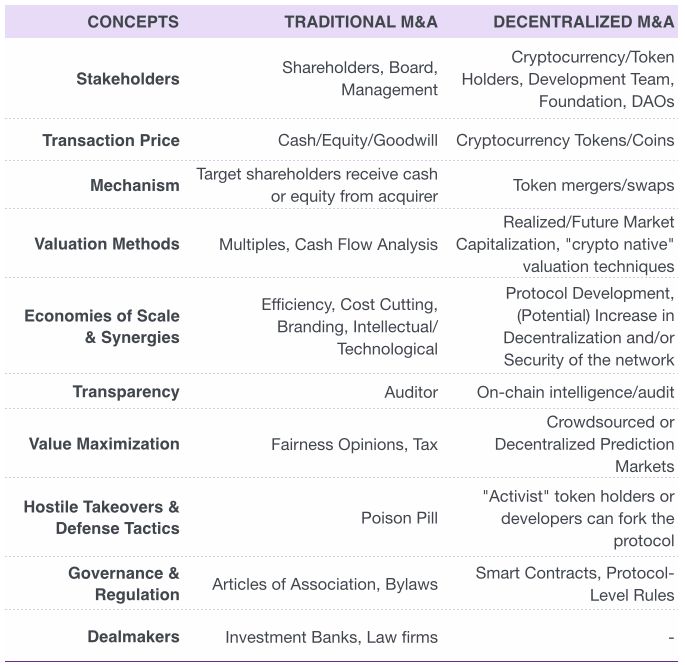

Decentralized M & A

So far, we have focused on conventional concepts such as "traditional" financial and mergers of centralized companies. Below we will discuss how cryptocurrency networks merge.

There have been many pieces of thought trying to construct theories to predict what mergers and acquisitions of decentralized cryptocurrency networks will look like and what problems will arise. For example: What happens if two competing privacy coins merge or a decentralized prediction market launches a malicious acquisition of a competitor? Of course, such pure "decentralized mergers and acquisitions" have not yet appeared. After all, many cryptocurrency networks are still in the nascent stage of development, and most are operated by centralized enterprises and foundations.

Some thought fragments of decentralized mergers and acquisitions:

"Protocol M & A" by Ryan Selkis

https://medium.com/@twobitidiot/protocol-ma-91a129db1fe4

"What the First Token Hostile Takeover Could Look Like" by Andy Bromberg

https://medium.com/@andy_bromberg/what-the-first-token-hostile-takeover-could-look-like-c40be3ccb6b5

Crypto-native M & A concept: As existing cryptocurrency networks and blockchain projects mature, and the degree of decentralization increases, new stakeholders, concepts, and mechanisms will emerge in the M & A process. We summarized several concepts and mechanisms of "traditional mergers and acquisitions", and conceived corresponding concepts and mechanisms of crypto native and "decentralized mergers and acquisitions".

Real-time experiments: In fact, we have also seen experiments that try to turn theory into practice, such as mergers and acquisitions by development teams, and transactions that use tokens instead of capital and / or cash. We will talk about these examples in the following sections.

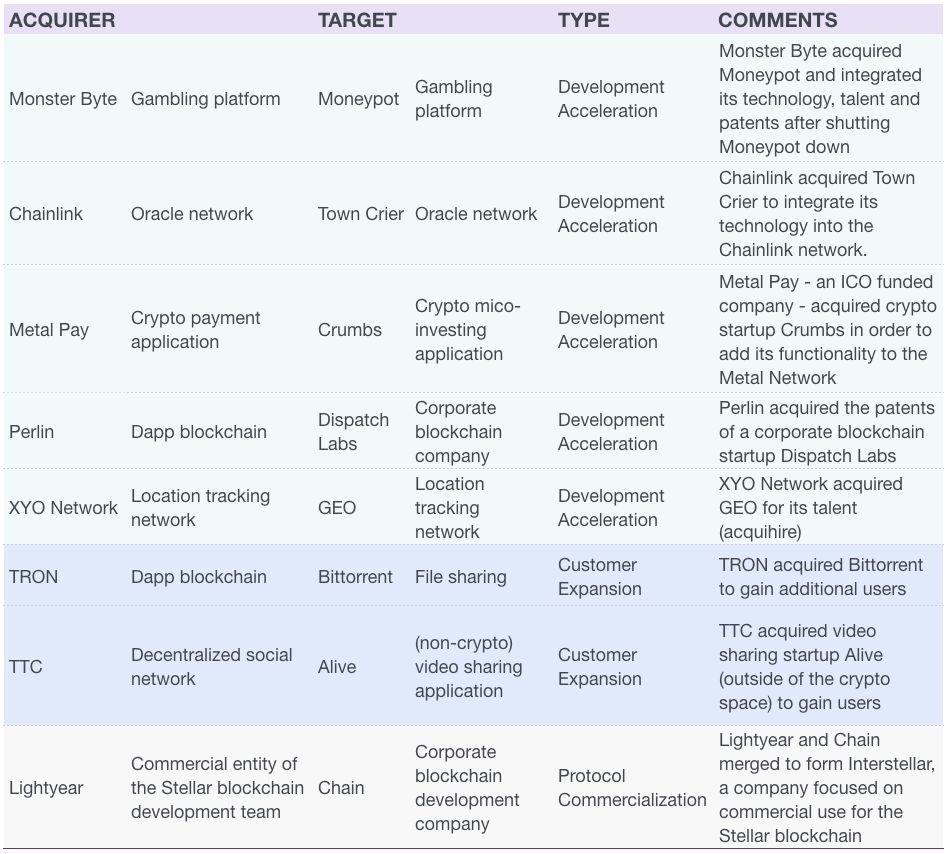

Agreements and M & As initiated by DApp projects

Although the real "decentralized mergers and acquisitions" have not yet occurred, there have been many mergers and acquisitions by cryptocurrency development teams. Many development teams want to create a decentralized agreement or application, and M & A can be a useful strategic tool for them to seek transformation. We found that the transactions used by these teams can be divided into the following three categories:

- Accelerate development progress: Acquisitions initiated by the development team of the decentralized agreement. Much like the tuck-in acquisition, these deals focus on acquiring talent and technology. We see that several teams that have raised funds through ICOs have conducted such transactions.

- Expand consumer base: acquire non-cryptographic companies / networks that already have a large user base. Without the need to grow users organically, such transactions can help acquirers acquire a large number of new users and start using their cryptocurrency network and / or tokens.

- Commercialization of the agreement: The ultimate goal of the development team initiating this type of acquisition is to commercialize its open source cryptocurrency protocol. For example, Lightyear, an entity formed by the Stellar development team, merged with Chain, an enterprise blockchain company. After the merger, the company re-branded Interstellar and brought Chain's customers into the Stellar blockchain.

The earliest batch of cryptocurrency mergers and acquisitions

2019 witnessed the first wave of cryptocurrency mergers. After the ICO and token sales frenzy in 2017, the over-funded crypto projects fell into a situation of insufficient motivation, and it is only a matter of time before each of them merges with each other. We found two cases:

- TR ONAce & TRONDice : In April 2019, two gaming applications running on the TRON blockchain, each with its own token, announced that TRONAce acquired TRONDice, and TRONDice tokens would be merged / exchanged into TRONAce tokens.

- COSS & ARAX (aka LALA) : In April 2019, Singapore's cryptocurrency exchange COSS and cryptocurrency wallet ARAX announced the merger of the two companies. Both companies raised funds by issuing their own functional tokens through an ICO in 2017. After the merger, the holders of the two projects will exchange the original tokens for a new token representing the merged entity.

Although these two transactions are not strictly "decentralized" because the project involves traditional enterprises, from a token perspective, they have their own meaning and value.

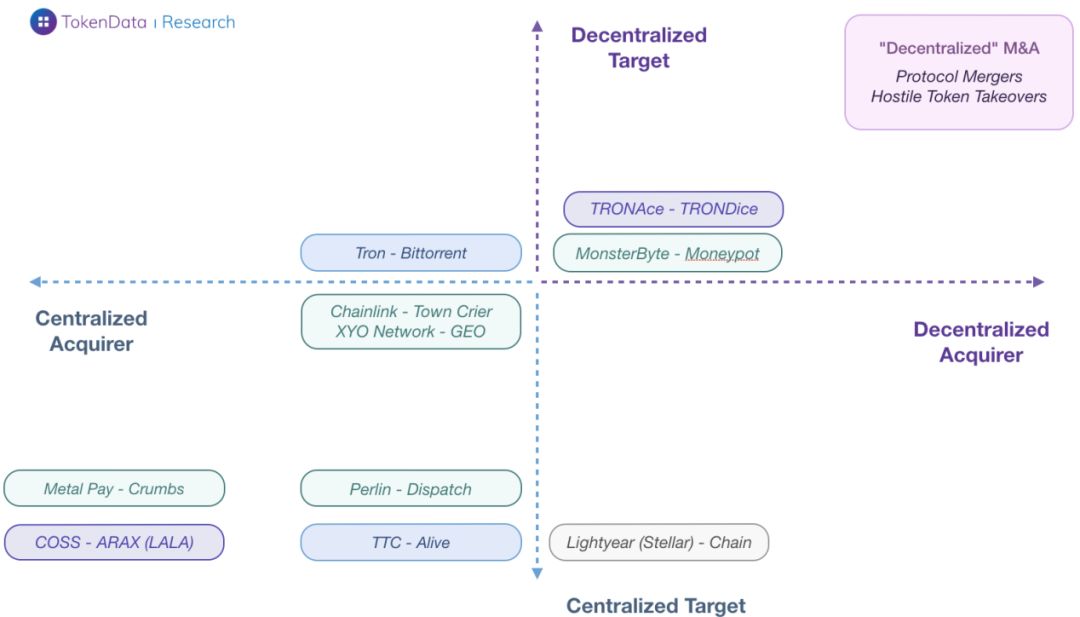

Use a centralized / decentralized matrix to depict the entire picture of related transactions

Where are the various types of M & A activities involving protocols and DApp development teams in the centralized / decentralized matrix (the acquirer and target are the horizontal and vertical axes , respectively) , the results can be seen in the figure below. Because there is no objective measure, the position is only relative. For example, we put the TRONAce–TRONDice merger in the upper right quadrant because it involves two DApps and the merger mechanism used is token merger. In contrast, although COSS-ARAX (LALA) also uses token consolidation, the two entities are highly centralized. The upper right quadrant is an imaginary case of decentralized mergers and acquisitions, and their entities and mechanisms belong to the decentralized camp.

Highlights

To sum up, we analyzed 350 transaction cases between 2013 and 2019 to understand the role played by M & A in the crypto industry. Looking ahead, we considered what a "decentralized merger and acquisition" would look like, and evaluated some transactions that could provide clues.

- Industry Maturity The cryptocurrency industry has been adept at M & A activity. 350 mergers and acquisitions have occurred since 2013, involving a transaction value of $ 4 billion. Although this is of great significance in the crypto industry, its quantity and amount are still small compared to the public value of the cryptocurrency network, or compared with mergers and acquisitions in other fields. The cryptocurrency field is still a relatively young industry, and mergers and acquisitions are a symbol of the upgrading and iteration of crypto companies and a strategic tool.

- Volatile M & A activity is highly volatile, showing signs of positive correlation with cryptocurrency prices. The frenzied rise in the second half of 2017 drove a surge in speculative financial M & As. The subsequent price collapse and recovery also created a better environment for strategic mergers and acquisitions.

- Funding Most cryptocurrency companies are backed by venture capital. However, in the foreseeable future, it is unlikely that a large crypto company IPO, and most crypto ventures have a short life, so mergers and acquisitions are not a good exit strategy.

- Corporate and strategic cryptocurrency exchanges such as Coinbase and Kraken have become leaders in M & A in the crypto industry. Acquisition (talent) and technology mergers and acquisitions are the most common types of mergers and acquisitions in this industry, and we expect this momentum to continue in the foreseeable future.

- There are clear signs of regulation that cryptocurrency exchanges are using mergers and acquisitions to meet regulatory requirements in different countries and regions. With the rapid changes in regulatory policies in various countries, M & A will become more attractive as a strategy for global compliance of crypto companies.

- Decentralization The true "decentralized" M & A has not yet appeared. However, many development teams are already actively acquiring companies to help them move from a centralized entrepreneurial stage to a more decentralized end state. In addition, 2019 also witnessed the emergence of the case of token mergers. In the future, this will be an important mechanism for decentralized mergers and acquisitions.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Babbitt Column | Neglected Blockchain Node Operations: The Hidden Value of Mining

- Save 31 billion US dollars in compliance costs in 5 years, large-scale adoption of blockchain in food and beverage industry

- China Blockchain Talent Recruitment Report

- Perspectives | Bitcoin from a Money Carrier Perspective

- Site | Blockchain national team landed in Hangzhou, 5 applications accelerate the "urban brain" evolution

- The future of Ethereum: technology and protocols become the next key element

- Observation | After the halo fades, where is the practical application of the blockchain?