Blockchain and the traditional financial industry turtles race, who can win?

Among them, the music industry provides the clearest example to illustrate this situation. The following is a breakdown of the global music industry's revenue over the past 17 years: it can be seen that the current streaming media revenue (dark blue part) has exceeded the physical income (red part) ), becoming the most important source of income for the music industry.

- Getting started with blockchain | Can Google's latest quantum computer crack bitcoin? Is the wallet safe?

- People who want to rely on Bakkt scams are really disappointed.

- The first domestic "Digital Currency Dictionary" was launched at the New Moganshan Conference, and the Babit Think Tank was the main editor.

But in the financial services industry, its business model has not experienced a similar transformation . Although FinTech (financial technology) services are being used in many specific markets (especially in the Chinese market), so far, most financial technology companies have mainly found new service areas (such as P2P lending platforms, fund raising, cross-border payments, Small businesses or customers without credit history provide loans, etc.), or choose to work with existing financial companies or large companies.

This collaboration allows these fintech start-ups to reach more customers (by providing white labels, co-branded products to customers) and, in many cases, reducing the regulatory compliance burden of these start-ups.

In other words, these financial technology companies often use software to extend existing financial services systems, rather than streaming services like the music industry (or shared travel service companies in the transportation industry (such as Didi), retail business. The multinational e-commerce companies (such as Amazon), etc. , rebuild the financial system .

At the same time, these financial technology start-ups are also difficult to compete positively with traditional banks because traditional banks have very flexible guarantees and advantages :

- Broad distribution through the establishment of branches;

- Monopolize financial data to form unique expertise (such as credit underwriting);

- Having the status as a regulated institution providing credit;

- Obtain deposit sovereignty insurance (such as FDIC insurance in the US);

- A trusted safe deposit and wealth management brand.

While mobile apps and new data sources are beginning to erode the traditional bank's distribution and data monopoly advantages, banks have a privileged position in the global economy , which is the result of deep structural reality in our financial system: participation in high-profile transactions Counterparty risk , while traditional banks have a strong position in dealing with counterparty risk .

This is because today's financial network can be summarized as an information network , and banks and other financial institutions are responsible for interacting with these networks on behalf of customers, that is, sending the right message and responding appropriately to the received message.

In order to avoid excessive costs, financial institutions rely on mutual trust to effectively manage capital flows, which exposes them to the risk of a party to the transaction not complying with the terms of the contract (ie, counterparty risk). This risk is controlled by the supervision of some of the most reputable financial institutions, and when transactions occur outside of trusted channels, these financial institutions pass on this risk to users in the form of high fees.

The attractiveness of the largest and most trusted traditional financial institutions strengthens the dominant position of large banks. This also explains why in many cases, fintech start-ups are forced to work with existing financial institutions rather than trying to replace them .

The conclusion is that this incremental improvement in Fintech start-ups (such as better user interfaces and new data sources at the edge) is not enough to push large financial institutions to step down . In order to transform the traditional financial services industry, it is necessary to re-architect its basic network to reduce the risk of counterparty. Only in this way, another business model is likely to gain sufficient competitive advantage to win the dominant market share.

This is why from a financial services perspective, blockchain networks are very interesting and promising: blockchain networks systematically reduce counterparty risk in financial networks – blockchain networks use open source software and The public computing environment in which purely economically motivated participants (ie miners/verifiers) operate protects the execution of financial transactions, thereby reducing counterparty risk!

The blockchain network lays the foundation for a more transparent and secure financial system : it relies on cryptography, decentralized consensus and incentives, rather than complex inter-bank relationships and regulatory tools, opening up new Trustless market, the traditional financial system cannot form such a market because it needs to build on the basis of trust.

The blockchain network has the potential to support all of the financial interactions that may exist in our current financial system and provide more choices in terms of products, costs and risks.

Today, a small group of engineers and entrepreneurs are aware of this opportunity and are building financial services on public chains such as Bitcoin and Ethereum . Most of these services are new, complex and mature (one of the most famous examples is MakerDAO), which serves a small number of businesses and individuals in the cryptocurrency ecosystem, providing payment services, credit facilities, and exchanges. , investment tools, account storage, insurance and derivatives contracts, etc.

On the surface, the technical and regulatory risks of these blockchain-based financial services may be higher than their long-term potential, so it is easy to think that they do not have clear market adaptability.

However, blockchain-based financial services have become a core business in the field of financial technology that has the potential to transform traditional financial institutions (including storage, payment, lending, investment, financing, insurance, etc.), fundamentally benefiting financial markets and The way consumers are.

The advantages of encryption financial services

But the blockchain differs from existing open source projects such as Linux in that the blockchain maintains a shared state (ie, a shared distributed ledger) . The function of the blockchain is like a global settlement machine that handles financial transactions, and the results are recorded in a secure public data structure (ie, a distributed ledger). The validity of all transactions can be verified by checking if the relevant records are included in the blockchain .

Nick Szabo, the father of smart contracts, describes the blockchain as a piece of transparent amber . The longer the transaction record is stored in the blockchain, the more confident participants are that their transactions will not be tampered with (the blockchain network is built on No need to trust on the basis).

This increases the social scalability of the financial system because participants in blockchain transactions use a shared settlement system to conduct transactions, and this settlement system gives them fewer ways to harm each other (ie, counterparties) Risk reduction).

By providing stronger trading guarantees, the blockchain system can accommodate a larger population worldwide .

The blockchain also has a programming language for building " encryption contracts, " which are the procedures that miners perform. Multi-signature addresses on Bitcoin are widely used encryption contracts.

Ethereum has further developed the concept of encryption contracts, allowing developers to deploy custom encryption contracts (smart contracts) that define arbitrary financial interactions. These contracts run on the blockchain network, and the contract code cannot be tampered with once it is deployed on the network.

Since these contracts run in a shared accounting system (ie blockchain), they can be tightly integrated. This feature is called composability, which is the encryption contract on the same blockchain platform. Can be combined with each other to produce new products and services without having to redeploy and maintain a code base for each underlying contract.

Therefore, crypto-finance services bring us a new financial computing paradigm based on open source software that reduces an order of magnitude of participation risk and allows developers from different organizations to work together.

In fact, the impact of this new paradigm can be divided into three major parts: 1) open access ; 2) minimum cost ; 3) new asset form, organizational form and market structure .

1) Open access

Anyone with Internet access can download and run open source software. Creating an encrypted wallet can be done without anyone's approval or permission (about 30 seconds).

This means that if encrypted wallets can provide a level of service similar to banks, they should at least be able to gain market share in marginal markets, where markets where people have difficulty accessing basic financial services .

If the quality of service for encrypted wallets is more advantageous, they may actually become the banking system in the Internet economy. Abra is one of the earliest access methods for cryptocurrency wallets. Users can acquire other crypto assets or invest in traditional stocks/ETFs and fiat currencies by pledgeing assets such as Bitcoin and Litecoin. With applications such as Abra, encrypted wallets open the door to a rich ecosystem of open financial products/services.

The open access feature also applies to blockchain-based financial products/service providers. Encryption contracts can make the creation of financial products/services more democratic, just as YouTube has made the production of video content democratized . This will have far-reaching implications, and I think we will see almost all imaginable markets, including some that financial institutions have never foreseen but are useful to many people.

What is important is that the value generated by these markets will be shared with all participants , rather than being monopolized by a small group of privileged traditional institutions, like traditional financial systems.

2) Lowest cost

Since the encryption contract is modular and can perform specific financial combination functions, it can effectively unbind financial services .

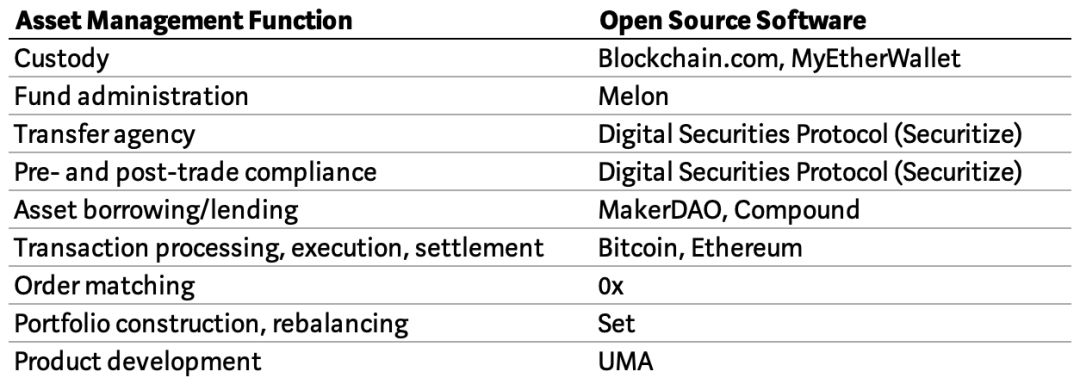

In the case of asset management, asset management is a service that includes many components, including activities such as product development, investment, transaction management, order execution, and pre-trade compliance management, as well as transaction processing. And logistics management activities such as settlement, custody, transfer agent and securities lending.

But with encryption contracts, many of these components can be implemented entirely in software in a reliable, de-mediated way . Currently, there are many open source blockchain projects that are working to achieve this, as shown in the following figure:

You no longer need to build a wide network of relationships within the financial services industry to start your business, you just need to deploy code and access an open blockchain network.

This will greatly reduce the production costs of financial services and will lead to healthier competition, and the cost savings will be passed on to customers .

In addition, there is another factor that keeps the cost of encryption contracts low: the risk of competitive forks . If a particular blockchain agreement is considered to be charging too much, then its competitors will be able to copy the protocol code and generate a forked chain, reducing costs.

To prevent competition from the forked chain, agreements typically reduce costs to the levels necessary to sustain development and ensure safety. This situation has brought continuous downward pressure on the cost of encryption contracts, stimulating a healthy competitive environment.

In other words, by relying more on encryption contracts, the fixed costs (infrastructure and development) and variable costs (depending on the costs of multiple intermediaries) of traditional operational financial services businesses are structurally reduced.

3) New asset forms, organizational forms and market structure

The most exciting prospects offered by encryption contracts may be the new assets, organizations and markets they support.

Encryption contracts allow the creation of provable scarce programmable assets . Some cryptographic assets (such as Bitcoin) are committed to becoming a fiat currency alternative, while other cryptographic assets (such as project tokens) are created to do a lot of other things, including granting members/governance/voting rights in the network. , assign ownership of real-world assets (such as commodities and securities), or represent the price of real-world assets in the form of synthetic assets (such as DAI).

Even in the early stages of the current blockchain development, any asset type has the potential to be represented in some form by a cryptographic contract, placing assets in a publicly accessible, low-cost global settlement system (such as Bitcoin and Ethereum network).

Once an asset exists in the form of a cryptographic contract, it can easily interoperate with cryptographic financial services to effectively allocate, transfer, and aggregate liquidity .

From a longer-term development process, we are currently only scratching the surface of the types of viable crypto-assets that need to be studied more deeply in terms of the potential for economic growth.

In addition, encryption contracts can be used to compile rules and governance mechanisms. This means that you can create a global organization (whether it is a legal entity in a specific jurisdiction or an open source software project) and define its ownership, rules, processes, and governance mechanisms through cryptographic contracts.

Many decentralized autonomous organizations based on Ethereum (such as MakerDAO, MolochDAO, Aragon, etc.) are the exploration and application of this organizational form.

Encryption contracts provide a toolkit for such organizations to enable organizations to coordinate the activities of their members in a responsible and verifiable manner, reducing reliance on local laws, regulations, and enforcement traditions that have national boundaries . In other words, the encryption contract fills a huge trust gap, and the issue of trust has historically been an obstacle to cross-border interaction.

One such organization is MakerDAO, a Decentralized Autonomous Organization (DAO) that manages the guaranty of credit instruments and Dai, a 1:1-linked synthetic asset. In the first year of its inception, MakerDAO issued more than $240 million in non-transaction risk loans, which is a good indication of the potential of DAO organizations to provide useful, open financial services to the global Internet economy.

Finally, because crypto contracts can operate within previously unattainable risks, they can create new markets that were previously impossible to achieve due to lack of trust, inaccessibility, or cost. A good example of this is IBISA, which creates a scalable alternative to crop microinsurance.

From a historical perspective, it is not cost-effective to let traditional insurance companies cover more than 500 million small-scale farmers. The reason is that management costs are high and the value of a single contract is low. Although riskized risk is seen as a potential approach, the risk sharing is still far beyond the local scale due to the difficulty of mutual trust between members who are far apart. With transparent contracts for cryptographic contracts, IBISA created the world's first incentive-compatible crop microinsurance company.

In summary, by running on a blockchain different from the current mainstream financial network, encryption contracts have advantages that traditional financial service providers cannot match. If systems based on encryption contracts reach escape speeds, their openness, verifiability, and cost-effectiveness will allow them to scale to every corner of the Internet, and they will cover markets that today's financial institutions cannot operate. , win in profit.

In other words, the impact of encrypted networks on banks is like the impact of the Internet on large music companies over the past 20 years: lively .

The road to the future

But it's becoming increasingly clear that the design of blockchains and encryption contracts is the most promising, able to coordinate financial services in this globally connected world in a more efficient and secure manner , and some new admissions are emerging today. For example, Libra, Telegram's TON project and the Chinese central bank's digital currency are the best explanations.

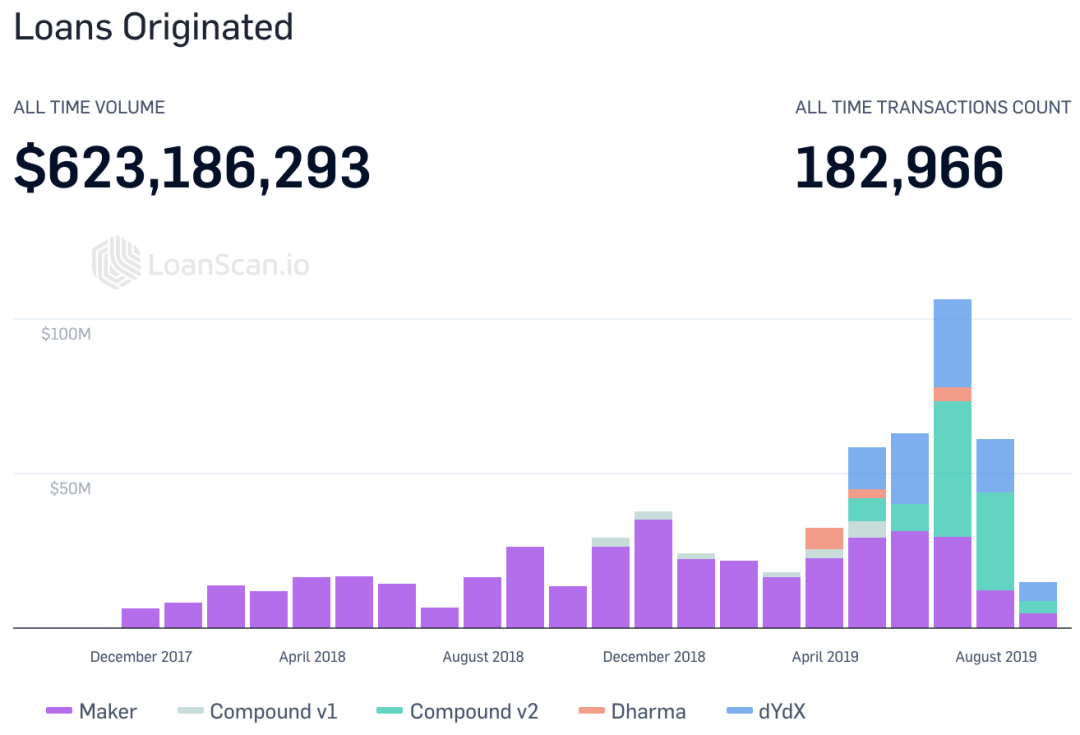

That's why, despite the overall decline in cryptocurrency prices by 70-90% in the bear market of 2018, the number of full-time developers working on open source encryption software has more than tripled .

During the same period, the open loan agreement on Ethereum generated more than $600 million in loans, as shown in the following figure:

In terms of scalability, the blockchain domain has used a layered architecture with Layer 2 technology such as State Channels to increase the transaction processing power of major blockchain networks, including Lightning networks on Bitcoin. ) and Plasma on the Ethereum .

In addition, in the next few years, with the use of Sharding technology, Ethereum will move to a sharded database model, processing transactions in parallel in 1,024 segmented chains, which will provide several orders of magnitude scalability. increase.

At the same time, there has been a lot of research on off-chain computation. Using zero-knowledge proof and other privacy protection technologies, we will be able to transfer more calculations to the chain while maintaining the advantage of trust. get on.

In general, these new layered architectures and technologies will enable the public chain such as Ethereum to grow by several orders of magnitude in terms of scalability, and ultimately enable these blockchain networks to handle large volumes of transactions, serving most financial use cases. .

At the same time, the user experience of blockchain networks and related applications is steadily increasing. For example, hosters and software providers are rapidly improving the workflow and key recovery procedures for private key management.

Over time, the nuances and frictions presented by each public chain will eventually be withdrawn from the end user, and the user may not even know that their financial services are running on the blockchain.

One day, blockchain-based financial services will set a new standard for user experience. The driving force behind this new standard is transparency, trust, and security (users will need these features once they become familiar with them). ). In these respects, traditional institutions are at risk of disintegration unless they also use the safest blockchain network—a change that does not occur naturally or quickly—and this is a fast-growing block. The opportunity for chain start-ups.

As for our understanding of the blockchain, perhaps it will develop like the Internet : at first, only experts can master the Internet; today, children have almost a natural instinct for its ability.

Financial products/services based on encryption contracts will take a long time to compete with traditional major financial institutions . But competition with traditional financial institutions may not be the most useful design. By occupying different parts of the risk/cost range, the encryption contract will expand the size of its economic cake by opening the door to industries and markets that are ignored by the current financial system or lack of financial services.

The most direct users of these financial products/services based on encryption contracts are organizations and individuals in the field of cryptocurrencies, many of whom have difficulty accessing basic financial services from traditional institutions. By providing open and transparent financial services, encrypted financial networks can have a large, addressable market that enables them to scale without directly challenging existing financial giants.

By the time they pose a real challenge to Wall Street, the defense of the latter may be too late, as the network effects of blockchain-based financial networks will become increasingly difficult to defeat as the network grows.

Finally, it is worth emphasizing that many of the projects built on the blockchain network are public utilities . In other words, the ultimate promise of these projects is to enable people connected to the Internet and carry mobile phones to control their economic life.

In today's world, people from different parts of the world and from social and economic classes have equal initiative, but they do not have equal opportunities. This inequality of opportunity is one of the biggest drivers of the widening gap between rich and poor , both within and between countries.

Financial services based on encrypted networks, as public Internet facilities (available to everyone and with the lowest level of rent-seeking), are our greatest hope for a world where opportunities are more equal . This is a world that people will fight for. Now, software provides people with the tools to achieve this .

Special thanks to Spencer Bogart, Kinjal Shah and Derek Hsue for their review and feedback on this article.

Author | Aleks Larsen

Edit | Jhonny

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- One-quarter of the nodes are hosted by AWS, is Ethereum really decentralized?

- Fighting against the US SEC? The Kik app will be closed and its cryptocurrency subsidiary will be laid off

- Science | Bitcoin governance

- Babbitt Column | On the Similarities and Differences of Traditional Contracts, Electronic Contracts and Smart Contracts

- Opinion: On the three major reasons for government cryptocurrency to replace banknotes

- North Korea is developing its own cryptocurrency to circumvent international sanctions

- A woman in Xiamen strayed into the "bitcoin investment" scam and was cheated 360,000 in 3 days!