Most investors are completely unable to determine whether a BTC is a currency, a commodity, a security, or other property. Economists point out that the value of BTC is influenced by the so-called "indeterminacy": "It relies on so-called self-fulfilling beliefs, and the belief in promoting self-realization is enormous." In other words, from the perspective of agnosticism The fundamental driver of BTC prices may be sunspots.

BTC has become a digital gold. This argument helps explain why BTC is attractive to investors and how its historical returns and non-correlation make it a part of a reasonable portfolio. Still, investors have a long way to go if they want to say why $10,000 is a good price or explain why there are unusual price fluctuations.

This vacuum of understanding may be an obstacle for investors to enter the crypto-asset market, but it also provides an opportunity for ambitious analysts to try to define new valuation methods and determine new fundamentals.

This white paper is for these analysts and it introduces concepts and metrics that can help us better understand cryptographic asset valuation. Our overview is not comprehensive—the field of cryptographic asset analytics is rapidly evolving, and new metrics and methods are emerging almost every week, which is one of the factors that make the industry so attractive to analysts and professional investors.

Product attributes of BTC and ETH

In this section, we will examine the value proposition of BTC and ETH and describe how the narrative based on the commodity investment analogy dominates. These analogies provide a way to assess the supply and demand relationship between BTC and ETH: understanding the supply curve and the basis of the drive demand to arrive at a quantifiable estimate.

Digital Gold BTC

The potential use of BTC in global commercial and digital investment contracts has been noted, but in 2019, the sentiment surrounding BTC has become clear that it is “a means of digital storage of wealth that is difficult to extract, freeze or depreciate”. Investors understand the global demand for such assets, because during the financial crisis, governments of all sizes tend to eliminate domestic debt through inflation. BTC's storage and transfer costs are relatively negligible, and it is the gold of the digital age. The fundamental factors behind the gold price, such as supply demand and macroeconomic indicators, are well understood.

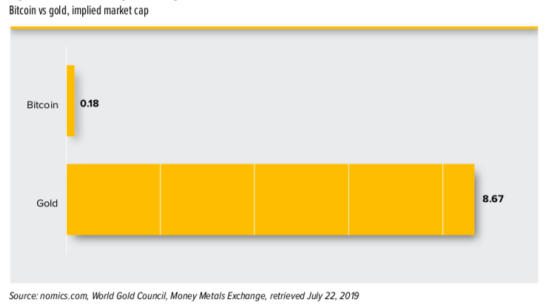

There are many reasons for the lack of attractiveness of BTC as a gold substitute, the most important of which is its history is too short compared to the long-term status of gold as a means of value storage. To figure out the value of BTC as a digital gold, an easy way is to calculate its implied value against a certain percentage of the demand for gold.

BTC's golden road is long

Digital petroleum ETH

The BTC divides the task of controlling the money supply and provides it to computers around the world, as does Ethereum in terms of computing. The data and logic behind the Ethereum application is “decentralized” and can run “decentralized applications” or “DApps” on the Ethereum protocol, a network that connects computers worldwide.

ETH itself is a payment currency used to purchase the processing power of the network. Those who expect ETH demand to grow will think that distributed applications will have an advantage over centralized existing applications. This can happen, for example, if “anti-Facebook sentiment” prompts users to seek alternative social networks. In other words, ETH may be the oil of the information economy.

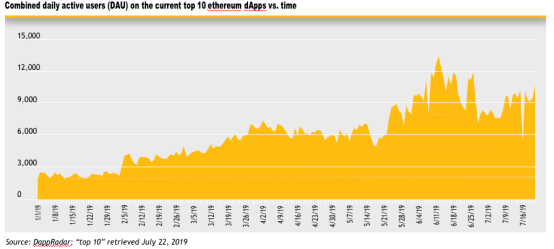

Just as the metrics for FAANG (Facebook, Amazon, Apple, Netflix, Google) stocks are subscribers or active users, similar basic metrics can be used by Ethereum and several other competitors' DApp platforms. Since the transactions on these networks are public, they can be measured in real time. So far, there is little evidence that any user demand based on Ethereum's DApp is comparable to Facebook or other FAANG companies, which means that they are still small.

The demand for Ethereum data “oil” is growing?

Tracking indicators of digital gold demand

Like commodities, BTC and ETH do not generate revenue, so they must be evaluated against supply and demand. Analysts are continuing to develop and refine new metrics. Prices and market capitalization are not enough, and in some cases they may be misleading. The following are some of the emerging indicators, and we will explain their use in BTC networks. (Most also applies to ETH and other cryptographic assets.)

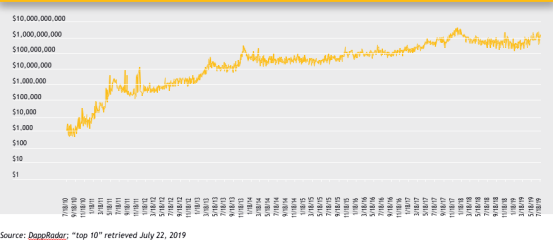

Metcalfe's law Metcalfe's Law is named after the pioneer of Ethernet cable Bob Metcalfe, which assumes that the effect of the network is proportional to the square of the number of participants. In other words, the value of the network to its users grows logarithmically with the increase in new users, rather than linear growth. A typical example is a fax machine: two fax machines can form one communication path, and four fax machines can generate six. Facebook is a good proof that its revenue growth is indeed proportional to the square of the number of users. Unfortunately, the same logic does not apply to cryptographic assets. The number of active addresses is independent of the price of the BTC. It shouldn't be relevant: Metcalfe's law deals with effects, not values. A larger network of fax machines increases the efficiency of each fax machine on the network; it does not represent a higher value for each individual machine or telecommunications service. To determine the value of the BTC, a more detailed understanding of the BTC's trading and holding methods is required.Trading volume Trading volume is an indicator of BTC usage. In this regard, BTC is often compared to larger payment networks such as Alipay, SWIFT and VISA. However, we are talking about BTC as a means of value storage, similar to gold. Gold is not used to buy coffee. Compared to more mature commercial payment methods, BTC deals with fewer transactions, but its average transaction value is much higher. The chart below shows the logarithmic increase in BTC daily trading volume (24-hour chain trading volume multiplied by BTC closing price). BTC's trading volume is billions, but less than 10 billionBTC holding day was destroyed Trading volume is interesting, but it does not necessarily reflect real economic activity. For example, for security and convenience, users may transfer a large number of BTCs from one account to another. The “BTC Holding Date of Destruction”, first proposed in 2011, is an indicator of the extent of changes in long-held BTC balances. When a user moves them for 1000 days after holding 100 BTCs, it is equivalent to “destroying” 100,000 BTC holding days. This number is the same even if the BTC is sent to multiple addresses. This eliminates some of the internal account management transaction noise, providing more accurate information about real economic activity.Market value achieved In addition to the volume of transactions, it is also useful to measure how much wealth is stored in the BTC. In the stock market, this is achieved by “market capitalization”, which is the stock price multiplied by the number of shares outstanding. The same calculations are often applied to BTCs and other cryptographic assets, removing a large number of assets that are lost, inaccessible, or excluded by the market—according to data from the encrypted asset data company Chainalysis, these assets are up to 3.7 million BTCs, encrypted asset data company Coin Metrics analysts have come up with an indicator they call "realized market capitalization." “Achieved Market Value” refers to the market value of each BTC at the time of the last transaction. Every change in ownership will cause this number to change. For example, if a user purchased 100,000 BTCs on July 1, 2011 and held them all the time, then on July 1, 2011, the realized market value of the BTC asset will be at the BTC price for that time (ie $15.40) for calculations.

“Practical tokens”: Valuation of cryptographic assets other than BTC and ETH

BTC may be similar to digital gold, ETH may be similar to digital oil, but hundreds of other crypto assets? Some of them are intended to improve the BTC and ETH models and may be evaluated using some of the same metrics listed above. Others are more like private currencies, such as game tokens, casino chips or temporary vouchers. Stocks and bonds represent claims for future returns, so the changes in issuer wealth are well grasped. What is the relationship between a game currency and the income of the Chuck Cheese Restaurant (a chain of restaurants that combine American fast food, games and entertainment)? Some early crypto-asset analysts tried to answer this question and described how cryptographic assets capture value in decentralized applications. Here are some examples of their work.

Encrypted assets in the form of tokens

A company captures the value of business flow by charging a higher cost than a product. Decentralized applications may have similar value streams, but they have no value capture points. It may eliminate the risk of rent-seeking middlemen or reduce counterparties, but crypto assets used to implement incentives on such a network may not have cash flows associated with them. Some observers have suggested that these so-called "utility tokens" be evaluated as private currencies rather than discounted cash flows. They see the asset holder network as an independent economy and apply the currency exchange equation expressed in mv = pq. In this equation, m is the supply of money, v is the velocity of the currency (the frequency of turnover), p is the “price level” (measured in US consumer price index), q is the new commodity in the economy and The number of services. This equation has been part of the analysis of cryptographic assets since the early days, but during the 2017 dollar financing boom, many “practical token” issuers ignored this. They ignore the careful study of how to use a proprietary currency to gain value. In the exchange equation, the increased trading activity "v" is a measure of how quickly people take off the currency they hold. In other words, high circulation speeds are related to currency depreciation. Low speed indicates the tendency to hold it. Unlike gold, people over the age of 15 do not hoard Chuck cheese restaurant tokens.

Encrypted assets in the form of work permits

As a more mature understanding of value capture, some investors suggest that utility tokens are not considered a medium of exchange, but rather a license to work. Asset holders are suppliers to private bilateral markets who must “pled” tokens in order to support payments. Fund managers at multi-investment venture capital firm Multicoin Capital refer to this model as “working tokens” and point out that this model supports network usage and is a fundamental driver of the value of encrypted assets.

Encrypted assets in the form of governance

Based on the concept that crypto assets are work permits, some investors have proposed a new, more participatory form of investment. Traditional finance ignores participation rights (such as voting rights) and only priced stocks based on their expected cash flow rights. However, CoinFund and Placeholder Ventures, two managers of funds focused on crypto assets, have proposed “generalized mining”, a way for investors to generate returns by having other rights acquired by crypto assets. In the case of a cryptographic asset in the form of a work permit, an investor holding a token in a decentralized Uber may use data science to determine the most profitable location. Investors get a return on their profits through the services they provide on the web. As this operation increased the number of cars and car activities on the network, it increased the “right to assets” and Placeholder recommended it as a metric for basic analysis. The term “generalized mining” comes from BTC, in which “miners” must consume resources to obtain a return on transaction verification. Other encrypted network designs require the verifier to "pledge" the asset to achieve the same kind of return. These forms of work are ways in which investors can actively participate and earn income. Skeptics point out that speculators are as likely to be short as they are long. Participatory models may invite forms of participation that are not intended to increase the value of assets, not to mention whether professional investors other than VCs are willing to pick up their sleeves to drive a taxi or mine tokens. This is doubtful.

in conclusion

As can be seen from this review, the advanced concepts proposed by early adopters of crypto assets pose serious challenges for investment innovators. The basic principles of crypto-asset evaluation are accepted by most professional investors and there is still a long way to go. The purpose of this article is not to promote or expose them, but to introduce them objectively as an institutional resource for considering the investment in encrypted assets. Perhaps some of these organizations will have some ideas, and these ideas will become examples of asset valuation in this area in the future. We hope to incorporate these ideas into future versions of the resource.

The content is for reference only, not as an investment recommendation.

Copyright is strictly prohibited without permission

We will continue to update Blocking; if you have any questions or suggestions, please contact us!