Dragon White: A practical Chinese central bank digital currency and Libra design

Author: Long Tao white, computer Tsinghua University undergraduate, master's and doctoral. I like to study blockchain and cryptocurrency technology and monetary and financial theory. Continuous entrepreneurs. He founded Zhixiang Technology, which focuses on financial cloud computing, quantitative investment, and machine learning. He obtained 27.5 million RMB investment from Qifu Capital; he served as chief technology officer of Zhongjin Jiazi Investment Fund before starting business; Data co-founder and chief strategy officer; previously a senior executive in financial services at Accenture Consulting and IBM Global Consulting Services, providing long-term technical, business and strategic consulting services to clients in China's financial services industry, representing Accenture as Shanghai Securities Chief designer of the Exchange's new generation trading system project.

Babbitt Information: This article is another masterpiece of Dr. Long Bailu following " The History, Current Status and Future Evaluation of Libra " from the Monetary and Financial System , the " Financial Model of the CFMI Pass and the Mechanism of Stabilizing the Currency ". This article focuses on the central bank digital currency (CBDC), combined with in-depth research on Libra, and proposes two sets of design plans for the Chinese central bank digital currency (CBDC) and Libra China version from a forward-looking perspective. It is also the industry's first systematic and detailed academic. Rigorous overall design article. Babbitt information is especially recommended to readers.

The following is the text:

introduction

Since the release of the Libra white paper by Facebook, there has been a lot of discussion around the world. China is particularly hot about how the Chinese government and the private sector should respond to the challenges Libra brings, whether the Chinese version of Libra should be developed, and once again spurred attention to the Central Bank Digital Currencies (CBDC).

- Encrypted currency and class traversal (5): The digital printing industry has ushered in a heavy elite organization. Do ordinary people have the opportunity to turn over?

- Stick to the dead sky! Gold predators indicate that the higher the bitcoin rises, the more people prove the wrong

- Fed interest rate meeting, interest rate cuts expected or lay a solid foundation for bitcoin prices

Some important features of Libra, such as super-sovereignty and international payment convenience, have important reference significance for the challenges and implementation paths of RMB internationalization. Therefore, this article will focus on the design of a practical Chinese CBDC (hereinafter, unless otherwise specified, CBDC refers specifically to the Chinese central bank digital currency) and discuss its impact on financial stability. This paper also believes that the Chinese folk version of Libra (hereinafter referred to as Libra-x) and CBDC are different from the issuer (the former is dominated by the enterprise consortium, the latter is dominated by the central bank), and its design goals and implementation methods are very similar. Therefore, this paper will also discuss the Libra-x design based on the CBDC design. Unless otherwise stated, this discussion of CBDC will apply to Libra-x.

The author of this article is not aware of the research and development work of the central bank's digital currency, which is being promoted by the People's Bank of China. This paper proposes a CBDC feasibility proposal only from the perspective of theory and practice. It only represents the author's personal views and does not reflect any official opinions and working conditions. .

Chapter 1 Design of China Central Bank Digital Currency CBDC

Introduction

From the perspective of financial stability, the CBDC design plan should follow the following principles to avoid or mitigate the impact of the introduction and implementation of CBDC on the stability of existing financial systems:

- Do not introduce uncertainty into existing monetary policy instruments and transmission mechanisms;

- Considering that CBDC may serve a completely different core objective, introduce new monetary policy tools for CBDC as much as possible;

- Does not change or significantly weaken the business model of commercial banks (creating deposit currency through loans, providing credit and liquidity to society);

- Does not affect or significantly weaken the ability of the entire financial system (after the introduction of CBDC) to provide credit and liquidity to the entire society;

- Avoid commercial bank runs that may result from the introduction of CBDC (such as depositors switching from bank deposits to CBDC on a large scale)

In 2017, the Bank for International Settlements (BIS) proposed in its quarterly comment [1] that the famous "Flower of Money" proposed a relatively complete taxonomy of different currency forms. In March 2018, the publication of the BIS paper [2] The CBDC conducted a comprehensive review of its impact on payments, monetary policy and financial stability. Major global central banks and major monetary policy institutions are in full swing to conduct research in the field of CBDC. Different CBDC systems may have very different scope of application in principle. Some regard CBDC as the electronic version of central bank cash, some regard CBDC as the central bank reserve for expanding accessibility, and some regard CBDC as a substitute for commercial bank deposits. Some CBDC systems continue the existing central bank/commercial bank account-based system, and most CBDC systems are expected to be token-based.

At present, the renminbi is still under capital control and cannot be freely convertible, but the renminbi is facing strong international demand. For example, it is necessary to encourage more countries to use the renminbi for pricing and settlement in a wider range of trade practices, or to use the renminbi as a value storage tool or reserve currency. . In this paper, the demand for RMB internationalization is further extended in the scope of super-sovereignty. RMB CBDC should allow a wider range of entities to participate in its issuance process and share the coinage tax. Therefore, this paper defines CBDC as follows:

- The CBDC is a form of currency of the central bank that is consistent with the face value of other forms of central bank currencies (such as cash and reserves) (ie, maintaining parity);

- Compared to central bank reserves, CBDC allows for broader access to the main body (the former is accessible only to commercial banks, some payment institutions and foreign central banks, which are designed to allow commercial banks, non-bank financial institutions, households and companies to access);

- The CBDC is token based and the reserve is account based;

- Use a separate operational architecture with other forms of central bank currency, thus allowing CBDC to serve completely different core objectives;

- The CBDC can be interest-bearing and, under reasonable assumptions, can pay interest different from the reserve;

- In addition to supporting retail payments, CBDC supports cross-border payments. In contrast, cash is primarily a retail payment instrument, while reserves are primarily used for interbank clearing purposes;

- The CBDC's issuance mechanism can be different from cash and reserves, such as supporting different collaterals, allowing a wider range of entities to participate in CBDC issuance.

Further explanation for the above features:

Feature 1: This feature has two meanings. The first layer of meaning points out that CBDC is a kind of debt of the central bank, which belongs to the category of traditional currency concept M0, which is consistent with the statement of the Chinese Central Bank Research Bureau Director Wang Xin that CBDC is positioned at M0 [3] . The second layer of meaning indicates that CBDC needs to maintain a parity relationship with other forms of central bank currency. In most currency frameworks, different types of central bank currencies can be exchanged at equal face value. For example, one unit of central banknotes can exchange one unit of central bank reserves, but there are some authors suggesting to break this tradition, especially in the case of CBDC. under. For example, Kimball and Agarwal's paper [4] describe a framework in which a flexible exchange rate can be maintained between cash and CBDC to help achieve cash negative interest rates to overcome the classic “liquidity trap”. This means that an economy runs two legal currencies simultaneously, even though they are under a manageable exchange rate. This will pose a serious challenge. Is cash or CBDC the financial accounting unit of the economy? If both types of legal currency are widely used, all goods and services have to be quoted in two ways, which will bring serious management costs. The industry generally agrees that managing both currencies at the same time will pose significant risks to currency stability. Therefore, although theoretically CBDC can have different denominations from other forms of central bank currency, this paper assumes that CBDC must be consistent with the central bank's other forms of currency, meaning that under the CBDC scenario (same as Libra-x), there is no new financial record. The necessity and possibility of the account unit.

Feature 3: The existing monetary system is account-based. For example, the central bank only opens a reserve account for a few institutions including commercial banks, while commercial banks open deposit accounts for ordinary users; cross-bank payments need to be cleared in real time by the central bank ( The Real Time Gross Settlement: RTGS) system clears the relevant commercial bank between the central bank's reserve accounts. The CBDC is a token-based system, so all participants can transfer and pay directly without relying on the existing RTGS system. Therefore, the token-based design also provides the possibility for 4).

Based on the above definition of CBDC characteristics, this paper will explore whether CBDC can be used as a new monetary policy tool, in conjunction with price rules (the central bank sets CBDC interest rates to allow its quantity to change) or quantity rules (the central bank sets the supply of CBDC) Volume to allow its interest rate to change).

According to the definition of CBDC, this chapter will discuss the relationship between CBDC and the existing monetary system, and discuss the four core principles of CBDC in detail for potential financial stability risks, and analyze its impact on financial stability.

The ternary paradox of CBDC monetary policy

Bjerg's paper [5] modified the classic monetary policy ternary paradox to make it applicable to two competing domestic monetary systems – the central bank and the commercial banking system. This paper uses a similar approach to modify the classic model to be applicable to two competing domestic currency systems, CBDC and the existing central bank monetary system.

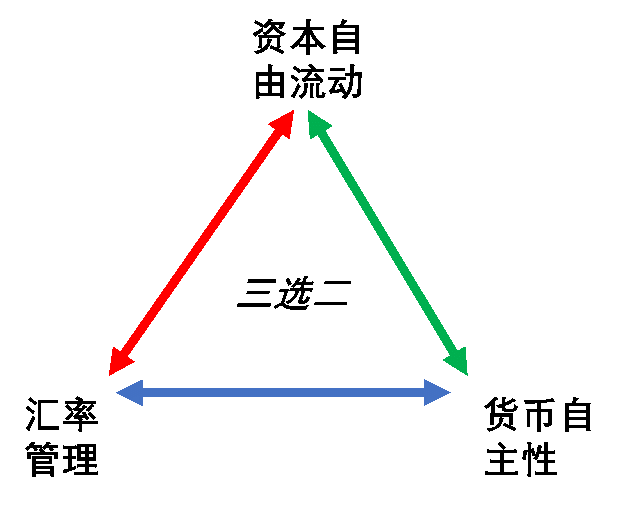

The original idea of the classic monetary policy ternary paradox came from Keynes [6] , followed by Mundell [7] and Fleming [8] , and finally Obstfeld and Taylor [9] gave the now widely known definition – "open economy" The ternary paradox of macroeconomic policy… follows a basic fact: an open capital market deprives a government of its ability to simultaneously realize its exchange rate and use monetary policy to achieve other economic goals." Figure 1 below summarizes the ternary paradox that any monetary policy authority (government or central bank) can only achieve two of the following three policy objectives: monetary autonomy to set interest rates, manage currency exchange rates, and The free flow of capital. For example, the renminbi implements a floating exchange rate with the US dollar, and chooses a manageable floating exchange rate and currency autonomy for setting interest rates among the three policy objectives, at the expense of free capital flow; the Hong Kong dollar implements a linked exchange rate system with the US dollar fixed exchange rate, The choice among the three policy objectives is to manage the fixed exchange rate and the free flow of capital, while sacrificing the monetary autonomy of setting interest rates.

Figure 1: The ternary paradox of classic monetary policy

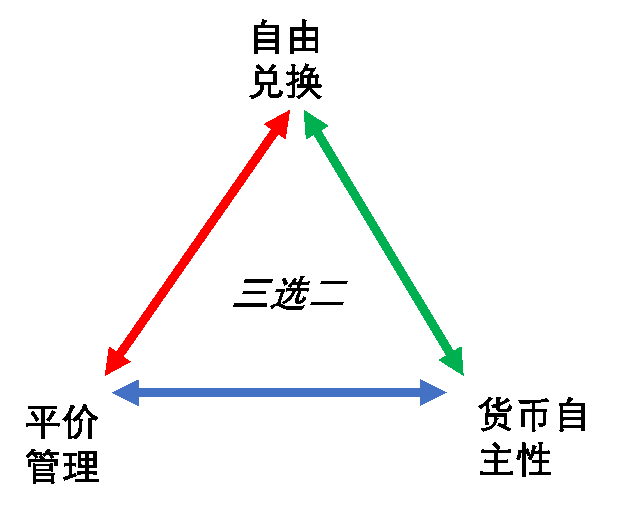

The function of the CBDC is basically equivalent to the existing monetary system of the central bank, thus forming some form of competition between the existing monetary system and the CBDC, which can be compared with the competition between different currencies in the ternary paradox of the classic monetary policy. The realization of CBDC will bring about the same type of contradiction in the classic ternary paradox. We converted the classic model into the model shown in Figure 2 according to the following rules:

- The traditional policy objective of exchange rate management between the two currencies translates to ensuring financial stability by maintaining CBDC consistent with the face value of other forms of central bank currency (ie, maintaining parity) ;

- The traditional policy goal of setting the monetary autonomy of the central bank's interest rate is transformed into the monetary autonomy of setting the CBDC interest rate;

- The traditional policy goal of free capital movement translates into the free exchange of CBDC and other forms of central bank currencies, including cash, reserves and bank deposits. Implementing CBDC will introduce this redemption. The CBDC allows all entities to access the central bank's balance sheet, and the average user has the opportunity to choose whether to hold commercial bank deposits or CBDC for the first time.

Figure 2: CBDC monetary policy ternary paradox

According to the definition of CBDC, maintaining the face value between CBDC and other forms of central bank currency is a policy goal that must be chosen. The remaining two policy objectives, choose to be able to set CBDC interest rates, or choose free exchange between CBDC and other forms of central bank currency?

The CBDC is designed to support cross-border payments. If CBDC can be freely exchanged with other forms of central bank currency, it will directly undermine China's existing foreign exchange management system; in addition, considering that CBDC is actually a safer, risk-free liquidity than bank deposits. Assets , if CBDC can be freely exchanged with the central bank's reserves, it is easy for users to switch bank deposits to CBDC on a large scale, which forms a “run” of the entire banking system (described in detail later). Considering the above two points, we must rule out the policy objectives of free exchange .

Therefore, in the CBDC design, we choose to maintain the policy objective of CBDC consistent with the central bank's other forms of currency and the ability to set CBDC interest rates , and abandon the policy objectives of CBDC and other forms of central bank freely convertible .

So far this paper has drawn the policy objectives of CBDC design. The core principles of CBDC will be used to discuss in detail the CBDC interest rate issues, the convertibility of central bank reserves and bank deposits, the method of maintaining parity with bank deposits, and the method of CBDC issuance.

CBDC Core Principles

Michael Kumhof of the Bank of England and Clare Noone of the IMF presented the core principles of CBDC in the paper [10] to reduce the risks brought to the commercial banking system after the introduction of CBDC. These principles are: (1) CBDC pays an adjustable interest rate; (2) CBDC is different from the central bank reserve, and the two cannot be exchanged; (3) the central bank or commercial bank does not guarantee the exchange of bank deposits to CBDC; (4) the central bank only CBDC is issued based on eligible collateral (mainly government bonds).

CBDC pays adjustable interest rates

The most fundamental reason for paying adjustable interest rates for CBDC is to maintain price stability and maintain parity between CBDC and other currencies. The supply and demand of CBDC in the market needs a price to reach equilibrium. Suppose CBDC pays zero nominal interest rate like cash. If the central bank over-provisions CBDC because of the inaccurate forecast of real CBDC balance, then the method of eliminating over-supply can only be as follows: (1) CBDC depreciation thus destroys CBDC The parity relationship with other forms of currency, or (2) reducing the true value of the nominal CBDC balance makes it consistent with the real demand of CBDC, thus clearing the market through the general price level, but doing so directly violates the central bank's anti-inflation target. If the interest rate paid by CBDC is fixed, there is no third possible method. However, the adjustable interest rate can increase the demand of CBDC without the adjustment of the central bank's balance sheet, without destroying the parity relationship and without the price level adjustment.

CBDC is different from reserve and cannot be exchanged

First, this principle helps maintain financial stability when depositors seek to switch to CBDC in large numbers. If CBDC and reserves are freely convertible, in this case, a single bank willing to pay CBDC for deposits is enough to threaten financial stability. This stems from the bank's commitment to settle interbank payments in reserves through the RTGS system. When a bank pays CBDC for deposits, all non-bank entities can take advantage of this by transferring the deposit to the bank. When the deposit is lost to the bank, other banks must use the RTGS system to settle interbank payments with reserves. When the central bank supports the immediate conversion of the reserve to CBDC, the bank can use its newly acquired reserves to obtain CBDC in order to pay to the depositors for this purpose. This will result in the destruction of deposits and trigger a system-wide, almost instantaneous bank run. Similarly, if the reserve is the same as the CBDC, the run can be triggered in the same way by the RTGS system.

Second, this principle enables the Reserve Fund and CBDC to serve their respective core objectives. CBDC can be used not only as a retail payment medium, but also as an interbank settlement asset, and also supports cross-border payments. This gives the central bank a new policy tool, especially the number or interest rate of CBDC. This allows the central bank to maintain control over the amount of reserves and its interest rates in the financial system. Maintaining control over reserves allows the central bank to continue to influence risk-free interest rates in the economy, which is a key factor in actual investment decisions and cross-cycle allocation decisions.

Papers by Jack Meaning and Ben Dyson of the Bank of England [11] argue that the reserve market has been incorporated into the new CBDC system. Or, they assume that CBDC was created by expanding access to reserves rather than introducing a new central bank currency. This system of expanding reserve access may affect the transmission mechanism of existing monetary policy in an unknown way, and if the reserve and CBDC remain separated, the traditional monetary policy transmission mechanism through policy interest rates will remain unchanged.

Michael Kumhof's paper [10] further examines the arbitrage of household and corporate sectors and bank arbitrage from the perspective of CBDC's convenience yield, demonstrating the reserves and CBDC in the equilibrium state of arbitrage and non-arbitrage. Interest rates do not converge to the same value, so they are different. Core arguments include:

- The risk-free nominal interest rate of an economy equals the interest rate of a nominally risk-free pure value storage asset (such as local currency short-term government instruments);

- The nominal interest rate currently paid for the reserve, or equal to, or arbitrage, is closely related to the risk-free nominal interest rate of the economy;

- The interest rate of CBDC is equal to the risk-free rate minus the convenience income of CBDC (ie the premium of CBDC as a trading medium);

- The convenience income of the CBDC decreases as the number of CBDCs increases. The marginal holders of the CBDC are the corporate and family sectors, and their demand for CBDC and the central bank's supply of CBDC determine the convenience of CBDC. In the case of marginal holder non-arbitrage, such as CBDC's convenience income is zero, the CBDC supply is required to be at a saturation point – the supply of CBDC is close to the level of bank deposits. This will bring two challenges: the first is the lack of sufficient qualified collateral central bank can be used to issue CBDC; the second is if the liquidity of CBDC supply reaches the level of bank deposits, which will make bank deposits and loans not It is necessary to destroy the bank's business model. Therefore, the reasonable expectation is that the central bank will only issue CBDC in moderation ;

- Because it is not a marginal holder of CBDC, it is very unlikely that a bank will receive more marginal benefits from holding a CBDC than it holds a reserve or bond. Therefore, banks tend not to hold large amounts of CBDC because the opportunity cost is too high. Banks holding CBDC's decisions are similar to banks holding physical cash, minimizing holdings only to satisfy customer requests.

The central bank or commercial bank does not guarantee the exchange of bank deposits to CBDC

Some CBDC studies [11] suggest that banks are obligated to convert deposits to CBDCs at any time, in any quantity. They believe this is the key to maintaining CBDC and other forms of central bank parity. The paper [10] discusses that it is neither dangerous nor necessary to use this recommendation as a necessary feature of CBDC.

The danger comes first from the credibility of the obligation. When the net inflow of CBDC and net outflows is small and the action is slow, the banking sector may be able to cope. However, the challenge is whether or not the obligation can be fulfilled during the stress period. Assuming that the entire non-banking sector needs more CBDCs, and that the entire banking sector runs out of its own CBDC, banks need to sell or repurchase qualifying assets to the central bank to obtain CBDC. The central bank may have to expand the list of eligible collateral, or even completely waive the collateral requirements for large unsecured loans. Therefore, the credibility of this obligation depends on the commitment of the central bank as the lender of last resort. Given the potential size of liquidity requirements, there may be unprecedented risks to the central bank's balance sheet. In other words, the bank is ready to convert the deposit into a CBDC guarantee must ultimately be guaranteed by the central bank.

If the central bank promises to accept bank deposits in exchange for CBDC in an emergency, this will open the door for bank deposits to CBDC. It is conceivable that this kind of run can be run almost instantaneously, at an unprecedented scale, because it is run from the entire banking system, not from one bank to another. This reflects the fact that the liquidity support that the banking sector may need to request from the central bank will be an order of magnitude larger than the traditional bank run.

It is also not necessary to guarantee the convertibility of deposits to CBDC to maintain the parity of CBDC and bank deposits. In fact, you can maintain the parity of CBDC and bank deposits as long as the following conditions are met:

- The central bank may allow adjustments to CBDC's interest rate (according to the CBDC quantity rule), or allow the exchange of non-deposit qualifying assets to adjust the number of CBDCs (according to CBDC price rules), thus allowing the private sector to expect parity relations to be maintained. In other words, the central bank continuously and reliably meets the needs of CBDC according to the target quantity or price;

- CBDC Qualified Assets has an operational and liquidity market;

- At least one private sector participant (which may be a bank or non-bank financial institution) can receive/initiate payments from bank deposits and be active in the CBDC market and the CBDC qualifying asset market.

Condition 1) speaks for itself. According to the CBDC design goals, eligible assets can be government bonds or native digital assets. The former corresponds to the mature bond trading market, and the latter corresponds to the emerging digital asset exchange. Conditions 2) and 3) allow the agent to take advantage of any arbitrage opportunities in the market to push the parity deviation between CBDC and bank deposits to zero. Under these conditions, a reasonable result is that there will be a large liquid private market where the family and corporate sectors can trade bank deposits with CBDCs, and a small number of participants can access the inventory of qualifying assets to obtain additional CBDCs from the central bank. . Therefore, relying on this market, plus at least one participant can trade on any arbitrage opportunity, can ensure bank deposits and CBDC parity. The risk of relying on this market is much less than the risk of relying on bank exchange guarantees.

We further explain that the above arbitrage mechanism drives the maintenance of CBDC and deposit parity. Suppose CBDC trades to a deposit at a 1-x (x>0) exchange rate. Then, the financial institution can obtain 1 RMB unit deposit inflow from the customer, buy 1 RMB unit bond in the market, immediately sell 1 unit bond to the central bank for 1 unit CBDC, and deliver 1-x CBDC to the customer, thus locking The x unit CBDC is a risk free profit. Arbitrage will drive x to zero. Please note that it is the central bank that promises to pay 1 unit of CBDC for a value of 1 unit of “deposit currency”, ie the central bank uses a parity exchange rate in its operations, thus enabling this strategy to work.

In terms of preventing runs, there are several other ways to establish a CBDC system to limit the conversion of deposits to CBDCs, for example, to limit the amount of deposits a bank must convert to CBDC within a specified period of time or to limit the number of CBDCs held in a CBDC account. However, even at normal times, these limits have the risk of not maintaining parity. In addition, as stated in the paper by Gürtler and Nielsen et al. [12] , CBDC's holding cap will limit the amount or value of transactions that may be made, potentially damaging the effectiveness of CBDC as a payment system. Regarding financial stability, Callesen's paper [13] argues that if a sufficiently high cap is set to make CBDC useful in trading, it would be too high to control the risk of a bank run. Therefore, this core principle is expressed as the fact that banks are not obligated to provide CBDC for deposits. Banks are free to exchange CBDC for deposits, or they are not redeemable. This is a flexible approach that allows banks to decide for themselves how to manage the risks they face.

The central bank issues CBDC only on eligible collateral (mainly government bonds)

The core principle is that the central bank only uses its selected eligible collateral to redeem CBDC. It does not support the use of reserves or bank deposits for CBDC. This principle allows the central bank to manage the risk of issuing CBDC to its own balance sheet, just as it does for issuing reserves and cash. More importantly, these issuance arrangements can eliminate the risk of a run on the banking sector as a whole, either because CBDC and reserves are convertible, or because CBDC and bank deposits can be redeemed immediately.

Now, we explain how to provide CBDC from the perspective of policy rules. The quantity rule determines the amount of the corresponding central bank currency and allows its interest rate to be adjusted. The price rules determine the interest rate of the corresponding central bank currency and allow its quantity to be adjusted. The terms of price rules and interest rate rules are interchangeable.

The CBDC can be provided according to quantity rules or price rules. According to the CBDC quantity rule, the central bank will not issue CBDCs to cope with the increase in demand, but will allow CBDC's interest rate to be adjusted downward until the market clears. According to the CBDC price rules, the central bank sets the CBDC interest rate and allows the private sector to determine its quantity. In doing so, the central bank is free to issue (or withdraw) CBDCs to the private sector on an as-needed basis, limited to qualifying assets. According to such rules, the issuance arrangement of CBDC is crucial.

Assume that the qualifying assets only contain government bonds. A private sector agent who wants to convert bank deposits into CBDC must first exchange deposits for bonds, then provide the bonds to the central bank in exchange for CBDC, or the agent must find a counterparty who uses bonds to convert CBDC from the central bank and is willing to use the agent. The deposit is exchanged for CBDC. Through these transactions, as long as the bonds are not obtained from the banking sector, the deposits will not leave the overall banking system, they simply transfer to the sellers of the bonds. Therefore, when the private sector receives additional CBDCs, bank financing will not “disappear” overall. The key to achieving this result is that the central bank will not accept bank deposits in exchange for CBDC. In other words, it does not directly fund commercial banks. This forces the agent to first convert the bank deposit into an asset that is not a bank liability. Here, the bond, the stakeholder holding the CBDC will reduce its bond holding rather than deposit holding.

If the source of the bond is the banking sector, the overall balance sheet of the banking sector contracts, but we will continue to discuss it later, which will not immediately affect the amount of credit or liquidity in the economy. In addition, if the bank is not obligated to provide CBDC for deposits (as suggested above), then the bank will not be forced to use its own bonds to provide CBDC for deposits in the first place.

At present, the RMB issuance mechanism is based on the US dollar foreign exchange, and is supplemented by the open market operation mechanism (that is, the commercial bank borrows/returns additional liquidity by entering into a repurchase agreement with the central bank through mortgage-qualified assets). It can be seen that the CBDC issuance mechanism is different from the RMB. The domestic financial and regulatory circles have been clamoring to change the mechanism of relying too much on foreign exchange payments to avoid excessive renminbi impact on the US dollar monetary policy and economic cycle.

CBDC provides China with a suitable opportunity to try to change the CBDC issuance mechanism: cancel foreign exchange holdings, and mainly obtain/recover liquidity by selling/purchasing qualified assets to the central bank ; in addition, it can also enter into the central bank through mortgage-qualified assets. Repurchase agreements to borrow/return additional liquidity. At present, the People's Bank of China has developed a wealth of policy instruments for open market operations, allowing financial institutions to borrow/return liquidity to the central bank, including short-term liquidity adjustment tools (SLOs) within 7 days and standing loan facilities of 7 days to three months ( SLF), a three-month to one-year medium-term loan facility (MLF) or a tool with a longer term. The central bank only needs to adjust these tools to apply to CBDC.

The central bank can also develop a special catalog of eligible collateral for CBDC, which can include high-credit renminbi/ sovereign debt, financial corporate bonds and corporate bonds . In order to strengthen the positioning of CBDC as a super-sovereign currency, foreign currency sovereign bonds and original digital assets (such as Bitcoin and Ethereum) can also be added to the eligible collateral list , which can weaken the impression that CBDC is dominated by China and encourage relevant countries. Actively participate in the issuance of CBDC. Increasing foreign currency assets into the list of eligible collateral will bring additional exchange rate risk to the central bank's issuance of CBDC, but mainstream central banks have relatively rich experience in this regard. Native digital assets are more volatile than traditional bonds and require more careful management of their market and liquidity risks. The author's paper [14] details the method for issuing and supplying cryptocurrency stabilized coins based on native digital assets.

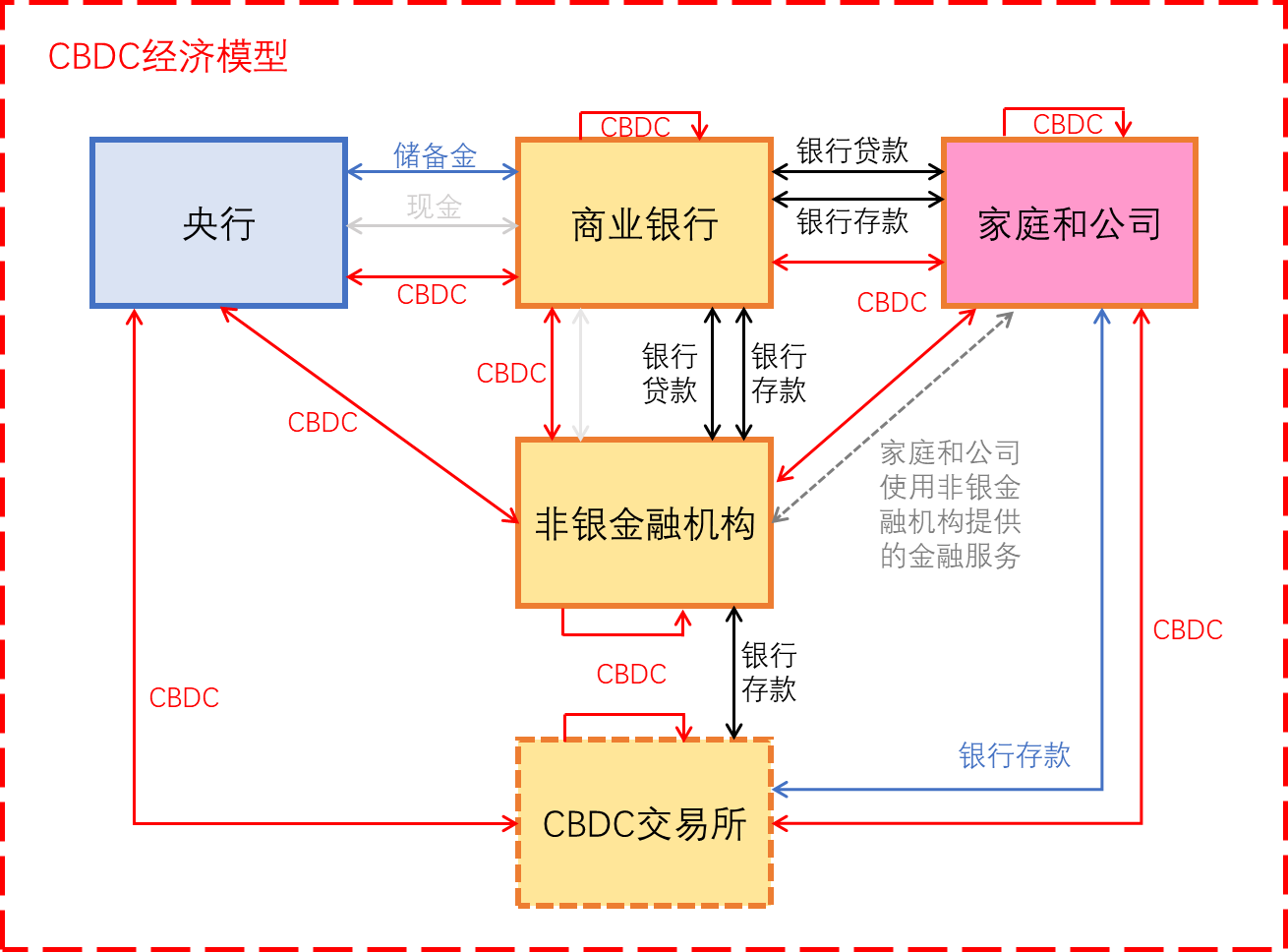

China CBDC Economic Model

Michael Kumhof's paper [10] proposes three CBDC economic models in which the entire economy's CBDC access model (Economy-wide Access Model), all participants, including banks, non-bank financial institutions, households and companies, can access CBDC, therefore CBDC is the currency of all agents in the economy. This is in line with the definition of CBDC function in this paper, so this paper builds China CBDC economic model based on this model, as shown in Figure 3.

Figure 3: China CBDC Economic Model

Access to CBDC by all agents does not mean that the central bank provides retail services to all CBDC holders. In the CBDC economic model, only banks and non-bank financial institutions can directly interact with the central bank to buy and sell CBDC, while households and companies must use CBDC exchanges to exchange deposits for CBDC. Of course, families and companies can always trade each other to buy and sell CBDC. . The CBDC exchange can be a new independent entity or operated by a bank or non-bank financial institution, but for clarity of explanation, this article considers the CBDC exchange as an independent entity.

Commercial banks maintain debit and credit positions for non-bank financial institutions, households and companies (indicated by “bank deposits” and “bank loans”). Non-bank financial institutions provide financial services to households and companies, such as fund management services, with the result that non-bank financial institutions bear debts to households and corporate sectors.

The CBDC Exchange performs the following four types of transactions:

- Sell/purchase CBDC to/from home and company to exchange bank deposits;

- Sell/purchase deposits to/from other private sector counterparties to exchange central bank eligible collateral (eg government bonds);

- Selling/purchasing bonds to/from the central bank to exchange CBDCs;

- Enter into a repurchase agreement with the central bank to borrow/return CBDC

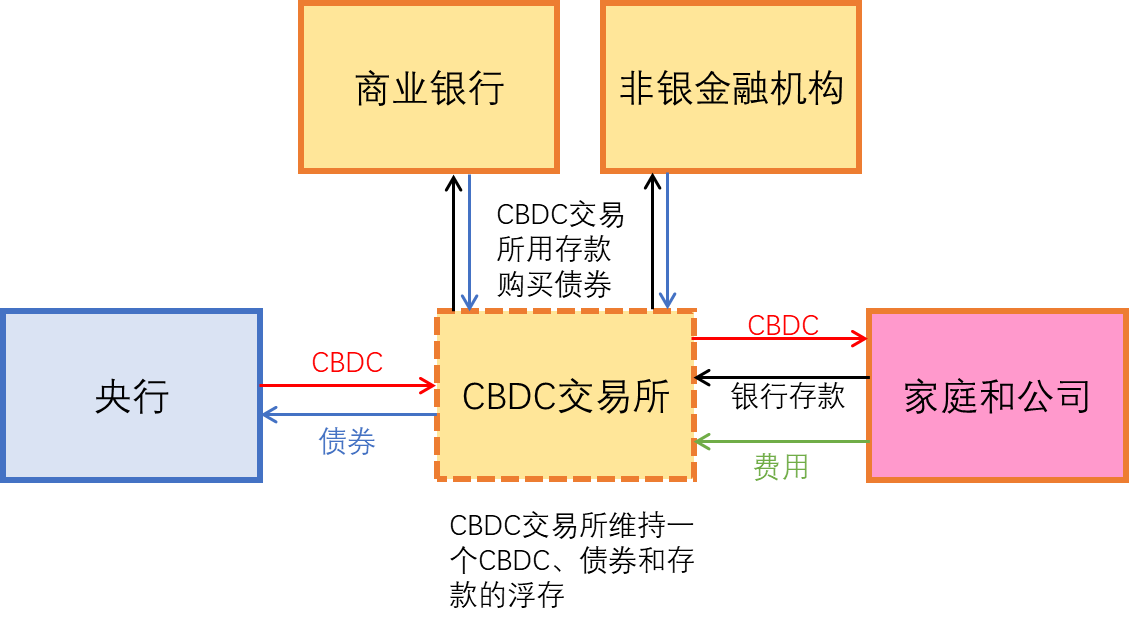

Figure 4: CBDC Exchange Operation Instructions

The CBDC Exchange will charge a fee or spread for the sale/purchase of CBDC services to families and companies. It is also conceivable that banks may choose to subsidize CBDC exchange service fees for their customers, just as banks today subsidize cash distribution costs for their customers. To supplement its holding of CBDC, the CBDC exchange uses the deposits it receives to buy bonds and then uses bonds to obtain CBDC from the central bank. The CBDC exchange has an account with at least one commercial bank in order to receive deposits. The CBDC exchange will periodically rebalance its holdings of bonds, bank deposits and CBDC floats to return to target allocation.

Financial Stability Analysis of CBDC Economic Model

In 2016, Michael Kumhof calibrated the pre-crisis US macro data through DSGE modeling in the paper [15] , and found that CBDC based on 30% of GDP issued by treasury bonds can permanently increase 3% of GDP, in addition to adopting countercyclical CBDC price and quantity rules. As a secondary monetary policy tool, it can significantly enhance the ability of the central bank to stabilize the business cycle. Although there is no in-depth analysis, we can carefully speculate that the introduction of CBDC may stimulate economic activity and may also improve the efficiency of the currency system.

To assess the impact of the CBDC economic model on economic outcomes, we use “total credit” to indicate that borrowers in the non-bank sector (including non-bank financial institutions, households, and companies) receive total funding, which determines the borrower’s investment and trading capacity. Use "total liquidity" to indicate the ability of non-banking sectors to conduct economic transactions. “Total credit” is roughly equal to the sum of “loans” in the balance sheet of the banking sector and “non-loan bank assets” held by the banking sector and non-banking departments. “Total liquidity” is roughly equal to bank deposits held by non-banking departments. The sum of cash and CBDC .

Look at changes in the balance sheet from a departmental perspective. When the non-banking department tries to unload deposits that exceed its demand, they either use the deposit exchange bank to hold non-loan assets (such as securitized assets) or deposit exchange banks to provide non-deposit-type debt (such as commercial bank bonds). . The analysis of the paper [10] shows that in all scenarios, the central bank's balance sheet will expand, in most scenarios, the banking sector's balance sheet will shrink, but total credit and total liquidity will not be directly switched to CBDC by bank deposits. The impact, in fact, may increase, as the introduction of CBDC liquidity may stimulate economic activity. The expansion of the central bank's balance sheet is a predictable result as it gets the asset issuance CBDC. The reason for the shrinking of the banking sector is that the banking sector generally needs to sell assets to the central bank to respond to the growth of demand for non-banking CBDCs, or to sell assets to the non-banking sector in response to a reduction in demand for bank deposits. If the banking sector sells non-deposit bank liabilities to the non-banking sector in response to a reduction in its deposit requirements, the banking sector's balance sheet composition will change but its capacity will remain unchanged.

Although total credit will not be directly affected by bank deposits switching to CBDC, however, bank loan interest rates may result in a change in the equilibrium of credit numbers. Some of these changes may be due to regulation. For example, Basel III requires restrictions on the share of “unstable” bank financing (through the “net stable financing ratio”) and requires minimum liquidity holdings to cover potential outflows of certain types of funds (through “ Flow coverage ratio"). These restrictions, in turn, affect the bank's ability to lend. The switch from bank deposits to CBDC not only exposes banks to the relatively stable loss of retail deposits, but also removes relatively high liquidity bonds. Commercial banks may have to use wholesale financing to replace bank deposits. These conditions may affect the regulatory ratio, which affects the amount or price of credit. The Deputy Governor of the Bank of Mexico recently expressed similar concerns [16] .

Regarding the bank run risk brought about by the introduction of CBDC, the CBDC core principle proposed in the previous article for this risk, and the CBDC economic model is proposed according to these principles, so the risk of bank run has been fully discussed and resolved.

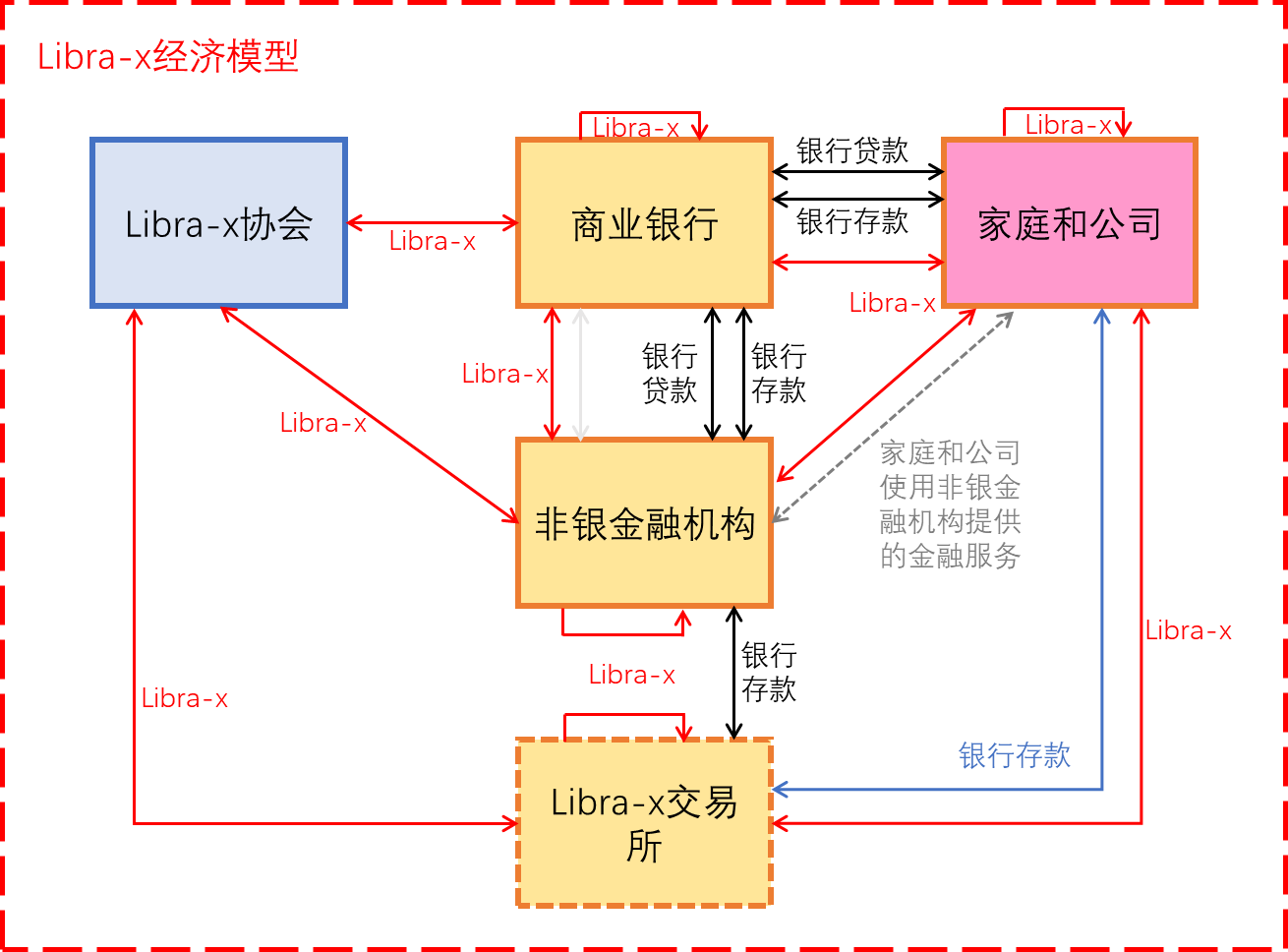

Chapter II Libra-x Economic Model

China's CBDC and Libra-x, except for the issuer's main body, have almost the same function and positioning. In addition, CBDC's design scheme is almost completely decoupled from the existing central bank system. For example, CBDC is different from the central bank reserve, serves a completely different core objective, pays interest rates different from the reserve, and is not freely convertible with the reserve; The CBDC-related policy instruments are independent of existing monetary policy instruments; the CBDC operating structure is independent of the central bank's existing system. Because of the decoupling of CBDC from the existing central bank system, the CBDC design proposed in this paper can be translated to Libra-x almost unchanged, except for some necessary central bank-related modifications. The previous conclusions about the ternary paradox of CBDC monetary policy, the four core principles of CBDC and the impact of CBDC economic model on financial stability can be directly applied to Libra-x, so it will not be detailed here. Therefore, we only list some of the most important conclusions of Libra-x. For details, please refer to the relevant content of CBDC.

Libra-x has the following characteristics:

- Libra-x is a cryptocurrency stable currency issued by the Libra-x Association of the Enterprise Consortium, consistent with the face value of other forms of RMB currency (such as cash and bank deposits) (ie maintaining parity parity);

- Libra-x allows for a wide range of access entities, including commercial banks, non-bank financial institutions, homes and companies;

- Libra-x is a token-based system;

- Libra-x can be interest-bearing, and under reasonable assumptions, can pay interest different from the central bank reserve;

- Libra-x supports cross-border payments;

- Libra-x's distribution mechanism supports a wide range of eligible collateral, including RMB government bonds and sovereign bonds, foreign currency sovereign bonds, and native digital assets, allowing a wider range of entities to participate in Libra-x distribution.

From the ternary paradox of Libra-x monetary policy, we can see that Libra-x design choice can set the currency autonomy of interest rate and the policy goal of maintaining Libra-x and RMB parity relationship, and give up Libra-x and the central bank already have the type currency. Free convertibility of (cash, reserves and bank deposits).

To avoid the introduction of Libra-x to bring systemic risk to the existing banking system, Libra-x's design follows core principles similar to CBDC: (1) Libra-x pays adjustable interest rates; (2) Libra-x is different from central bank Reserves, the two cannot be exchanged; (3) Libra-x associations or commercial banks do not guarantee the exchange of bank deposits to Libra-x; (4) Libra-x Association only issues Libra-x based on eligible collateral.

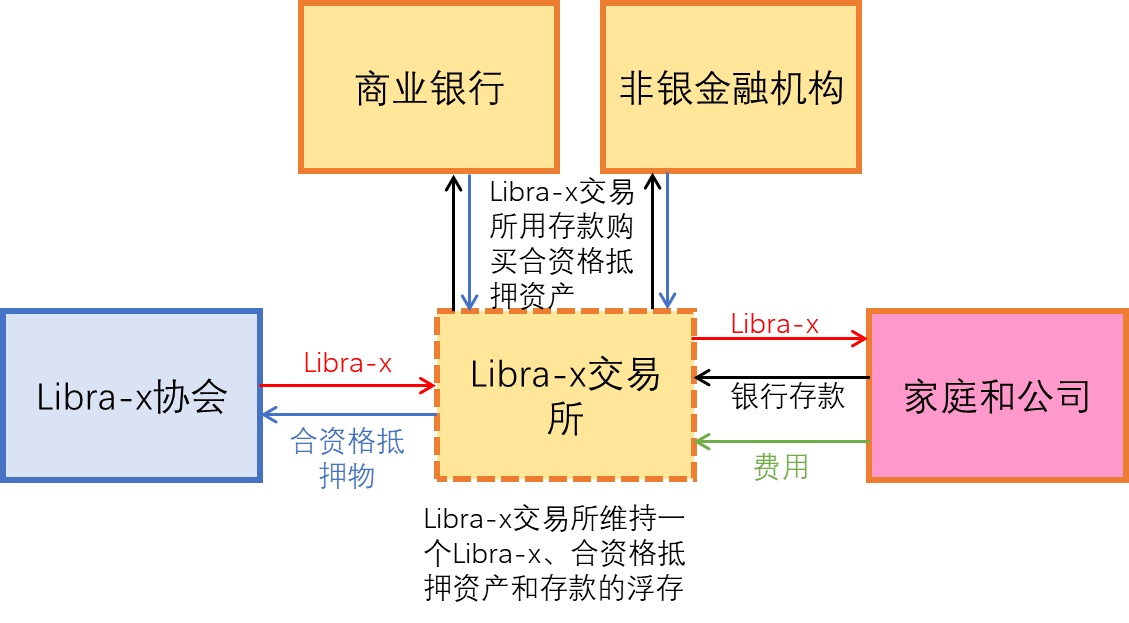

The Libra-x economic model is shown in Figure 5:

Figure 5: Libra-x economic model

All market participants, including banks, non-bank financial institutions, homes and companies, have access to the Libra-x system, so Libra-x is the currency of all agents in the economy. In this model, only banks and non-bank financial institutions can directly trade Libra-x with Libra-x, and families and companies must use Libra-x exchanges to exchange bank deposits for CBDC. Of course, domestic and corporate departments can trade each other. To buy and sell Libra-x. The Libra-x exchange can be a new independent entity or operated by a bank or a non-bank financial institution. For clarity of explanation, this paper assumes that the Libra-x exchange is an independent entity.

The Libra-x exchange performs the following four types of transactions:

- Sell/purchase Libra-x to/from home and company to exchange bank deposits;

- Sell/purchase deposits to/from other private sector counterparties to exchange Libra-x Association eligible collateral;

- Sale/purchase of eligible collateral to/from the Libra-x Association for exchange of Libra-x;

- Invoking a repurchase agreement with the Libra-x Association to borrow/return Libra-x

Figure 6: Libra-x Exchange Operation Instructions

The Libra-x exchange operates as shown in Figure 6, which charges a fee or spread for the sale/purchase of Libra-x services to homes and businesses. It is also conceivable that banks may choose to subsidize Libra-x exchange services for their customers, just as banks today subsidize cash distribution costs for their customers. To supplement its Libra-x, the Libra-x exchange uses the deposits it receives to purchase eligible collateral and then use these assets to obtain Libra-x from the Libra-x Association. The Libra-x exchange has an account with at least one commercial bank in order to receive deposits. The Libra-x exchange periodically rebalances its eligible collateral, bank deposits and Libra-x floats back to the target allocation.

Similarly, the impact of CBDC on financial stability, total credit and total liquidity will not be directly affected by the switch of bank deposits to Libra-x. In fact, it may increase, as the introduction of Libra-x liquidity may stimulate economic activity. In addition, the introduction of Libra-x's bank run risk has been well addressed by Libra-x design.

Although Libra-x has many similarities with CBDC, Libra-x is not dominated by government or central banks, and its distribution leadership and participation are more extensive and diverse. Therefore, the governance structure, coinage tax distribution and business model of the Libra-x system can be very different from CBDC, but these topics are not the focus of this article. Interested readers can continue to follow the author's follow-up articles or project white papers.

references

1.Bech, M and R Garratt (2017): “Central bank cryptocurrencies”, BIS Quarterly Review, September, pp 55–70. ↵

2.BIS Committee on Payments and Market Infrastructures, Markets Committee, Central bank digital currencies ↵

3. Wang Xin, “The State Council has approved the research and development of the central bank's digital currency”, https://www.zilian8.com/163931.html ↵

4.Kimball, M., & Agarwal, R. (2015). Breaking Through the Zero Lower Bound. IMF Working Paper(15/224) ↵

5.Bjerg, O. (2017). Designing New Money: the policy trilemma of central bank digital currency. Copenhagen Business School. ↵

6.Keynes, John M. 1930. A Treatise On Money. London: Macmillan. ↵

7.Mundell, Robert A. 1963. 'Capital Mobility and Stabilization Policy under Fixed and Flexible Exchange Rates'. Canadian Journal of Economics and Political Science/Revue Canadienne de Economiques et Science Politique 29 (04): 475–485.

8. Fleming, J. Marcus. 1962. 'Domestic Financial Policies under Fixed and under Floating Exchange Rates'. IMF Economic Review 9 (3): 369–380. ↵

9.Obstfeld, Maurice, and Alan M. Taylor. 1997. 'The Great Depression as a Watershed: International Capital Mobility over the Long Run'. Working Paper 5960. National Bureau of Economic Research. ———. 2002. 'Globalization and Capital Markets'. Working Paper 8846. Cambridge MA: National Bureau of Economic Research. ↵

10.Kumhof, M., & Noone, C. (2018). Central Bank Digital Currencies design principles and balance sheet implications. Bank of England. ↵

11.Meaning, J, J Barker, E Clayton and B Dyson (2018), 'Broadening narrow money: monetary policy with a central bank digital currency', Bank of England Working Papers, No. 724. ↵

12. Gürtler, K, Nielsen, ST, Rasmussen, K and M Spange (2017), 'Central bank digital currency in Denmark?', Analysis, No. 28, December 2017. Available at: http://www.nationalbanken. Dk/en/publications/Pages/2017/12/Central-bank-digital-currency-in-Denmark.aspx ↵

13.Callesen, P (2017), 'Can banking be sustainable in the future? A perspective from Danmarks Nationalbank', Speech at the Copenhagen Business School 100 years celebration event, Copenhagen, 30 October 2017. Available at: https://www .bis.org/review/r171031c.htm ↵

14. Long Baiyi, CFMI Pass Financial Model and Stabilizing Currency Mechanism, https://www.8btc.com/article/451663 ↵

15.John Barrdear and Michael Kumhof, The macroeconomics of central bank issued digital currencies ↵

16.REMARKS BY JAVIER GUZMÁN CALAFELL, DEPUTY GOVERNOR AT THE BANCO DE MÉXICO, ON “SOME CONSIDERATIONS ON CENTRAL BANK DIGITAL CURRENCIES”. THE OMFIF FOUNDATION–FEDERAL RESERVE BANK OF ST. LOUIS SYMPOSIUM “THE NEXT DECADE OF FINANCE: ASSESSING PRIORITIES AND IMPLICATIONS FOR SOCIETY, POLITICS AND ECONOMICS”. Washington University in St. Louis, Missouri, July 9, 2019 ↵

This article is authorized by the author to launch Babbitt information. Thanks to the following media units for their joint release (in no particular order):

Golden Finance, Chain News, ChainNews, Planet Daily, Carbon Chain Value, Zero Financial, Scallion, Vernacular Blockchain, Shared Finance, Interlink Pulse, Firebird Finance, Gyro Finance, Fire Finance, Pomegranate Finance, Coin Express, Youyou Finance

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- QKL123 Quote Analysis | The bullet has been uploaded, and then the sucker is raised? (0731)

- [Chainge]Technical Salon Roundtable "Frequent Times of Robbery | How to Build a Solid Line of Defense"

- For ten years, the blockchain is still a toy for the technical house, but this is not a bad thing.

- Technical Perspectives | How do ordinary users earn miners in cross-chain?

- Opinion | US Senator: Blockchain may be widely adopted, but it still does not address financial inclusion issues

- Zhou Xiaochuan's latest speech: If piloting digital currency, you should consider 100% cash payment

- From the cathedral to the bazaar, the charm of hackathon and the soul of the developer community