Research Report | Finance must be the most suitable application area for blockchain (Part 1)

Source: Standard Consensus

Overview

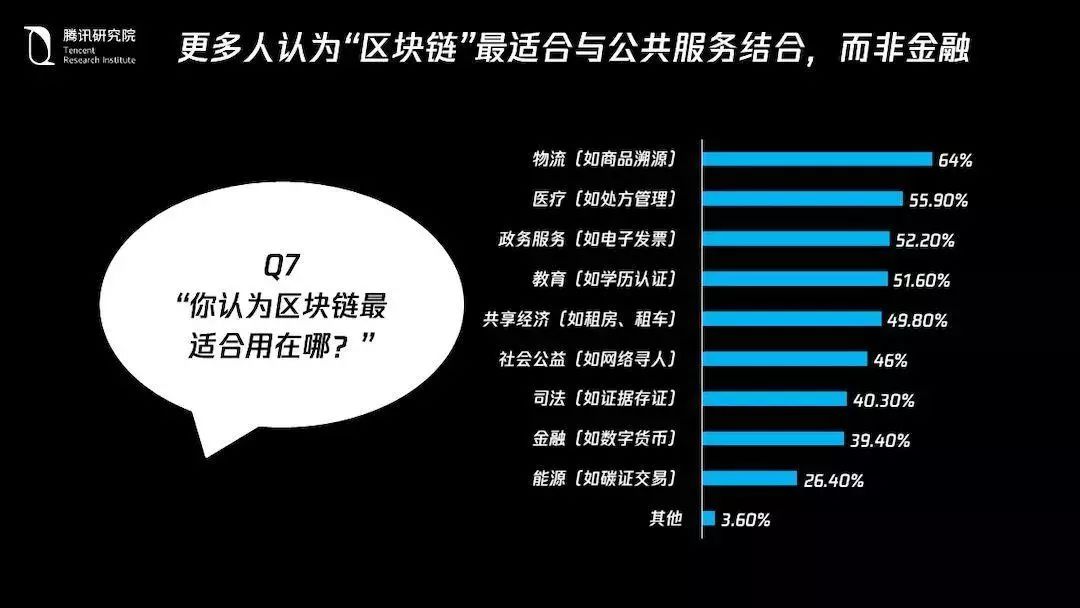

In the "Review of the Industrial Internet 2019 and 2020 Outlook" recently released by Tencent, Tencent Research Institute surveyed 5,567 individuals using WeChat. Only 39.40% believe that blockchain is the most suitable for application in the financial field. And most people think that blockchain is most suitable for application in the logistics industry. Starting from the inter-bank market, this article explains that the market scale that the blockchain can leverage is much larger than the top few applications.

- Blockchain + notarization sets off a wave of landings, another example in Shanghai

- Listed company's blockchain business dynamics: 7 companies disclosed blockchain dynamics, and 5 new entrants

- The big brothers in the currency circle have shrunk the battlefield, and the popularity of traditional venture capital institutions has plummeted. How will the primary market of the blockchain play in the second half?

Report

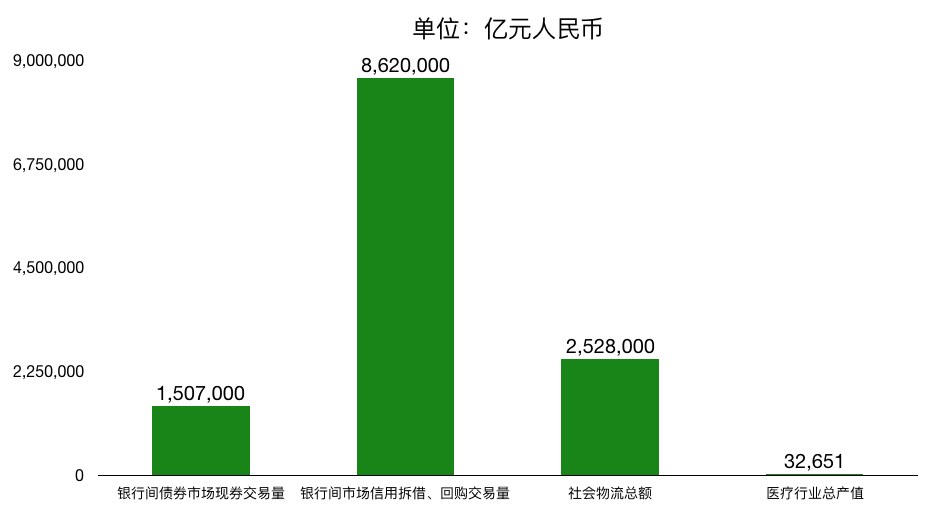

In 2018, the bond market's spot trading volume was 156.7 trillion yuan, a year-on-year increase of 44.6%. Among them, the inter-bank bond market spot trading volume was 150.7 trillion yuan, with an average daily turnover of 602.9 billion yuan, a year-on-year increase of 47.2%.

In the same year, the total transaction volume of interbank lending and repo transactions was 862 trillion yuan, a year-on-year increase of 24%. Among them, the interbank lending totaled 13.93 trillion yuan, a year-on-year increase of 76%; the pledged repo totaled 708.7 trillion yuan, a year-on-year increase of 20.5%; the buy-out type repo totaled 14 trillion yuan, a 50.2% year-on-year decrease.

The interbank RMB interest rate derivatives market has accumulated a total turnover of 21.4 trillion yuan, a year-on-year increase of 48.6%. Among them, the total nominal principal of interest rate swaps was 21.3 trillion yuan, a year-on-year increase of 48.0%

In comparison, the total social logistics in China in 2018 was 252.8 trillion yuan, and the total output value of the medical industry was only 3.2651 trillion yuan. The weight is large and small.

The blockchain can solve the problems in the inter-bank market and the cross-border settlement market, and empower the banking industry from the actual point of view. Serving millions of billions of markets.

Pain points in the interbank market-liquidity

Liquidity is often ranked as one of the three major concerns of banks and regulators.

In 2017, Baoshang Bank's two-year fixed deposit has a deposit interest rate of 6.68%. The risk of liquidating high interest rates on reserves may be punished by regulatory pressures.

In order to enhance the flexibility of liquidity operations and payment and settlement networks, although participants in the financial industry have invested heavily in their liquidity monitoring and computing capabilities, the results have not been satisfactory. In addition, in the context of stricter regulations, the industry trend is moving towards the establishment of faster processing and more automated payment and settlement infrastructure.

The CBRC promulgated the “Measures for the Management of Liquidity Risks of Commercial Banks” on May 25, 2018, which will be implemented as of July 1. The head of the relevant departments of the China Banking Regulatory Commission said that in recent years, new features have emerged in China's banking business, and the current liquidity measures (trial) include only two regulatory indicators: liquidity ratio and liquidity coverage ratio. Among them, the liquidity coverage rate is only applicable to banks with assets of more than 200 billion yuan (inclusive), and small and medium-sized banks with assets less than 200 billion yuan lack effective regulatory indicators. The main content of this revision is the introduction of three new quantitative indicators. Among them, the ratio of net stable funds is applicable to commercial banks with an asset size of 200 billion yuan or more, the adequacy ratio of high-quality liquid assets applies to commercial banks with an asset size of less than 200 billion yuan, and the liquidity matching ratio applies to all commercial banks.

One potential way to achieve this is through liquidity management through interbank trading markets. However, this will be difficult to achieve using traditional infrastructure. With the help of blockchain technology, it will be easier to integrate the interbank market.

Source of liquidity

The evolution of the payment and settlement system has occurred over five major phases over time, with the focus on:

1. Risk control through the introduction of RTGS (Note 2) for high-value payment and delivery payment (DVP Note 1) systems.

2. Liquidity costs associated with RTGS and DVP systems. These costs are further mitigated by algorithms and by bilateral and multilateral netting arrangements (such as CHIPS in the United States and TARGET2 in the European Union). The recent push for central counterparty clearing (CCP Note 3) and the introduction of CLS (Note 4) Risk, while enabling the company to use its liquidity more effectively through margin and netting capabilities.

3. Timeliness of payment requires CLS payment or change margin settlement in one day to facilitate ongoing payment, clearing and settlement activities. This feature is systemically important because it enables intra-day settlements on a system-wide basis, thereby further reducing the settlement risk for system participants.

4. Throughput requirements. These requirements ensure that sufficient payments are made throughout the day so that the system can continue to operate even during periods of market turmoil or distress. These requirements are another important step in the resilience of the system. These requirements ensure that member banks have paid at least a certain percentage of daily payments before a certain deadline.

5. Speed and efficiency, this is the latest step to enhance the payment environment by introducing new RTGS.

These five stages tell us that the payment and clearing environment has changed dramatically and will continue to develop and affect banks' balance sheet use, operating costs and liquidity buffer costs.

Note 1 : The results of the silver transaction are synchronized in real time, final and irrevocable. The purpose of establishing the DVP system is to reduce the credit risk of counterparties, and to eliminate the principal risk of the securities that have been delivered by the seller but have not received the corresponding amount, or the principal risk of the securities that have been delivered by the buyer without receiving the funds. That is, the core connotation of DVP is that securities and funds are settled at the same time, so as to prevent the default risk of settlement counterparties.

Note 2 : RTGS: Real Time Gross Settlement is a cross-bank electronic transfer system established in accordance with international standards. It specializes in processing cross-bank transfers initiated by the payer's bank.

Note 3 : In derivative transactions, the central counterparty clearing house replaces bilateral clearing and becomes the buyer of each seller. The seller of each buyer can also ensure the completion of the transaction if one of the counterparties defaults.

Note 4 : CLS is a professional US financial institution that provides settlement services for members of the foreign exchange market.

Industry Trends

Structural changes are taking place in global financial markets, which will continue to affect the management of liquidity. Here are four major changes.

First, in terms of macroeconomics, low and slowly rising global interest rates, coupled with liquidity and capital regulation, have led banks to hold too much cash and collateral in central banks.

Secondly, as customers, especially indirect liquidators, are working to increase transparency and control their day-to-day use of net cash, banks' old infrastructure is under tremendous pressure.

Third, financial market infrastructure is meeting the needs of customers, regulators and investors for greater transparency and efficiency. Despite being in a new global stage, the UK-led rapid get rich scheme is an example of the development of market infrastructure towards increasing the speed and transparency of banking flows. With Quick Payments, payment times between customer accounts are reduced from three business days to real-time transfers.

Finally, new market entrants and technologies such as blockchains record current data by creating digital ledgers that update in real time to support instant payments and settlement. The cryptocurrency market has sparked debate around the benefits of distributed governance, decentralized organization, and democratic standards, which challenge today's market infrastructure.

These new, evolving and potentially opposite market trends continue to put pressure on bank finance executives to explore the effectiveness of intraday liquidity financing models. We believe that by using the blockchain to establish a transparent financial market for overnight lending, it is possible to create more sources of liquidity.

Our goal is whether the blockchain can be used as a startup technology for intra-day liquidity in financial markets. Enterprise blockchains allow untrusted entities to enter and reach agreements with each other directly on shared facts. These shared facts can represent cash, assets, and contracts in a wide range of industries.

In a payment or capital market environment, blockchain can facilitate immediate settlement and reconciliation on the ledger-a network of directly interacting nodes can simplify the interaction of counterparties. For example, depending on the implementation, when the market infrastructure introduces other adverse consequences, the blockchain can reduce the amount of dependence on a centrally controlled or operated market infrastructure.

Compared with the existing decentralized financial market infrastructure, certain blockchain platforms have greater design flexibility. Assets on the ledger may eventually free many payments and capital markets from these rigid, isolated, and complex infrastructure constraints, enabling new types of transactions.

Automated processes on the blockchain network can also enable new types of interactions. For example, pre-agreed rules can be programmed to automatically execute on a network-wide basis without requiring a single activist to maintain and ignore these rules. These self-executing contracts may involve atomic transactions, such as delivery and payment or settlement functions for payments.

The intra-day liquidity of blockchain technology needs to find a truly pragmatic balance for the industry. In many enterprise environments, complete decentralization at each level is impossible and undesirable. In some cases, the industry needs a pragmatic structure that strikes the right balance between avoiding reliance on central entities and ensuring that each entity has sufficient decision-making power, autonomy and accountability.

Bank's existing liquidity management model

The key factors driving intraday liquidity demand are:

- Financial market infrastructure system participation: The direct participants and liquidators of the financial market infrastructure (FMU) system and real-time total settlement (RTGS) system have different intraday liquidity needs from indirect clearing institutions.

- Products and transactions: Products (such as fixed income, loan products, structured), transaction types (cash payments), transaction volume and size drive the bank's liquidity needs.

In most countries, the central bank provides a method of settling small payments in cash and a method of settling large payments electronically (usually interbank payments). For this reason, the central bank usually adopts a system through which banks can settle central bank payments. Inter-bank payments are settled through the net settlement system, but as the volume and value increase, central banks begin to worry about the risks inherent in deferred net settlement systems, so most central banks choose to implement a real-time gross settlement (RTGS) system. With RTGS, payments will be processed immediately and finalized within operating hours. The central bank eliminated settlement risks at the cost of rising liquidity needs of participants.

RTGS system of each country

Liquidity requirements in RTGS systems can be huge. Fedwire Funds is a large payment system in the United States. In 2016, it paid approximately 590,209 payments per day, with a total value of nearly $ 3 trillion.

HVPS is China's large-value payment system. In 2014 alone, its total transaction volume exceeded 200 billion yuan.

CHAPS is the UK's large-value payment system, with an average daily transaction volume of approximately 165,285 in 2017, valued at nearly 334 billion pounds.

Target2 (the European Union ’s large payment system) has an average daily transaction volume of 342,008, with daily transaction volume of up to 1.7 trillion euros in 2016. In most countries, the amount paid every 5 to 6 working days is equivalent to annual GDP.

Liquidity savings mechanism

For the past 20 years or so, central banks around the world have implemented liquidity savings mechanisms (LSMs) in their large payment systems to reduce the liquidity requirements of these systems. LSM works by encouraging greater liquidity reuse or allowing banks to liquidate net debt on the day. Liquidity recovery stems from the fact that banks can use the incoming liquidity to make payments, and often, if the bank pays in time, it will recover more liquidity. Policies that encourage timely payment processing (such as throughput guidelines) or penalize delayers (such as tariffs that change over time) make liquidity more likely to be recovered, thereby reducing the overall liquidity requirement of the system.

However, the most effective LSM is an LSM that saves liquidity needs by matching offset payments that have been submitted to a central queue and using only the liquidity required to meet net debt to settle those payments. Suppose bank A needs to pay bank B a value of 100, and bank B needs to pay bank A a value of 80. Then, if these two payments are entered, the amount that needs to be liquidated into the queue using the offset algorithm will be the value of Bank A's net debt to Bank B of 20. In contrast, in a pure RTGS system without LSM, the liquidity requirement to settle these two payments is 100. Larger gains can be achieved by netting payments between two or more banks on a multilateral basis.

However, most wholesale payments cannot be delayed all day. Typical payment requests that banks receive from customers need to be processed on the same day, but banks usually have some flexibility in when they execute these requests during the day. It is estimated that 4% of payments are urgent payments, which means that the bank must process these payments immediately or it will have significant consequences for customers. But this 96% payment is more flexible. Many economists have suggested that delayed payments can cause some customers to be dissatisfied. Therefore, banks need to make a trade-off between saving liquidity due to delayed payments, increasing net settlement opportunities, and saving liquidity against delayed costs.

The net settlement algorithm run by the central bank runs a centralized queue, which is usually cleared at predetermined intervals. This is a difficult task, and the central bank must try to solve it with imperfect information. The central bank does not know what payment obligations each bank has outside the RTGS system, or whether it has chosen to enter it into a queue. In addition, if the centralized system only considers complete offset payments, the chances of making money will be very limited. The liquidity available in the cohort is a participant's choice variable, which in turn is what the central bank may have to estimate when designing its system.

Even with known liquidity and payment methods, the problem of finding the best netting solution can be complex. If there are n payments in the payment file, the number of net combinations to consider is 2n-1.

Another problem is that centralized netting algorithms try to maximize the value or amount of settleable payments, but they often fail to weight the importance of payments or assess the cost of liquidity, which can occur throughout the bank and throughout the day. The difference. There is an incomplete information problem that prevents central operators from maximizing the social welfare of the system. Finally, centralized queues run within a given authority or banking system. Payments can be networked across systems, but this involves providing liquidity to another centralized system, such as CLS payments.

Conclusion

This article is divided into two parts: the first part discussed the market size, the pain point of the industry and the bank's existing liquidity management model in the financial sector (especially banks), the next part will continue to proceed from the liquidity management model, Explore how blockchain solutions can improve banks' liquidity management in the day.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Shanghai Blockchain Industry and Park Development Report: Yangpu District established the first 5 billion-scale blockchain industry guidance fund, which has a good foundation for industrial development

- Zhu Jiaming's New Work: Recognizing Future Currency Needs New Thought Resources

- KPMG report: China's fintech will enter the 2.0 era, and blockchain has been widely used in various fields of financial services

- Overview of the crypto asset industry in 2019: the rotation of the cycle and the dawn of dawn

- What would Soros do if he wanted to destroy Bitcoin?

- These 7 directions are expected to become "new air outlets"! “ Sichuan Province Blockchain Industry White Paper (2019) '' released

- Higashino Keigo and Zhang Xinzhe all "boarded"! Concert ticket data on the chain