Viewpoint | On the safety budget of Bitcoin

This article aims to explore the ability of Bitcoin to withstand 51% of attacks (ie, Bitcoin's "safe budget"). The fierce competition between miners makes it impossible for the system to collect transaction fees from a network sufficient to maintain a secure budget, so we should get transaction fees from all payment markets.

This article is a continuation of the “Two Types of Block Space Requirements” and “Building on Bitcoin” speeches, and the analytical position is more empirical than the old one.

1. What is a "safety budget"?

Bitcoin’s “safety budget” refers to the amount of money we pay to miners each year (in other words, the money spent on mining every year, which is no different) (Translator's Note: The two are not equal in accounting, but in economics Both have the same meaning). When the security budget is not high, a 51% attack can be initiated at a very low cost. Bitcoin's 2018 security budget is about $7 million a day. It is inferred that the one-year cost of the Bitcoin system (the never-ending 51% attack arms race) will not exceed $2.6 billion.

In 2017, the US military's defense budget was about $590 billion, and the Fed's annual operating expenses reached $5.7 billion. In comparison, the 2.6 billion security budget is still too small.

- 70% is inaccurate, the researchers said that the actual market share of Bitcoin has exceeded 90%

- Bitcoin node distribution at a glance: the largest in the United States, the fifth in China

- Countdown to two days | Harmony will attend the 2019 than the original global developer conference to discuss the current challenges and trends of the public chain

2. Block reward

Fortunately, we can hope that the value of the block reward will bring us higher security. Although regardless of the price of the currency of the bitcoin, the block reward is always halved every four years (equivalent to a year-on-year decrease of 0.84), but as long as the annual appreciation of bitcoin exceeds 19%, it is enough to offset the output. The impact of the block rewards caused by halving. From a historical perspective, Bitcoin's average annual appreciation is much higher than 19% (up to 70%), so it is certain that Bitcoin's security budget can grow over time.

Of course, the price of Bitcoin will stop growing one day. Although Bitcoin has been designed to be quite successful, it is likely to eventually stagnate at the annual value growth of 1.077 [1], which is the nominal value growth rate of all currencies in the world today.

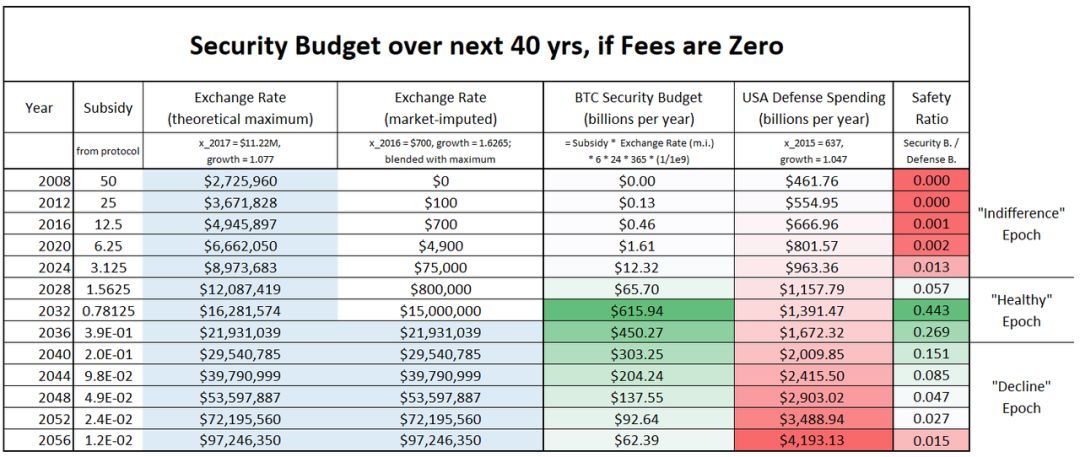

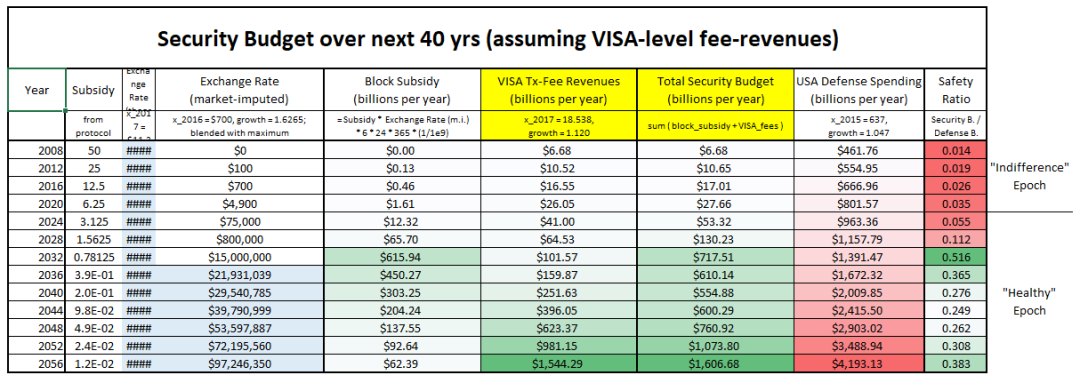

The table below shows the growth trend of the security budget and the decline after the final turning point:

The above table depicts the trends in the Bitcoin security budget, with rows representing different years. The theoretical maximum exchange rate cap is taken from the paper by Game and Watch. The estimated market exchange rates in the table are calculated from historical data and growth factors, while some additional processing is done to reach the theoretical upper limit more quickly. The US defense budget is estimated by Wikipedia data. “Safety ratio” means that the proportion of the defense budget can be successfully destroyed. All of the above data is expressed in the US dollar.

"Indifference period" means that bitcoin is fragile, but only a handful of attackers are willing to attack, and most of the forces do not care about the new thing of Bitcoin. “Healthy Period” means that Bitcoin after its growth and development has the ability to withstand malicious attacks from oversized consortia. The final “death period” refers to a bleak ending, and Bitcoin will eventually be easily attacked by a 51% attack.

3. Transaction fee

I. The ideal "transaction fee pressure"

As everyone knows, the transaction fee is designed to solve this problem. As highlighted by Greg Maxwell:

Trading fee pressure is part of the system's intentional design and is currently the best solution for the long-term survival of the Bitcoin system.

He later proposed a famous point:

From my personal point of view, I do believe that market activities can be safe without giving inflation and providing sufficient fees.

This view (the need for “transaction fee pressure”) is very common. Roger Ver has cited similar views from other Bitcoin researchers, although the purpose is to discriminate against dissidents, but the views quoted are still very accurate.

II. Duality

Since the advent of Bitcoin, its duality (as an attribute of currency units and as a means of payment) has been confusing to many people.

Often, monetary scientists and economists ignore the bitcoin's means of payment (the blame of bitcoin has no "intrinsic value"). Merchants and bankers tend to ignore the currency unit attributes of Bitcoin (thinking that buying Bitcoin is an innocent investment), and then harvesting the value of the “blockchain” concept with a mindfulness.

The duality of Bitcoin is also reflected in the current “expansion debate”. It is more important that the discussion focuses on whether the “transaction medium” is important or the “value storage” usage scenario.

At the same time, I believe that in the long-term security budget analysis, the dilemma of bitcoin duality still exists. Consider the following table:

III. Is it really “paying the transaction fee with Bitcoin”? Although block rewards and transaction fees are both “safe budgets”, the two can be said to be two things that are irrelevant . The difference between block rewards and transaction fees is like the difference between “2017 VISA total profit” and “2017 M2 total growth”. VISA's profit reflects the value of VISA's superior service to its competitors (MasterCard, Automated Clearing House, Western Union, etc.), while M2's changes are quite different, reflecting the elections Other factors, such as results, public comments, business cycles, federal policies, and so on. It may not be possible to compare M2 with the Japanese yen, but it would be too exaggerating to compare it with MasterCard.

The transaction fee is denominated in Bitcoin as a unit. But the difference with block rewards is that the amount of fees will change as the exchange rate of Bitcoin fluctuates. As the bitcoin exchange rate rises, the current Cong/Byte transaction pricing will become too high, and users will not be willing to pay transaction fees at this price (and then reduce the nominal price of Cong/Byte).

So the transaction fee is not really "priced in bitcoin", although the Bitcoin protocol has been trying to mislead users to pay transaction fees according to this logic, but the market behavior has not developed. The transaction fee is actually priced according to purchasing power. The current (the booming period before the arrival of bitcoin) can be said to be reflected in the US dollar.

So for example, “In December 2017, Bitcoin’s transaction fee was equivalent to $28” is no problem. On the contrary, if Bitcoin's transaction fee is "up to .0015,0000 BTC", it is the real pricing rule that does not understand the current transaction fee. Because if the price of Bitcoin appreciates by a factor of 10 [2], the transaction fee will drop to 0.0001,5000 BTC.

IV. Incentive products

Whenever the price of a commodity rises, entrepreneurs will find ways to increase production. (The holder will always try to trade, but this piece is temporarily outside the scope of this article)

It is well known that the maximum number of Bitcoins is set at 21 million. At present, the production rate of Bitcoin (ie) is 12.5 bitcoins per block, and this rate will continue until the next production is halved.

In addition to Bitcoin, another item "Bytes in Bitcoin Blocks" is also set to the upper limit. Initially the block size was limited to 1MB, which was later widely discussed, and is now set to approximately 2.3 MB per block.

As mentioned earlier: As long as the block becomes more valuable, entrepreneurs will find ways to produce more blocks.

One way is to restart old, old mining machines with smaller marginal rents. With the addition of computing power, the production rate of the block can be temporarily accelerated. Of course, as the new difficulty cycle adjusts, the block's output rate will return to normal (one block per 10 minutes). As another way out, entrepreneurs will dig up the altcoin.

V. Altcoin as a substitute

The cottage "coin" is a poor substitute for the bit "coin". Every form of currency is inevitably in competition with other currencies: money has a strong network effect; identifiable attributes have a super-linear effect on the spread of money; The token conversion will be very inconvenient. So what people really need is bitcoin, everyone wants to throw other coins into the ruins of history!

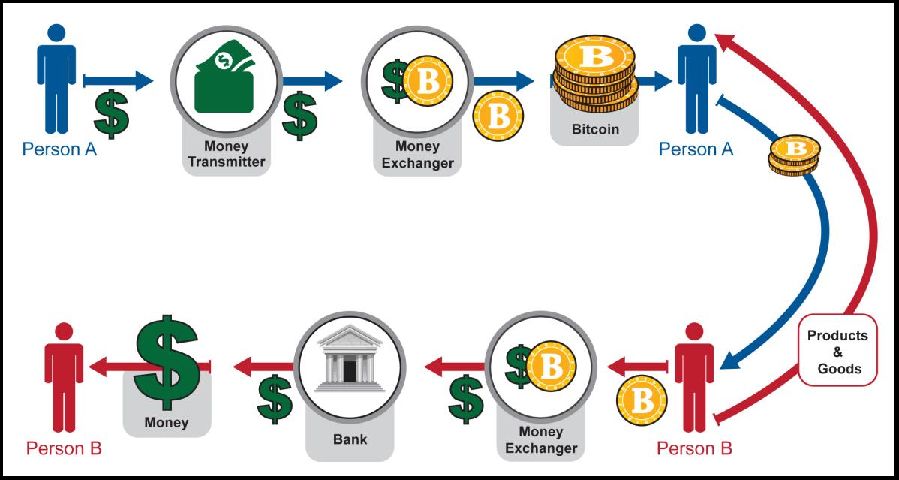

However, if you consider the transaction price and the high price of the "bytes in the Bitcoin block", there will be a subtle turn: the block space of the altcoin can be regarded as a good substitute for the bitcoin block space. However, such demand does not affect people's continued pursuit of bitcoin, and only a small number of users are willing to use bitcoin as a means of payment when buying things. This picture from the 2013 FINCEN Congress question may explain this:

The currency sent by blockchain payment can always be adjusted. People may send LTC worth “$20”; they may also send dog coins worth “1 BTC”; or EOS worth “one sandwich”. With the help of “exchanges” (eg Coinbase, ShapeShift, SideShift, BitPay, LocalBitcoins, multi-currency wallets, CC ATMs, etc.), people can easily pay with different forms of currency.

Further, even those hard-core bitcoin fundamentalists occasionally recognize this (real) assumption [3], that is, the payment method of the altcoin is a substitute for the bitcoin payment method. At the end of 2017, when transaction fees soared, many people talked about this:

-

Samson Mao -

Francis Pouliot -

"Digital currency as a means of payment"

VI. Demand for competitive payment methods

At present, the “transaction fee pressure” that should have played a central role has been a small gap.

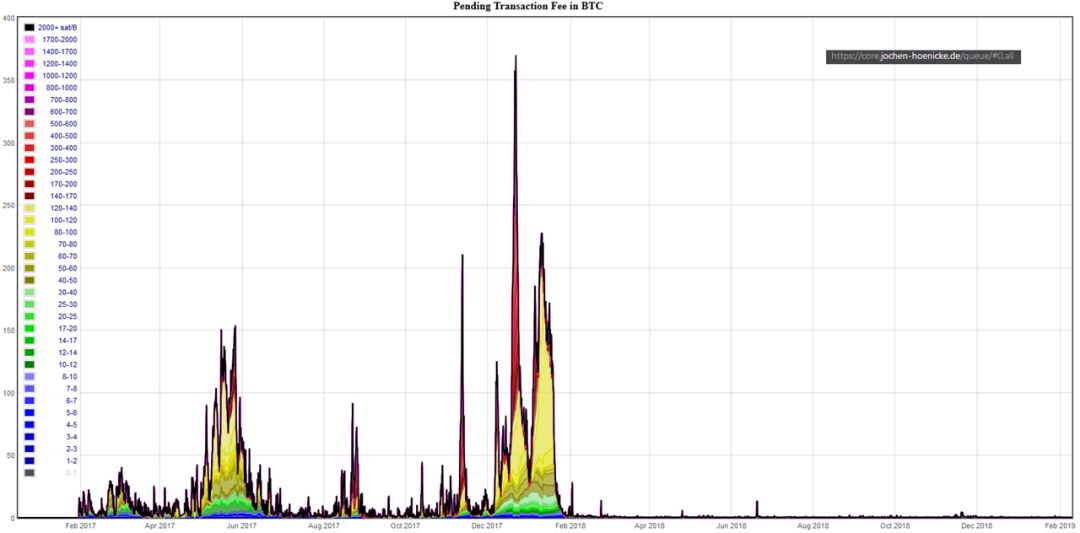

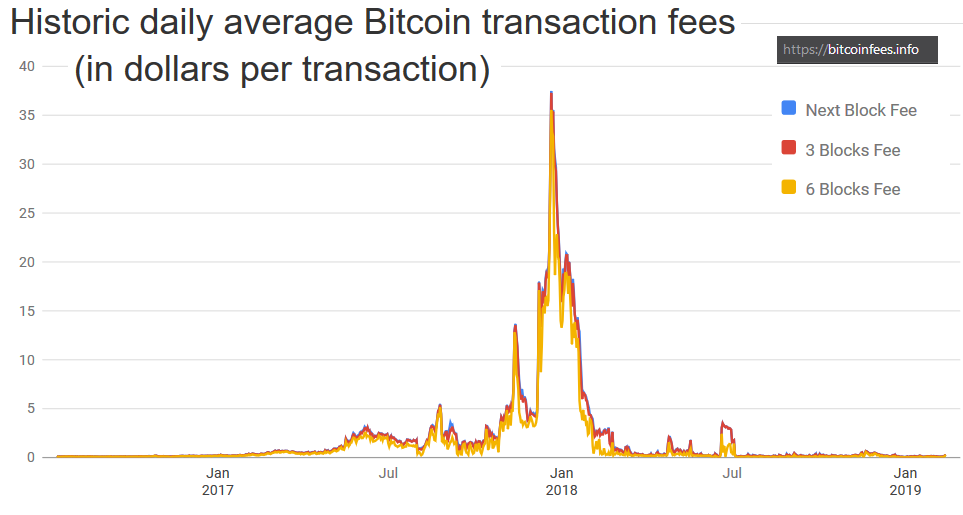

The chart below is a transaction fee priced in Bitcoin (pictured from this page):

This chart is a dollar-denominated transaction fee (pictured from this page):

It can be seen that the role of transaction fee pressure is seventy-eight. A typical bitcoin transaction currently costs about 30 to 40 cents – much cheaper than VISA trading.

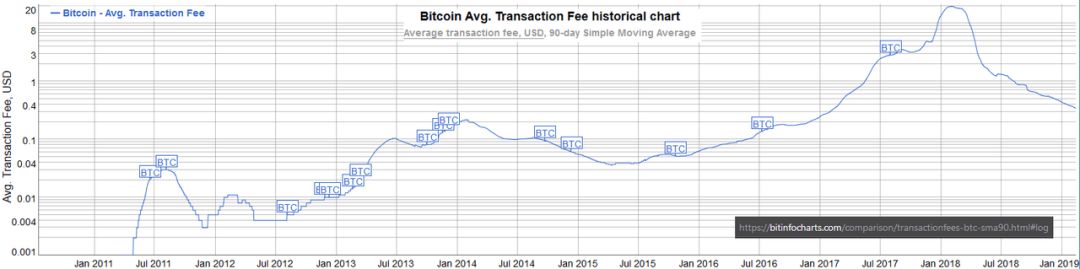

Compare historical data and find moving averages over a 90-day period…

We can see that Bitcoin crossed the “1 US dollar transaction fee red line” in May 2017, which is consistent with the rise of the altcoin. It is also possible to see the rapid disappearance of “transaction fee pressure” at the end of 2017, and then appear small. In the end, it can be seen that this release of pressure is consistent with a sharp drop in trading volume in the Bitcoin network (an unprecedented decline).

For me, the above data proves that the theory that users are willing to pay high bitcoin transaction fees is wrong. In fact, they just reluctantly paid high transaction fees, and only limited to a short bubble period (people are afraid to step empty).

If the theory that people pay high Bitcoin transaction fees is falsified, then according to the US dollar, the future transaction fee will not be higher than today's transaction fee.

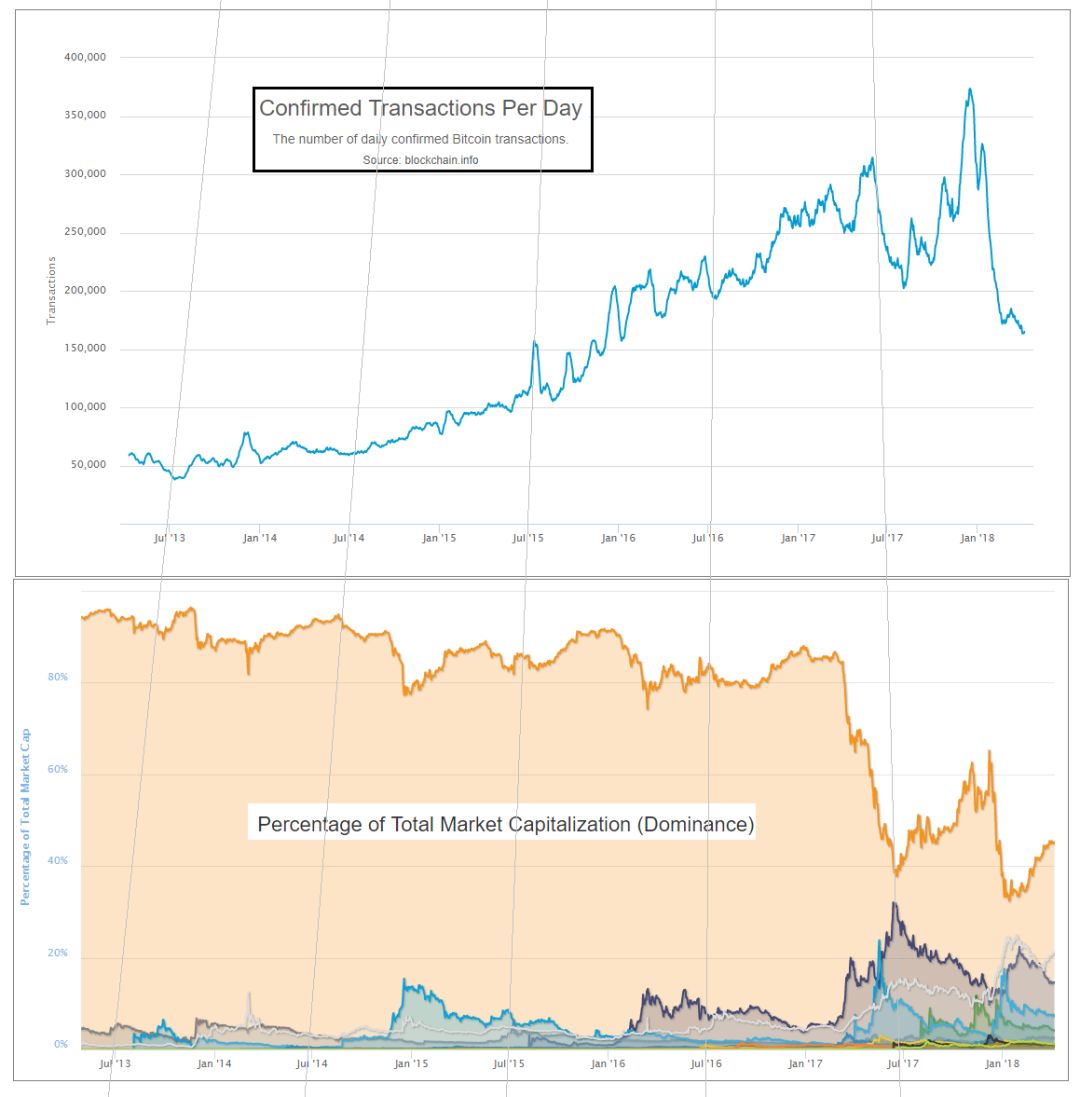

According to blockchain.info, the total transaction fee for the past 12 months is $70 million. (12 months ago this figure was $770 million)

Looking back at the chart above, the total transaction cost is negligible. After all, the transaction fee of 70 million US dollars is only 0.07 according to the unit (1 billion) in the above chart.

If the user is sensitive to the price of the transaction fee and is only willing to pay the lowest possible transaction fee, how can we increase the total transaction fee?

VII. Source of remaining transaction fees

a. Lightning Network

Lightning Network (if successful) can put many "real-world transactions" into two-chain trading.

The direct impact of this outcome is to reduce transaction costs on the chain, but in the long run it can increase the total transaction fee. The Lightning Network makes every user willing to pay more for the transaction fee by increasing the utility of each transaction on the chain (one chain transaction completes multiple transactions).

Any point of view at the moment is just speculation. I think the lightning network could not raise the total transaction fee to more than two orders of magnitude.

First, there is still a need to create chain transactions and periodically maintain lightning networks. Therefore, lightning network users who still need to pay the transaction fee on the chain will still try to reduce this expenditure. At the same time, the altcoin can completely establish its own lightning network (there is no difference between copying the lightning network and copying the code anyway). The competition between such lightning networks and the competition between different blockchains are actually the same.

It should be noted here that, by definition, the transaction fee paid to the lightning network relay node [4] is not paid to the miners. Therefore, there is no such thing as the multi-lightning network transaction fee envisaged to "aggregate" into a large chain transaction fee (because it is not economically viable).

Second, the user experience of the lightning network is always worse than the experience of the users on the chain. The lightning network needs to interact, that is, each user must be online and perform operations such as [signed transaction] to receive the payment. This also means that users in the lightning network may cause inconvenience (such as they do not reply or the computer is really on fire), and even directly disrupt the normal use of the user. Although the clever design of Lightning Network minimizes the risk of introduction, it ultimately affects the user experience. Naturally, troublesome users can easily switch from lightning network transactions on the main chain to using chain transactions on the altcoin.

b. Combined side chain mining

Combining the side chains of the mining can accomplish all the functions of the altcoin, but there is no need to purchase new tokens. Therefore, the exchange rate risk under this scheme is extremely low and can provide a good user experience.

In addition, the combined sidechain mining will send all the transaction fees received to the Bitcoin miners. With the combined blind digging technique, this process eliminates the need for users or miners to run additional sidechain node software.

A set of sidechains consisting of large blocks can handle a large number of transactions. In the next section, I will assume that a sidechain network completely replaces VISA (VISA only) and thus earns all VISA transaction fees. VISA is only a small part of the entire payment market (including checks, Western Union payments, Apple payments, etc.), but it can already explain the problem.

VIII. VISA transaction fee income

I thought that VISA mainly used the interest paid by users as the main income, but by consulting relevant information, the fact is not taken for granted.

The 40th page of their recent annual report shows:

Therefore, the main profit of VISA is still derived from transaction fees. In this way, the following comparison is logical.

VISA's total profit increased from $11,778 million in 2013 to $18,838 million in 2017. The growth rate is about 12% per year.

Assuming that this momentum grows, you can get the following picture:

The above table is the “Safety Budget Table” above. A new column has been added: VISA transaction fee. These transaction fees plus the basic block rewards are the final new security budget.

Such a security budget is safer in the long run and in the overall situation.

in conclusion

Resisting 51% of attacks requires Bitcoin to have a high "safe budget." Today's transaction fee income is far from enough. We must ensure that the total transaction fee in the future can be raised enough to pay the “safety budget”.

Although raising prices (such as increasing Cong/byte trading rates) can increase revenue to a certain extent, it is unfortunate that due to competition among many chains, blindly raising the transaction rate will only be countered by the market, which is counterproductive.

A better way is to swallow the entire payment market and put all the transaction fees into the bag. With the combined side chain mining, this goal can be achieved without compromising decentralization.

footnote

[1]. This data is calculated by 1.077 = (25.94/5.85)^(1/20). It can be seen that 1.077 is lower than the required "stagnation speed" of 1.19.

[2]. I mean that if the “bubble” at the end of 2017, the price of USD/BTC will skyrocket by more than 10 times. In other words, if Bitcoin was only $9,000 in January 2017, it went up directly to $190,000.

[3]. I clearly remember that there are many examples, but (before I give up) I only found the following. If you find or remember other examples, please be sure to send me a message. If there is no more illustration, I will eventually delete this paragraph.

[4]. “Transaction fee paid to the lightning network transponder”, here refers to the cost paid by the user (under the chain) to the lightning network node that maintains the lightning network payment route. (Finish)

(A lot of hyperlinks are provided in the article, please click to read the original text to get the EthFans website)

Original link:

Http://www.truthcoin.info/blog/security-budget/

Author: Paul Sztorc

Translation & Proofreading: Anzai Clint & Ajian

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- "Federal" design is a major focus, and Bystack first disclosed the OFMF specification.

- Global blockchain investment report for 2019: 75% of blockchain investment goes to early stage companies

- Twitter Featured | V God: I am more and more pessimistic about the second-tier solution under the chain

- Bitcoin vs Gold: Is Bitcoin really a new “safe haven” asset?

- The low price of Monroe, why squeeze out BTC to become the "dark net coin king"

- US SEC approved digital securities platform Securitize registered as a transfer agency

- Bitcoin.com Twitter picks up all BCH supporters, comment: Mysterious power appears