Zou Chuanwei: Economics and regulatory issues in blockchain

This article is based on the “Golden Classroom” lecture of the Shanghai Institute of Advanced Finance, Shanghai Jiaotong University on July 16, 2019. It does not represent the position of the author's institution.

Author: Zou Zhuanwei universal block chain & PlatON cloud chief economist, has studied at Peking University, Tsinghua University and Harvard University, has a long career in the Central Huijin Investment Corporation and China Nanhu financial services company, added universal block In front of the chain is the chief economist of Bitland. Dr. Zou Chuanwei's research areas include commercial banks, fixed income securities, financial investments, risk management, internet finance/financial technology and financial regulation. Representative research in the blockchain includes "bubbles and opportunities – digital cryptocurrencies and districts. Nine Economic Issues in Blockchain Finance and What Can the Blockchain Do and Can't Do (People's Bank Working Paper No. 4, 2018). Dr. Zou Chuanwei won the first "Sun Yefang Financial Innovation Award" and the 5th China Soft Science Award (Frontier Exploration Award)

Thanks to Gao Jin for inviting me to do this sharing, and thank you for taking the time to participate. The content shared today comes from three papers: "Foam and Opportunity – Nine Economic Issues in Digital Cryptographic and Blockchain Finance" (Financial Accounting, 2018, 3), What can the blockchain do? What can't be done" (in collaboration with Researcher Xu Zhong, Financial Research, 2018, 11) and "Blockchain and Financial Infrastructure – Also on Libra's Risk and Regulation" (Financial Regulation Research, 2019, 7) . I mainly share five aspects: one is the Token paradigm of the blockchain, the second is the blockchain application classification, the third is the blockchain and financial infrastructure, the fourth is the risk and supervision of Libra, and the fifth is the regulatory issue of the blockchain. .

It should be noted that Token has multiple Chinese translations in different contexts, such as cryptocurrency, encrypted assets, tokens and certificates. To avoid confusion or ambiguity, this article mainly uses Token instead of its Chinese translation. Token does not refer to any specific cryptocurrency unless otherwise stated.

- Coindesk Senior Analyst: The dollar is coming to an end, bitcoin or become one of the global reserve currencies?

- New Iranian law: the government does not recognize cryptocurrency-related transactions, but allows for conditional mining

- There is no doubt about Bitcoin's safe-haven properties. Will there be spring in the altcoin?

First, the block model of the Token paradigm

1. Token paradigm summary

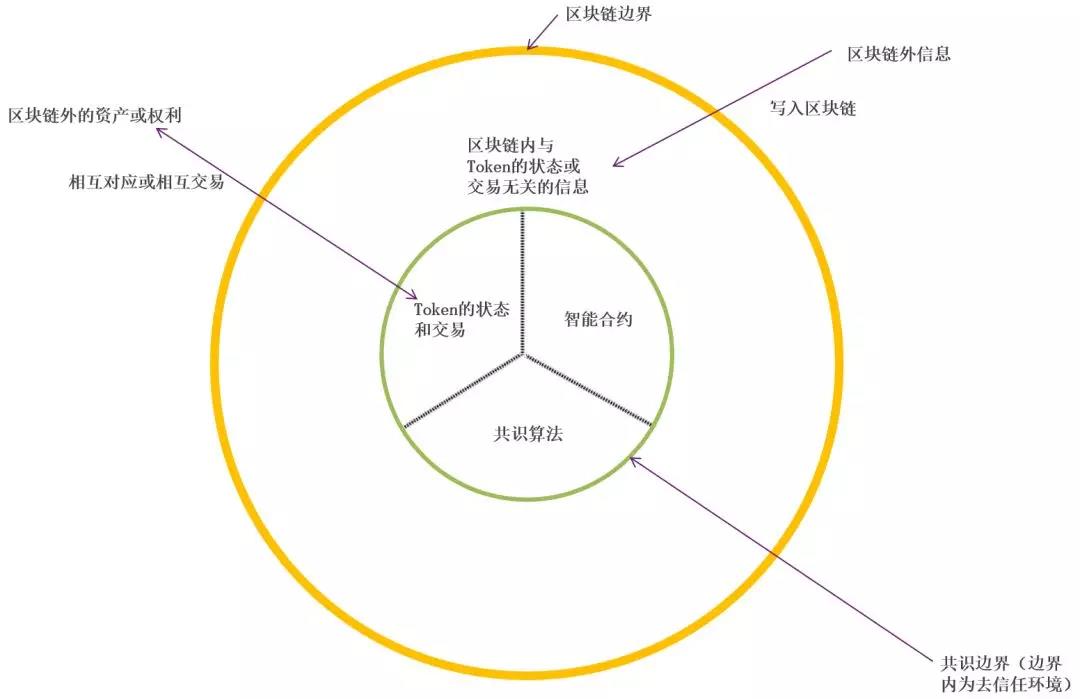

Figure 1 summarizes the design of the mainstream blockchain from an economic perspective. At present, the mainstream blockchain system, whether it is a public chain or a coalition chain, adopts the UTXO model represented by Bitcoin or the account model represented by Ethereum, regardless of whether the scripting language has Turing completeness or whether it supports smart contracts. Regardless of whether a non-mainstream blockchain structure such as a directed acyclic graph structure (DAG) is adopted, it is economically consistent with the description of FIG.

Tokens, smart contracts, and consensus algorithms are all within consensus boundaries. Tokens are inextricably linked to smart contracts. Consensus algorithms ensure a trusted environment within the boundaries of the consensus. Information that is unrelated to the state or transaction of the Token within the blockchain is outside the consensus boundary and within the blockchain boundary. There are two kinds of interactions inside and outside the blockchain: one is that the information outside the block chain is written into the blockchain; the other is the mutual transaction or mutual correspondence between the Token and the assets or rights outside the blockchain.

Figure 1: The Token paradigm of the blockchain

Figure 1: The Token paradigm of the blockchain

2. The nature of Token and its transactions

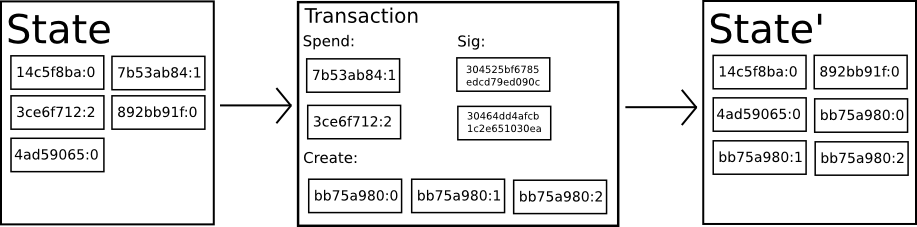

Token is essentially a state variable defined within a blockchain (Figure 2). Tokens defined by the same rule are homogeneous and can be split into smaller units. Asymmetric encryption guarantees the anonymity of the Token holder. Token can be transferred between different addresses. Blockchain consensus algorithms and non-tamperable features ensure that Tokens are not "double-flowered." The total amount of the Token transfer process is the same – the income of the A address is the loss of the B address. The status (book) update is completed at the same time as the transaction confirmation, and there is no settlement risk. Confirmed transactions are open to the public and cannot be tampered with. Token transactions within the blockchain do not rely on centralized trust institutions.

Source: Ethereum White Paper

Source: Ethereum White Paper

Figure 2: Token and its transactions

Figure 2: Token and its transactions

3. Consensus boundaries

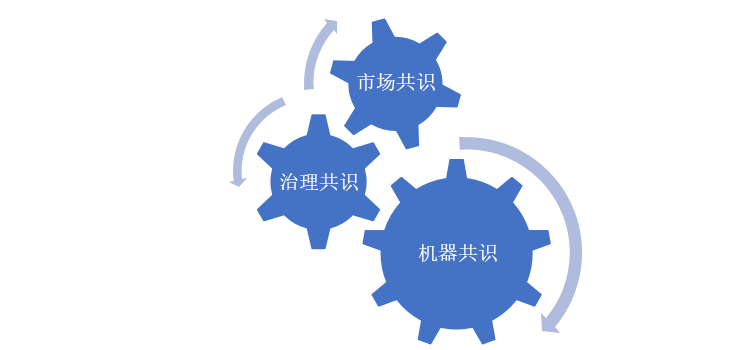

The current discussion of blockchain consensus involves consensus concepts in three different contexts—machine consensus, governance consensus, and market consensus (Figure 3). Governance consensus and market consensus can be called “human consensus.” However, many commentators have confused these three types of consensus, or generalized the scope and nature of the consensus.

Figure 3: Three types of consensus related to blockchain

Figure 3: Three types of consensus related to blockchain

First, machine consensus is a problem in the field of distributed computing. The goal is to have a variety of errors, malicious attacks, and possibly peer-to-peer networks, and without central coordination. Ensure that the distributed text of the distributed ledger on different network nodes is consistent (not semantically consistent). PoW, PoS, and DPoS, which we often say, are within the scope of machine consensus.

Second, governance consensus reflects the process of formulating or modifying algorithmic rules by people (including the owners or controllers of network nodes). The goal is for group members to develop and agree on a decision that is most beneficial to the group. Elements of governance consensus include: (1) different interest groups; (2) certain governance structures and rules of procedure; (3) conflicts between conflicting interests or opinions; and (4) groups with general constraints on members decision making. The discussion of “expansion” and forks in the Bitcoin community can be understood within the governance consensus framework. Many blockchain projects have adopted the structure of decentralized and open source communities. How to design a sustainable and open and inclusive governance consensus mechanism has become an important research topic.

Third, when Token participates in a transaction (whether it is a transaction between different Tokens, or a Token and a block-chain asset transaction), it involves market consensus. Market consensus is generated by market mechanisms based on machine consensus and governance consensus. The core of the market mechanism is trading and competition. Different buyers and sellers value differently for the same item. The market can match supply and demand. When equilibrium, commodity supply equals demand, and market price represents the price that suppliers and demanders can accept. Although market participants may still have their own valuation of the goods, they can only trade at the market price at that point in time. This is the meaning of market consensus. Market consensus does not mean that prices are stable – the sign of market equilibrium is the balance between supply and demand (or market clearing), which can go hand in hand with price fluctuations.

4. The function of the smart contract

A smart contract is a computer code that runs inside a blockchain and performs complex operations on the Token. The limited operating environment within the blockchain currently makes such code far from the smart phase. The image is that smart contracts are neither smart nor contractual.

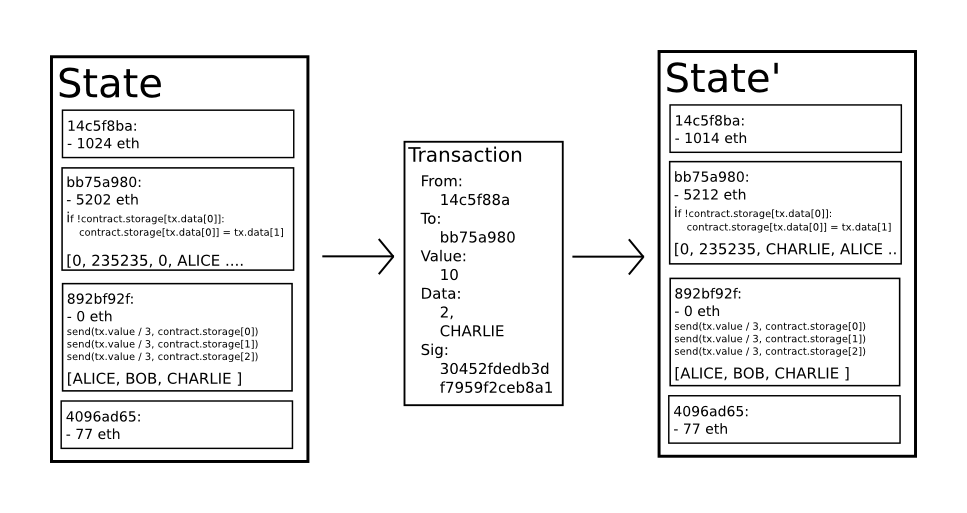

There is an inextricable link between Token and smart contracts. Token itself is an embodiment of a smart contract. For example, the Token contract represented by Ethereum ERC20 stipulates a series of logics such as the total amount of Token, the issuance rules, the transfer rules and the destruction rules. The Token contract manages a series of states, recording which addresses have as many tokens as Token. Based on the Token contract, you can build smart contracts that perform complex operations on Tokens. The result of these smart contract executions is mainly that the status of the Token has changed.

The shortcomings of smart contracts cannot be ignored. First, when the trigger condition of a smart contract depends on the information outside the blockchain, this information needs to be written into the blockchain first. This is called the oracle mechanism. There are two types of oracles that are currently discussed: one is to rely on a centralized information source (such as Bloomberg and Reuters). The second is to discretize the information outside the block and then use economic incentives and voting to write the blockchain. There is no perfect decentralized design in this respect.

Second, smart contracts cannot directly manipulate blockchain assets, such as bank deposits, houses, and vehicles.

Third, smart contracts are difficult to handle incomplete contracts. People are bounded and rational. It is impossible to foresee all possible situations in the future. Even if they are foreseen, they cannot be written into the contract, so the contract is bound to be incomplete. This is the exception to the existence of legal contracts in reality and the need for judicial arbitration in the event of a dispute. Smart contracts, as computer protocols, make it difficult to deal with incomplete contracts.

5. Two types of information within the blockchain

According to whether it is related to the status and transaction of Token, the information in the blockchain is divided into two categories—the relational and the unrelated. The two types of information have completely different status under the consensus algorithm. When the node runs the consensus algorithm, it checks whether the first type of information conforms to the predefined algorithm rules. For example, a Bitcoin node will test that a random number (nonce) is a solution to the "mining" problem, and that transactions in the block conform to pre-defined criteria in terms of data structure, grammatical normativeness, input and output, and digital signature. The second type of information is written into the blockchain as additional information for the Token transaction, and the node does not have the ability to verify the true accuracy of such information.

Distinguishing these two types of information is the key to understanding the scope of the blockchain consensus. The blockchain consensus is for information about the status and transactions of Token. For example, the Bitcoin consensus determines the number of UTXOs corresponding to each address, as well as the transfer of bitcoin records between addresses. Information in the blockchain that is not related to the status or transaction of the Token is basically outside the scope of consensus. If the information outside the blockchain cannot be guaranteed to be true and accurate at the source and write links, writing into the blockchain only means that the information cannot be falsified, and the true accuracy of the information is not improved. For example, “The Times 03/Jan/2009 Chancellor on brink of second bailout for banks” in the founding block of Bitcoin, although it is open to the whole network and cannot be tampered with after writing into the blockchain, if the source of information cannot be true Accurate, it is just "garbage in, garbage out." However, the blockchain helps to solve the problem of data registration and traceability. The data registered in the blockchain has a traceable subject identity signature and can be used for post-audit, and the irreversible modification of the uplink data also helps to control operational risks.

6. Blockchain and trust

De-trust comes from the fact that the Token's status change and transaction confirmation occur synchronously when the Token is traded. Imagine Alice buying a certain item from Bob in Bitcoin. Alice's process of paying Bitcoin to Bob does not require any knowledge between the two, nor can it be secured within the blockchain without a trusted third party. This is the true meaning of trust. But at the other end of the transaction, how does Alice ensure that Bob will deliver qualified goods to her on time? As long as you can't do bitcoin and deliver in one hand, there is a risk of counterparty credit that cannot be ignored. Many transactions can only be carried out if the credit risk is accurately identified, assessed, and risk prevention measures are introduced. For example, in a dark web transaction, the trading platform usually sets up a third party escrow account. The buyer first enters the bitcoin into a third-party escrow account, and waits for the transaction platform to confirm and then informs the trading platform to transfer the bitcoin to the seller. If there is no means of adding credit to third-party escrow accounts, the transactions between loyal fans of Bitcoin will be greatly reduced.

Therefore, the de-trust environment within the blockchain cannot simply be extrapolated outside the blockchain. Once the native scenes such as Token transactions are removed, the blockchain must solve the real-life trust problem and often need to introduce a trusted central mechanism outside the blockchain to assist. The management of block credit risk outside the block is the core obstacle faced by many blockchain projects (eg, asset chaining, intellectual property registration, etc.).

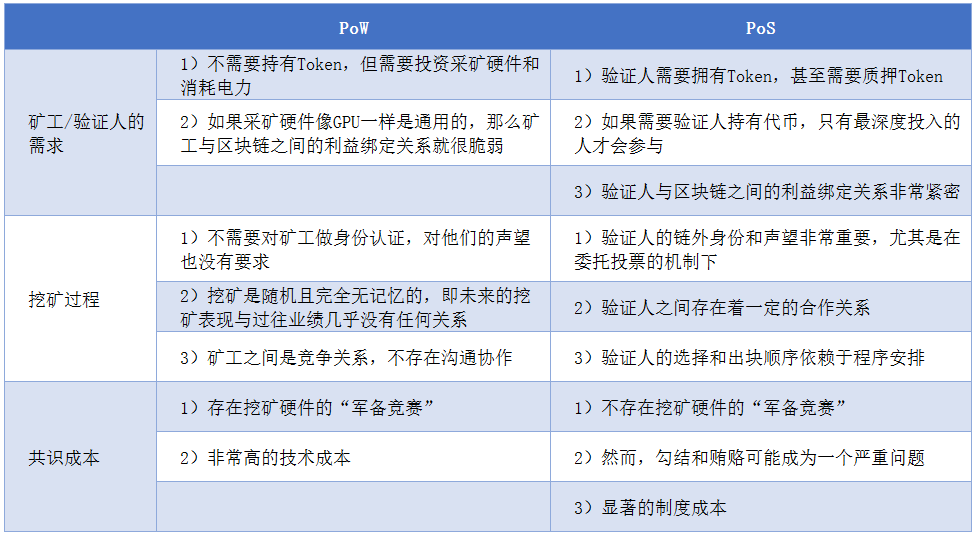

In the field of blockchain, we can observe two types of trust: one is based on technology-based trust, represented by POW; the other is based on institutional trust, represented by POS. Table 1 compares the trust foundations of P0W and P0S.

From: Platon Economic Blue Book

Table 1: Trust base for POW and POS

Table 1: Trust base for POW and POS

Second, blockchain application classification

Blockchain applications are generally classified according to the industry in which the application scenario belongs, such as the application of blockchain in the fields of financial services, supply chain management, culture and entertainment, smart manufacturing, social welfare, and education and employment. Based on the economic function of Token, I propose a different classification standard.

1.Token's economic function and application classification criteria for blockchain

From the perspective of industry practice, Token has four functions. First, the purpose of the Token is defined by rules within the blockchain, where Token is generally referred to as cryptocurrency. For example, in the Bitcoin system, Bitcoin is used to pay transaction fees to “miners”; in Ethereum, Ether is the “fuel” for running smart contracts. Since the goods or services in the blockchain cannot be purchased in a fixed currency, the cryptocurrency price generally has no significant effect on this scenario.

Second, use Token to purchase goods or services outside the blockchain. But Token price is an important factor. The Token supply has no flexibility, lacks intrinsic value support and sovereign credit guarantees, and has high price volatility and cannot effectively perform monetary functions. Therefore, stabilizing the currency is an important direction, and you can also understand the central digital currency from this perspective.

Third, the equity type Token. Token is given a certain income right and governance right, in which the income right can be realized through dividends, Token repurchase and so on, and the governance right is realized by voting.

Fourth, use Token to represent assets or rights outside the blockchain. This reflects the function of the blockchain as a financial infrastructure.

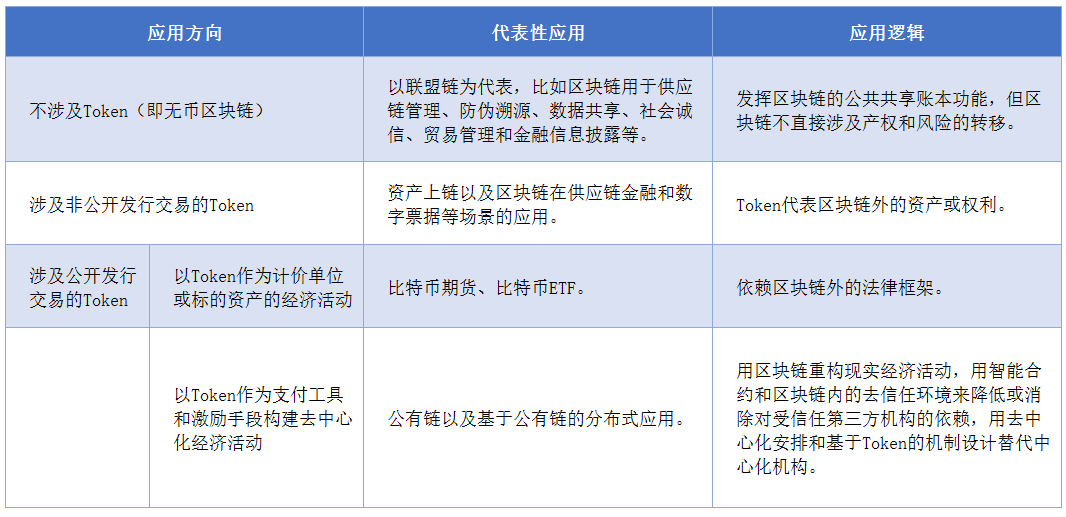

Table 2 proposes a new classification method based on the blockchain application for Token usage:

Table 2: Main application directions of blockchain

Table 2: Main application directions of blockchain

2. Currency-free blockchain

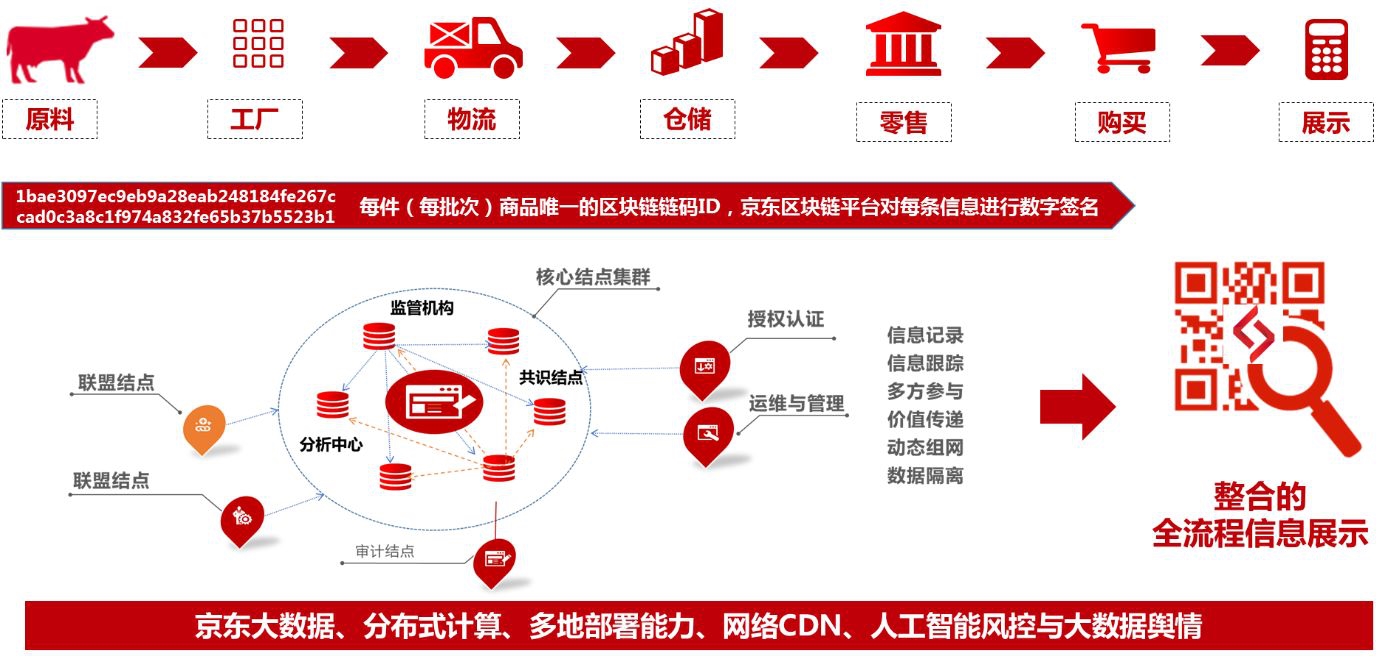

This type of application does not involve Tokens, and mainly uses blockchains as distributed databases or decentralized databases. The public shared ledger function of the blockchain helps to alleviate the information asymmetry between economic activity participants and improve the efficiency of their division of labor. The main problem faced by such applications is how to ensure the authenticity of the information outside the blockchain at the source and in the blockchain. Compared to the public chain, the alliance chain is more suitable for such applications. The alliance chain is only open to the authorized nodes and is jointly maintained by the authorization nodes to achieve inter-organizational consensus. The authorized nodes know each other's identity, and the evil will affect the reputation. The cost of writing false information into the blockchain is relatively high. The information written into the blockchain can also be introduced into a third-party authentication organization to verify the authenticity of the information. However, these safeguard mechanisms are mainly based on real-world constraints rather than the characteristics of the blockchain itself. In addition, the alliance chain also faces storage and throughput limitations, and the unstructured information outside the blockchain is often “hashed up”. Figure 4 shows an example of JD's application of blockchains in the supply chain.

Source: Jingdong

Figure 4: Jingdong's application of blockchain in supply chain management

Figure 4: Jingdong's application of blockchain in supply chain management

3.Token represents assets or rights outside the blockchain

Such applications use Token to represent assets or rights outside the blockchain to improve the registration and transaction process of those assets or rights. But does the Token correspond to assets or rights outside the blockchain, and whether the status and transactions of the Token are binding or influential on the real world outside the blockchain, depending on whether the laws and institutions outside the blockchain give Token Beyond the connotation of the blockchain.

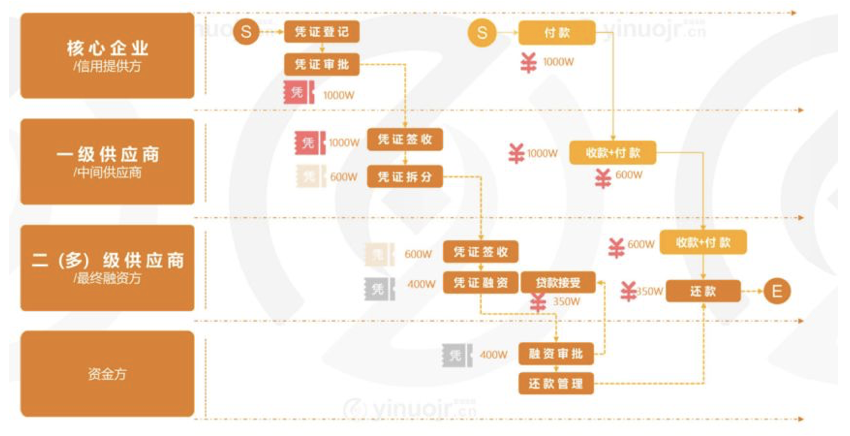

In this type of application, the application of blockchain in supply chain finance is worthy of attention (Figure 5). At this point, Token represents the claims of a core institution and acts as an internal settlement tool in the supply chain. Token replaces the “triangular debt” between the upstream and downstream enterprises in the supply chain and replaces them with the liabilities of the core institutions for these enterprises, which can reduce capital occupation and improve capital turnover efficiency. The core institution acts like a central counterparty and is responsible for the exchange between Token and fiat currency. It should be said that this application scenario is not technically difficult. The challenge lies in regulatory compliance and business development.

Source: yinuojr.cn

Figure 5: Application of blockchain in supply chain finance

Figure 5: Application of blockchain in supply chain finance

In general, Token represents assets or rights outside the blockchain that essentially reflect the relationship between the blockchain and the financial infrastructure. The application of blockchain in scenarios such as trade finance, accounts receivable and digital notes, stable currency and central bank digital currency are all examples of such applications.

Distributed business

Many blockchain projects attempt to build a distributed autonomous organization (DAO) with blockchains and propose that distributed autonomous organizations can replace the functions of real-world companies. However, there are no widely recognized success stories in this area, which are mainly subject to the following obstacles: (1) the physical performance of the public chain is not high enough to support large-scale transactions; (2) the shortcomings of smart contracts; (3) Token prices The high volatility limits the effectiveness of Token as a payment instrument and incentive; (4) The design of token economics (token economics or crypto economics) is unreasonable.

Another economically viable direction is distributed commerce. Distributed commerce has four core business logics: one is to replace the centralized platform company with a distributed and autonomous economic organization; the other is to replace the profit and equity appreciation of the centralized platform company with the network value and Token appreciation; The trust relationship of the blockchain replaces the trust of the centralized platform company; the fourth is the self-organizing alternative centralization coordination. Distributed commerce involves very complex mechanism design, asset pricing, and monetary theory issues, but there are solutions. The core is to design the value capture mechanism of Token.

Third, blockchain and financial infrastructure

The financial infrastructure is divided into account paradigm and Token paradigm. The former is represented by the bank account system, and the latter is represented by the blockchain. These two paradigms are very different, but they can all be used to carry financial assets and transactions, presenting very complex alternatives and complementary relationships in many application scenarios.

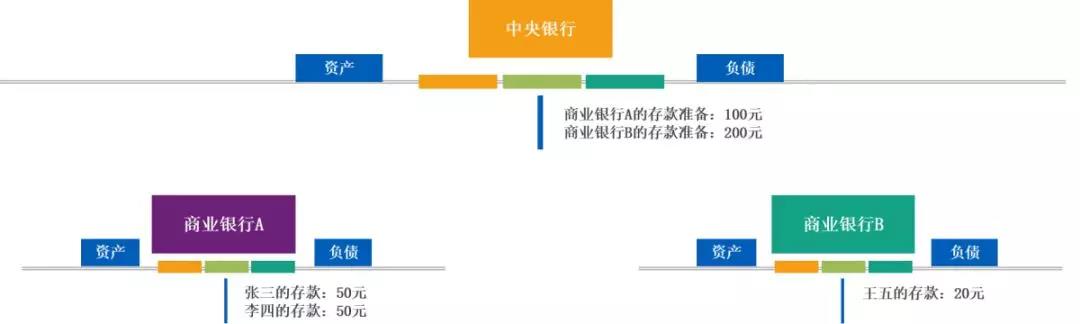

1. The secondary bank account system of legal tender

Individuals and enterprises open deposit accounts in commercial banks, and commercial banks open deposit reserve accounts in central banks. The legal currency exists in the liability side of the financial system. The base currency is the liability of the central bank. Among them, the cash is the central bank's debt to the public, and the deposit reserve is the central bank's liability to commercial banks. Deposits are the central bank’s liabilities to individuals and businesses. In modern economies, cash is only a small percentage of the money supply, and most of the broad money supply is deposits. Currency forms such as deposit reserves and deposits have all been electronic.

Figure 6: Secondary Bank Account System

Figure 6: Secondary Bank Account System

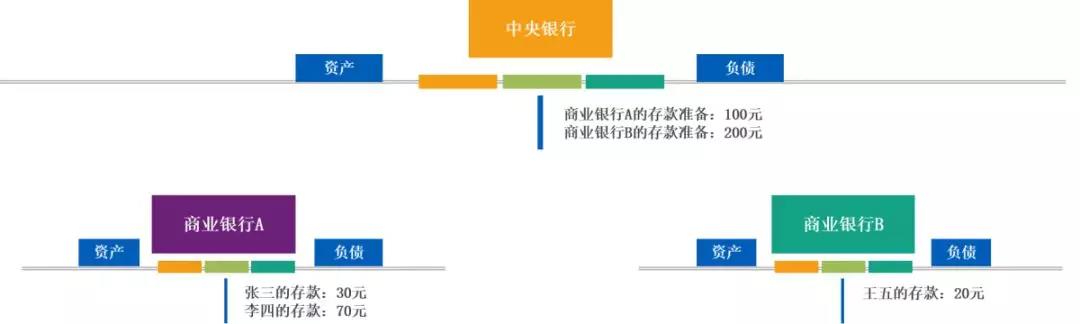

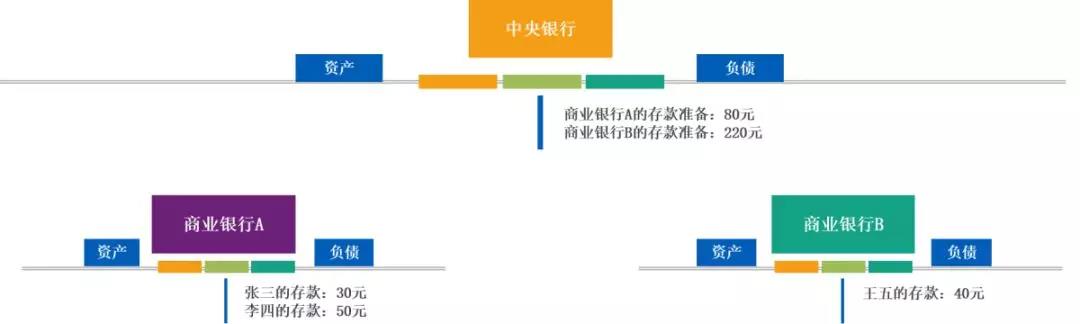

In a cash transaction, the parties to the transaction can deliver the cash as long as they confirm the authenticity of the cash, without the need for a third-party trusted institution. This is similar to the Token transaction that will be introduced later. Transfers and remittances involve bank account operations. For example, peer transfer should simultaneously adjust the balance of the deposit accounts of the two parties in the same bank. In addition to adjusting the balance of the deposit accounts of the two parties in the respective bank, the inter-bank transfer involves settlement between the two banks. Settlement between commercial banks is subject to adjustments to their deposit reserve accounts at the central bank. Figure 7 is a simple example.

(Peer-to-peer transfer: Zhang San turns 20 yuan to Li Si)

(Peer-to-peer transfer: Zhang San turns 20 yuan to Li Si)

(Inter-bank transfer: Li Si turned 20 yuan to Wang Wu) Figure 7: Transaction currency

(Inter-bank transfer: Li Si turned 20 yuan to Wang Wu) Figure 7: Transaction currency

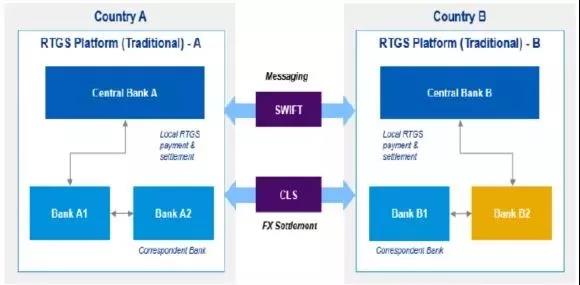

The bank account operations involved in cross-border payments are more complicated. Figure 8 is taken from Bank of Canada, Bank of England, and Monetary Authority of Singapore (2018), from Bank of Canada, Bank of England, and Singapore Monetary Authority, page 28 of the report. Figure 1.

Figure 8: Cross-border payment

Figure 8: Cross-border payment

Suppose two countries, A and B, and their respective currencies, A currency and B currency. Both currencies have their own payment systems established by their respective central banks (RTGS in Figure 8, the real-time full payment system). For example, the renminbi is a large-value payment system and a cross-border payment system (CIPS), and the US dollar is the Federal Electronic Funds Transfer System (Fedwire) and the New York Clearing House Interbank Payment System (CHIPS).

Assume that A country resident Alice has a deposit of A currency in a bank A1 in country A. She has to pay Bob, a resident of Country B, who has a B-currency deposit account at a bank B2 in Country B. The problem is that there is no direct business relationship between Bank A1 and Bank B2. Therefore, it is necessary to introduce a correspondent bank, namely bank A2 and bank B1 in FIG. The correspondent bank played a bridge between bank A1 and bank B2, but extended the cross-border payment chain.

In the correspondent banking mode, cross-border payment is performed as follows. First, in country A, Alice's A currency deposit at bank A1 is transferred to bank A2 (through the A currency payment system). Second, funds are transferred from bank A2 to bank B1. Acting banks open accounts with each other. For example, from the perspective of bank A2, the account opened by bank B1 is called the nostro account (B currency), that is, the foreign bank account is deposited. The account opened by bank B1 at bank A2 is called the vostro account, which is the interbank deposit account. The transfer of funds from bank A2 to bank B1 is achieved by adjusting these account balances. Currency exchanges need to go through a continuous connection settlement system (ie CLS in Figure 8). Finally, funds are transferred from bank B1 to bank B2 (through the payment system of B currency).

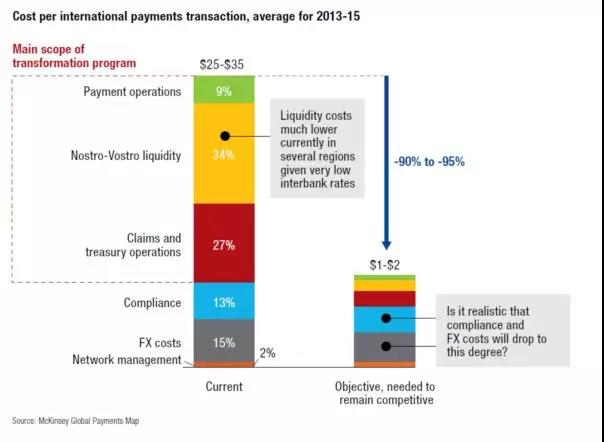

Two points need to be explained: First, unlike popular cognition, the Global Interbank Financial Telecommunication Association (SWIFT) is an interbank messaging system that handles the flow of information in cross-border payments. The flow of funds in cross-border payments is carried out through the bank account system. Second, some blockchain projects believe that SWIFT is the main reason for the high cost of cross-border payments. However, it is not. McKinsey & Company's 2016 study shows (McKinsey & Company, 2016) that the average cost of a cross-border payment by a US bank through a correspondent bank is between $25 and $35, which is more than 10 times the average cost of a domestic payment. Of these, 34% of the cost comes from liquidity locked into the correspondent bank account (because these funds could have been used in higher-paying places), 27% from treasury operations, 15% from foreign exchange operations, 13% From compliance costs. See Figure 9, taken from McKinsey & Company (2016), which is Exhibit9 on page 21 of the report.

Figure 9: Cost of cross-border payments

The above briefly describes how the account paradigm carries currency and its transactions. We sacrificed rigor for readability. For example, account balance adjustment and capital flow are not rigorous academic terms, and can be expressed as a series of complicated debit and credit operations in accounting.

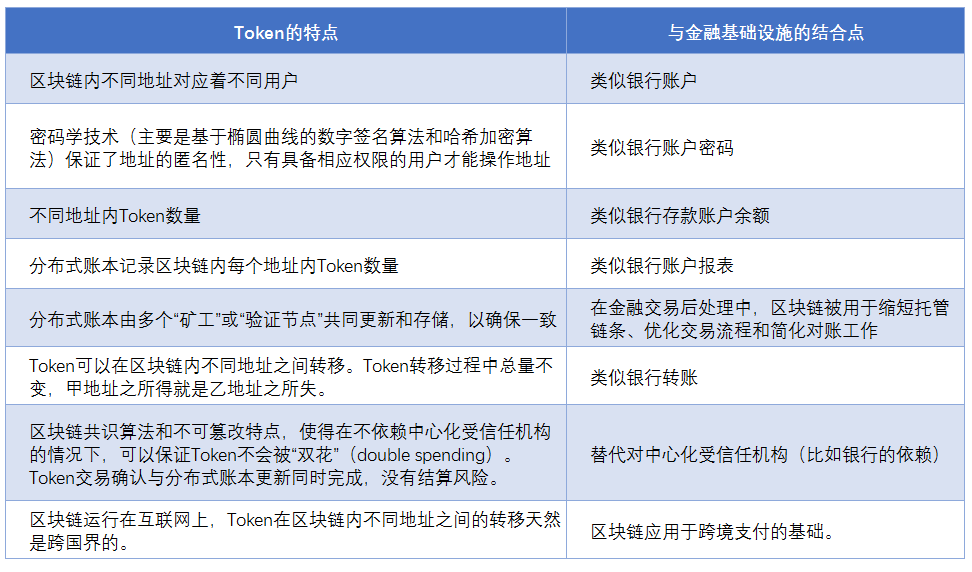

2.Token carrying assets and transactions

The following nature of Token and its transactions is key to the application of blockchain to financial infrastructure (see Table 3 for a summary). First, different addresses within the blockchain correspond to different users, similar to bank accounts. Cryptography technology (mainly based on the elliptic curve digital signature algorithm and hash encryption algorithm) guarantees the anonymity of the address, only users with the appropriate permissions can operate the address, similar to the bank account password.

Second, the Token is essentially a state variable defined by rules within the blockchain. Tokens defined by the same rule are homogeneous and can be split into smaller units. The number of Tokens in different addresses, similar to the bank deposit account balance. The distributed ledger records the number of tokens in each address within the blockchain, similar to a bank account statement. The distributed ledger is updated and stored by multiple “miners” or “verification nodes” to ensure consistency. In the post-financial transaction processing, blockchain is used to shorten the custody chain, optimize the transaction process and simplify the reconciliation work, which is based on the characteristics of distributed ledger.

Third, Tokens can be transferred between different addresses within the blockchain, similar to bank transfers. The total amount of the Token transfer process is constant, and the income of the A address is the loss of the B address. The Token transaction confirmation is completed at the same time as the distributed ledger update, and there is no settlement risk. Distributed ledgers and confirmed Token transactions are publicly available and cannot be tampered with.

Fourth, the blockchain consensus algorithm and the non-tamperable feature make it possible to ensure that the Token will not be double-flowered without relying on a centralized trusted organization.

Fifth, the blockchain runs on the Internet, and the transfer of Tokens between different addresses within the blockchain is naturally cross-border. This feature is the basis for the blockchain to be applied to cross-border payments.

Table 3: The combination of the Token paradigm and the blockchain

Table 3: The combination of the Token paradigm and the blockchain

Token is a piece of computer code in its form of existence, without any intrinsic value. So what is the source of Token's value? Token is generally translated into symbols or representations in Chinese. The token or representation itself has no value, and the value comes from the assets it carries. The use of Token to carry real-world assets (so-called “asset-winding”) is essentially based on laws and regulations, using economic mechanisms outside the blockchain to link Token to the value of certain types of underlying assets. This process is inseparable from centralized trustees (Table 4).

Table 4: Carrying assets with Token

There are 3 rules that must be followed to carry assets with Token. The first is the issuance rule: the centralized trustee is issuing a token based on the underlying asset in a 1:1 relationship.

The second is the two-way redemption rule: the centralized trustee ensures a two-way 1:1 redemption between the Token and the underlying asset. The user gives the unitized assets of the unitized trusted institution 1 unit, and the centralized trusted organization issues a unit of token to the user. The user returns 1 unit Token to the centralized trusted authority, and the centralized trusted organization returns 1 unit of the asset to the user.

The third is the credible rule: centralized trustees must regularly audit third parties and fully disclose information to ensure the authenticity and adequacy of the underlying assets of the Token distribution reserve.

Under the constraints of these three rules, a unit of Token represents the value of an asset of 1 unit of the subject. When Token has a secondary market transaction, the Token market price will deviate from the value of the underlying asset, but the market arbitrage mechanism will drive the price to return to value: if the price of the 1 unit token is less than the value of the 1 unit of the asset, the arbitrage will press The market price buys 1 unit of token, and then returns the unitized assets from the centralized trustee to obtain the intermediate spread (=1 the value of the unit's underlying asset – the price of the unit token). Arbitrage activity will increase demand for Token and drive its price up. Conversely, if the price of the 1 unit token is higher than the value of the 1 unit asset, the arbitrageur will exchange 1 unit of the asset with the centralized trusted institution for 1 unit token, and obtain the intermediate price difference (=1 unit token price -1 unit) The value of the underlying asset). Arbitrage activities increase the supply of Token, driving its prices down.

Once these three rules are not strictly adhered to, the effect of the market arbitrage mechanism will be weakened, and the Token price will be decoupled from the value of the underlying asset (not necessarily completely decoupled).

Which assets are suitable for hosting with Token? This depends mainly on whether the asset meets the requirements of the two-way exchange rules, which in turn depends on the existence of the asset, the level of standardization or homogenization, the system of property rights recognition and registration, and the transaction process. Assets with standardized, clear property rights and simple transaction processes are best suited to be carried by Token, mainly including monetary and financial securities.

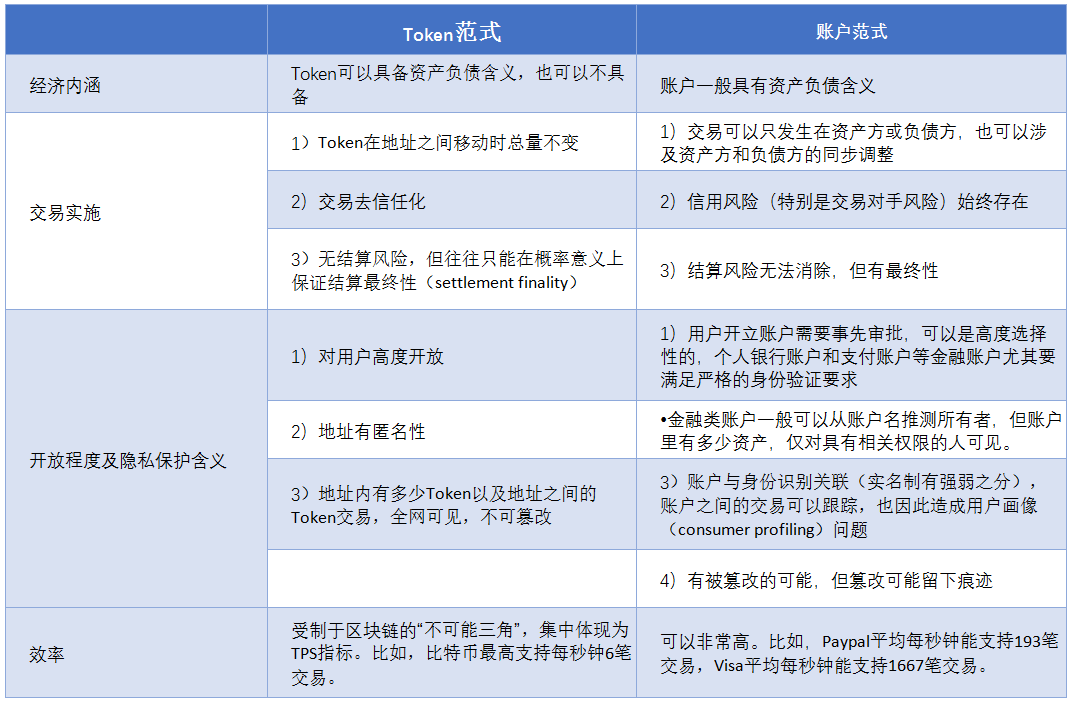

3. Comparison of the two paradigms

Table 5: Comparison of Token Paradigm and Account Paradigm

Table 5: Comparison of Token Paradigm and Account Paradigm

(1) Performance in trading scenarios

When the Token is transferred between different addresses in the blockchain, the total Token does not change. Token transactions do not rely on centralized trustees. The transaction confirmation and distributed ledger update are completed synchronously and there is no settlement risk. However, many blockchains can only guarantee settlement finality in a probabilistic sense because of the possibility of bifurcation, although the probability can tend to be 100% over time. The blockchain is subject to the "three-dimensional paradox": no blockchain can have three characteristics of accuracy, decentralization and cost efficiency. In particular, the higher the decentralization of the blockchain, the lower the efficiency, and the efficiency is concentrated in the number of Token transactions (TPS) that can be supported per second. For example, Bitcoin supports up to 6 transactions per second.

Under the account paradigm, the transaction can involve only the internal adjustment of the asset side or the liability side, or it can involve the simultaneous adjustment of the asset side and the liability side. For example, if a bank lends money to a company, the bank has an additional loan to the enterprise on the asset side and an additional corporate deposit on the liability side. Under the deposit reserve system, this process continues as a multiplier expansion mechanism for deposits. Account maintenance is inseparable from centralized trusted institutions (such as banks), and credit risk (especially counterparty risk) is always present. The settlement risk cannot be eliminated, but there is a final settlement. Transaction efficiency under the account paradigm can be very high. For example, PayPal can support an average of 193 transactions per second, and Visa can support an average of 1,667 transactions per second.

(2) Openness and privacy protection

Blockchains are highly open to users. Anyone who generates a pair of public and private keys based on a digital signature algorithm can have an address within the blockchain. The address has good anonymity. It is difficult to identify the address owner without using techniques such as cluster analysis. However, there are many Tokens in the address and Token transactions between the addresses, which are visible on the whole network and cannot be tampered with. Trading with Token is like an anonymous veil. While this helps protect the privacy of address owners, it also increases the regulatory difficulty of KYC ("know your customers"), AML (anti-money laundering), and CFT (anti-terrorism financing).

Opening an account generally requires approval and is therefore highly selective. Personal bank accounts and payment accounts must meet strict authentication requirements. Interested readers can refer to the “Administrative Measures for Network Payment Services of Non-bank Payment Institutions” (People's Bank of China Announcement [2015] No. 43) and “Implementation of Personal Banking” Notice of Account Classification Management System (Yinfa [2016] No. 302). Financial accounts can generally infer the owner from the account name, but how many assets are in the account, only visible to those with relevant permissions. This is also a key difference between the account paradigm and the Token paradigm.

If you expand your horizons from financial accounts to social network accounts, e-commerce accounts, and various application accounts, you will find that although the real-name system of different accounts has strengths and weaknesses, accounts are always associated with identification. The account records the behavior of its owner in different scenarios, such as social, shopping, and travel. By analyzing these behavioral information, the account owner can be imaged (consumer profiling) and inferred important characteristics such as account owner preferences, credit and income. This is the information base for Internet companies to conduct advertising business (which is still the main source of revenue for Google and Facebook) and for financial services such as financial precision marketing and online lending. In 2013, Mr. Wan Jianhua made a very predictable introduction to the concept of “the account holder gets the world” in the “Financial E-Time”.

However, the collection and use of personal information under the account paradigm can easily evolve into infringement of personal privacy. Personal information is difficult to defend, difficult to protect, easy to use without reasonable authorization, or data collected from A business is used for B business. Organizations holding personal information may cause personal information to be stolen if they are not adequately secured. This is reflected in the data breach scandals of Facebook and Cambridge Analytica. These problems faced by the account paradigm do not exist under the Token paradigm.

Data management and privacy protection have increasingly become an important policy issue that can significantly impact future Internet business models. In May 2018, the European Union began implementing the General Data Protection Regulations (GDPR). In May of this year, China's Internet Information Office issued the "Data Security Management Measures (Draft for Comment)." Data management and privacy protection are not entirely institutional issues, but also cryptographic techniques such as verifiable computing, homomorphic encryption, and secure multi-party computation. Readers interested in these cryptography techniques can refer to PlatON (2018).

(3) Alternatives and complementarities between the two paradigms

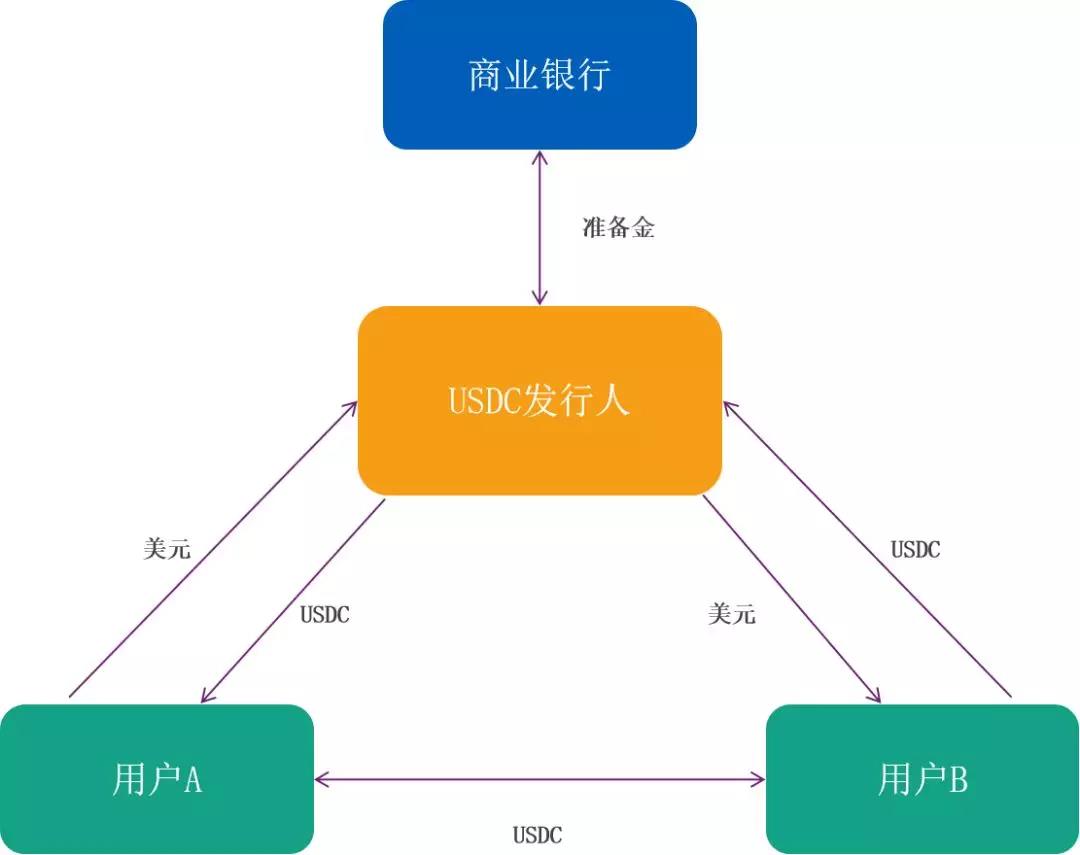

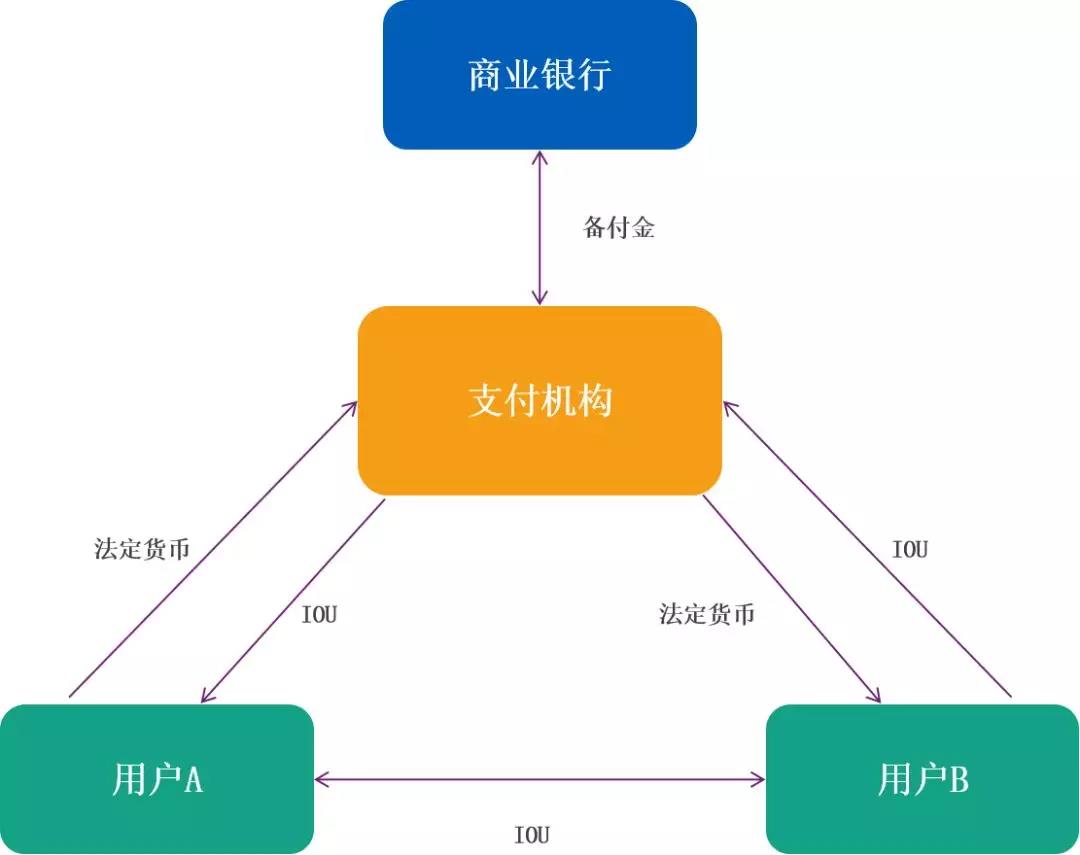

First, there are alternative relationships between the two paradigms in some scenarios, such as stabilizing cryptocurrencies and third-party payments (Figure 10).

In September 2018, Circle Company of the United States launched USDC (Circle, 2018) based on Ethereum. The USDC is issued in 1:1 with a US dollar reserve. Any organization that follows the USDC agreement and meets regulatory compliance requirements can become a USDC issuer. The USDC follows the rules for two-way redemption. The USDC issuer will be deposited in a FDIC-protected bank upon receipt of the US dollar reserve provided by the user. The USDC transaction between users is a Token transaction within the blockchain and does not affect the reserve at the bank. When the USDC user redeems the USDC, the USDC issuer will transfer the corresponding amount from the reserve to the user's bank account in addition to destroying the received USDC.

(The above is a stable cryptocurrency)

(The above is a stable cryptocurrency)

(The above is a third party payment)

(The above is a third party payment)

Figure 10: Comparison of stable cryptocurrency versus third-party payment

In the third-party payment, after the user recharges the payment institution, the payment institution will deposit the legal currency received into its reserve fund account in the bank, and increase the balance of the account of the user in the payment institution. The balance of this account is essentially IOU (I owe you). Transfers between users only affect their account balance (IOU transactions) at the payment institution, and will not affect the reserve fund at the bank. When the user withdraws, the payment institution deducts the balance of the user account (deregistered IOU), and transfers the corresponding amount from the reserve fund to the user's personal bank account. It should be noted that the mode described before is "broken straight". After "disconnected directly", if you combine the network with the third-party payment, the description here is still applicable.

Therefore, the stable cryptocurrency and the third-party payment are isomorphic in the model, the former belongs to the Token paradigm, and the latter belongs to the account paradigm.

Second, the complementary relationship between the two paradigms is followed by the USDC example (Figure 11). Currently, most USDC transactions take place on cryptocurrency exchanges. The user transfers the USDC to the blockchain address of the cryptocurrency exchange, and the cryptocurrency exchange equalizes the account balance (IOU) of the user on the exchange. The USDC transaction within the cryptocurrency exchange is actually an IOU transaction. The reason for this is that USDC transactions within the blockchain are subject to the performance of the blockchain, and IOU transactions are much more efficient.

Figure 11: Complementarity between the two paradigms

Figure 11: Complementarity between the two paradigms

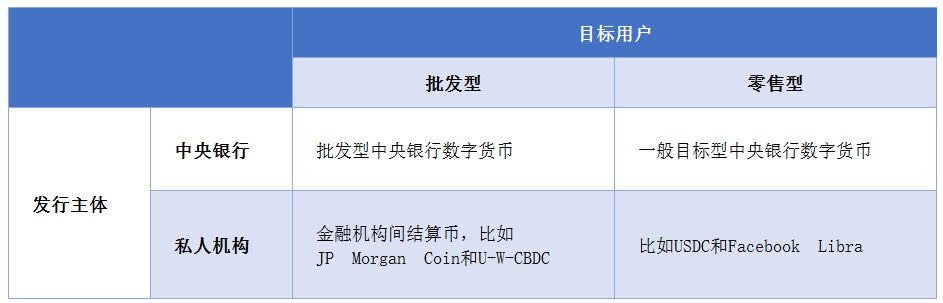

4. Application classification of Token paradigm in the legal currency field

Table 6 classifies the Token paradigm of the fiat currency domain in two dimensions. The first dimension: whether the issuer is a central bank or a private institution. The second dimension: whether the target user is wholesale (institutional only) or retail (public).

Table 6: Application classification of Token paradigm in the field of French currency

Table 6: Application classification of Token paradigm in the field of French currency

Since the deposit reserve is electronic, the wholesale central bank digital currency is less meaningful, so we only introduce the types in Table 6 other than the wholesale central bank digital currency. This discussion helps us understand the technical and economic context of Facebook Libra.

(1) Central Bank Digital Currency (CBDC)

The CBDC is a form of legal tender, which is the electronic currency issued directly by the central bank to the public and is also the liability of the central bank. The CBDC replaces the cash.

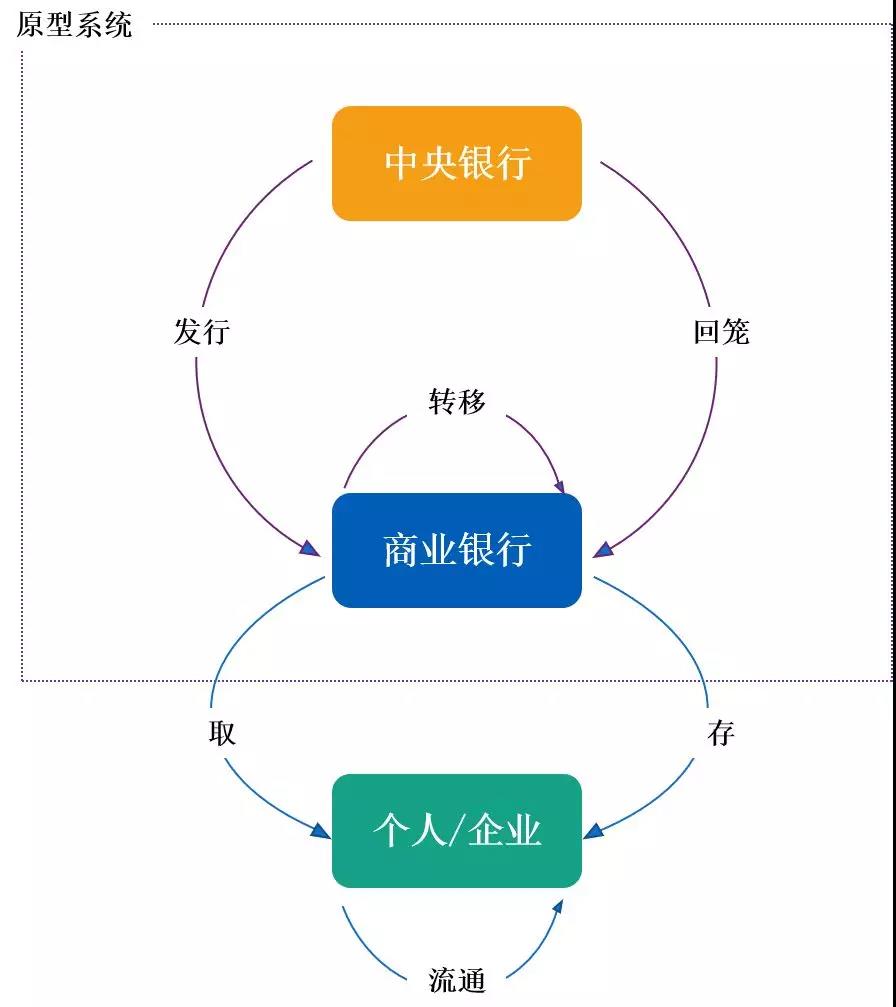

The CBDC faces several controversial issues. First, in the technical path, CBDC can adopt the Token paradigm or the account paradigm. How to choose is still inconclusive. Second, whether CBDC pays interest. If CBDC is used to completely replace cash and pay interest, it is theoretically a new monetary policy tool, especially at the zero lower bound of the nominal interest rate. Third, the impact of CBDC on the stability of commercial bank deposits. Because the central bank’s credit is higher than that of commercial banks, will ordinary people withdraw large-scale commercial bank deposits and switch to CBDC? Because of these problems, there is currently no major country to introduce CBDC.

The following CBDC prototype system was designed from Yao Qian (2018). The CBDC prototype system is divided into three layers (Figure 12, Figure 1 on page 3 of Yao Qian (2018)). The first layer is the issuance and withdrawal of CBDC between the central bank and commercial banks, and the transfer between commercial banks. The second layer is for individuals and business users to access CBDC from commercial banks. The third layer is the transfer of CBDC between individual and business users.

Figure 12: Central Bank Digital Currency Prototype System

Figure 12: Central Bank Digital Currency Prototype System

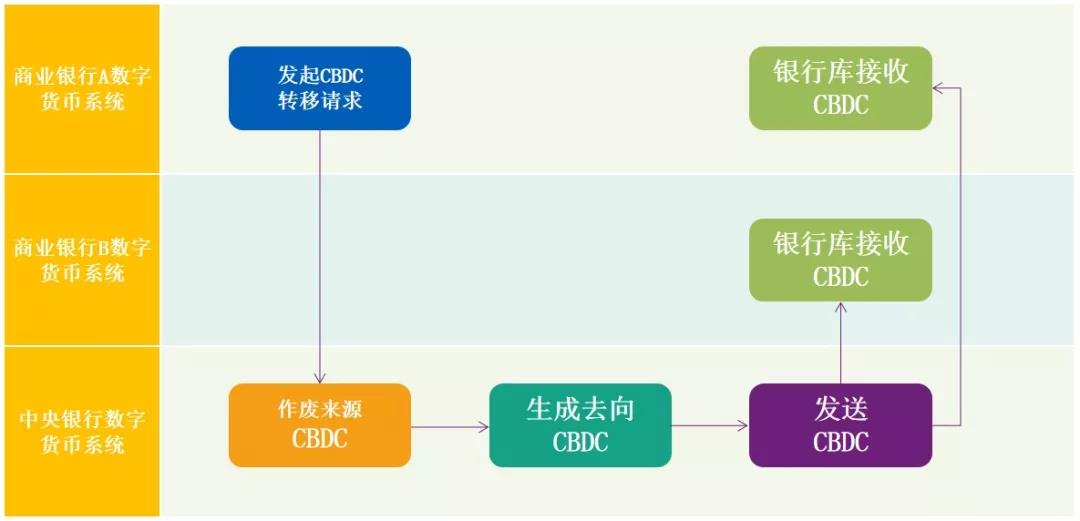

The transfer of CBDC between commercial banks, between commercial banks and between individuals and business users, and between individual and corporate users is essentially a Token transaction within the blockchain. Figure 13 shows the transfer process of CBDC (Figure 6 on page 7 of Yao Qian (2018)). After the commercial bank A issues a CBDC transfer request to the central bank, the central bank invalidates the source currency and generates the denomination currency of the commercial bank B according to the transfer amount. If there is a balance after the transfer, the return currency of the owner is the commercial bank A. This transfer process is similar to the UTXO (unspent transaction output) mode.

Figure 13: Central Bank Digital Currency Transfer Process

Figure 13: Central Bank Digital Currency Transfer Process

The CBDC issuance and returning follow the two-way exchange rules, and the central bank deposit reserve account needs to be adjusted. After the commercial bank applies to the central bank for the issuance of CBDC, the central bank first deducts the deposit reserve of the commercial bank and equalizes the digital currency issuance fund, and then generates the CBDC whose owner is the commercial bank. After the commercial bank applies to the central bank to deposit the CBDC, the central bank first destroys the deposited CBDC, deducts the digital currency issuance fund and increases the deposit reserve of the commercial bank in equal amounts. This ensures that the total amount of currency issuance remains the same in CBDC issuance and return.

(2) Inter-enterprise settlement currency

In February 2019, JPMorgan Chase announced the launch of JP Morgan Coin (JP Morgan, 2019, see Figure 14) for real-time settlement of inter-client transactions based on the Quorum Alliance chain. JP Morgan Coin represents the US dollar deposited in the designated account of JP Morgan Chase. After depositing the US dollar into the designated account, the customer will receive an equal amount of JP Morgan Coin. The transfer of JP Morgan Coin between customers took place on the Quorum Alliance chain. Customers are not necessarily in the United States, which enables cross-border payments. After the customer returns to JP Morgan Coin, they will receive an equivalent amount of dollars transferred from the designated account.

Figure 14: JP Morgan Coin

Figure 14: JP Morgan Coin

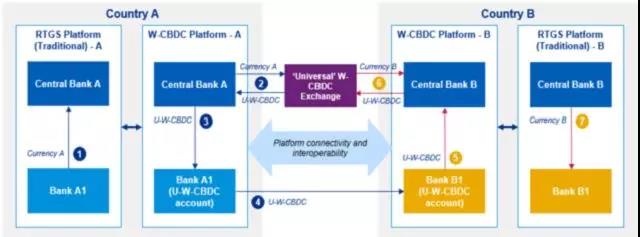

(3) Application of blockchain in cross-border payment

UW-CBDC is a cross-border payment scheme proposed by the Bank of Canada, the Bank of England and the Singapore Monetary Authority's 2018 study, Cross-Border Interbank Payments and Settlement. In UW-CBDC, U refers to the global, W refers to the wholesale type, and CBDC refers to the central bank digital currency (but UW-CBDC is not issued by the central bank). UW-CBDC is similar in many ways to Facebook Libra (Figure 15, Figure 5 on page 36 of the above report).

Figure 15: UW-CBDC for cross-border payments

Figure 15: UW-CBDC for cross-border payments

UW-CBDC is created by multiple countries through their central banks or an international multilateral organization. UW-CBDC uses a basket of currencies as a reserve. UW-CBDC is issued and returned through an exchange, and the central bank participating in UW-CBDC can use its exchange to buy and sell UW-CBDC through the exchange. National commercial banks then exchange UW-CBDC with their national currency to their central bank.

Commercial banks directly settle cross-border transactions through UW-CBDC. Commercial banks using UW-CBDC do not need to be in the same country, do not need to open each other's nostro account and vostro account, nor do they need to go through a correspondent bank. This simplifies the cross-border payment chain and eliminates the cost of locking liquidity at the correspondent bank.

If you extend the reach of UW-CBDC to both personal and business users (from wholesale to retail), it's actually the Facebook Libra model.

5.Token paradigm in the post-financial transaction processing

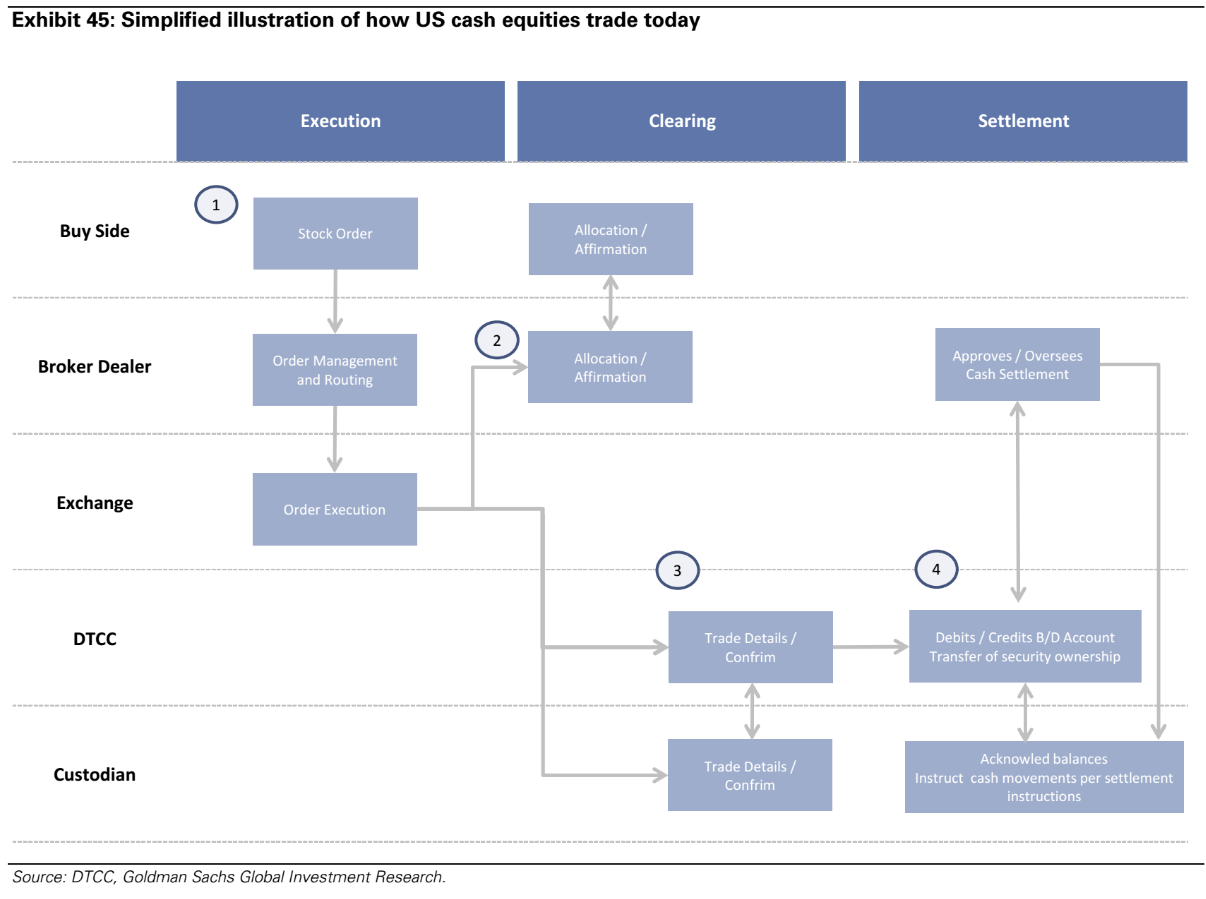

Post-financial settlement is mainly composed of three steps: (1) transaction order management (including transaction verification); (2) liquidation, that is, calculating the financial obligations of both parties to the transaction; and (3) settlement, which is the final asset transfer. Central Security Depositories (CSDs) play a key role in settlement and undertake three main functions, including: first, certification, which is a record of fair and trustworthy maintenance of issued securities; second, settlement , that is, the ownership of the securities is transferred from the seller to the buyer; third, the account maintenance, that is, the establishment and update of the ownership record of the securities. Central securities registration agencies sometimes also perform functions such as securities custody, asset services, financing, reporting or securities lending.

In post-financial transaction settlement, a transaction involves multiple intermediaries. Each agency uses its own system to process, send and receive trade orders, check data, manage errors, and maintain its own transaction records. Moreover, the data standards used by each intermediary are also not uniform. These will incur a lot of cost (Figure 16).

Figure 16: Post-financial transaction process

Figure 16: Post-financial transaction process

The blockchain application is used in post-financial transaction settlement, which mainly replaces the settlement and account maintenance functions of the central securities registration authority, and establishes and maintains shared, synchronized accounts, simplifying the transaction reconciliation process. Currently, the settlement industry discusses the introduction of private, restricted access blockchain systems in post-financial settlements. Each of the nodes plays a different role and has different permissions in reading the information on the blockchain, and a group of trusted participants assumes the verification function.

The benefits that blockchain may bring to post-financial settlement include: First, simplifying and automating post-trade settlement through distributed, simultaneous, and shared securities ownership records, reducing transaction reconciliation and data management costs; , shorten the time required for settlement and reduce the settlement risk exposure; third, because the transaction-related information is shared by both parties to the transaction, which can promote automatic liquidation; Fourth, shorten the chain of custody, so that investors can directly hold securities and reduce investors Legal, operational risk and intermediary costs; Fifth, good traceability and high transparency; sixth, decentralized, multi-backup can improve system security and compression resistance.

However, blockchain applications still face many challenges in post-financial settlement: First, how to implement delivery versus payment (DvP)? This requires the blockchain to process cash accounts simultaneously. Second, how to ensure the settlement finality? For example, the Bitcoin blockchain system can only guarantee the finality of the settlement in a probabilistic sense because of the possibility of bifurcation (although the probability tends to be 100% over time). Third, transaction matching and error management. Blockchains still face many obstacles in comparing data in different dimensions, handling contract mismatches and exceptions. Fourth, how to ensure the confidentiality of transaction information in the case of multiple parties participating in the verification. One option is for a trusted institution and both parties to participate in a transaction-related consensus mechanism. Another option is to distinguish between transaction data and verification required data. Zero-knowledge proofs (ZKPs) are also a possible solution. Fifth, operational-level issues include identity management, system scalability, and compatibility with existing processes and infrastructure.

The impact of the Token paradigm on the post-financial trading can be found in the 2017 Banking Payments and Market Infrastructure Committee (CPMI, formerly known as CPSS) Research Report on Distributed Bookkeeping in Payment, Clearing and Settlement: An Analytical Framework. The US DTCC company gave a specific design in a 2019 report (Figure 17).

Figure 17: DTCC design for the application of blockchain to post-financial transactions

Fourth, Libra's risk and supervision

1.Libra operating mechanism

Libra is a composite currency unit based on a basket of currencies. The Libra Alliance claims that Libra will have stability, low inflation, universal acceptance and fungibility. Libra's currency basket is expected to consist mainly of the US dollar, the euro, the pound and the yen. Libra prices are tied to the weighted average exchange rate of this basket of currencies, and although they do not anchor any single currency, they will still exhibit lower volatility.

The Libra release is based on a 100% legal currency reserve. These French currency reserves will be held by investment-level custodians around the world and will be invested in bank deposits and short-term government bonds. The investment income of the French currency reserve will be used to cover the operating costs of the system, ensure low transaction fees and dividends to early investors (the “Libra Alliance”). Libra users do not share the investment income of the French currency reserve.

The Libra Alliance will select a number of authorized resellers (primarily compliant banks and payment agencies). Authorized dealers can trade directly with the French currency reserve pool. Libra alliances, authorized dealers, and the French currency reserve pool link Libra prices to the weighted average exchange rate of a basket of currencies through a two-way exchange between Libra and French currency.

The Libra blockchain is part of the alliance chain. Libra plans to recruit 100 verification nodes early and support 1,000 transactions per second to cope with normal payment scenarios. The 100 verification nodes form the Libra Alliance and are registered as non-profit organizations in Geneva, Switzerland. Currently, Libra has recruited 28 verification nodes, including companies, non-profit organizations, multilateral organizations, and academic institutions located in different geographic regions. The governing body of the Libra Alliance is the Board of Directors, composed of member representatives, and each verification node can be assigned a representative. All decisions of the Libra Alliance will be made through the Board of Directors, and more than two-thirds of the members of a major policy or technical decision will be required to vote.

2. From a currency perspective Libra

As a synthetic currency unit based on a basket of currencies, Libra, like the IMF Special Drawing Rights, is a super-sovereign currency. Governor Zhou Xiaochuan has a profound explanation of the super-sovereign currency.

In the issuance process, Libra is based on 100% legal currency reserves. Libra has no currency creation function because it represents a basket of existing currencies. The only way to expand Libra's is to increase the French currency reserve. If Libra is widely circulated and Libra-based deposit and loan activities occur, is there a currency creation? We don't think so. This depends on whether the Libra loan-derived deposit (that is, the “50 Libra deposits from the company” at the bottom of Figure 18, which is part of the account paradigm, not the Token paradigm) is considered currency. But what is certain is that Libra represents a basket of currencies, there is no real monetary policy, and it is far from currency denationalization.

(The bank holds 100 Libras before the loan)

(The bank holds 100 Libras before the loan)

(After the bank lends 50 Libras to the company, it is still 100 Libras, held by banks and companies respectively)

(After the bank lends 50 Libras to the company, it is still 100 Libras, held by banks and companies respectively)

(After the company deposits 50 Libras to the bank, it is still 100 Libra)

(After the company deposits 50 Libras to the bank, it is still 100 Libra)

Figure 18: Libra-based deposit and loan activities

Libra has valuable storage capabilities. But because of the currency network effect and the fact that there are no Libra-denominated goods or services in reality, Libra's trading medium and pricing unit functions will be limited in the early stages of Libra's development. For example, consumers who use Libra to shop in a country may have to convert Libra to local currency during the payment process. This can affect payment efficiency and experience.

Libra can promote financial inclusion. According to the Libra Alliance, users have the physical conditions to own and use Libra by simply installing a Calibra digital wallet on their mobile phone. Libra's transaction fees are low. Libra Alliance members have a rich industry background and a deeper understanding of user needs, helping to embed Libra flexibly into many aspects of user life and improving the convenience of users using Libra.

In the lower right area of Table 6 of Libra ("Private Issues + Retail"), there have been many stable cryptocurrencies (such as USDC). These stable cryptocurrencies are mainly used in cryptocurrency exchanges and do not really enter the daily lives of ordinary people. Whether Libra can become a real payment tool remains to be tested by the market. One limitation that cannot be ignored is the performance of the Libra Alliance chain. 1000 transactions per second certainly cannot support the daily payment needs of hundreds of millions of people. The Libra alliance chain has a plan to turn into a public chain. The public chain is more open, but its performance is more limited. Will Libra, like Figure 11, combine the account paradigm to circumvent the performance limitations of blockchains?

Finally, there are two issues worthy of attention: First, in countries with political economic instability and monetary policy failures (such as high inflation), can Libra replace the country's currency to achieve a similar "dollarization" effect? This can cause complex problems in monetary sovereignty. Second, with the passage of time, can Libra-denominated economic activities reach the size of a small economy, thus becoming the optimal currency area in a certain sense?

3. Libra's risk analysis

The Libra Alliance did not disclose the Libra currency basket rebalancing mechanism, the currency reserve pool management mechanism, and the two-way exchange mechanism between Libra and constituent currencies, making it difficult to accurately analyze Libra's market risk, liquidity risk and cross-border capital fluctuation risk. Once the relevant information is disclosed in detail, we can analyze the risks in these categories and evaluate the corresponding prudential regulatory requirements. At present, the following points are quite certain.

First, if the Libra coin reserve pool implements a more aggressive investment strategy for the pursuit of investment income (such as a high proportion of investments in high-risk, long-term or low-liquidity assets), when Libra faces concentrated, large redemption, the French currency reserve Pools may not have enough high liquidity assets to deal with. The Libra Alliance may have to "fire the sale" of the French currency reserve assets. This can lead to pressure on asset prices and worsen the liquidity and even liquidity of Libra systems. Libra does not have the support of the final lender of the central bank. If Libra is large enough, Libra runs may trigger systemic financial risks. As a result, Libra's currency reserves will be prudently regulated as a requirement for bond type, credit rating, maturity, liquidity and concentration.

Second, Libra's legal currency reserves are held by investment institutions that are located around the world and have investment grades. However, investment grade does not mean zero risk, and Libra's chosen custodian should meet certain regulatory requirements. If the Libra currency reserve custodian includes one or more central banks, then Libra is equivalent to implementing “synthetic CBDC”.

Third, Libra naturally has cross-border payment capabilities, and Libra's use will be cross-border, cross-currency and cross-financial. Libra will have a complex impact on cross-border capital flows and will be prudently regulated for this risk.

Fourth, if Libra-based deposit and loan activities are accompanied by currency creation (see above), Libra should be regulated accordingly for its impact on monetary policy enforcement.

Finally, it should be noted that although the Libra Alliance is not yet able to analyze Libra's price volatility risk, it is one of the biggest challenges Libra will face. When Token carries assets, the relationship between Token price and asset value is guaranteed by market arbitrage mechanism, and the premise of market arbitrage mechanism is three rules: issue rules, two-way exchange rules and trusted rules. Among the three rules, the most difficult thing for Libra to satisfy is the 1:1 two-way redemption rule. Libra authorized dealers do not necessarily use a basket of currencies when trading with the French currency reserve pool, and may only trade Libra in a constituent currency. In this way, the currency composition of the French currency reserve pool will gradually deviate from the initially set ratio. The strength of the constituent currency exchange rates may be further magnified, which may cause Libra prices to show significant fluctuations. Libra price fluctuations may trigger complex arbitrage activities between Libra and constituent currencies. These challenges stem from the arrangement in which Libra anchors a basket of currencies, and there is no CBDC or inter-financial settlement currency that anchors only a single currency.

4. Libra's compliance issues

Libra involves multi-country and multi-currency and meets the compliance requirements of relevant countries. For example, there is a regulatory framework for issuing stable cryptocurrencies in the US and the Eurozone, and these regulations will apply to Libra. For example, the USDC must meet at least the following compliance requirements: first, the US Treasury Department has a financial services business (MSB) license for the Financial Crimes Enforcement Network (FinCEN); second, operates a state-directed currency transfer license; third, the US dollar The reserve is to be deposited in a bank protected by the FDIC. Fourth, the authenticity and adequacy of the US dollar reserve are regularly audited and disclosed by third parties. Fifth, the provisions of KYC, AML and CFT. In particular, in the area of AML and CFT, the Financial Action Task Force (FATF, an international intergovernmental organization) released the Virtual Assets and Virtual Service Providers: A Guide to a Risk-Based Approach on June 21.

Gao Weijun's law firm has comprehensively combed Libra's compliance issues. First, according to Howey's test, will Libra be regarded as a kind of securities under US securities law? Second, if Libra is considered a virtual currency, the US Commodity Futures Trading Commission will likely have the authority to regulate fraud and manipulation. Third, because of the existence of the French currency reserve, Libra may be considered as a collective investment plan in the EU and subject to corresponding regulation. Fourth, data privacy protection issues related to Libra users and transactions. Fifth, taxation supervision issues.

V. Supervision of blockchain

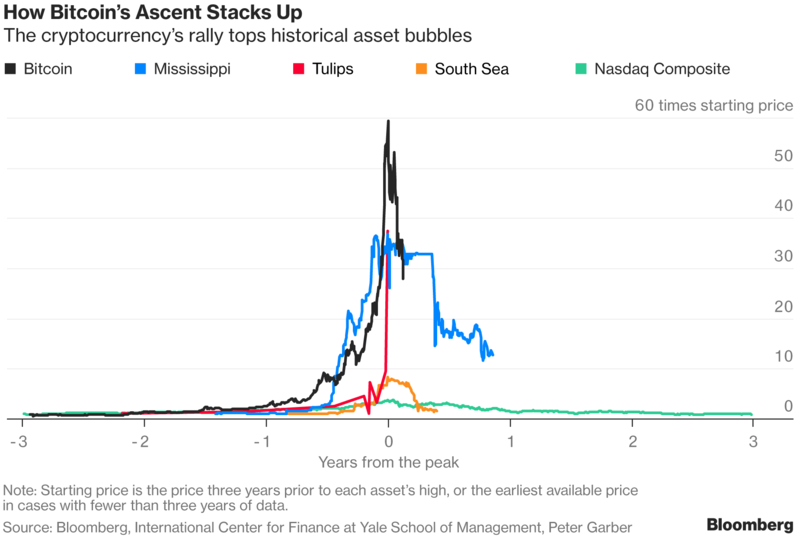

Cryptographic currency bubble

According to research by Convoy Investments in the United States, Bitcoin in 2017 may be one of the largest asset bubbles in history, measured by the speed and magnitude of price increases, surpassing the Mississippi bubble from 1718 to 1720 and 1719-1721 South Sea foam. The cryptocurrency represented by Bitcoin should be the first global asset bubble, and many individuals and groups of irrational behaviors in behavioral finance research can be observed in the cryptocurrency market. Figure 19 from Bloomberg compares bitcoin with other asset bubbles in history.

Figure 19: Bitcoin and other asset bubbles in history

Figure 19: Bitcoin and other asset bubbles in history

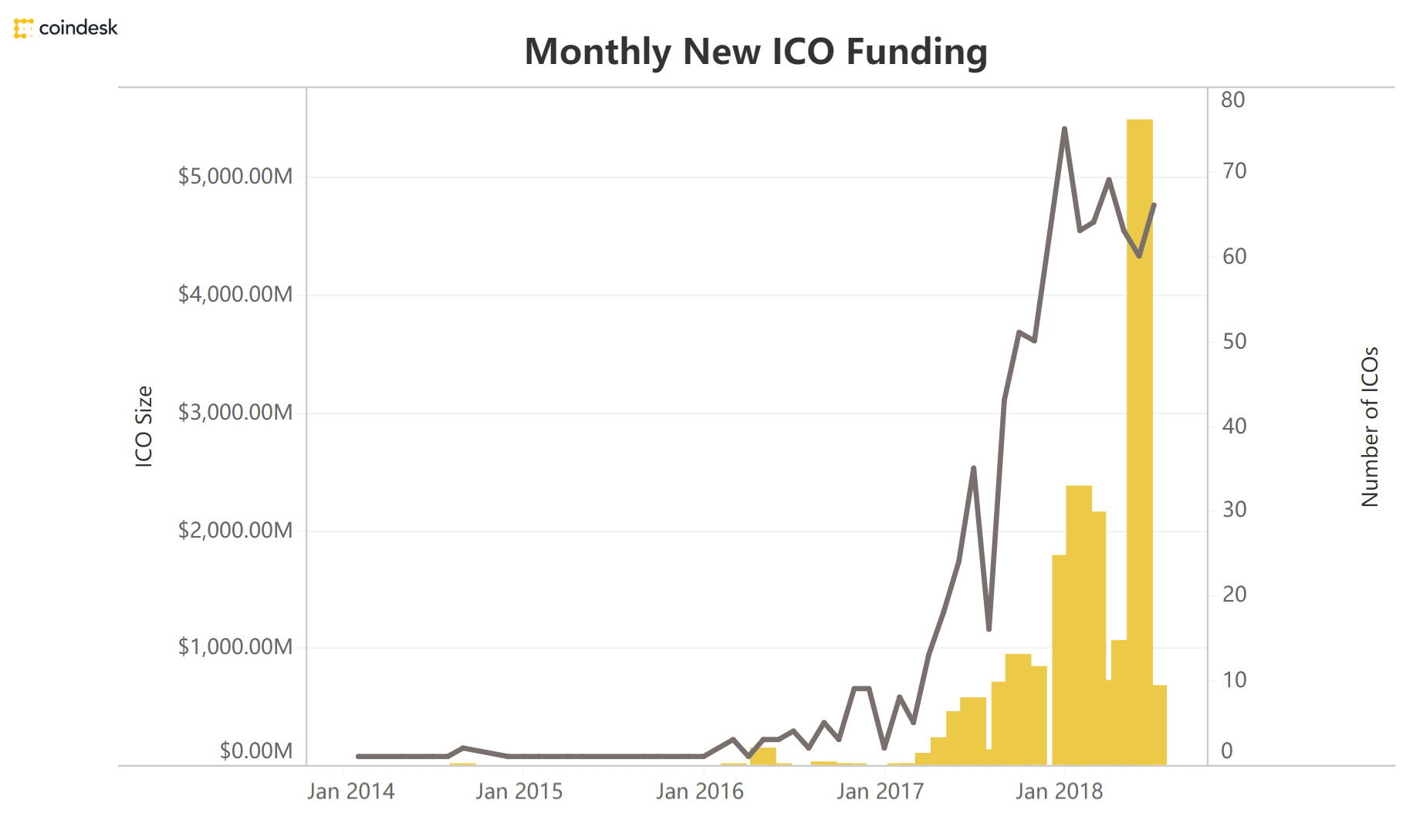

The blockchain project has two financing channels: equity financing and ICO. The cryptocurrency bubble is also reflected in the 2017 ICO madness (Figure 20). After 2018, with regulatory tightening and market return to rationality, ICO madness has faded.

Figure 20: ICO Mania

Figure 20: ICO Mania

2. ICO ubiquitous problems

First, the economic connotation of the tokens that ICO gives to investors is unclear. In theory, tokens have three possible connotations: (1) trading medium; (2) equity notes in the sense of balance sheets, ICOs that issue such tokens are close to equity crowdfunding; and (3) obtain evidence of goods or services, The ICO that issued this token is close to commodity crowdfunding. Many tokens have multiple connotations, it is difficult to value them, and the corresponding ICO has the characteristics of commodity crowdfunding and equity crowdfunding. However, many tokens directly enter the hype when the economic connotation is not fully revealed or discussed.

Second, the problem of token speculation after ICO. Unlike crowdfunding, after many ICOs occur, tokens can have secondary market transactions, especially into cryptocurrency exchanges. In theory, if the token is a certificate of interest, goods or services, its valuation should be “anchored” to some fundamental factors. But in reality, many token prices have been speculated to levels well above the fundamentals. Some tokens have been speculated even during the pre-sale phase of the ICO (called presale or pre ICO). It is difficult for ICO to ensure investor suitability. The ICO project is at an early stage and the risks are very high. In theory, the ICO should be open to qualified investors with certain risk identification and affordability, as well as the amount of investment by qualified investors. But some ICO projects are actually open to the public through cryptocurrency exchanges.

Third, ICO distorts the incentives of the blockchain startup team. The secondary market of tokens allows the tokens held by the blockchain startup team to quickly have a monetization channel, and the blockchain entrepreneurship project may remain at the white paper stage. In contrast, in the venture capital industry, entrepreneurs spend much more time from getting venture capital investments to IPOs. ICO's rapid liquidation mechanism will distort the incentive mechanism of the blockchain startup team. Token holders are often in a vague position in the governance structure of blockchain entrepreneurship projects, and there is no effective measure to ensure that the entrepreneurial team is consistent with its own interests for a long time.

Finally, in the field of cryptocurrency, ICO forms a positive feedback mechanism between “central currency” such as Bitcoin and Ethereum and general tokens. ICO collects Bitcoin, Ethereum, etc., which will increase demand for Bitcoin, Ethereum, etc., and push up their prices. The price of Bitcoin, Ethereum, etc., often becomes the token of ICO issued. Value benchmark. In this way, a mutually positive positive feedback mechanism is formed between Bitcoin, Ethereum, etc. and the general token. This is an important reason for the general increase in cryptocurrency prices in 2017. However, after the price of Bitcoin and Ethereum entered the downtrend channel in 2018, this positive feedback mechanism will also accelerate the price of the general token.

3. Encrypted currency regulation

(1) Production links and primary markets

First of all, the production of POW-type cryptocurrency represented by bitcoin requires a large amount of electric energy, which is controversial in many countries. Second, as mentioned earlier, many ICO projects are suspected of illegal securities activities. Securities regulation has become a core regulatory issue related to the blockchain, reflecting the discussion of STO and ATS after 2018.

(2) Circulation and secondary markets

The cryptocurrency faces many outstanding problems in the circulation and secondary markets. First, the lack of appropriateness of investors. Some cryptocurrency exchanges have essentially no investor suitability checks for account holders. Second, the problem of market manipulation. Many cryptocurrencies are very concentrated. For example, about 40% of Bitcoin is held by 1,000 people, and the “pre-drilling” mechanism of ICO and forked coins also causes the centralization of these tokens. In addition, cryptocurrency exchanges do not have an information disclosure system like a stock exchange, making market manipulation possible. There has been a lot of empirical research in this area. Third, hacking attacks on cryptocurrency exchanges, theft of client assets and even bankruptcy have occurred many times. Fourth, if a cryptocurrency exchange participates in POS mining (known as the staking pool), it will conduct a term conversion or liquidity conversion similar to that of a commercial bank. On the debt side, the cryptocurrency exchange gives investors the IOUs that can be withdrawn at any time, similar to demand deposits. On the asset side, the cryptocurrency involved in POS mining needs to be locked for a certain period of time and can obtain mining revenue, similar to bank loans. If the POS mining business of the cryptocurrency exchange is large enough, in the face of investor concentration and large cash withdrawals, the cryptocurrency exchange may not have enough liquidity cryptocurrency to deal with the withdrawal. Fifth, because of the anonymity of cryptocurrencies, they are related to illegal transactions or gray transactions from the beginning. The early "Silk Road" website is a typical example.

Correspondingly, the regulatory measures include: first, the requirements for cryptocurrency wallet, exchange “know your customer” (KYC), anti-money laundering and counter-terrorism financing; second, taxation on cryptocurrency transactions; third, investors are appropriate Sexual requirements; Fourth, combat fraud and market manipulation; Fifth, the exchange of cryptocurrency and statutory activities; and sixth, the issue of global regulatory coordination.

Source: Chain smell

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Breaking the "7" on the CNY, the BTC is rising, is it an inevitable cause and effect, or is it an accidental coincidence?

- Bitcoin and gold are opening their hearts this week, and the RMB exchange rate has fallen back 10 years ago.

- Canada: Blockchain technology is at the core of the government's new policy, with 51% of companies investing

- Libra wants ICO? Be wary: Beware of the scam of the Libra hotspot

- After excavating a large block of 210 MB, the BSV suddenly appeared in the "three-chain separation" situation.

- Getting started with blockchain | Exchange's official smart brick arbitrage? Is money really so profitable?

- Wright halved, mining machine washing, the whole network computing power is expected to be reduced by 20% -30%