2019 Dapp Market Report · Ecology: Ethereum is the most popular, EOS opened higher and lower

Dapp (Decentralized Application), which is the decentralized application, is the most important part of the large-scale implementation of blockchain technology. It is also an important indicator for evaluating the use of a public chain and infrastructure. DappReview has been committed to digging data for the industry. Provide valuable insights and industry trend analysis. We put together this year's observations and reflections and compiled this "2019 Blockchain Application Market Report". This annual report will focus on the following aspects:

-

Development status of the Dapp ecology of each public chain -

Observation and analysis of hot spots such as DeFi, NFT, and blockchain games -

Data-based industry insights and outlook for 2020

Full year overview

In 2019, the entire Dapp industry continued to flourish. DappReview added 1,955 new Dapps throughout the year. The total number of Dapps reached 4,087, and the total on-chain transaction volume reached 23.6 billion U.S. dollars. In terms of user scale, although it is far from being comparable to centralized applications, if the vertical comparison is made, the Dapp industry has still gained a certain number of incremental users. More and more teams and individuals have entered the game, which has also brought brand-new blood to the industry. Over the past year, the Dapp industry has emerged a series of breakthrough innovations in the fields of finance, NFT and games.

- Dry Goods | Security and Scalability in Commission-Based Sharded Blockchain

- Hangzhou Blockchain Industry and Park Development Report: 1,611 registered blockchain companies, layout of 6 major blockchain industrial parks

- Regarding cryptocurrency, these 11 points are the truth, but they are also very controversial

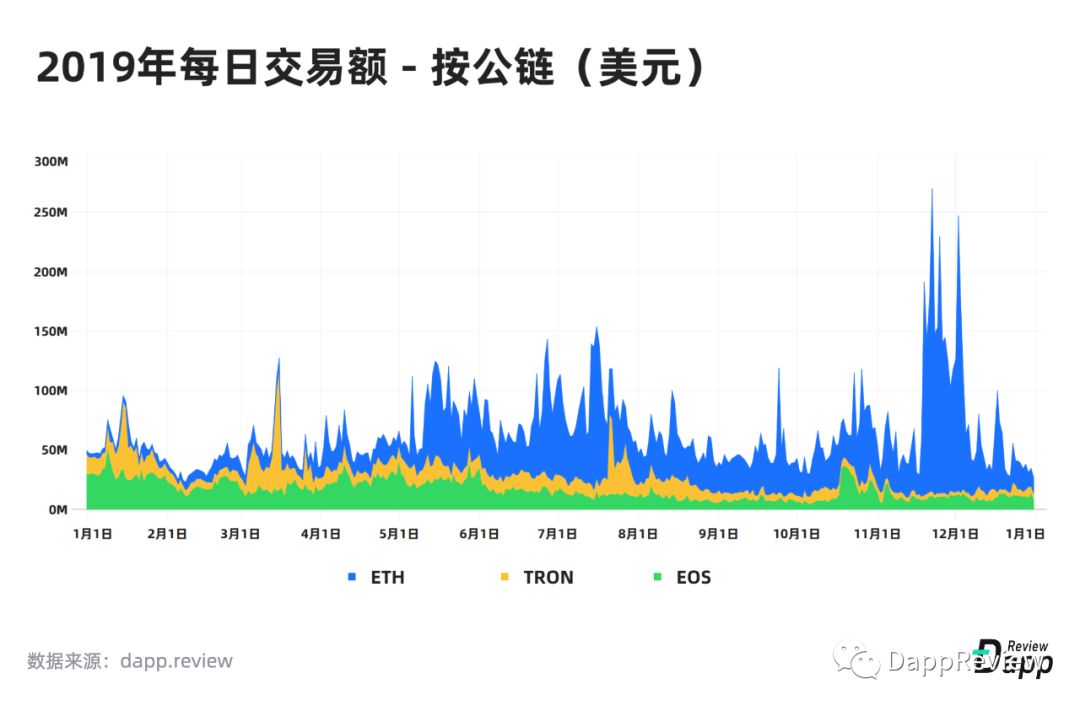

As the first large-scale application of a smart contract platform, Ethereum's leading position in the Dapp field is still difficult to shake. In 2018, TRON and EOS, which have been launched on the main network in succession, also maintained a good momentum of development. At present, these three major public chain transactions account for more than 98.55% of the Dapp market, forming an oligopoly situation. Starting in 2019, a series of newly launched public chains have been working hard to develop the Dapp ecosystem. In addition to Ethereum, Tron, and EOS, DappReview also tracks 9 other public chains, which have contributed a total of 354 Dapps.

This report will focus on the three major Dapp ecosystems of Ethereum, Tron, and EOS. The remaining public chains are relatively insignificant, and strive to highlight the key points.

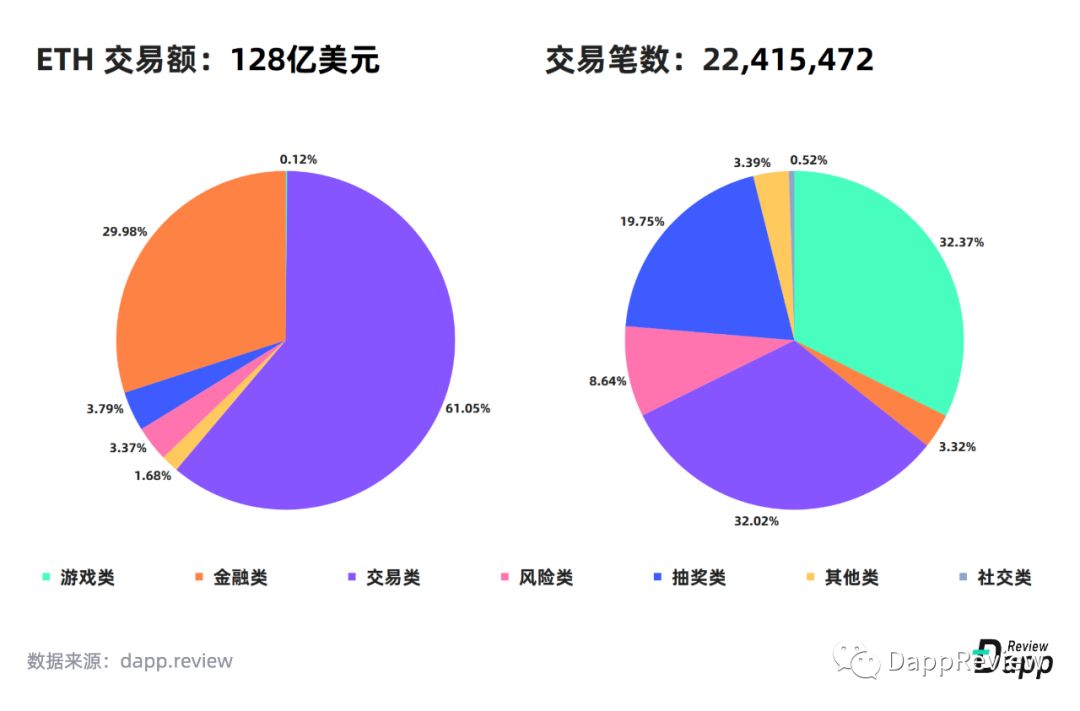

In the first half of 2019, the transaction volume on TRON and EOS was mainly contributed by lottery and risky Dapps. With the market becoming colder in the second half of the year, the speculative desire of a large number of users has decreased, and a single ecology has led to a continuous decline in Dapp transactions on these two main chains. In early 2019, DeFi began to become the main value manifestation on the Ethereum network. Relying on a series of projects built around DAI, Ethereum ushered in the explosion of DeFi. If you include the ERC-20 token transaction value, Ethereum's annual Dapp transaction value has reached $ 12.8 billion, exceeding the total of EOS ($ 6.1 billion) and Tron ($ 4.4 billion).

Ethereum

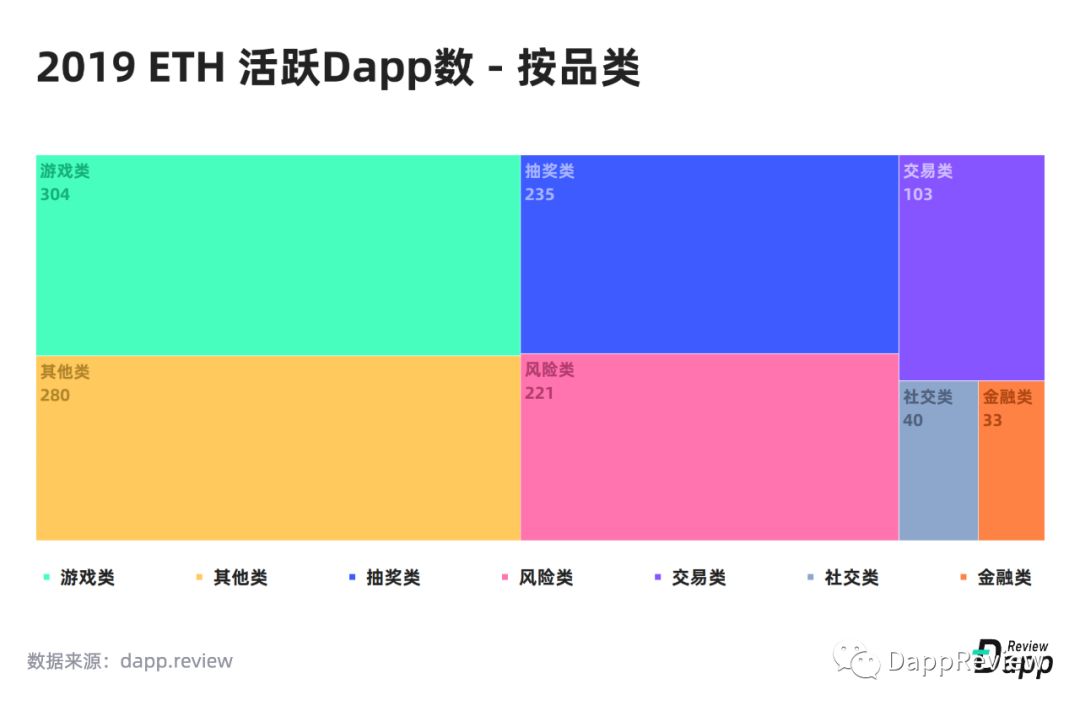

Ethereum has the most diverse Dapp ecosystem and has always been the Dapp development platform preferred by developers. Of the 2,146 Ethereum Dapps included in DappReview, 1,223 are still active in 2019.

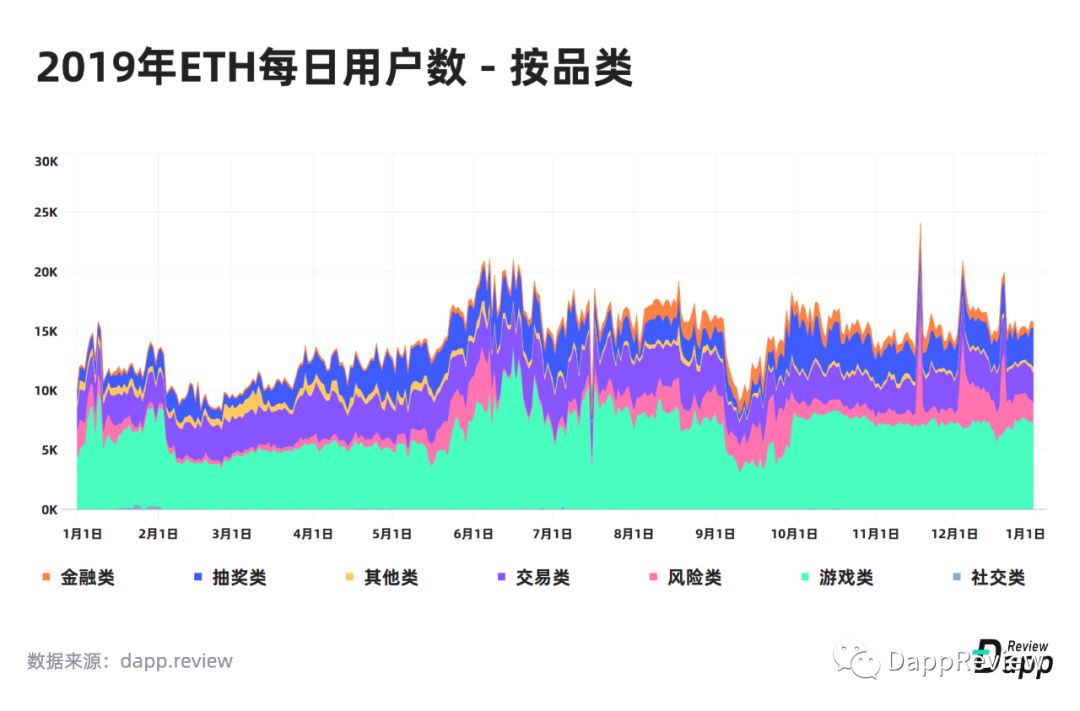

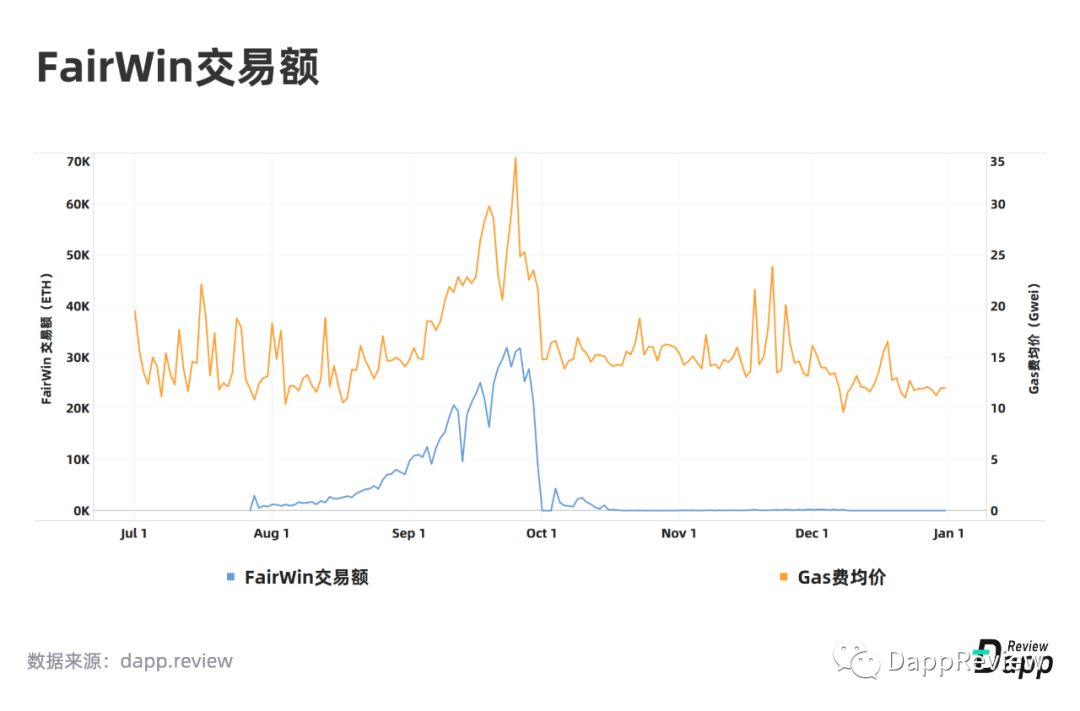

From the perspective of Dapp category distribution and daily active user distribution, Ethereum has fully demonstrated its ecological diversity. Among them, there are the most game users, accounting for 46.5%, and the number of users of decentralized exchanges (trading) is second, accounting for 20.9%. Risky Dapps are special, and the number of players is not stable. With the rise and collapse of Dapps, there will be drastic fluctuations in a short period of time. Take Fairwin as an example. During the active period of the project, more than 3,000 players participated every day. After the crash, users only had single digits. In addition, its game mechanism also caused a significant increase in Ethereum Gas Fee, which indirectly affected the active number of other Dapp users. The decline in Ethereum user numbers in September was caused by Fairwin. Although financial Dapps have not many users, the value of each transaction is very high.

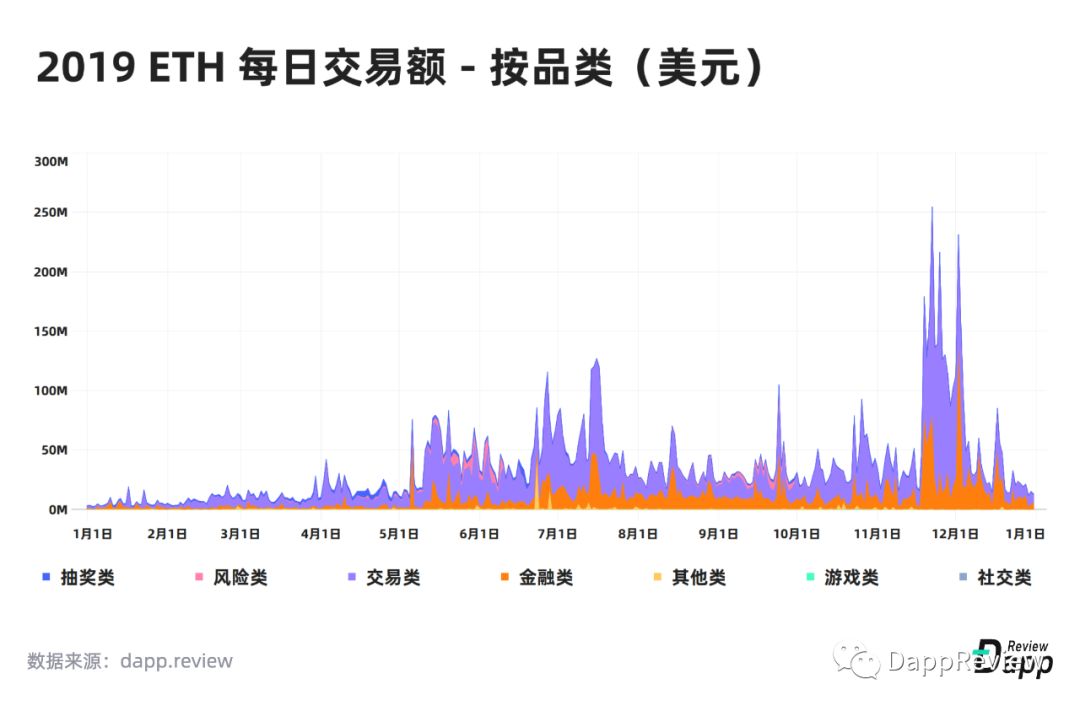

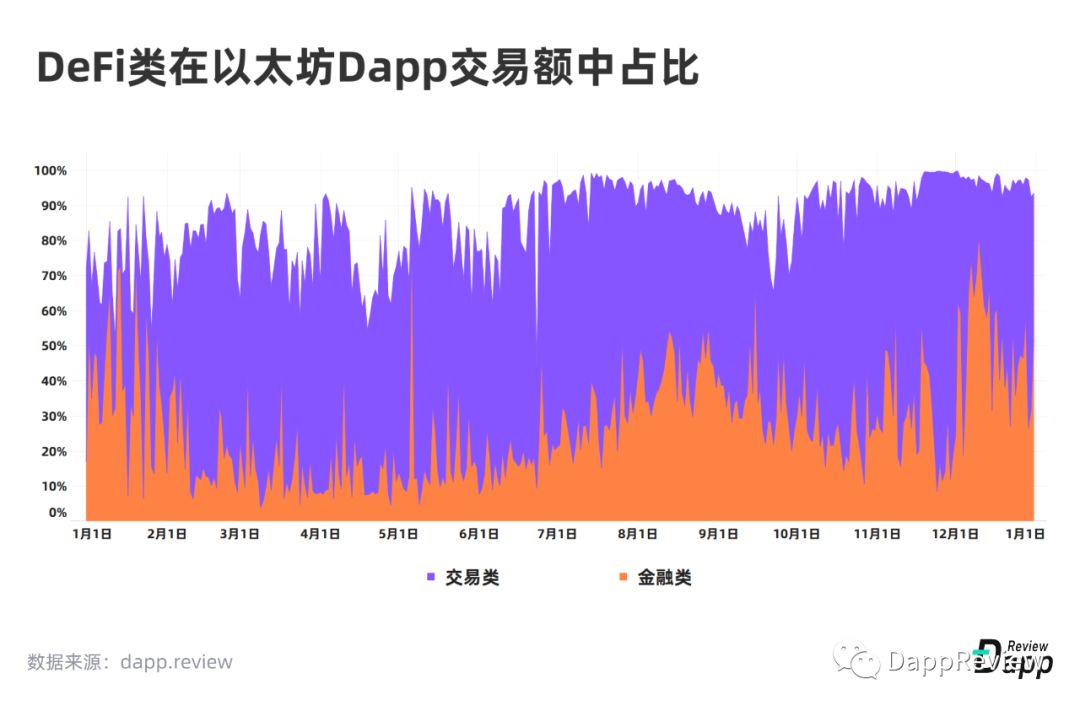

In 2019, the total transaction volume of Ethereum is about US $ 12.8 billion, and the transaction volume of DeFi (transaction + financial) applications accounts for more than 90%. Among them, transaction Dapp and financial Dapp contributed 61.05% and 29.98% of the transaction amount, respectively.

Although the game Dapp has the most users, the proportion of transaction value is not high. The reason is that on the one hand, transactions in the game may not necessarily involve the transfer of assets; on the other hand, many game assets exist in the form of NFT, and NFT transactions are mainly on decentralized exchanges such as Opensea Rather than in-game.

game

For a long time, games have been regarded as one of the best landing scenarios on the blockchain. Since the great success of CryptoKitties, more and more developers and game teams have entered the market, trying to make more interesting attempts in the game section. In 2019, many excellent blockchain game teams have won the favor of capital:

Most of them use Ethereum as their main position for blockchain game development. How should games be combined with blockchain? The answers given by the development team vary. Some teams choose to chain the gameplay mechanism of the game and interact with users in the form of smart contracts , such as CryptoKitties, Axie Infinity, MyCryptoHero, etc. Under this scheme, limited by the performance of Ethereum and the threshold of the blockchain, compared with traditional games, the user experience is poor, and only users who are familiar with the blockchain can easily get started. In order to ensure the smooth experience of the game, other game teams usually only put the assets in the game in the form of NFT (Non-Fungible Token, non-homogeneous tokens), and the core gameplay of the game is all off-chain . Such as GodsUnchained, SkyWeaver and so on.

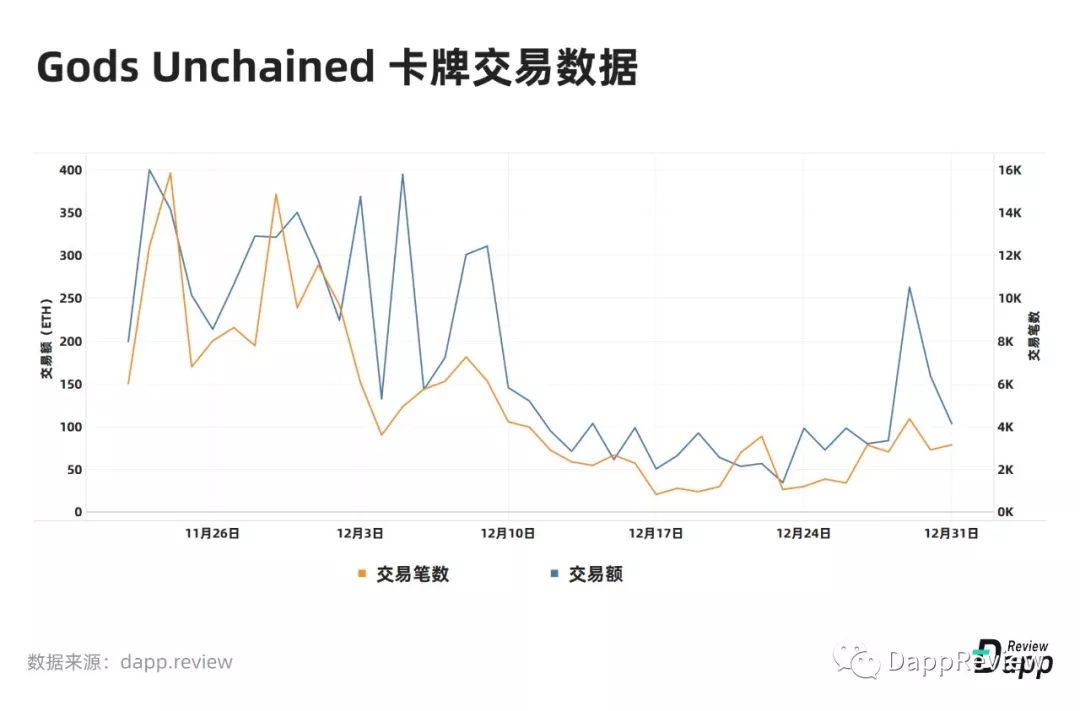

Last November, GodsUnchained, which had been pre-sold for more than a year, finally issued card ERC-721 tokens to players, and subsequently opened the card trading market. By the end of the year, a total of 203,000 card transactions had occurred, with a transaction value of USD 1.03 million. The first two weeks of card trading opening were peak trading hours, and then began to decline, and did not pick up until the end of December. Two mythological cards Atlas and Prometheus were sold on Opensea on December 8th and December 10th for 210ETH and 235ETH, respectively.

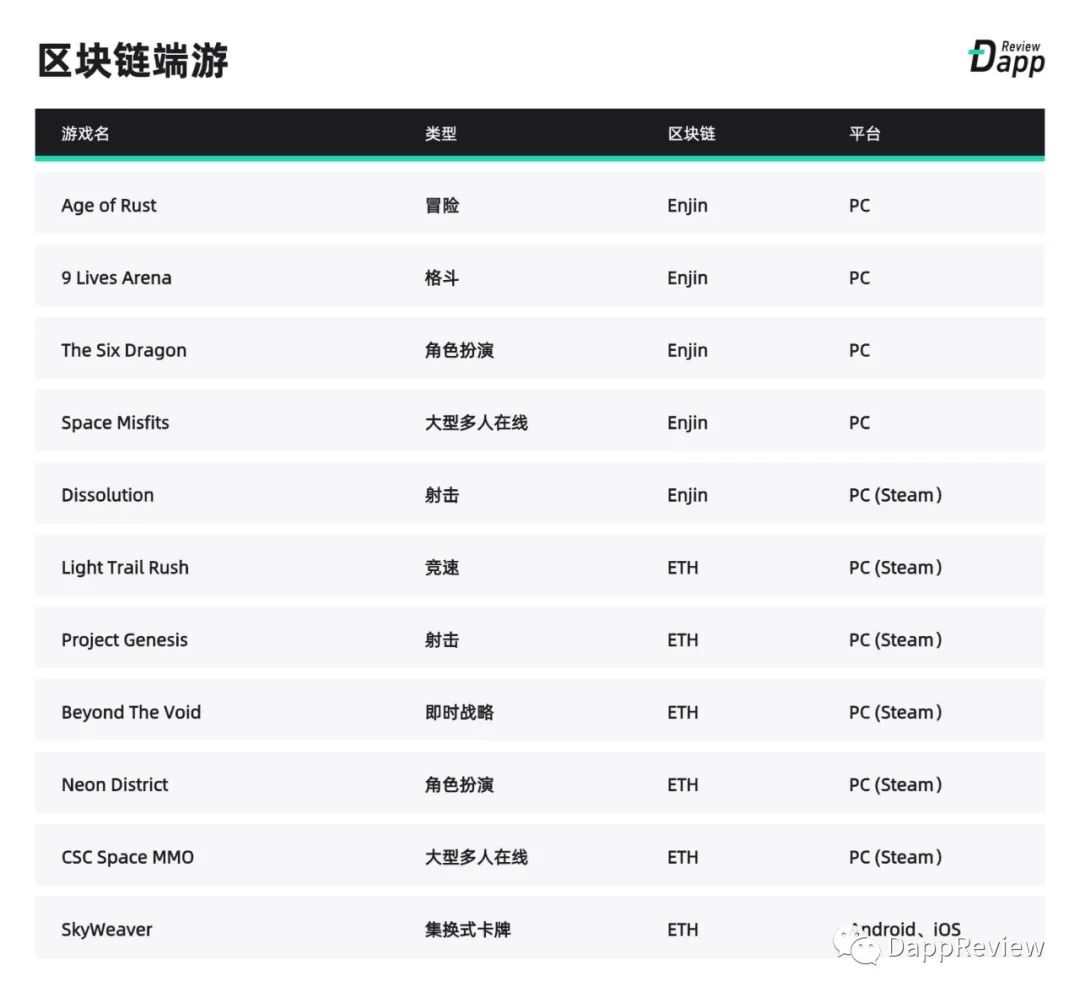

After more than a year of development, the overall quality of blockchain games has improved significantly. The most direct manifestation is that there are more and more cross-platform games. In 2018, almost all Dapps were only available in web versions. By 2019, the number of game-based Dapps that launch native mobile apps has begun to increase. There are also many teams that have launched computer client versions. Blockchain games represented by Light Trail Rush have even logged in to the Steam game platform.

Most web-based blockchain games are limited to role-playing, card, and collection types, while mobile- and computer-side blockchain game types are more abundant, including first-person shooting, real-time strategy, role-playing, and large-scale multiplayer online. , Racing, fighting and many other types of games. Compared to page games, the advantages of end games are very fast, high speed, high picture quality, and diversified gameplay. In the future, the end game of integrated blockchain will be the general trend, and within a few years we are likely to witness the advent of an AAA blockchain game.

NFT

Games such as CryptoKitties and GodsUnchained use NFT based on the ERC-721 standard. On June 18 last year, ERC-1155 proposed by Enjin officially became the official Ethereum token standard. The standard has many new features and is more suitable for game props from a design perspective. For example, users can package multiple tokens and send multiple tokens to one or more recipients through only one transaction, which can effectively reduce Gas costs. A more interesting mechanism is that when NFT (or FT) is minted, ENJ tokens can be pledged and the intrinsic value (or production cost) of NFT is injected. ENJ tokens are equivalent to raw materials, just like we forged a knife, Can't do without metals.

DappReview believes that the core value of NFT comes from the value of its use scenarios and the premium brought by brand endorsement. The many advantages that the blockchain gives to NFT, such as immutability, true ownership, etc., are just inherent attributes of NFT.

The value of NFT = intrinsic value + use case value + brand premium + blockchain enablement value

At present, there are more than 48 million FT and NFTs cast using ENJ, and a total of more than 9 million ENJ tokens (valued at 700,000 US dollars) have been locked up.

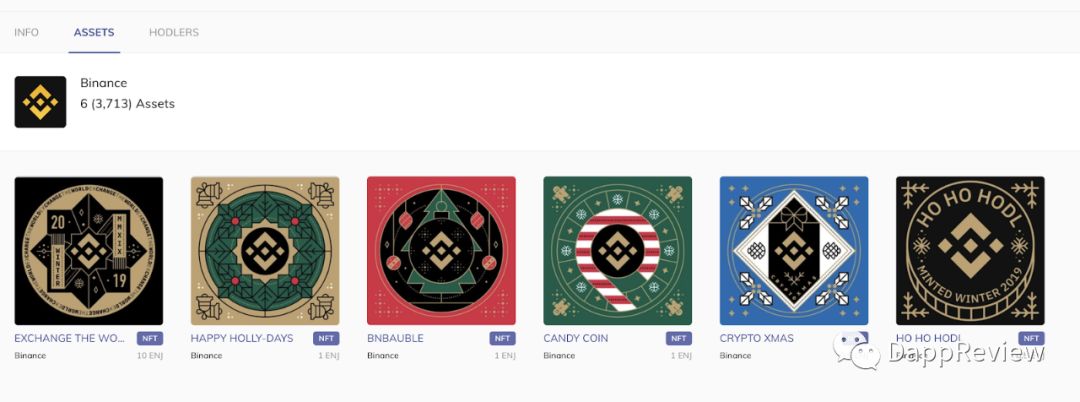

It is worth mentioning that in December last year, Binance issued a series of limited collections NFT based on ERC-1155, which became the most active asset in recent trading. These NFT lockup ENJ tokens are only 0.5 ENJ, and the average transaction price is between 100-200 US dollars, up to 20,000 ENJ (about 1570 US dollars). It can be seen that Binance ’s brand premium and scarcity bring its NFT A strong price support.

High Risk-Fairwin

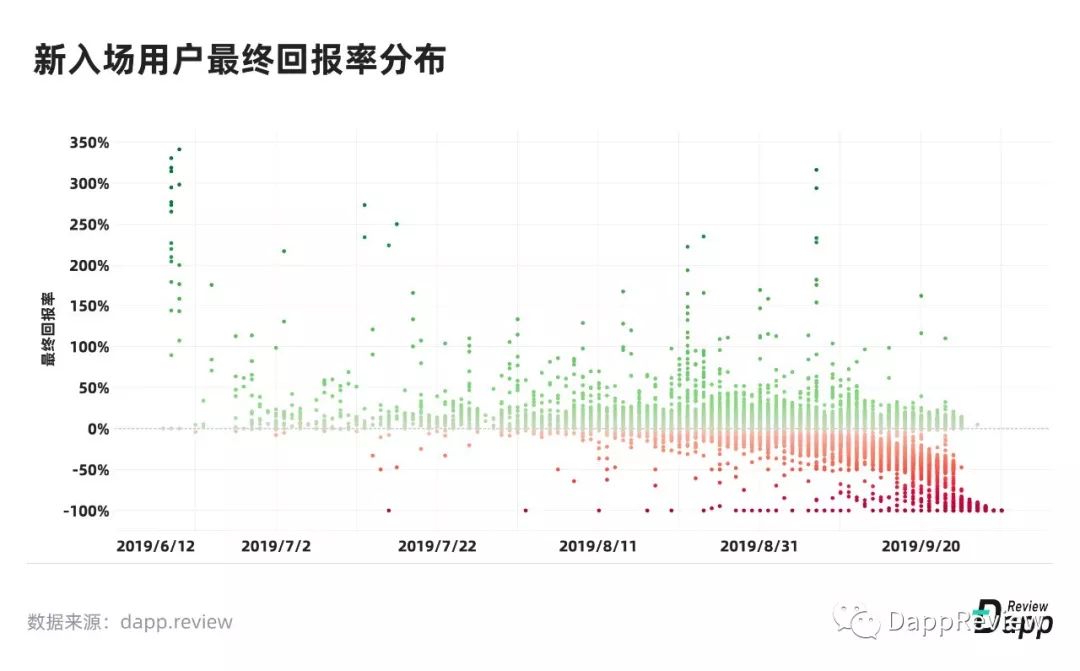

High-risk Dapps have always been a sensitive topic in the industry, including various types of funds. But we must admit that this category of Dapp has always maintained a high level of user engagement, and players are here to dance with greed and fear. Taking Fairwin as an example, this is an obvious Ponzi scheme. However, before its crash, a total of 19,028 addresses participated in the game, with a total transaction value of more than 690,000 ETH, and contributed nearly 9,000 ETH Gas Fee to Ethereum.

The purpose of most users participating in Fairwin is to speculate and try to earn more tokens, but what is the result?

- 8,316 addresses have positive returns, with an average yield of 12.94%, earning an average of 8.32ETH

- The return of 10,129 addresses is negative, the average yield is -47.59%, and the average loss is 9.57ETH

- 763 addresses do not lose or make money, just recover the principal

The developer of the project charged a 4% commission and made a total profit of 27,785 ETH.

DeFi

This section is provided by Binance Research Institute (Etienne), which launched a series of comprehensive and insightful reports on decentralized finance ("DeFi Series") in June last year.

The following content is from the third report, which discusses the latest developments and important narratives in the field of DeFi. For the full version of the report, read the report from Binance Research.

https://research.binance.com/

DeFi includes (decentralized) transaction services and financial applications such as lending markets, asset management services, and payment solutions.

In 2019, the price of ETH fluctuated between $ 100 and $ 350, with a median price of $ 173. So far, regardless of its price, most decentralized financial ecosystems are built on Ethereum.

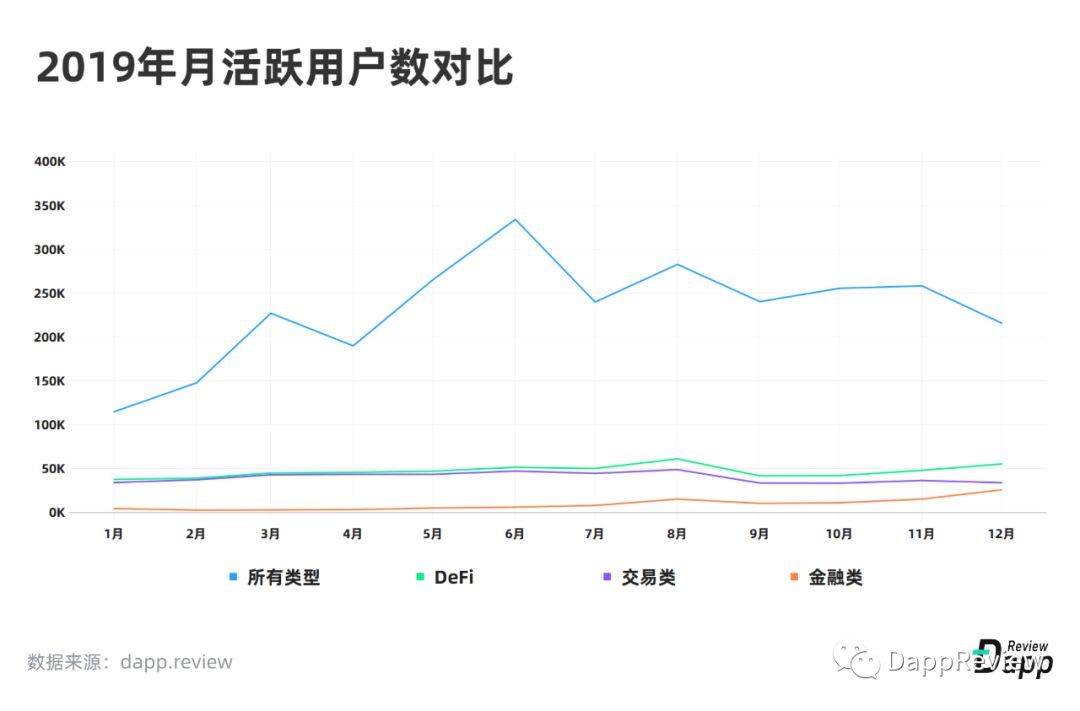

In January 2019, the number of monthly unique users of decentralized exchanges was 34,244, and financial applications were 4,649.

The number of users on the decentralized exchange has increased, reaching a peak of 48,934 in August 2019, and then falling back to the initial level, with 34,033 users in December.

On the other hand, the number of users of financial applications has been increasing since January. In August, the monthly users exceeded 10,000. In December, there were a total of 25,925 users of decentralized financial applications on Ethereum.

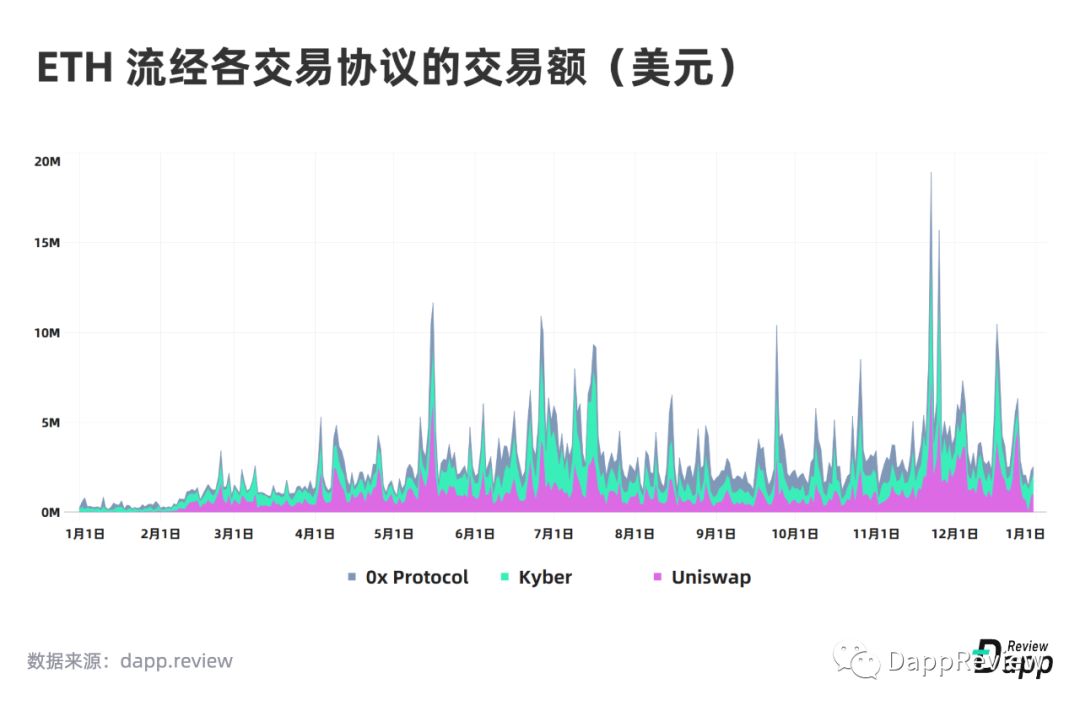

The number of users of the decentralized exchange "2.0" has also increased. Uniswap is used by 19,000 users and the total transaction value for the year is $ 390 million. Similarly, Kyber is used by more than 35,000 users with an annual transaction value of $ 387 million.

The chart represents all on-chain activity, which may include some exchanges that are not fully decentralized (such as IDEX). As shown in the figure above, more than 90% of all on-chain transaction volume of Ethereum-based Dapps come from DeFi-related applications: From the perspective of users, DeFi has been the driving force for Ethereum growth in 2019.

In short, Ethereum and DeFi have become "two-headed monsters", leading the pace of their further development.

Although DeFi represents only a small part of the crypto industry, it is one of the most dynamic of them.

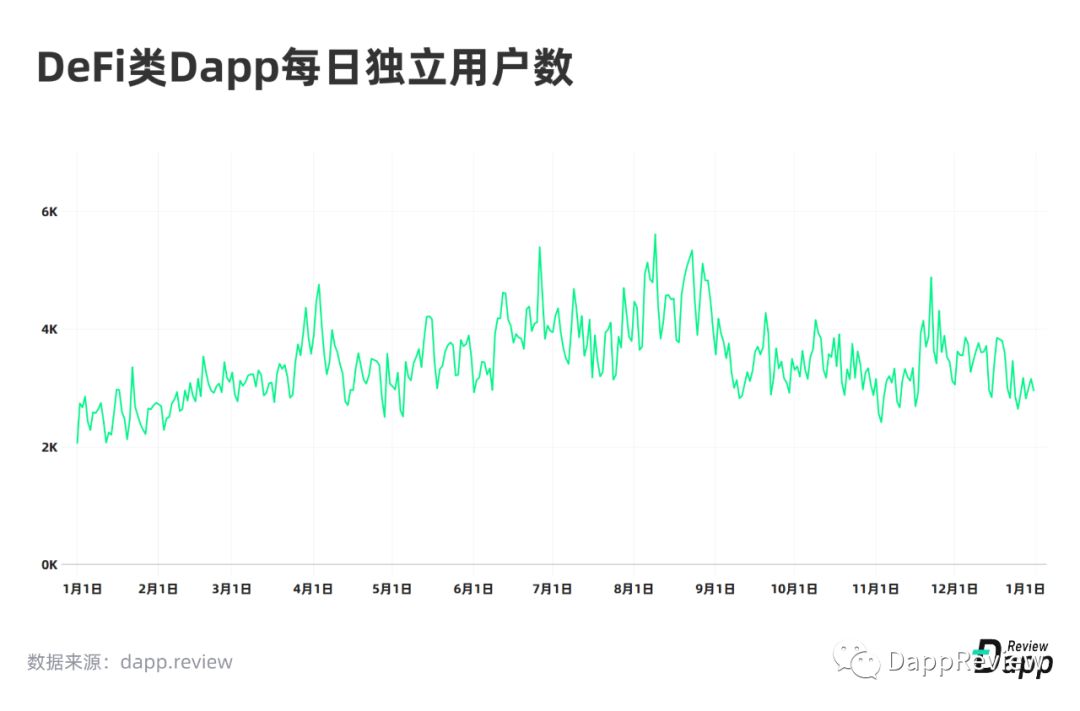

In 2019, the average daily independent users of the DeFi platform based on Ethereum is 3,456.

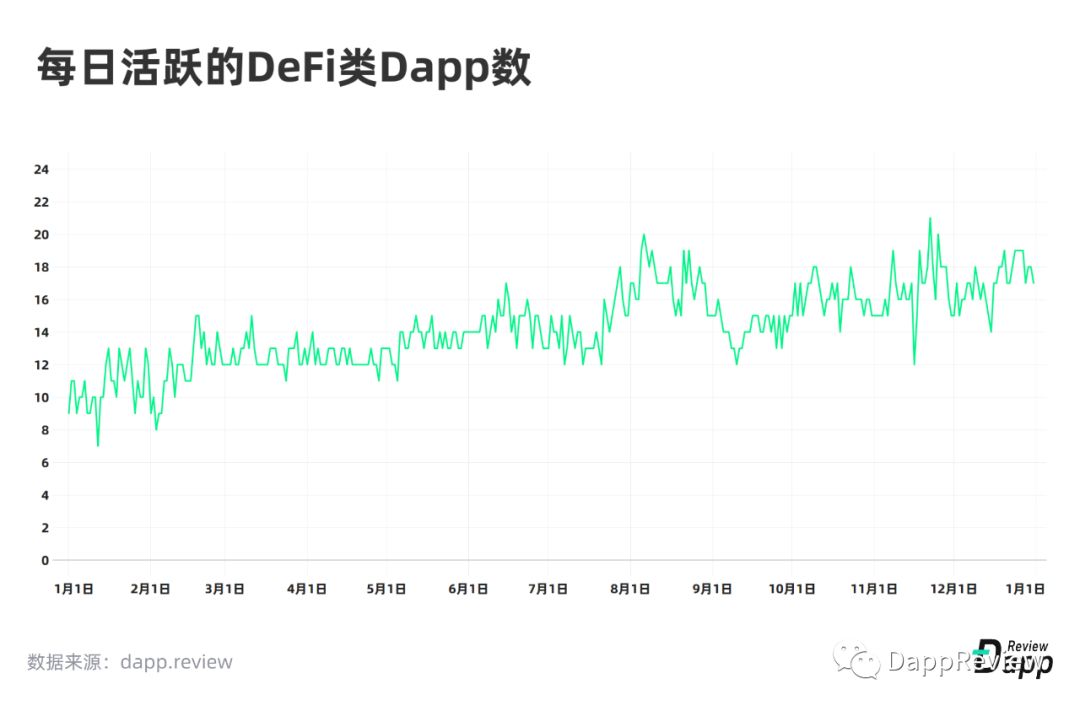

The number of active projects (defined as those with more than 50 unique users per day) nearly doubled in 2019. However, the absolute number is still small, with fewer than 20 projects.

In addition, DeFi is still small in the crypto world. For example, the total value of collateral locked in Staking products is much higher, about $ 6 billion, more than five times higher than the total value of collateral in DeFi.

Finally, the size of DeFi is still negligible compared to the (traditional) fixed income market. The latest estimate of the total size of the debt market in 2019 is approximately $ 250 trillion. In the United States alone, consumer loans in 2019 are estimated at approximately $ 1.6 trillion.

In 2020, we expect the Ethereum platform DeFi to have these trends:

-

Maker's dominance will come to an end : we expect Compound to have the opportunity to surpass Maker in terms of transaction volume and hedging amount . Synthetix also has the potential to challenge Maker because it has great flexibility in compositing assets. But Synthetix also has a hidden danger, that is, the liquidity of its core collateral SNX is worrying. In comparison, Maker's collateral (ETH and BAT) has better liquidity. -

Maker's DSR integration : Although MakerDAO's dominance may be challenged, it will still be the backbone of the DeFi field. After a major update at the end of the year, Maker brought DSR (Dai Savings Rate) integration and multi-collateral Dai. ETH and BAT became the first mortgage assets of multi-collateral Dai. At the same time DSR may become one of the most important interest rates in the DeFi field . For example, Fulcrum has integrated DSR into its platform, and exchanges that support Dai trading pairs will also integrate this interest rate into their own platforms. -

Borrowing solutions beyond over-collateralization: As we mentioned in our first DeFi report, over-collateralization does not help those who do not have a bank account. So we are exploring some early solutions other than over-collateralization, they include: social fund recovery, credit scoring system, zero proof, credit market DAO and so on. We also expect that one day the DeFi project will be able to borrow like a credit card, allowing users to use future expected cash flows as a promise . Sablier, an experiment on Ethereum that uses smart contracts to automatically pay, can pave the way for related proprietary protocols. In early 2020, Aave (LEND) will migrate its lending market to the main network and launch a new loan product, Flash Loans, that does not require over-collateralization. -

More DeFi derivatives will be born on the Ethereum mainnet : The Convexity protocol and some other platforms (such as the UMA protocol) will bring more trading opportunities to the DeFi field. But from the perspective of option underwriters, many people are worried about risk control and rewards. Not to mention that there are synthetic assets like SwanDai that track the price deviation between DAI and the anchor price (one dollar) in an index form, which will also be launched on the main network. -

USDT: As USDT migrates to the Ethereum platform on a large scale, it can be expected that USDT will also be integrated into various DeFis in the near future . USDT has already appeared in Compound's "next support currency" vote. - Increase of one-stop platforms: Platforms such as Zerion and InstaDApp are committed to reducing the threshold of DeFi use by creating a one-stop DeFi platform, and integrate multiple Defi platforms under the same UI . At the same time, protocol aggregators such as DeFiZap and Dex.ag will also attract some users, because they allow users to conduct transactions with the lowest gas fee, and because they integrate multiple platforms, users can easily put eggs in different Basket.

EOS

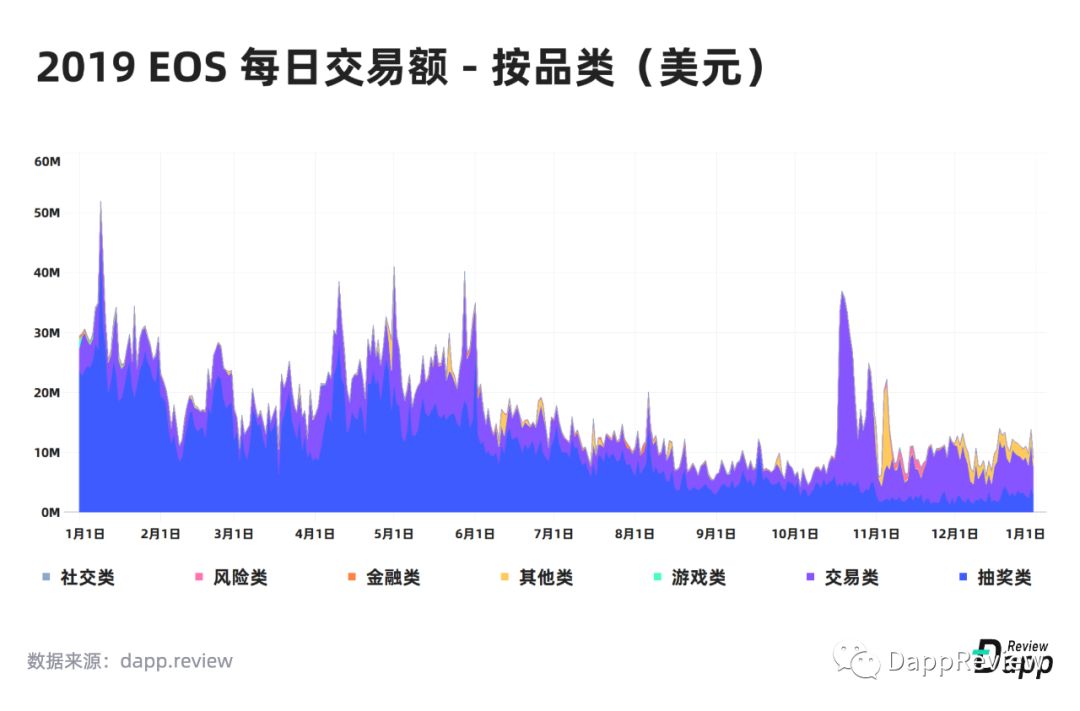

The performance of EOS throughout 2019 can be said to be "open high and go low."

At the beginning of 2019, the lottery Dapp on EOS has been popular for a while, so it has been "favored" by hackers. According to Chengdu Chainan statistics, as of early December 2019, there were over 60 typical attack events on the EOS public chain, with cumulative losses reaching hundreds of thousands of EOS. The first quarter was a concentrated outbreak period, mainly due to the security of Dapp contract code. Weakness, coupled with the continued popularity of lottery applications on the EOS public chain during this period, led to hackers conducting continuous attacks on the same vulnerability on multiple Dapps. The main methods were transaction blocking, rollback transaction attacks, counterfeit currency attacks, random number cracking, etc. .

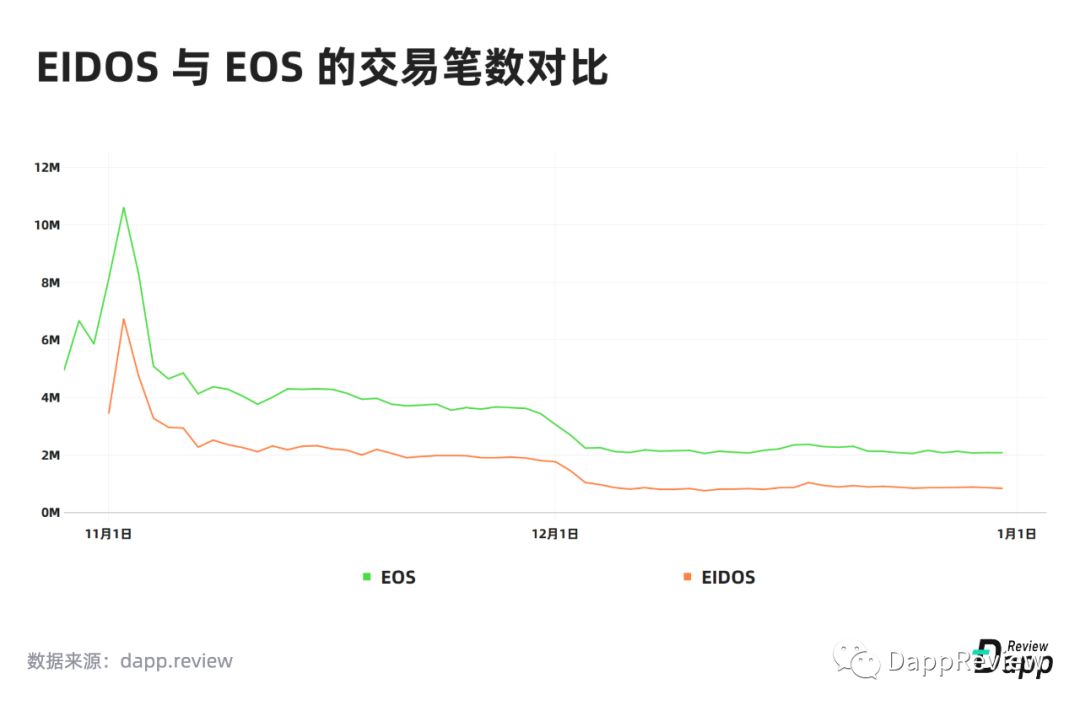

In the last quarter of 2019, after the EIDOS went online on November 1, it was almost alone to paralyze the entire EOS network. EIDOS is an airdrop token contract. Users only need to initiate any amount of transfer to their contract (minimum amount 0.0001EOS), and they can receive an airdrop reward. Under this mechanism, a large number of users frantically initiate transactions with EIDOS, earning EIDOS tokens at almost no cost, and some large tenants have leased huge amounts of resources to call multiple accounts through scripts to initiate transactions. Some wallets and exchanges even launched "EIDOS "Miner" is designed for users to hoist wool.

After the launch of EIDOS, an average of 1.69 million transactions are generated each day, accounting for 50.64% of the entire mainnet transaction, which directly caused the EOS mainnet resource price to skyrocket. If a user wants to initiate an ordinary token transfer, he must mortgage 30EOS to obtain resources, which is undoubtedly an irony for EOS, which has advertised zero transaction fees.

The main network congestion has seriously affected the user experience of other Dapps. Even under the new features of EOS1.8, the Dapp team can pay for resources for users, but this will not help, because most teams cannot afford the high network costs. A number of head Dapps have left the EOS platform one after another, including the blockchain game EOSKnight, which has the largest number of users, and the EOS veteran Dapp EOSBet. EOSBet issued a statement in November last year announcing the upgrade of its brand to EarnBet. At the same time, the team stated that they were very frustrated with the state of the EOS mainnet. They thought that this was not a problem of REX's algorithm or a smart contract, but a governance issue of EOS.

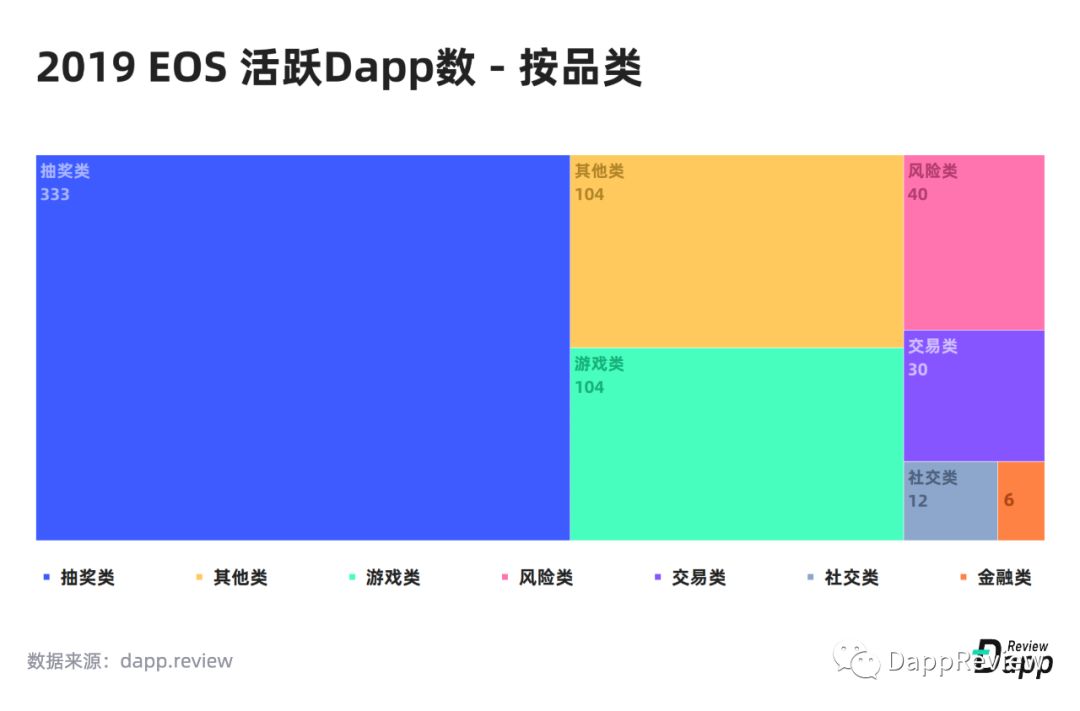

In terms of the average daily number of users, the lottery category and other categories of Dapps have always been difficult to distinguish, each accounting for about 40%. In other categories, there have been popular Dapp Hashbaby and many tool applications. But after November, with the launch of EIDOS, the average daily number of users of these two categories of Dapps dropped sharply, and at the end of December, they were surpassed by the stable performance of game Dapps throughout the year. This is because there are a large number of swiping robot accounts and fleece accounts in the lottery and other types of Dapps. With the EIDOS causing network congestion, the cost of using these accounts has increased significantly, making it difficult to maintain the amount of credit. Most game Dapp users are real players. In order to cope with network congestion, some game Dapps begin to pay resource fees for players to ensure their normal use.

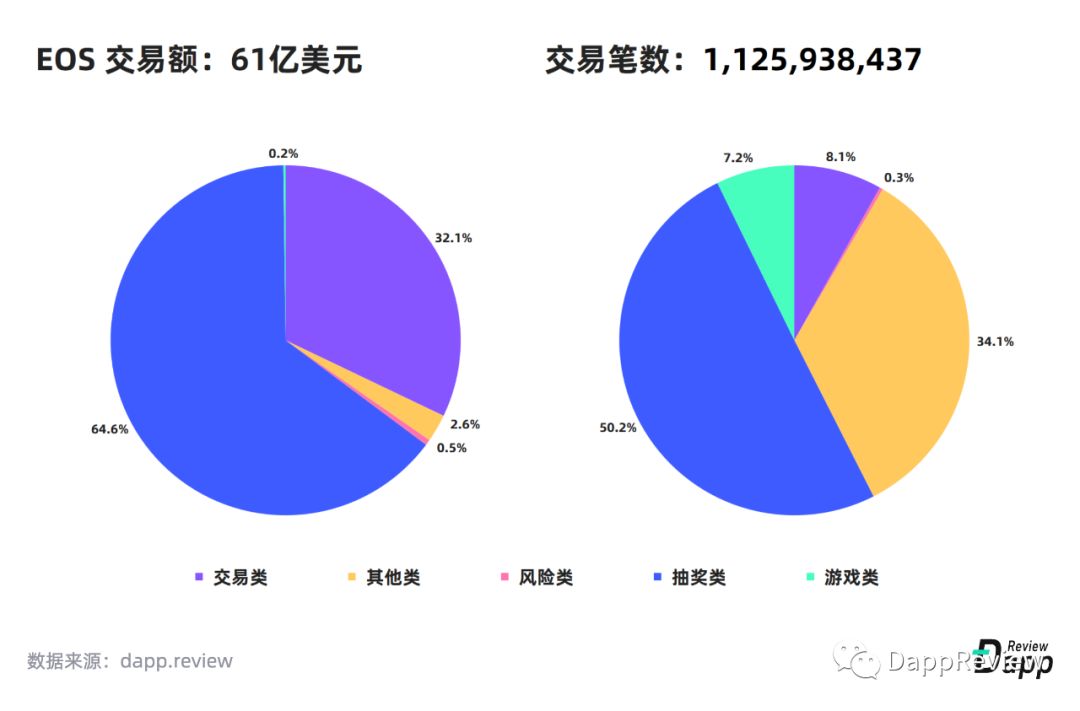

From the perspective of transaction value, the lottery Dapp was the main force of EOS in the first half of the year, and it showed a downward trend in the second half of the year, accounting for 64.6% of the whole year. Similar to the TRON ecology, most of these lottery Dapps have their own dividend tokens, which also drives the transaction volume of the head decentralized exchanges WhaleEx and Newdex, which account for 32.1%.

game

In 2019, a lot of excellent game Dapps have emerged in the EOS ecosystem, most of which are based on native mobile App. These games will call the blockchain wallet application through depplink to complete the transaction signature. If the game involves frequent on-chain interactions, it will jump back and forth between the two applications and the user experience will be greatly reduced. However, the graphics enhancements brought by native apps are far better than H5 web games, and the game's fluency and operating experience are also more friendly than Dapp browsers. Unfortunately, due to the review policies of the App Store and Google Play, most native apps based on the blockchain are difficult to put on the shelves and cannot be distributed in the app store.

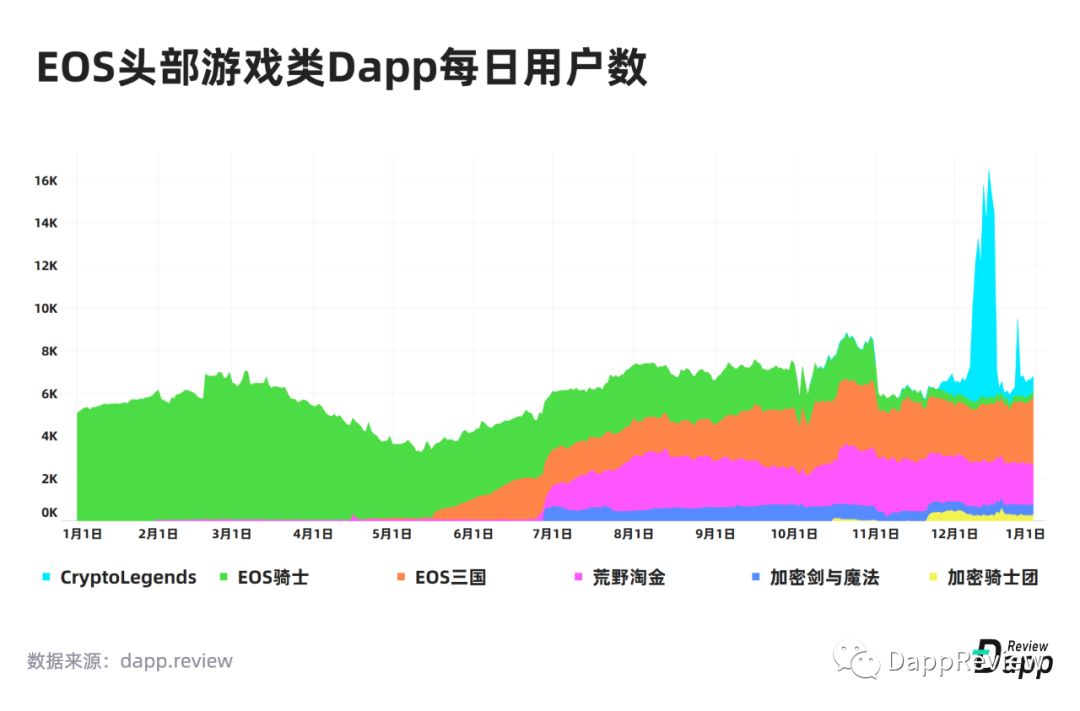

In the EOS ecosystem, there are many blockchain games that live more than 1,000 days, such as EOS Knight, EOS Three Kingdoms, Prospectors, etc. As the first true game Dapp on the EOS mainnet, the EOS Cavaliers had created nearly 7,000 days at the peak of early 2019. The EOS Three Kingdoms borrowed from the gameplay of EOS Knight, added on-chain tokens to enhance user participation, and effectively controlled inflation through in-game numerical design. Later, it became the most popular Dapp in the second half of last year.

However, these excellent blockchain games still have to face a cruel reality: the airdrop of EIDOS will continue for 15 months, and the congestion of EOS main network may be difficult to resolve in the short term, and the existing users are gradually losing. How will Block.one break the dilemma?

In addition, Block.one announced in June last year that it would launch a new social media Dapp—Voice. It would cost US $ 30 million to buy the voice.com domain name alone. This shows that Block.one attaches great importance to this Dapp. It is officially announced that the beta version will be launched on Valentine's Day on February 14 this year, and the entire community is waiting for it.

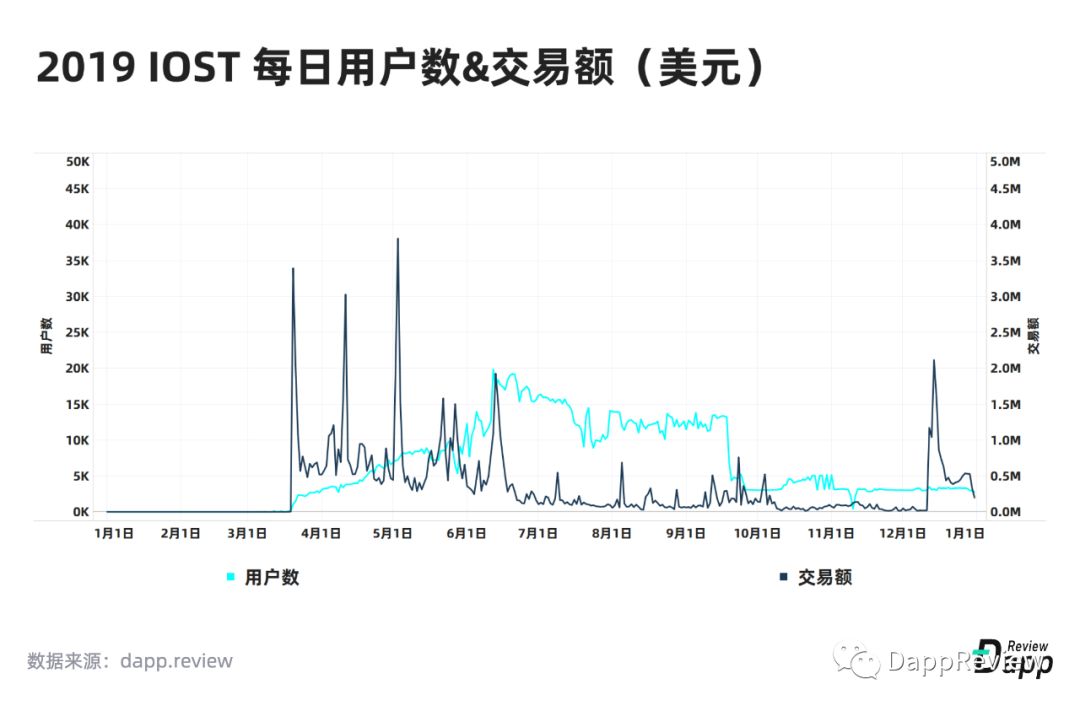

IOST

IOST is a high-performance public chain based on the PoB (Proof of Confidence) consensus mechanism.The mainnet was launched on February 25, 2019. Up to now, the IOST mainnet has launched 43 Dapps, of which the game category and raffle category are the main types.

iPirates is currently the largest lottery Dapp with a turnover of 100 million IOST (US $ 210,000) per day. Prior to this, the most popular lottery Dapp was IOSTPlay, but the game's server was hacked in November last year and forced to shut down. Crypto Three Kingdoms and Monster World are two of the most popular game Dapps on IOST.

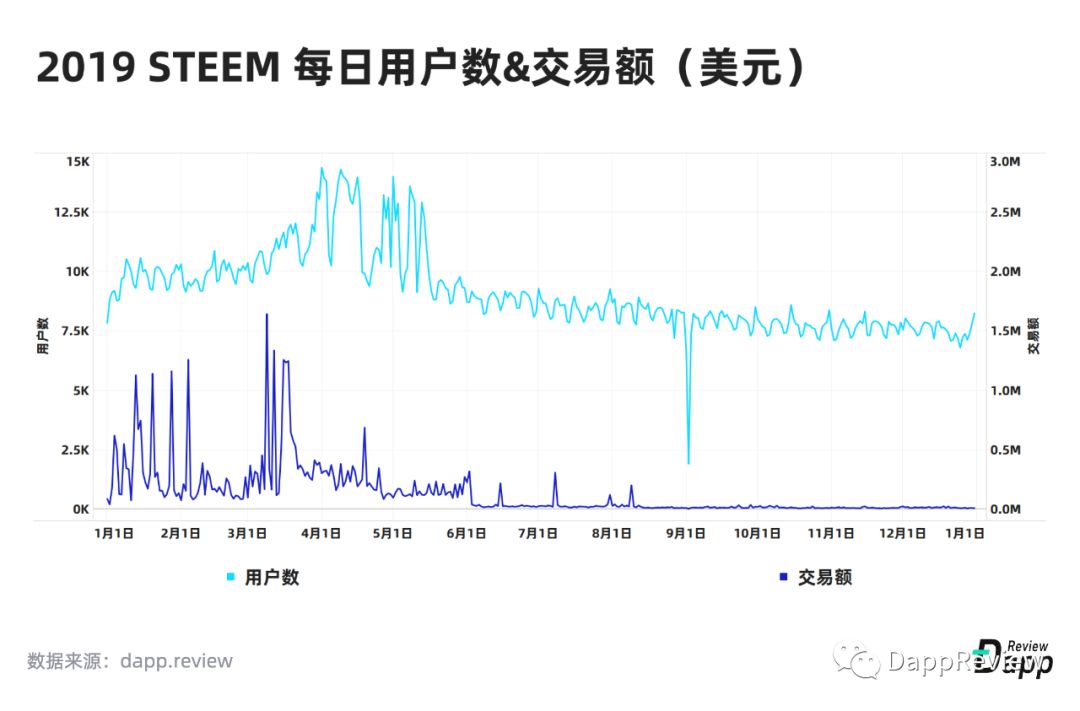

STEEM

Steem is a high-tps public chain. The underlying architecture, like BitShares, also uses graphene technology. In 2019, the platform's most popular Dapps are Steemit and Steem Monster.

Steemit is a decentralized content platform. As the first Dapp on Steem, it has always had many loyal users. However, from the data point of view, the number of users in 2019 is declining, with 5,000 livelihoods at the beginning of the year and only 2,000 by the end of the year.

Steem Monster is a card game, definitely the No. 1 game Dapp on the Steem platform last year. The average daily active user is between 3,000-4,000, and the user retention is high.

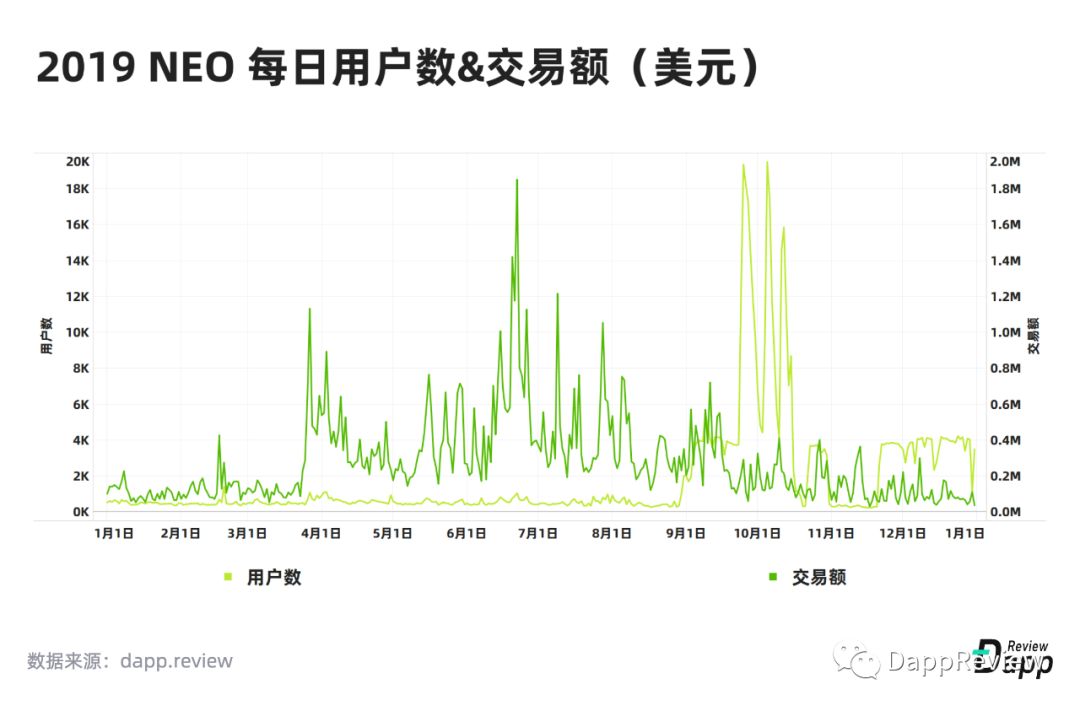

NEO

NEO is an open network created for the smart economy, and it is also one of the earliest public chains, created in 2017. In 2019, NEO began to develop the Dapp ecosystem. Within a few months, many excellent blockchain games joined the NEO ecosystem to expand users, including Blockchain Cuties, NeoFish, and Monster World.

As of now, the NEO mainnet has launched 31 Dapps, of which the game Dapp has the most users. CardMaker and NEOLAND are the only applications with more than 1,000 daily activities. Switcheo, as the first decentralized cryptocurrency exchange on the NEO blockchain, accounts for 5.28% of the total transaction value.

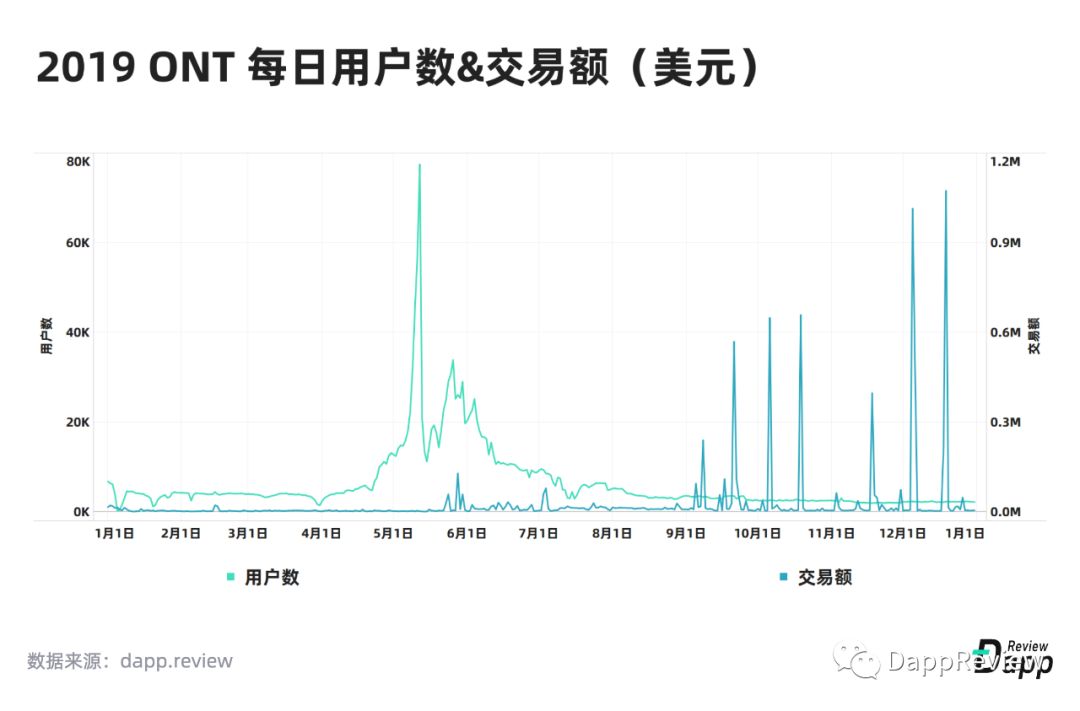

ONT

ONT Ontology Network is a new generation of public basic chain & distributed trust collaboration platform. The mainnet was launched on June 30, 2018. As of now, ONT is running 55 Dapps, of which 31 are game Dapps.

ONT launched the "Renaissance" activity in April 2019, inspiring developers to develop Dapps on ONT. In the following four months, ONT Dapp ushered in an outbreak, with an average daily user of more than 10,000 and a peak approaching 80,000. However, the "Renaissance" plan did not bring substantial development to ONT's Dapp ecosystem. After the enthusiasm of the incentive plan faded, ONT's Dapp users returned to the level of 1,000-2,000, mainly relying on HyperSnake and HyperDragons Go maintain. It was not until November that the MMO game Treasure Land went online, which injected some fresh blood into ONT's Dapp market.

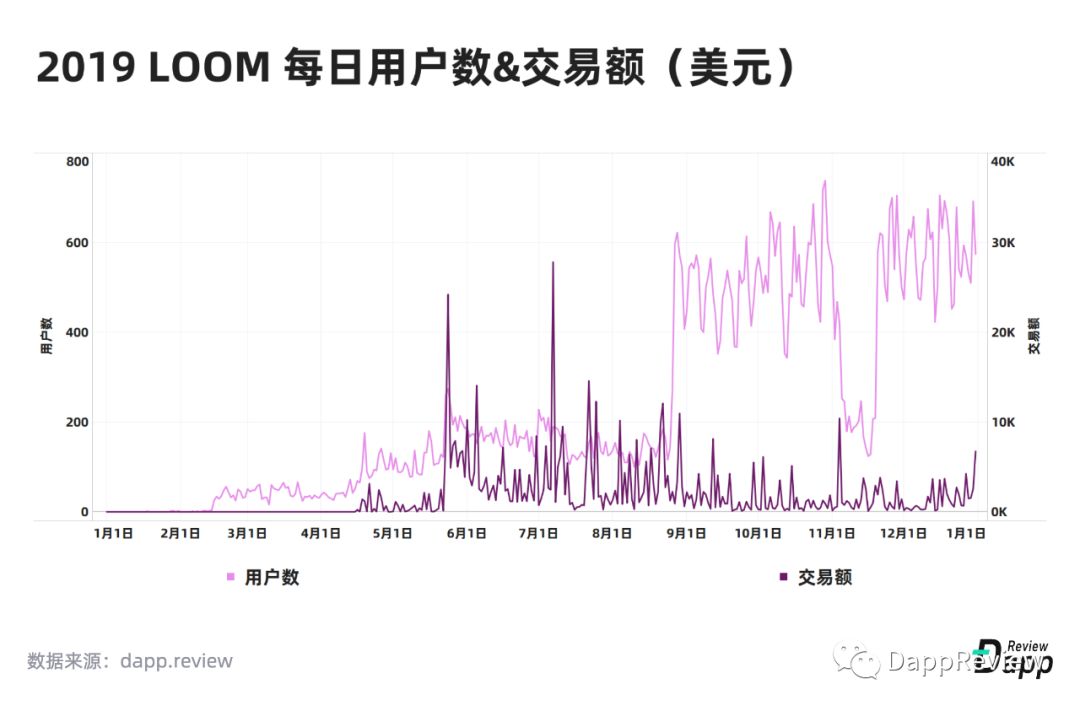

LOOM

LOOM Network is a multi-chain interoperability platform, launched in early 2018.

There are 16 Dapps on the LOOM Network. CryptoZombies, as the most representative Dapp on the LOOM, has been relatively stable. Since the chain was launched in August last year, the overall data of the second half of the entire chain has been basically supported by oneself. Zombies Battlegrounds (later renamed Retentless), a card game that previously raised $ 321,000 on Kickstarter and was highly expected, encountered dystocia after a year and a half of development. The main person in charge of the game has left and the entire project will be open source Give it back to the community.

At present, LOOM focuses on Basechain, and strives to find a breakthrough in the field of DeFi. In September 2019, LOOM Network announced that MakerDAO became the first project to support its cross-chain gateway. The stablecoin Dai will be able to cross-chain to TRON and Binance Chain through the LOOM Network. Binance has launched its verification node on LOOM's Basechain, and soon users will be able to lock positions and get rewards directly from their Binance account. In the future, LOOM Network will continue to develop and support EOS and Cosmos, and plans to launch a pilot project cooperation with the Thai government in 2020 to promote the implementation of blockchain technology.

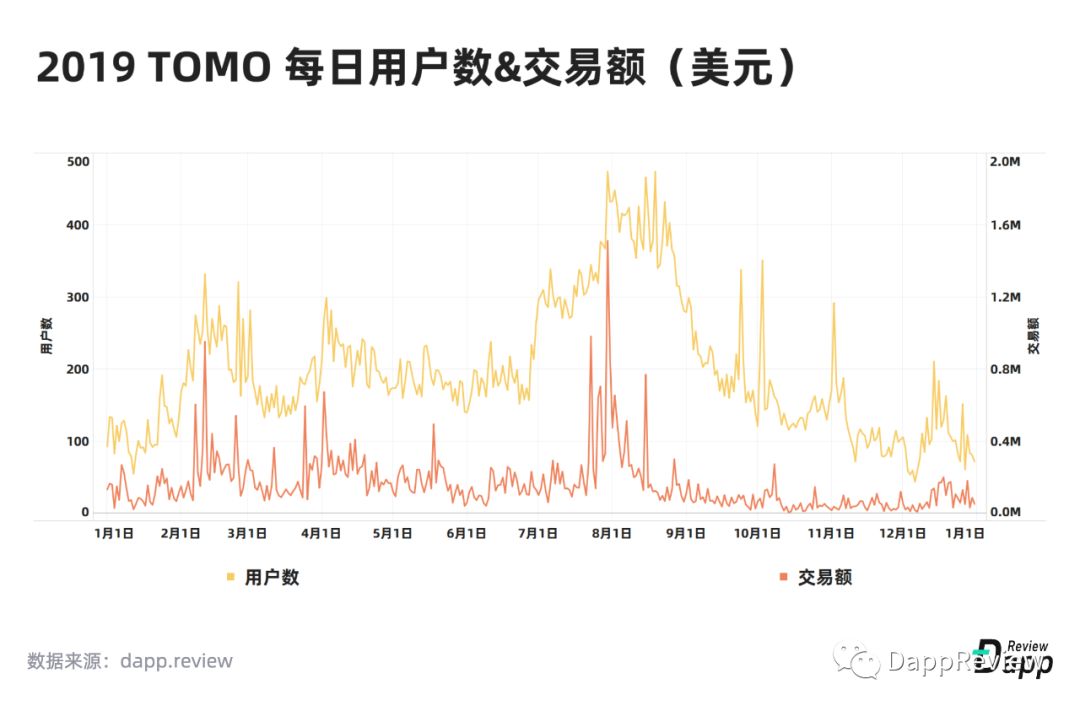

TOMO

TomoChain provides a solution to the scalability problem of the Ethereum platform.

There are currently 22 Dapps on TOMO. The largest Dapp on it is TomoMaster, a TomoChain governance Dapp, and the rest of the Dapps are mostly in the draw category. The activity of these Dapps ushered in a wavelet explosion in the second and third quarters, and gradually became unattended from the fourth quarter. At present, there are less than 10 Dapps with traffic, and this number is still decreasing.

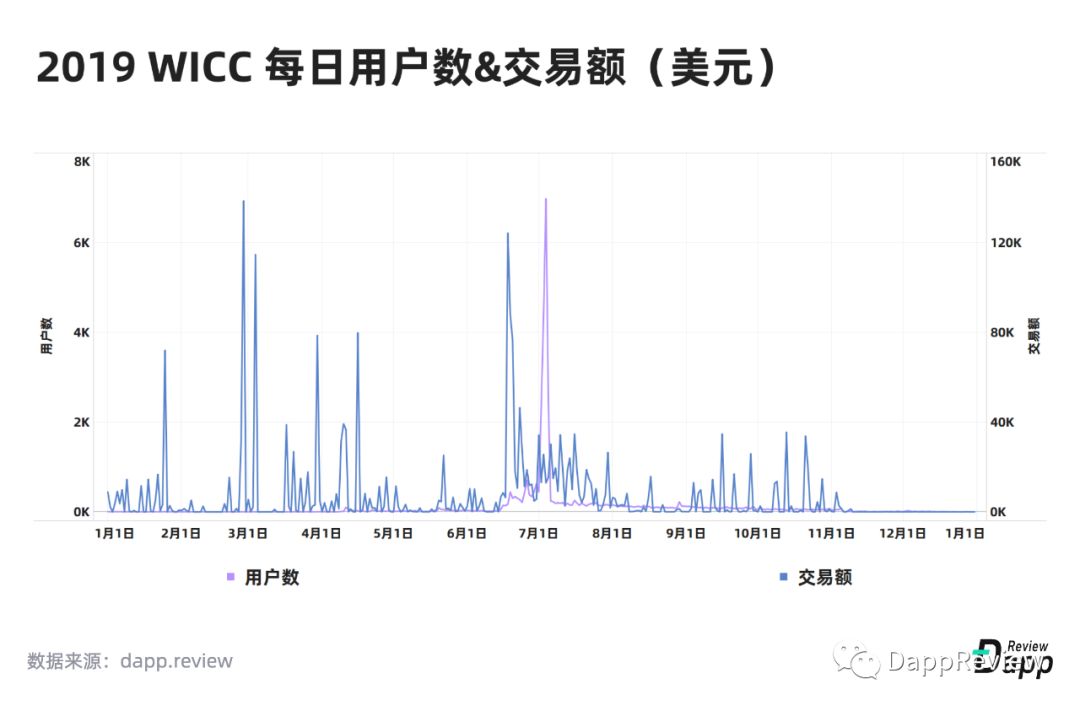

WICC

WICC WikiChain is a Turing complete smart contract platform.

WikiChain has launched 20 Dapps, mainly in games and sweepstakes. However, what really has an impact on the transaction volume of the year is a Dapp called "Hedging." This Dapp is officially developed by WikiChain. WikiChain investors can lock their own Wicc and share the revenue. In July last year, the launch of the lottery Dapp "Gemstone Contest" brought a little vitality to the entire ecosystem, and the number of active users once exceeded 6,000.

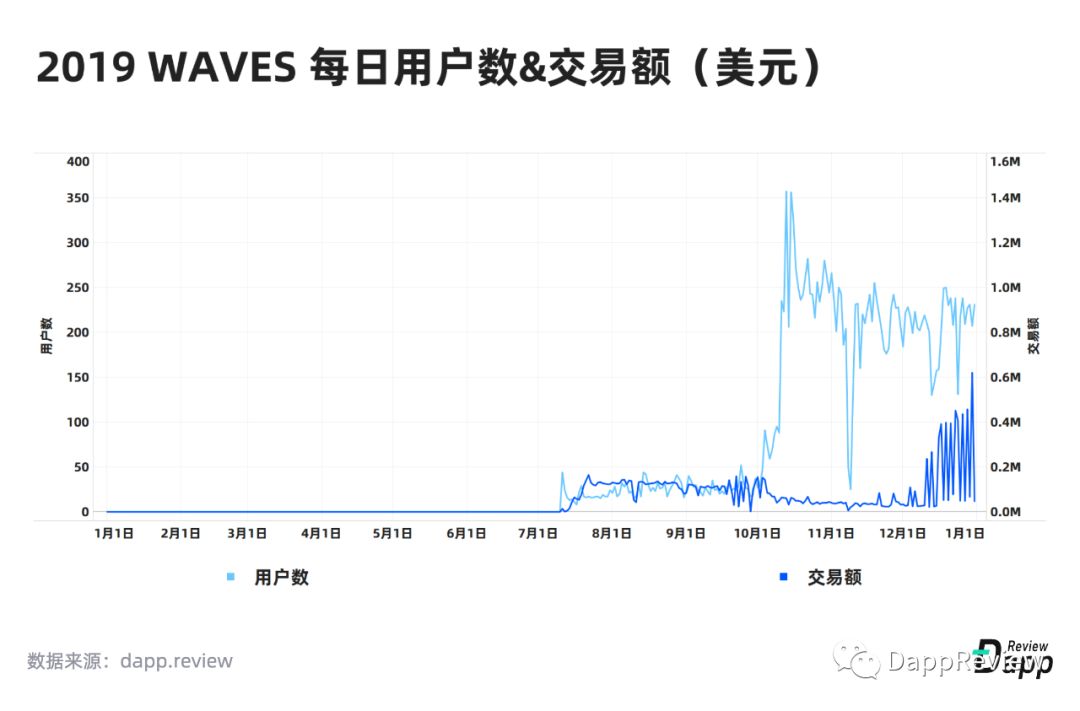

WAVES

As an open application platform for Web 3.0, the Waves mainnet has currently launched 24 Dapps, mainly drawing Dapps.

The most traded Dapp on Waves is Dice Roller. In August 2019, the Waves team released the decentralized platform DappOcean to encourage developers to make Dapp programs. At present, the DappOcean platform has released a variety of lottery Dapps including Dice Roller, Ride on Waves, and Coin Flip.

Perhaps due to the fiery market sentiment of Ethereum DeFi, Waves has also begun to transform to a DeFi-friendly public chain. The annual Waves conference at the end of last year was based on DeFi. DeFi is currently the hottest theme in the Dapp world, and DappReview also hopes that this theme can shine on major public chains outside Ethereum.

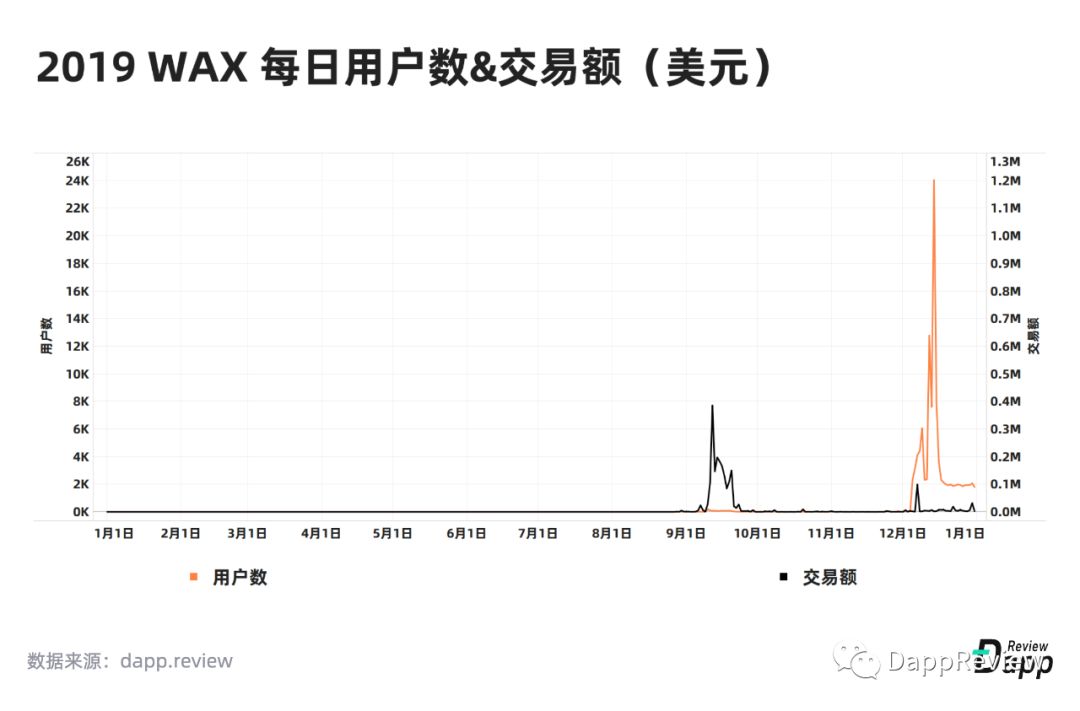

WAX

The WAX Global Asset Exchange is a public chain that was created after customizing based on EOSIO code and carrying out major transformations according to its own needs.

The significant increase in WAX's active users at the end of the year comes from Prospectors. This game was released in June with the EOS version and will be available on the WAX platform at the end of the year. As a public chain that will be launched on the mainnet in the second half of 2019, there are now 26 Dapps, and we look forward to the performance of WAX in 2020.

(Source of this article: DappReview, with cuts.)

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- I was on site in 2019 | After covering 62 events, I ventured to make 3 predictions

- Is there a relationship between Bitcoin price and time? Read the Logarithmic Growth Model of Bitcoin Value in One Article

- 2019, 3 Chinese blockchain keywords in the eyes of foreigners

- Ant Financial Jiang Guofei: Industrial Blockchain Opens, Ten Million Days of Live Applications Will Appear

- From GB to KB, how does zero-knowledge proof create a concise blockchain?

- New collision attack relentless whipshake SHA1 algorithm, using SHA256's BTC to tremble?

- How accurate are people in the industry for the 2020 Bitcoin price prediction?