Academic Direction | How does Bitcoin drive breakthrough innovation in accounting?

Author: Permabull Nino

Editor's Note: The original title is "Viewpoint / Bitcoin as an Accounting Innovation"

Bitcoin was first and foremost an accounting revolution, and this accounting revolution gave birth to a currency revolution. To put it another way:

The accounting revolution is technological;

- Viewpoint | Blockchain is a digital social governance system for AI smart new species

- Bitfinex parent company submits a search application to the US court, intending to recover the frozen 880 million US dollars

- The World Internet Conference is coming. I found a blockchain company in Wuzhen.

The currency revolution is social.

Subversive technology will inevitably lead to social movements, otherwise (by definition) can not be called disruptive technology. Facebook, YouTube, and Airbnb have changed our understanding of social, content creation, and travel, respectively, and have provided us with new ways to interact. The same is true for Bitcoin, which is an accounting technique itself, but is changing the way we understand and use money.

This article discusses in detail what Bitcoin is and how it is driving breakthrough innovation in accounting. Keep this in mind – thinking about Bitcoin from an accounting perspective requires some background knowledge. The outline of this article is as follows:

1. A brief history of accounting and auditing

2. Historical development trends of accounting and auditing

3. In-depth introduction to Bitcoin and three-entry bookkeeping

4. Bitcoin bookkeeping method vs. double entry bookkeeping method

5, Bitcoin + Lightning Network vs. Double Bookkeeping

6. Revelation and conclusion

1. A brief history of accounting and auditing

In order to better discuss, we need to explore the rich history of accounting and auditing. It is important to understand how these areas have evolved over time to better understand the structure and design of Bitcoin. When it comes to the history of Bitcoin, people usually talk about password punk and their technological innovation. However, from a historical point of view, Bitcoin created by Nakamoto has actually accumulated thousands of years of history. Below, let's review each historical development stage of accounting and briefly explain its importance:

count

Before considering the ability to record value, we must have the most basic digital communication capabilities. The basic components of digital communication are: (1) non-verbal expressions of numbers; (2) verbal expressions of numbers; and (3) written communication of numbers. These three elements were born in the same way as historical development, and they all evolved from the human body. At the earliest, people naturally used body language to communicate, and this habit has continued to this day. The parts of the body most commonly used for counting are fingers, toes, joints, and ears. Different human groups have established different digital systems and used specific body parts to represent digital languages, and the choice of body parts determines the digital settings. It's no wonder that in the modern counting system, the two numbers 2 and 5 are so important. Just look at your body and you will feel that the truth is self-evident.

Single bookkeeping

With the development of human exchange behavior, the need to record transactions has arisen. Prior to the 14th century, the nature of transactions was recorded on the “tickets” through the format of sentences/paragraphs, including the parties, commodities and quantities. There is no real “account” in this period, just put together the same type of transaction records, and you can see the balance at a glance (however, there is a receipt and a payment slip).

At that time, the practice of assigning a column to the number on the right side of the transaction description was not yet widespread, and the transaction amount was only included in the handwritten transaction description. During this period, the single-entry bookkeeping method is the mainstream, and this kind of accounting mechanism will become a disaster when it encounters complicated transactions. what happened? Simply put, if you use the single-entry bookkeeping method, the trading party will only write your own unilateral transaction records into the ledger. This defect seriously affects the auditability of the transaction records, and of course it will greatly improve the difficulty of resolving disputes. Because of the lack of resources and the lack of reliable accounting methods as a “safety net” to protect the facts, those who do business are less willing to expand the trading surface (this does make sense). Fortunately, there are new solutions to solve these problems…

Double entry bookkeeping

The quality standards of the single-entry bookkeeping method have not been satisfactory. This is also extenuating, after all, only the participants of the transaction will record the transaction details. However, the auditability of the books to external participants ultimately led to the need for systematic bookkeeping techniques and became a major leap in the history of accounting technology. External third parties need to use an efficient and simple method to record transaction history so that when a dispute arises, it can be used as an auditable clue to identify the fault/fraud party. The double-entry bookkeeping method solves this need simply and skillfully. The double-entry bookkeeping method originated in Genoa, Italy, in the 14th century, and was not yet popular in other parts of Italy and neighboring countries in Europe. Luca Pacioli, a mathematic monk in Florence, promoted the double-entry bookkeeping method. A chapter in his book "Mathematics Encyclopedia" introduced the newly created double-entry bookkeeping system.

After the publication of Luca's work, the double-entry bookkeeping method has become popular in the world, but there are also voices of opposition. Accountants scattered in parts of Europe tried to discredit double-entry bookkeeping on various occasions, or reinvented a new version of the improved bookkeeping system, but it did not work. The double-entry bookkeeping method has been recognized in the industry and is still in use today. In fact, the reason why the double-entry bookkeeping method can't stand the test of time is because the "lender" and "debit" are recorded at the same time, which captures the essence of the transaction. Although the double-entry bookkeeping method has been successful in the early stage of implementation and defines the basic accounting framework, it still needs years of iteration:

(1) People do not understand the principle that “borrowing and borrowing must be equal” (the total difference between the borrower and the lender is always equal to zero), which was discovered later.

(2) After the end of the accounting reporting period, the residual income should be transferred to the capital account (net income → retained earnings). This is not something that can be realized at once, and it takes time to discover.

Although the above two points are the basic knowledge necessary for professional accountants today, they are actually the result of the development of the double-entry bookkeeping method in the past 600 years. Despite such a huge breakthrough, double-entry bookkeeping and accounting reporting systems such as GAAP (American Generally Accepted Accounting Principles) and IFRS (International Accounting Standards) based on double-entry bookkeeping are still evolving. Note: With the promotion of double-entry bookkeeping, auditing has also become mainstream. Three-entry bookkeeping

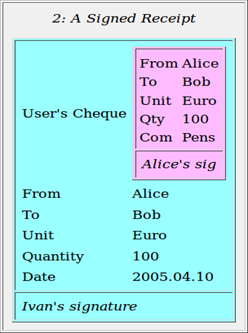

After a thousand years of development, accounting has ushered in a turning point: the three-entry bookkeeping method. Based on the topics discussed in this article, Ian Grigg's proposed three-entry accounting implementation is more relevant. He believes that the three-entry accounting system is “an anti-attack accounting system created for radical applications and users”. . This anti-attack accounting system may combine "financial cryptography innovations such as signature receipts with the standard accounting technique of double-entry bookkeeping." Further, the system created three sets of entries: two of the entries are standard for double-entry bookkeeping, and the other is provided by the issuer. The item provided by the publisher is presented in the form of a digital receipt of the transaction with the signature of the publisher, creating a dominant record for the transaction and storing it jointly by the three parties.

– Signature receipt, the "leading record of the transaction" –

Note: Alice + Bob = the party, Ivan = "publisher"

Grigg made several valuable ideas, such as ensuring transparency within the system to track "clear relationships between participants" while ensuring system anonymity. He also mentioned that from the perspective of information transmission, electronic receipts have a great advantage, but when it comes to contract processing, electronic receipts are relatively weak . In general, there is such an in-depth understanding of the three-entry bookkeeping method in 2005, and the intellectual strength is undeniable. If I guess, the paper written by Grigg is not known to anyone on the day of publication. However, I think this paper has just laid the groundwork for the accounting system used in the decentralized digital currency that was born three years later. Grigg's paper was written on Christmas, and Bitcoin's white paper was published in Halloween in 2008. Is this really just a coincidence?

2. Historical developments in accounting and auditing

After a brief review of the history of accounting and auditing, there is an understanding of human progress in value integration and documentation. In this section, we will list historical trends in accounting and auditing as complementary knowledge. In this way, we can better understand the core components of the accounting system, and can compare their advantages and disadvantages by analyzing the performance of different accounting models on these attributes. Not much nonsense, there are mainly the following development trends:

Anti-mite modification: Accounting can't play a role in value tracking if records can be easily revoked/tampered.

Example: In 2600 BC, the Babylonians recorded business transactions on the mud board and dried or dried them to preserve these records permanently.

Redundancy: This feature prevents mis-accounting and false accounting. Redundant information such as financial management helps to ensure the quality of internal accounting, and independent third-party auditing constitutes another way to find problems.

Example: In order to achieve this financial redundancy, the ancient Egyptians assigned two officials to record the separate accounts of each transaction.

Transparency: Without transparency, you cannot be held accountable.

Example: In ancient Greece, the elected financial officer had to engrave his account on the slate for public supervision. A more modern example is the public offering and the publication of quarterly/annual audited earnings, which also reflects transparency/reproducibility.

Adaptability: As a technology, accounting must be able to adapt to the needs of each era. Without this adaptability, the future development of any economy will be hampered, as entrepreneurs will be constrained by the lack of value-keeping capabilities when expanding their business.

Example: Pacioli (the priest who promotes double-entry bookkeeping) records the accounts in a book, named "Memorial", and then writes "Journal" on this basis. . In the Middle Ages, the various monetary systems were very different, so the memo book was treated as a “converted account book”, and the number recorded in it was converted into the same unit of account and then recorded in the journal book. Let's take a more modern example – GAAP and IFRS are still changing to deal with emerging complex issues.

Empowerability: There is a certain reflexive relationship between the accounting system and the economies they support. The accounting system needs to adapt to the needs of entrepreneurs. Once they have done this, they can further promote economic expansion and prosperity.

Example: The double-entry bookkeeping method originated from the nascent period of the Renaissance, which is the transition period we know of entering the modern era. Although it is not a very common point of view, some people think that this bookkeeping method has played a powerful role in promoting the development of the times.

Exclusivity: Accounting has always been a high-level area, dominated by educated people.

For example, at the rise of the double-entry bookkeeping method, the number of accountants in the entire country will be counted. Later, accountants with insufficient training/educational hours were not qualified to practice. These standards are still used in some areas today.

Simplicity: There is an unwritten rule in the accounting/audit industry that the complexity of the accounting process can only be comparable to actual demand. Simplicity is critical to (pre-existing) prevention and (post-event) errors. In addition, the simplicity makes the accounting system more smoothly promoted.

Example: British accountant Edward Thomas Jones pioneered a bookkeeping system in the late 18th century and claimed that it would replace the status of double-entry bookkeeping. His so-called groundbreaking system replaced the two columns of double-entry bookkeeping with 10 columns, which should be better able to prevent mis-accounts/false accounts. Undoubtedly, this kind of system is too complicated in design, at the expense of simplicity, the improvement of the correctness of the accounts is negligible.

3. In-depth introduction to Bitcoin and three-entry bookkeeping

The previous section summarizes several major characteristics of the accounting system, the most important of which can be said to be (1) anti-mite modification, (2) redundancy, and (3) transparency. As far as Grigg's three-entry bookkeeping method is concerned, it has significantly improved the mature double-entry bookkeeping method in terms of real-time transparency. In addition, Grigg proposed a three-entry accounting system that pioneered the introduction of a receipt (the “led record of transactions”), which was shared by both parties and the “issuer (third-party verifier)”, enhancing system redundancy. Sex. However – because there are only three-party storage receipts, there is still the possibility of loss.

In addition, there may be a problem where the holder intentionally discards the receipt. I would like to conclude that the three-entry accounting system proposed by Grigg in the 2005 paper cannot achieve true anti-aggression because the system is still inadequate in terms of tamper resistance and redundancy.

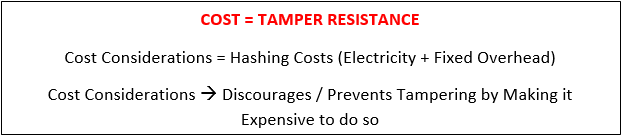

This is the sagacity of Nakamoto. He made minor changes to Grigg's three-entry bookkeeping system, completely solving the problem of lack of tamper resistance and redundancy in the original system design. How is ta done? In a nutshell, the introduction of a betting mechanism in the process of signing the issuer’s receipts makes verification and signatures clearly profitable, thereby triggering competition. With the opportunity to make a profit, many outsiders will provide third-party verification services for personal gain, which will greatly increase the redundancy of the system . The most striking part is that the redundancy provided by Nakamoto's three-entry bookkeeping system also helps to improve tamper resistance. This mechanism is called "Position Proof (PoW)."

In short, PoW refers to the amount of work that cannot be forged and costly in order to calculate results that meet certain criteria. In the Nakamoto consensus mechanism used by Bitcoin, the so-called "work" is to hash a subset of the relevant block data and a random number (nonce); this work is repeated until a match is found A certain required hash value is considered to be a "workload proof"; this "requirement" is also well known in the network, also called "network difficulty requirements." This hash value can be verified by other third party certifiers in the Bitcoin network and finally used as the "receipt signature" for each published receipt (ie, block).

The cost of a hash operation comes from the power consumed to power a hash machine (mining machine). At such a huge cost, the dominant record of tampering with transactions (ie, the blockchain) is costly. Part of the economic incentive comes from the coinbase reward (newly generated token) + transaction fee for each block that has reached consensus across the network. The following is a brief summary of the solutions to the problem of tamper resistance and redundancy:

Profit = redundancy implementation mechanism

Profit Motivation = Block Reward + Transaction Fee

4. Bitcoin bookkeeping method vs. double entry bookkeeping method

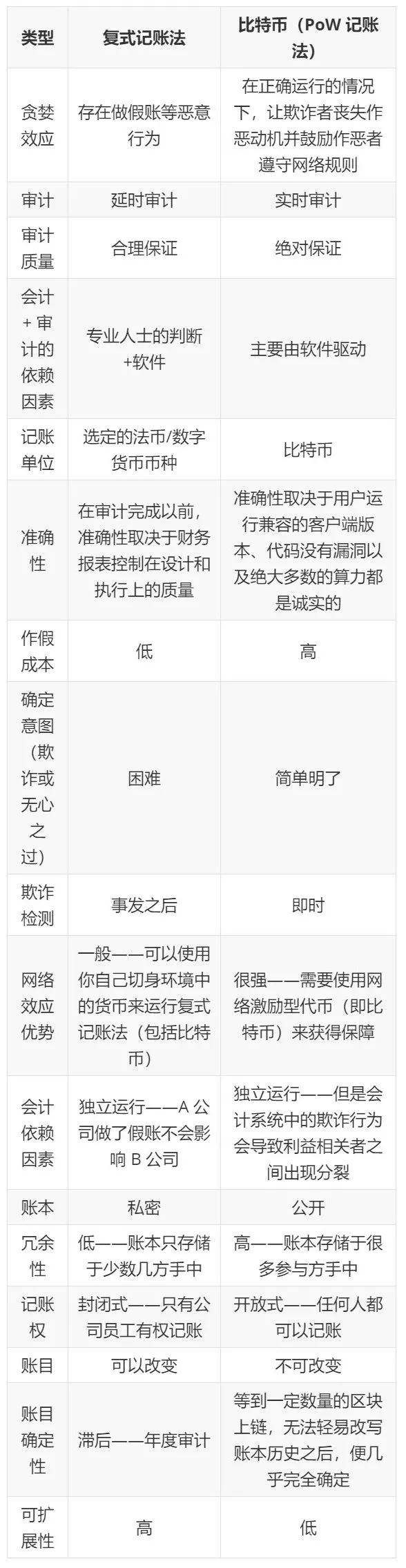

The difference between Bitcoin's three-entry bookkeeping method and Pacioli's double-entry bookkeeping method is not just the three characteristics mentioned above. In this section, we will explore in detail the differences between the two systems, the impact of Bitcoin on accounting, and whether there is a substitution or complementarity between the two systems. The following table lists the main differences between Bitcoin's bookkeeping method and double entry bookkeeping:

– Duplex account vs. Bitcoin –

The differences between the two systems can be categorized into three categories: (1) flexibility, (2) scalability, and (3) guaranteed strength. However, these three characteristics are not in the same dimension. The flexibility and scalability of each system determines the assurance that it can provide. The former distinguishes Bitcoin from the traditional accounting system, while the latter embodies the “great innovation” of the entire Bitcoin accounting system. Next, we will focus on what is "great innovation"…

Remember – the whole world runs on a double entry bookkeeping system. This is foreseeable because double-entry bookkeeping creates a system that is extremely flexible, scalable, and simple to record/propagate value. In addition, if there is a wrong/false account, you can also use the audit trail to confirm where the problem is. Financial control can prevent (in advance) some of these problems, and external auditors (after the fact) perform the task of detecting problems. In summary, the double-entry bookkeeping method has achieved great success and will continue to provide us with good services.

However, it also has a very obvious flaw: in terms of data integrity, it cannot provide a strong guarantee to the user . From the accounting professional point of view, the guarantee strength provided by the double-entry bookkeeping method is called “ Reasonable guarantee." Although there is still a high degree of credibility brought about by ex post auditing, reasonable assurance cannot guarantee that the ledger is completely accurate and can only be said to be “sufficient” and accurate. Take the accounting/audit of cash balances as an example (this is a relatively low risk area in the audit work, and the cash balance in the balance sheet is also the most comparable asset to Bitcoin).

External audits require bank certificates for cash balances, which can be obtained from banks holding client assets, usually from 24 hours to several weeks. These reports from external third parties are considered reliable audit evidence because conspiracy is the only way to make false accounts (and we assume they will not collude). However, in fact, conspiracy is difficult to find. After all, auditors cannot access the bank's accounting system, and there is no reason to doubt the accuracy of the report. It is unlikely that the report will leave traces of fraud. This example is used to illustrate that even in the simplest case, double-entry bookkeeping does not fully ensure the accuracy of accounting data. This is the pain point of the double-entry bookkeeping method, and it is also a major breakthrough in the history of bookkeeping in Bitcoin…

Bitcoin is the first accounting system to provide absolute assurance of the integrity of the book data. Unlike double-entry bookkeeping, Bitcoin does this because it provides convenient third-party verification through a highly flexible, highly redundant protocol+ network . From an accounting point of view, the speed of this independent third-party verification is very important because it changes the cost-effective and inefficient verification mode in the past, opening the door for users to complete verification with a single click. . To put it simply, it changes the independent internal accounting + external auditing model in the past and integrates them into one .

It is worth mentioning that it is absolutely guaranteed that not all the characteristics of the public chain are natural and can only be realized if there are enough resources to invest in the network. These resources reinforce the two main characteristics of the anti-mite modification and redundancy we mentioned above (except Bitcoin), and few public chains can meet this standard. Any cryptocurrency network that wants to achieve sustainable development must provide absolute assurance as an important mission, because entrepreneurs only favor those accounting systems that have proven to be reliable.

It should also be noted that the double-entry bookkeeping method and the three-entry bookkeeping method of Bitcoin are essentially complementary. A quick look at the tables provided in this section shows that Bitcoin's accounting system fills the gap in the double-entry bookkeeping system and compensates for the lack of existing accounting services on the market. In addition, Bitcoin (accounting unit) can be compatible with both the Bitcoin network and the dual-entry accounting software that runs locally. However, the legal currency such as the US dollar, the euro and the British pound cannot do this. They can only follow a fixed set of paradigms (double-entry bookkeeping). In the next section, we will explore the impact of this distinction.

5. Bitcoin + Lightning Network vs. Double Bookkeeping

Black Bitcoin has always been known, and it is considered to be too poor for expansion. These sunspots also concluded that the second-tier expansion plan is just a daydream and can never be realized. Fortunately, at the beginning of 2019, Lightning Network expanded rapidly in terms of users, nodes, channels and bitcoin performance, and smashed the face. On the surface, Lightning Network is a payment channel that helps Bitcoin expand its trading surface. That's right, but the point is "Why can lightning network improve transaction throughput?" From an accounting point of view, the answer is: Lightning Network is an iteration of the double-entry accounting system, which is native to the Bitcoin network. Double billing system. Before delving into the lightning network, let's look at a table and add a new column based on the previous table:

– Duplicate Account vs. Bitcoin vs. Lightning Network –

From the above table, we can see that the lightning network is between the double-entry bookkeeping method and the bitcoin three-entry bookkeeping method. This compromise is at the expense of the simplicity and flexibility of double-entry bookkeeping. Therefore, in the accounting system of Bitcoin + Lightning Network, double-entry bookkeeping is still relevant and practical. More importantly, the Layer 2 expansion plan complies with the accounting + auditing principles . For financial statement audits, the portion of the single item + total amount that is less than a certain value is ignored, because the extra precision on the small amount of funds gives the financial statement a very limited quality improvement. Bitcoin and Lightning Networks take advantage of this. In order to enhance the scalability of Bitcoin, the small transactions are transferred to the less redundant accounting + auditing layer, and the channel on the lightning network can be closed with the click of a button. The final result will be packaged and guaranteed for absolute assurance.

6. Revelation and conclusion

Bitcoin is the ultimate accounting tool

Bitcoin is expected to be the center of the accounting profession. Why do you say this? Because Bitcoin (accounting unit) can be compatible with the existing three accounting tools, and the legal currency can only be used in double-entry bookkeeping. The figure below clearly reflects this difference:

– Legal currency bookkeeping tools –

– Complete Bitcoin Accounting Tool –

Since the legal currency is not a native asset on the cryptocurrency network, the deep accounting + practicality guarantee provided by the cryptographic currency is not available. Stabilizing coins can't do this either because they have serious centralization-dependent problems and only represent the dollar that exists under the chain (or, in some cases, the "reasonable" dollar that exists under the chain). This difference means that when Bitcoin matures, it will be more useful than French currency, providing future entrepreneurs with more reliable methods of value recording and creating powerful accounting models in different fields. In other words, there will be a new type of bitcoin-centric enterprise in the future, and the legal currency can only be watched.

Finally, the “Complete Bitcoin Accounting Tool” picture may raise concerns about lower subsidies in the future. If Bitcoin becomes the center of the accounting profession and the ultimate source of value facts, the demand for Bitcoin is likely to support the security of the network. Those who believe that "high fees will kill users" do not understand the guaranteed strength offered by Bitcoin and the simplicity of Bitcoin's implementation. In short – the cost of bitcoin is very low compared to other solutions that offer higher assurance. Bitcoin should have been a "moon landing" tool, but it was considered a scooter. Other thoughts: Bitcoin may not be considered a “accounting unit” from a monetary point of view, but from an accounting point of view, it has become the ultimate unit of account. The positioning of the Bitcoin model will not take many people to spend time thinking about this.

However, there are still some people who are thinking about other forms of Distributed Ledger Technology (DLT). If other distributed accounting models are designed to subvert the blockchain model, they provide (1) ease of value accounting or (2) assurance of blockchain models to achieve equal strength or higher strength. I think this is unlikely because the blockchain model is very simple (Zhong Bencong only uses 6 sentences in the Bitcoin white paper to explain), and in the case of correct implementation + resource commitment to the network, the district The blockchain is almost absolutely guaranteed. The most basic value proposition of Bitcoin There are many reasons why Bitcoin is valuable, such as sound currency, hedging of the central bank system, and so on. These are all right, but they are all off the network itself.

So far, I have not seen anyone giving a real value proposition to the Bitcoin network and its unit of account (bitcoin) at the most basic level. After we have identified the most basic value proposition, we can explore it from a more popular social level. Therefore, at the end of this article, we try to summarize the value proposition of Bitcoin: Bitcoin is valuable because it is an irreplaceable and scarce incentive token, in the new distributed three-entry accounting system. Acting as a glue to integrate currency + accounting + third-party verification into the same software-based product. The reason for the need for such software is that it provides absolute assurance for accounting in value transfer/storage, and no other accounting system can satisfy this claim.

Bitcoin's bookkeeping method is also unique because it has features that provide users with a strong guarantee of practicability, such as anti-censorship and asset seizure resistance. It is these features that make Bitcoin a popular value storage tool. This tool can "address malicious behavior and malicious users" and its digital/open architecture is more user-friendly. Accounting + Practicability-based guarantee + digital/open structure makes Bitcoin an ideal tool to counter the current monetary system and ultimately become a good candidate for a “sound currency” of market choice. Finally, thinking about double-entry bookkeeping has existed for 600 to 700 years, from textile companies in the Industrial Revolution to today's space travel companies, which have met the accounting needs of various companies. This accounting system has existed for more than 99% of the time and creates uncalculated value.

With this in mind, we have to think about how much human investment in the first 10 years of the double-entry bookkeeping method is equivalent today. Why should you think about this? Because of the emergence of Bitcoin, we have the opportunity to prove the investment workload + the three-entry bookkeeping method. From an accounting point of view, Bitcoin's ability to provide absolute assurance is unprecedented and completely undervalued by the market. The gibberish about “heavy blockchain, light bitcoin” between 2015 and 2016 has made everyone ignore the significance of bitcoin in accounting. However, it is time for us to return to our original heart and sit on the bitcoin in the accounting industry. It is the importance of Bitcoin in accounting that has made it possible, and it is likely to make it shine in the midst of a global currency war. Therefore, it is necessary for all industry insiders to regard Bitcoin as a currency and accounting revolution. Many thanks to Oke Pearson (@OkePearson on Twitter) for reviewing this article and all accounting content covered in this article.

(Finish)

Original link:

Https://medium.com/@permabullnino/bitcoin-an-accounting-revolution-40efcb903d7b

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- In the questioning, how does Libra's currency basket fall? Single anchor instead of integrated anchoring?

- The currency will be added to the legal currency transaction pair. The first supported legal currency is the Russian ruble.

- Exclusive interpretation | Tencent blockchain released 3 editions of white papers in 3 years, these landing applications are the most concerned

- Pick up IEO! Can Sthum's new gameplay at Bithumb Global Station create the next wave?

- After the 18 million bitcoins were dug up: these “18 million” milestones are also worth remembering

- Soul torture: Is Bitcoin or Bitcoin "Writing" on Wall Street?

- PlusToken launches a large number of chain transactions again, transferring 20,000 ETH