Opinion: The encryption technology hype cycle has begun, and the idea of retail investors is easier to guess than the wallet password.

Author: Joseph P. DiPasquale

Translation: First Class (First.VIP)_Maggie

Source: first class warehouse

Editor's Note: The original title is "The arrival of the bull market requires more investors to enter the market"

- 11 blockchain companies have become global unicorns! Is it still time to get off the train?

- Read the Bloomberg Beta, how the $250 million fund is deployed in the blockchain industry.

- "Focus on the AI era": 2019 The world's first AI era mining ecological summit ended successfully

Foreword: It is easier to guess the idea of “chives” than to guess the password of the wallet. Encrypted investors need to grow first before they can drive the entire encryption market.

The volatility of the cryptocurrency market is mainly based on short-term speculation, as there is still a long way to go before it can be adopted on a large scale. Many projects are experiencing growing pain: they are not new enough to make traders “gamble” on money, but they are not mature enough to justify higher market capitalization.

If the project achieves its goals and uses technology, it can strike a balance between hype and maturity. However, traders who only focus on hype during this transition may be those who are forced to take over after the dust settles.

Encryption technology hype cycle

We have all heard of Gartner's hype cycle (technical maturity curve) . The basic idea is that for any emerging technology, expectations of its potential will mature over time.

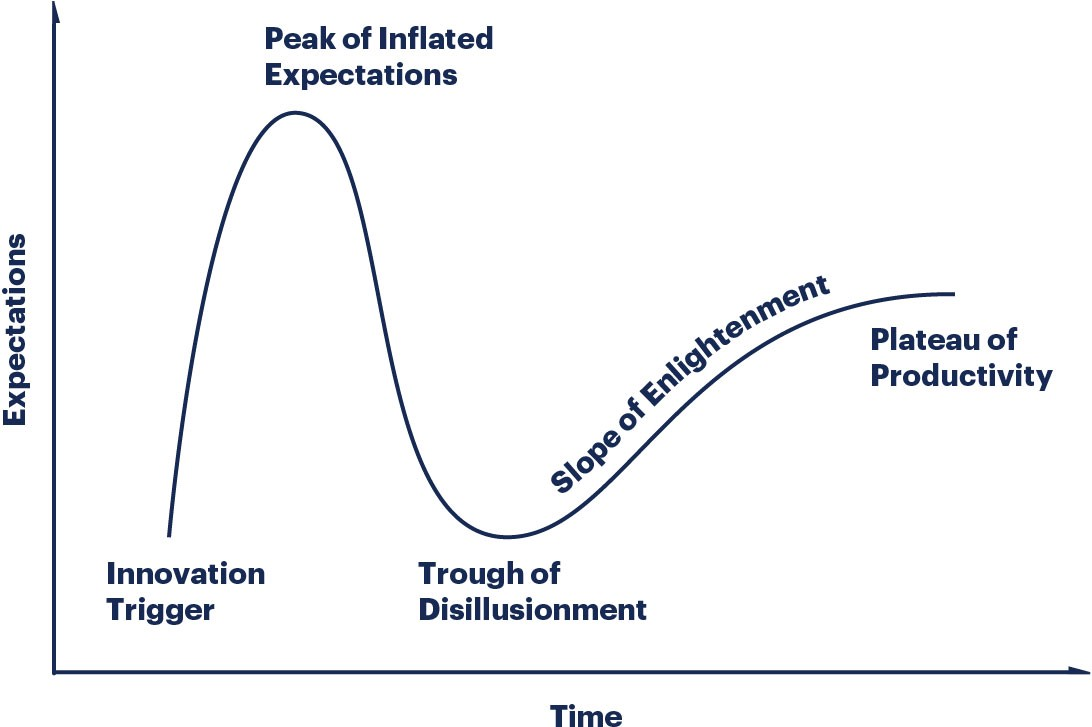

(Figure: technical hype cycle, source: Gartner)

The left-to-right stages in the picture are: technological innovations trigger public interest; the public's rising expectations finally reach its peak (optimistic); public expectations decline, eventually bottoming out (pessimism); adjusting expectations according to reality (realism) .

This model measures the function of two forces over time: hype and maturity. Like a pendulum, “hype” is the lateral force that fluctuates the expected value, and “maturity” is a kind of gravitation that ultimately aligns expectations with reality. When the expected value rises too high to be quickly satisfied, the pendulum will fall back and the expected value will drop sharply. When maturity is low, expectations may fluctuate wildly, but as maturity increases, expectations become more moderate.

In the cryptocurrency market, the hype cycles can occur simultaneously on three different levels. The first is the entire cryptocurrency market (currently dominated by bitcoin) and its technology maturity curve. Followed by different cryptocurrency and blockchain use cases (such as infrastructure, dApps, stable currency, securities tokens, etc.) in the industry, each use case has its own technical maturity curve. The third level is that individual projects try to stand out and compete for capital, market share and adoption rates – again, each project has its own technology maturity curve. Each layer (the entire encryption market, a certain use case, a single project) adds a "pendulum" to the chain, and it is impossible to try to determine the position of a particular project in a particular technology maturity curve in the chaos. of.

Even more confusing is that expectations for any particular project may be overestimated or underestimated, depending on who made the estimate. Everyone, the public, cryptocurrency traders, blockchain developers, project proponents, and competitors, can hold very different views and understandings, and these ideas can be amplified and filtered through social media. " Inducer" and "singer" (Editor's Note: Originally "shills and trolls", "shills" is what we call "inducers" or "childcare", such as sellers in commercial activities. In the presence of the buyer, pretending to be an unrelated person, using words, actions, etc. to mislead a type of person who uses other people to purchase goods; "trolls" refers to people who initiate or promote topics, often posting in a harmless way to cause confusion) When you yell at each other on the Internet, you can hardly convey any valuable information.

Huge expectations to fill the gap in maturity

Although exchanges and commercial organizations engaged in the integration of market data attempt to convey “valuable information” to investors, the cryptocurrency market is ultimately not a stock market. Both are speculative, but the stock price is based at least to some extent on objective data: including mandatory disclosures, company profits, assets and valuations, rules and rights clearly defined by the legislature and regulators, etc. And is supported by many experienced long-term investors. Based on such an informed and professional market, stock prices are usually more stable than cryptocurrencies.

On the other hand, the price of cryptocurrency is not so "traceable." The new blockchain entrepreneurship project has presented exciting ideas on paper that, once realized, seem to bring a staggering “outbreak”. However, there is little objective data (if any) that crypto-traders can rely on, and there are very few "effective products" or significant use cases for cryptographic projects that can be used to estimate the value of a project. Most projects do not disclose their own funds, income, losses or expenses. When robots and whales manipulate exchange price, institutional investors who may bring stability to the market are on the sidelines due to regulatory uncertainty. One-sided emphasis on potential high returns, while ignoring the high risks that follow, has led to overconfidence among small investors. In reality, if there is no strong anchor, there is no upper limit to the high expectations and prices.

Due diligence on blockchain projects is still very difficult. Find basic information about the project ( token use cases, supply curves and distribution, development progress, future roadmaps, team qualifications, consensus mechanisms, external partnerships, and usage statistics) often in multiple white papers, browsers, tweets, blogs , podcasts, video sites, and news reports sort through a lot of information — and this is based on the assumption that information is available and accurate at the outset. When a trader tries to evaluate a project with a competitor, the burden will multiply and it will be difficult to find a competitor to the project.

There are also many people who are not confident enough about projects that have produced tangible results. These projects are now experiencing the difficult process of building a vision and attracting users, which takes a considerable amount of time, effort and collaboration. They have already passed the “excessive peak of expectations” at this time, so the expectations are facing a downward trend, at the lowest point or moderately falling back to a position more in line with their outcomes, depending on their maturity. For most traders, it's as exciting as watching the paint dry: after experiencing peak expectations, while the team continues to move toward product maturity, holding these established projects The cryptocurrency is seen as an opportunity cost, and at this time the shiny new projects can only achieve price gains from the inflated expectations.

The idea of "chives" is easier to guess than the wallet password.

(Figure: The quality of the decision is inversely proportional to the quantity, source: idonethis blog)

In the face of too much (or even too little) information, we will resort to a variety of so-called "experience stickers" to guide our decisions. This may be practical and efficient, but many projects and their sponsors have begun to learn to cater to these heuristics, thereby gaining people's excessive attention or distracting people's attention to the project's own weaknesses. Therefore, you need to remember a truth:

"Protecting your brain is like protecting your private key ."

When you see these "hackers", please recognize them so that you can see through them. The following is not a comprehensive list, but describes some of the more common cognitive biases among traders, namely "prejudice":

1) Initial price bias: “The first decision will affect all subsequent decisions”. The price of a particular cryptocurrency at the time of the first sale/distribution may affect our perception of the current price, even if the initial price is arbitrarily set at the outset.

2) Accessibility bias: We usually focus on price anomalies, such as historical highs and lows, because they are prominent and easy to find. But usually, these data points reflect the current larger cryptocurrency market, supply dynamics, or market conditions, rather than the current strengths of the project.

3) Scarcity bias: You may have heard of some versions of a cryptocurrency that "only 1/x of the world has it." Limited supply means scarcity, and this seems to imply higher value, creating a “purchase urgency”. But think about it, for example, a kind of graffiti that we make ourselves, although rare, is not worth anything for anyone.

4) Sunken cost paranoia: We insist on what we have invested in, “often only when you sell, you will realize the loss”, but the reality is that now sell at a lower price than at a lower price in the future. better.

5) Dak effect: Dunning-Kruger effect or DK effect. The Dak effect is a cognitive bias. It is understood that the more we know, the more we may lack confidence; the less we know, the more confident we are . Community members who have a thorough understanding of the project's rationale may be more conservative and cautious about project expectations, while community members who are relatively unaware of the situation may make bolder predictions.

6) Herd thinking: The loudest, most confident, or the earliest voices tend to guide the team's decisions, but think about the existence of the Dak effect, which may be irrational, from people who know little, which may lead to decision making. Mistakes. Objective assessments and critical thinking within the project community should be encouraged to counter the rhetorical guidance from the majority (or a few loud people).

7) Social relations bias: We tend to rely on others to guide our behavior. Partnerships, support from influencers, and social media forces can bring credibility to a project, but this support can be superficial and driven by ulterior motives.

We need a better way to evaluate

Deloitte wrote an article about innovation hype last year and proposed some of the criteria we should consider when evaluating new technologies. These standards go beyond the scope of hype and involve the adoption of a technology and its technology. The issue of life can be used as a reference for the judging project.

1) Complexity and compatibility: How difficult is the technology to use? How many existing habits do users need to change? For example, the slogan "Become your own bank" sounds good, but for most consumer end users, managing and protecting private keys, guiding transactions, and running all the necessary software can be difficult.

2) Observability and communicability: How difficult is this concept to explain? Can we see its role? The higher the learning curve that understands the value of innovation, the less likely it is to adopt this innovation. (Editor's note: The learning curve can be understood as the rate of skill or knowledge acquired over time)

3) Testability: Can people test or try this technology before investing time, effort or money? Is there a test network and documentation for new developers to experiment with? Providing users with the opportunity to “try before you buy” helps reduce perceived risk, attract interest and demonstrate value.

4) Comparative advantage: What are the benefits of using the cost and effort to change the status quo? If the advantages of a new system are only trivial, and the current treatment is “good enough,” the dynamics of change may be low.

5) Perceived risk: What are the disadvantages/risks that may exist when the technology is adopted? For example, financial risks, social risks, outdated risks and performance risks, etc., the losses that may be caused by these risks may offset the original benefits.

6) Personalization and flexibility: How flexible is technology to meet user needs and desires? Just because a project has a solution doesn't mean it fits all the problems. A rigid format can stifle users who want to “think out of the box” and apply innovation in new and unique ways.

7) Embrace the subculture of innovation: How large is the group of adopters? How much influence do they have in this industry and throughout the public? Is it growing? The social media army may have effectively increased market awareness, but has little influence on adoption rates other than transactions.

8) Focus on potential phenomena and side effects: Bitcoin is a typical example of blockchain and cryptocurrency, but blockchain technology has a broader meaning than Bitcoin itself. What is the current hype surrounding decentralized finance that is unique to its use case? Is it based on the success of the Ethereum network? Or is it a real miracle that is a wide range of automated, untrusted transactions supported by smart contracts?

In the long run, technologies that are not practically adopted will die out. No matter how provocative the publicity of a project started, it seems promising. If there are no niche groups like traders, robots and whales that make up the majority of the market, no one buys and uses it. Eventually, when the market saw that new blood did not appear, most participants lost their escape. A project with a thriving ecosystem that attracts new users will bring new value and fuel to keep its economic engine running.

"The blockchain technology won't become mainstream until it becomes boring. It must be so subtle and 'infiltrated' so much that most people don't know if they are using it or how it is. Operational – and don't need to know."

We can continue to burn money on high-risk “white papers and dreams” projects, hoping to seize the opportunity of speculation before it reaches its peak (sell before it falls).

However, those experienced projects that are still open and adopting signs despite low expectations have less long-term risks and deserve further study. A healthy cryptocurrency market requires flexible and growing projects, and it's time to start treating them more seriously.

Author's Note: This is a review article. None of the above is considered as legal or financial advice. Although the author is a lawyer, but not your lawyer, you should have one-on-one consultations with a professional about your situation before making any major legal or financial decisions.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- The total market value of 11 blockchain unicorns is 269 billion. Will stable coins and DeFi be the new unicorns?

- Operation Guide: How to buy and sell Dai on OTC on imToken

- Babbitt column | Digital currency relative valuation method

- Li Lihui, former president of Bank of China: Digital currency, another restructuring of the monetary system

- The US group is ten years old, or is it no longer outside the blockchain?

- Bitcoin offline payments are now available via Lightning Network

- Libra or a stable currency that anchors a single currency, not a basket of currencies