Article describes the type, scale and trend of stablecoins

Written by: Baijun Qian, HashKey Capital Research

Review: Zou Chuanwei, Chief Economist of Wanxiang Blockchain, PlatON

Source: Chain News

Despite the ups and downs of the cryptocurrency market this quarter, stablecoins have become the biggest winners in the first quarter of 2020. According to media statistics from The Block, the trading volume of stablecoins in the market surged in the first quarter of this year, an 8% increase from the fourth quarter of last year, and exceeded the $ 90 billion mark for the first time in history. In comparison, the total volume of stablecoins last year was 250 billion U.S. dollars.

- On the Equity of Currency Stocks and Token Economy: How to Coordinate to Generate Synergy

- USDT issues more than 10 billion in six days. In a bear market environment, stablecoins become the biggest winners

- Free and Easy Weekly Review | "House N" Reflects the Weakness of Privacy and Sees How the "Sky Eye" of the Chinese Academy of Sciences Breaks the Game

In addition, data from Coin Metrics also shows that in the past 30 days, the issuance of various fiat currency reserve-type stablecoins on Ethereum has increased by more than 50%.

What is the current status of the stablecoin market? What challenges do you face? The research team of HashKey Capital, a leading digital asset investment institution in Asia, recently completed a report that deeply analyzed the feasibility, stability and potential risks of stablecoins, as well as the size, trend, use scenarios and regulatory issues of stablecoins.

After carefully studying the theory and various practices of stablecoins, please allow us to quickly give some overall views on the development of stablecoins:

- The fiat currency reserve type stable currency is currently the most feasible and stable mechanism with the widest demand.

- Risky assets with over-collateralized stablecoins have deficiencies in the mechanism, and algorithmic central bank-type stablecoins are not feasible.

- Stablecoins are still a long way from large-scale commercial applications, and need to overcome issues such as compliance, privacy, and limited application scenarios.

Stablecoin is a blockchain-based payment tool designed to achieve crypto asset price stability. Some stablecoins use fiat currencies as collateral assets, some use risky assets for over-collateralization, and some try algorithms to achieve price stability. Stablecoins provide a method of value measurement and storage for the crypto asset ecosystem, but how to break through the crypto asset ecosystem and enter the financial system and payment field is the goal of this article.

For specific analysis, we present in two parts: the first part introduces the main types of stablecoins and the economic analysis of their feasibility, stability and potential risks; the second part introduces the development of stablecoins and their scale , Trends, and usage scenarios to analyze and discuss the regulatory issues involved with stablecoins.

The main design types of stablecoins

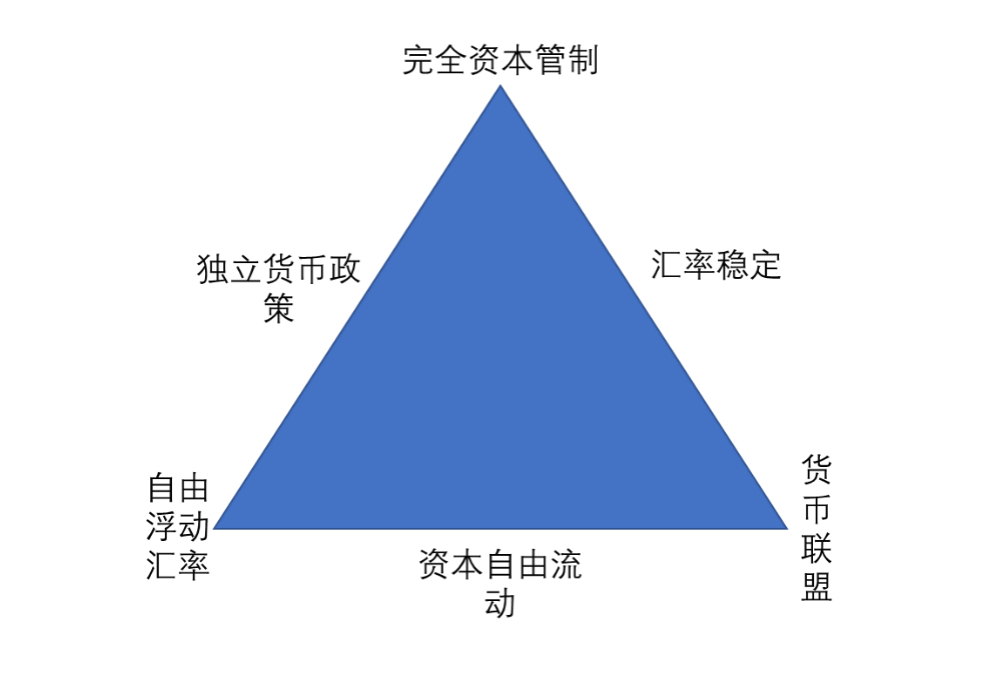

The stablecoin follows the "impossible triangle" (Figure 1): Each stablecoin system arrangement can only achieve a maximum of two policy goals (that is, two edges adjacent to the corresponding vertex), and basically it is impossible for the three goals With. If you want both the exchange rate stability and the free flow of capital (corresponding to the free exchange of stable and fiat currencies), you can only abandon the independence of monetary policy (that is, become a "currency union").

Figure 1: Impossible triangle of stablecoins

According to the stability mechanism used by stablecoins, we can divide stablecoins into three categories: fiat currency reserve support type, risky asset excess mortgage type, and algorithmic central bank type.

Fiat currency reserve support

The value of fiat currency reserve-backed stablecoins comes from fiat currency reserves. Users exchange stablecoin with stablecoin issuers at a ratio of fiat currency 1: 1. The stablecoin issuer opens a bank account and relies on a centralized custodian institution to host the user's fiat pool. The structure can be regarded as a digital bank deposit. The stablecoin exchange object can be the original issuer or a third party holding stablecoin or fiat currency. This stablecoin is similar to the mechanism in which the US dollar is linked to gold in the Bretton Woods system.

The fiat currency reserve type stable currency is currently the largest and most widely used, and is the type of stable currency with the highest market share. USDT issued by Tether, TrueUSD issued by TrustToken, USDCoin issued by Circle, etc., and the two stable coins GUSD and PAX approved by the New York Financial Services Authority are all such stable coins. The most representative of which is USDT.

Issuing mechanism

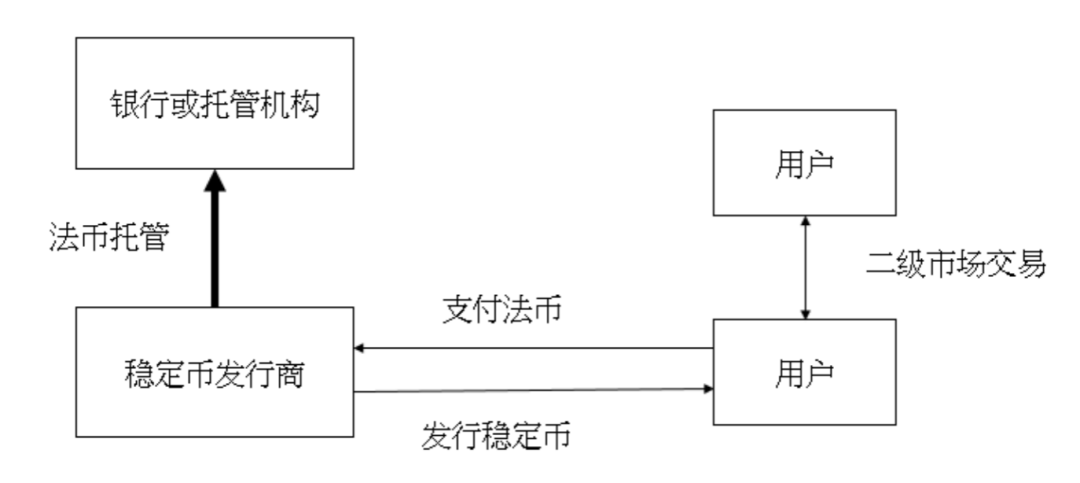

The fiat currency reserve type stable currency can be divided into two types according to the issuing mechanism, the Money Service Business model and the Trust Company model.

Figure 2: Fiat currency-based stablecoin issuance mechanism

- Trust Agency Model

The stable currency issuer under the trust institution model needs to obtain a trust institution license, which has the nature of fund custody. This type of stablecoin issuer not only bears the obligations of user funds custody, but also is a stablecoin issuer, subject to strong government supervision. Gemini and Paxos are the only stablecoin issuers currently licensed by a trust institution. In addition to being able to host digital assets, it can also host fiat currency assets, securities and gold, with a broader business scope.

Compliance is a major advantage for trust institutions, with trust concessions approved by the New York Financial Services Authority (NYDFS) to the highest level of regulation currently. The government has the power to freeze accounts and audit account balances. The trust will purchase insurance for the fiat currency reserve, store the funds in a segregated account, and the bank account where the fund pool is located is protected by the US Federal Deposit Pass-through Insurance, with a coverage of $ 250,000. The USDT parent company Tether has opaque funding conditions, which often raises regulatory concerns, and the openness and transparency of the trust institution model is market competitive.

- Money Provider Model

Treasury service providers are registered in the United States under the MSB model and cooperate with traditional trust institutions to issue stablecoins. The specific mechanism is as follows: The user transfers US dollars to the cooperative trust institution, and the cooperative trust institution sends information to the stablecoin issuer to confirm the purchase behavior. The stablecoin issuer then releases stablecoins to users. Under this mechanism, the fund service provider model only involves the issuance of stablecoins and has no fund custody nature. The fund service provider model is subject to audit and strict legal supervision. TUSD and USDC currently fall into this category.

There are two main differences between the money service provider model and the custodian institution:

- The former does not assume escrow funding obligations, but instead transfers risk to banks that are more closely regulated. The latter involves hosting business.

- The former business license scope is limited to digital assets, but the business development flexibility is strong, as long as the business does not involve security digital assets (Security Token), there is no need to report to the regulatory agency.

Stability mechanisms and economic models

Fiat currency reserve-type stablecoins must follow three rules to maintain stability.

- Issuing rules: Centralized trusted institutions issue stable 1: 1 relationship based on mortgage fiat currency.

- Two-way exchange rules: Centralized trusted institutions ensure two-way 1: 1 exchanges between tokens and mortgage fiat. The user mortgages 1 unit of fiat currency to the centralized trusted institution, and the centralized trusted institution issues 1 unit of stable currency to the user. The user returns 1 unit of stablecoin to the centralized trusted institution, and the centralized trusted institution returns 1 unit of mortgage fiat currency to the user.

- Credibility rules: Centralized trusted institutions must be regularly audited by third parties and fully disclose information to ensure the authenticity and adequacy of the mortgage fiat currency used as a token issuance reserve.

Constrained by these three rules, the stability of fiat currency-type stablecoins is controllable, and the core lies in arbitrage: as long as there is a high-liquidity redemption channel, you can find spreads and arbitrage in the market. This type of stablecoin has the same value of fiat currency endorsement, and users expect the mid-to-long-term market price to converge to the anchor price. Once the market price deviates from a reasonable range, there is profit margin, which can attract stablecoin users to participate in market regulation.

The asset side of the balance sheet of the fiat currency mortgage-type stable currency issuer is the fiat currency reserve, and the liability side is the stable currency. The goal of the fiat currency reserve is to guarantee the payment of fiat currency when someone redeems the stablecoin. 100% legal currency reserve is the most direct and effective way to achieve full payment of stable currency. However, according to the large number theorem, it is impossible for all holders of stablecoins to request conversion into fiat currencies at the same time.

Theoretically, it is not necessary to hold 100% of the legal currency reserve to be able to meet the demand for stablecoin redemption most of the time. If the stablecoin price is allowed to fluctuate slightly and the stablecoin redemption is controlled in extreme cases, it should be possible to reduce the requirements for fiat currency reserves and realize stablecoins at a lower cost, but it means greater risk. In this case, in addition to the revenue generated by the actual demand scenario, fiat currency stablecoin issuers also have two parts of economic revenue: coinage tax and fiat currency reserve management revenue.

First look at the coinage tax. If the stablecoin does not have a 100% fiat currency reserve, the issued stablecoins will not have the fiat currency reserve as support, but it also meets the needs of stablecoin holders, which is equivalent to issuing a portion of stablecoins "in a vacuum". These stablecoins have purchasing power in the real world, corresponding to the concept of coinage tax. This is the case for USDT. Although there are many doubts about USDT in the market, there has been no centralized and large-scale redemption of USDT (of course, USDT parent company Tether has also imposed various restrictions on redemption). Suppose that over a period of time, the supply of stablecoins has increased by ΔM, and the current price level is P. The issuer of stablecoins can issue stablecoins through vacancies and can purchase goods and services in the market with a quantity of ΔM / P. Mint tax. In the USDT scenario, P can be understood as the price of Bitcoin.

Secondly, look at the benefits of reserve management. In addition to a portion of the fiat currency reserve, which is invested in highly liquid assets that can be realised at any time, the remaining portion can be invested with higher risks to obtain higher returns. Because the stablecoin issuer does not pay interest to the holder, the reserve management proceeds are all owned by the stablecoin issuer.

There is a risk

- credit risk

There are two sources of credit risk for stablecoins. First, the credit risk of stablecoin issuers comes from the uncertainty of the internal rescue capacity of stablecoin issuers when the currency price is de-anchored. Coinage taxes and gains from management of reserves may pose a moral hazard for stablecoin issuers and ultimately manifest themselves as credit risk. If a stablecoin issuer is overly pursuing coinage tax and reserve management benefits, increasing the stablecoin amount / fiat currency reserve ratio indefinitely, or the proportion of fiat currency reserves used as high-risk investment, will hurt the stability of the stablecoin. Persistent. When there is a centralized, large amount of stablecoin redemption, the issuer may not be able to pay fiat money. In addition, opaque asset reserves and poor governance are among the risk points for stablecoin issuers.

Second, the credit risk of centralized custodians. The credit risk of fiat currency custodian institutions is affected by a variety of factors, including factors such as the regulatory level of the institution's location and its own risk control capabilities. For example, the fiat currency received by stablecoin issuers is deposited in a particular bank, which is located in a country with a poor deposit insurance system. If the bank suffers a major operational crisis such as bankruptcy, the stablecoin issuer will face default risk.

- Lack of liquidity

In a payment system with a very large amount of liquidation, if the reserve of a commercial bank in the central bank is difficult to meet the payment needs, the central bank will satisfy it by overdrawing the commercial bank (called intraday credit). The issuance of stablecoins is limited by the balance sheet and lacks flexibility. It may be difficult to play a good payment and settlement function when the amount of liquidation is large.

Risky asset excess mortgage

Such stablecoins are issued through over-collateralized risk assets, most of which are 1: 1 anchored in USD. The risk assets currently used for collateral are mostly crypto assets. The risk asset price has high volatility and cannot support the value of the stablecoin when the price plummets, so excess collateral is necessary. Most risky assets with over-collateralized stablecoins use regulated guarantee ratios and liquidation thresholds to stabilize currency prices. Dai, Havven, BitUSD belong to this category.

Issuing mechanism

There are usually four roles involved in the risky asset over-collateralized stablecoin ecosystem.

- Governance agency. The governing body decides the liquidation threshold, guarantee ratio and handling fee, and is responsible for adjusting parameters and maintaining the stability of the currency price.

- Keeper. Stabilizers are driven by economic incentives and participate in auctions of debt and collateral when liquidating collateral. Another function of the stabilizer is to stabilize the price of the currency. When the market price is de-anchored from the anchor price, the stabilizer stabilizes the market price and the anchor price by buying or selling stablecoins.

- Oracles. Stablecoin issuers need a predictor to provide real-time price information on mortgage assets and decide when to liquidate. The stablecoin issuer also needs to stabilize the market price of the currency in real time to determine whether the price of the currency is off anchor.

- Stablecoin users. In the process of exchanging stablecoins, users need to establish a mortgage position and transfer the collateral into the position. Then, the user determines the amount of stablecoin he needs to exchange according to the value of the collateral, and the corresponding amount of collateral in the position is frozen. Finally, when a user wants to redeem a mortgage asset, he must repay the debt in the mortgage position and pay a handling fee.

Stabilization mechanism

Risky asset over-collateralization has the characteristics of highly volatile mortgage assets and requires an appropriate stabilization mechanism. There are four stabilization mechanisms for risky assets with over-collateralized stablecoins:

- Arbitrage mechanism

Theoretically, the anchor price to market price ratio is 1: 1. When the stablecoin market price is lower than the anchor price, users can purchase stablecoins in the secondary market at a lower cost, and liquidate the mortgage positions in advance to exchange them for collateral. Instead, increase the exchange of stablecoins and sell arbitrage in the secondary market.

But in fact, the arbitrage mechanism of risky assets over-collateralization is not as effective as in the legal currency reserve-type stable currency. Take Dai as an example. When the market price of Dai rises to $ 1.01, the arbitrageur will spend $ 1 to buy ETH worth $ 1 and generate Dai. At present Dai's guarantee ratio is 150%. By collateralizing 1 USD of ETH, the arbitrageur gets 0.67 Dai. Arbitrageurs can sell 0.67 Dai at a 1% profit premium.

However, the ETH arbitrage mortgage is still locked in the mortgage position and cannot be redeemed. ETH is a highly volatile asset. It has been locked for too long in the mortgage position, and needs to bear the risk of ETH falling. Unfavorable arbitrageurs control the income. And arbitrageurs need excess capital costs (33%) for mortgage arbitrage, which further reduces the efficiency of arbitrage.

- Guarantee ratio and liquidation threshold

In response to the high volatility of risky assets, stablecoin issuers will set guarantee ratios and clearing thresholds. Among them, the guarantee ratio = the value of the collateral / the value of the stablecoin released, usually between 120% and 250%. This mechanism guarantees that the value of the collateral is higher than the value of the released stablecoin. When the ratio of the value of the collateral to the price of the stablecoin is below the liquidation threshold, the system will ask the user to make up the position. If the position is not filled for a period of time, the system will forcibly liquidate the mortgage position, and the stabilizer will participate in the mortgage auction.

- Stabilization fee

The stabilization fee is the most important way for MakerDAO to stabilize the price of the currency, and it is expressed in annual percentage income. The mechanism of the stabilization fee is as follows: When a user redeems a mortgage asset, in addition to repaying the debt in the mortgage position, a stabilization fee must be paid. The stabilization fee is paid by the owner of the mortgage position using MKR, and the MKR used for payment will be destroyed.

In theory, when the stable fee rate is increased, returning Dai in the future to exchange for ETH mortgage assets will require higher costs (pay with MKR). Rational investors will choose not to produce Dai, and the supply of Dai will decrease, and the price may rise; otherwise, the supply of Dai will increase and the price will fall. This is the theoretical basis for MakerDao to maintain Dai and USD 1: 1 anchoring.

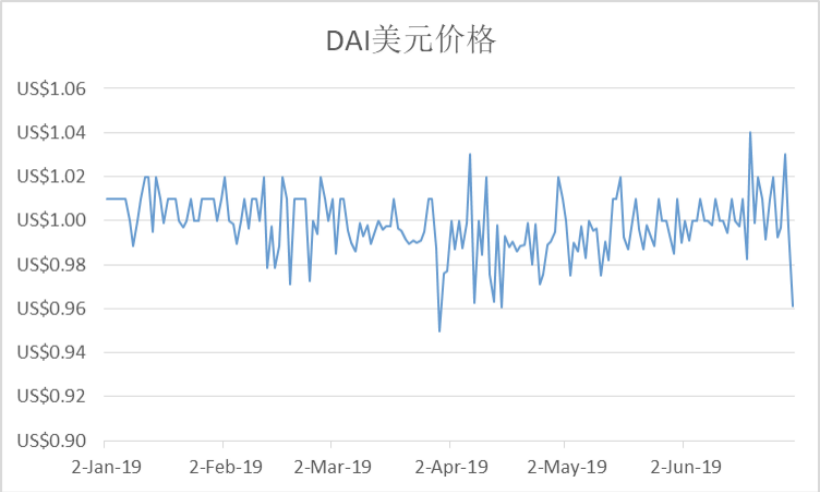

According to CoinMarketCap data, since February 2019, Dai prices have been below $ 1. The governing body initiated a vote to raise the stabilization rate and bring Dai back to the anchor price. From January 2019 to May 2019, MakerDao raised the stability fee a total of eight times, from 0.5% to 19.5%, an increase of 39 times.

Figure 3: Dai USD Price

As can be seen from the figure above, adjusting the stabilization rate is not an effective price stabilization mechanism. Stability rates cannot be compared with central bank policy rates. When the central bank raises interest rates, the demand for consumption and investment by people and businesses will decrease, which will reduce the money supply; the conversion of some short-term liquid funds into longer periods to obtain high interest income will also reduce the money supply. It is not direct enough to reduce the supply of Dai by increasing the stable rate. The effect remains to be seen. And so far, the use of Dai for users is mostly leveraged investment. The adjustment of Dai's stable rate cannot affect the market supply and demand structure, especially during the upward period of ETH prices.

- Global clearing

When a black swan event occurs in the market and the collateral quickly depreciates, the system will fail to clear the collateral and cause the liquidation mechanism to fail. Therefore, the risky asset over-collateralized stablecoin system will set up a global clearing mechanism. Global liquidators are designated by the governing body and have the right to terminate the entire system in exceptional circumstances. When the global clearing is started, the system will freeze, and all the stablecoin collateral positions will be forcibly liquidated by the system at the market price and the collateral will be returned.

Feasibility and risk

From the collapse of the crypto market on March 12, 2020, it can be found that leveraged investments within the DeFi ecosystem pose great risks to MakerDAO. Beginning in 2020, investors expect half of Bitcoin, making the market dominated by long positions, and many investors use leverage. There are two main leveraging behaviors in the DeFi ecosystem:

- Generate dai by pledged ETH in MakerDAO, and then use Dai to buy coins for investment.

- Financing by collateralizing coins in DeFi decentralized lending. The leverage in the DeFi ecosystem has multiple layers of nesting, there are obvious procyclicality and instability, and there are two levels of risk:

- Congestion risk on the chain

This time the market fluctuates violently, causing the panic withdrawal demand of ETH and ERC20 Token to increase, which makes the Ethereum network congested. Users actively raise Gas fees to speed up the transfer efficiency, which in turn makes Gas daily transaction costs increase sharply. The large market fluctuations also caused ETH of MakerDAO's large number of mortgage debt positions to fall below the liquidation threshold, triggering the liquidation process.

Originally according to MakerDAO's system settings, the liquidated collateral had a discount compared to the market price, which could attract stable people to participate in auction debt, and the successful bidder could get at least a 3% discount. However, those who should participate in the liquidation process cannot set a bid because the lower gas value is set. In a bidding environment where no other competitor is bidding, a stabilizer wins all liquidation debt with 0 DAI. MakerDAO has incurred $ 4 million in bad debts for this purpose and will need to auction its internal MKR to repay these debts.

The first phase of the debt auction was completed on March 19, and the second phase is underway. A total of 17,637 MKRs have been sold for a total price of 4.3 million Dai. The average price of a single MKR is 245.97 Dai, which is slightly lower than the current market price of 259.84. MakerDAO made a mechanism improvement on the risk of congestion on the chain and added an auction fuse mechanism: When the market fluctuates sharply, MakerDAO can suspend collateral auctions.

- Procyclicality due to high leverage

MakerDao's core mechanism is to over-collateralize ETH to lend Dai, which is leveraged in nature. When market sentiment is good, users will use repeated collateral ETH and lend Dai to invest, cycling to increase leverage. When the ETH price drops sharply, the guarantee ratio will drop sharply. Once the guarantee ratio is lower than the liquidation threshold, the mortgage debt positions will be liquidated in batches, and the cyclically enlarged leverage will double the default position. The liquidation of mortgage debt positions means that ETH as collateral is sold, which will further magnify the decline in ETH prices.

Algorithmic central bank stablecoin

Algorithmic central bank stablecoins do not have collateral assets as a value support, and a stablecoin system with smart contracts as the core. Algorithmic central bank-type stablecoins rely on algorithms to create "algorithmic central banks" to balance market supply and demand: When the market price is lower than the anchor price, smart contracts recover or destroy a certain percentage of stablecoins, reducing market supply and promoting market prices to rise . When the market price is higher than the anchor price, the smart contract issues a certain number of stablecoins, which expands the market supply and promotes a reduction in market prices. The advantage of algorithmic central bank-type stablecoin lies in its independence, which is not affected by the value of mortgage assets. The main projects are Basis, Nubits, uFragments, and Reserve.

However, although these projects have their own stabilization mechanisms, they have all experienced large-scale decoupling of currency prices and are difficult to recover. For example, NuBits has experienced two decouplings. The declining currency price has caused panic stablecoin holders to sell NuBits in large quantities, which has caused the price to collapse, and since then the currency price cannot be anchored at $ 1. Each NuBits is now about $ 0.03, with historical volatility of about 40%.

Theoretically, the main risk of algorithmic stablecoin is that it is not easy to regulate and control monetary policy. When large-scale market panics occur, the currency price is easily decoupled. When the market price is lower than the anchor price, the algorithmic central bank stablecoin will issue discount bonds to recover the stablecoin. If the market loses confidence in stablecoins, bonds will be difficult to issue. Even if issued, the bond issue price will be greatly discounted to the face value, reducing the effect of liquidity recovery. And when the bond matures, it will be accompanied by a net placement of liquidity. This is the main reason why algorithmic stablecoins are difficult to establish.

Development of stablecoin

Scale and development trend of stablecoin

Market value

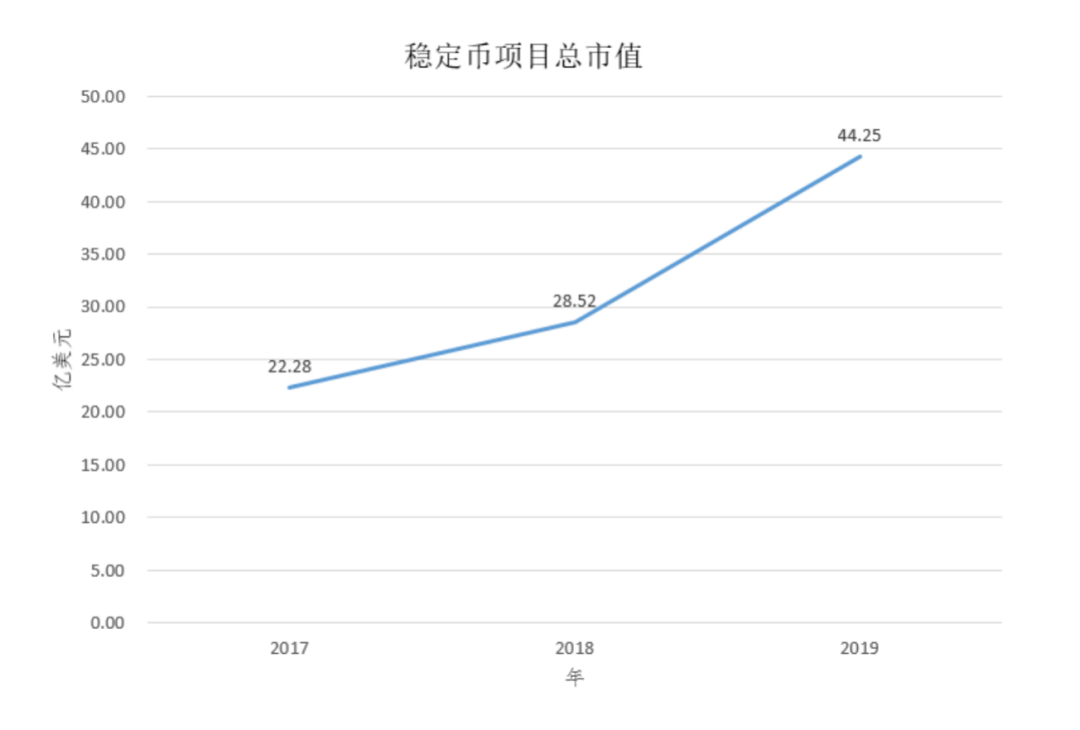

In 2019, a total of more than 237 billion dollars of funds were transferred to the chain through stablecoins. The total market value of the stablecoin has also climbed from $ 2.8 billion to $ 4.4 billion.

Figure 4: Total market value of stablecoin projects

USDT (the Omni protocol based on Bitcoin and the ERC-20 protocol based on Ethereum) accounts for 80% of the total market value of stablecoins, exceeding the total market value of other stablecoins. USDC and Paxos rank second and third respectively, accounting for 9% and 4% of the total market value of stablecoins, respectively. From the perspective of time changes, we can find three phenomena:

- GUSD has experienced a sharp decline in market share since mid-2019, and the current market share is less than 1%. There may be two reasons for the decline in GUSD market share: insufficient liquidity. Paxos, USDC, and TUSD are listed on the Binance exchange and all work with major exchanges. GUSD's liquidity is clearly insufficient. The discount plan failed. At the end of 2018, Gemini launched a campaign to purchase $ 1 worth of GUSD for $ 0.99, hoping to increase GUSD liquidity. However, Gemini has insufficient selectivity for users when distributing discounts, and most of the discounted GUSD falls into the hands of arbitrage traders. They convert these GUSD into other stable or fiat currencies at a ratio of 1: 1 to earn arbitrage profits.

- The launch of multi-collateral Dai has significantly increased the market share of Dai.

- The legal currency reserve stable currency market accounts for nearly 98%, which is the mainstream of the market today.

Figure 5: Changes in the market share of stablecoins, excluding USDT

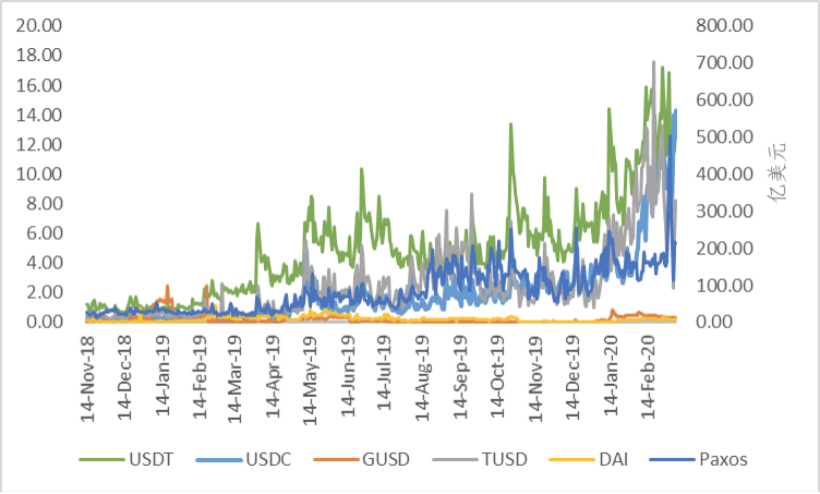

Trading volume

The average daily trading volume of stablecoins is USDT, which accounts for about 95% of the total. According to CoinMarketCap data, the 24-hour trading volume on March 9, 2020 reached 54.7 billion U.S. dollars. The following figure is a line chart of the historical stable trading volume of the top six stable currency transactions. The main coordinate is the USDT transaction volume and the secondary coordinate is the other stable currency transaction volume.

Figure 6: Daily trading volume of stablecoin

Two phenomena can be found: First, from the end of 2019 to March 2020, the average daily trading volume of stablecoin has increased by 200% -300%. This phenomenon can be attributed to the 40% rise in Bitcoin during this period. Second, the risky asset over-secured stablecoin is represented by Dai, and the transaction volume has increased by about 300% in 2019, which is close to the fiat currency reserve-type stablecoin GUSD.

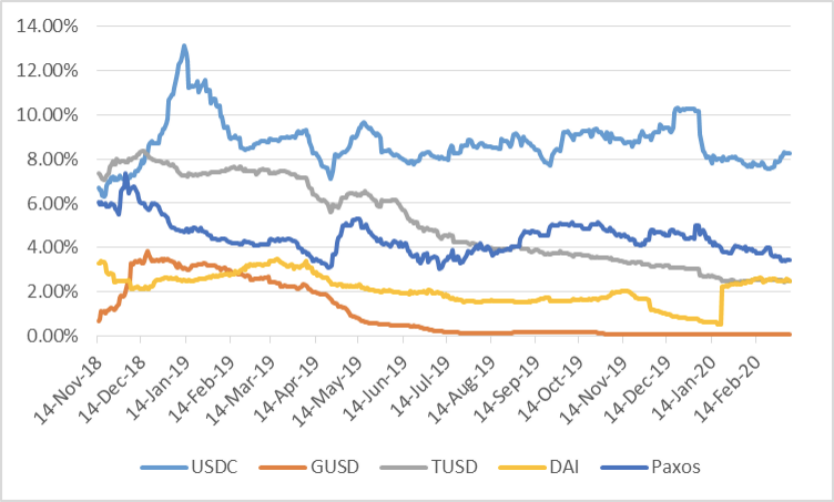

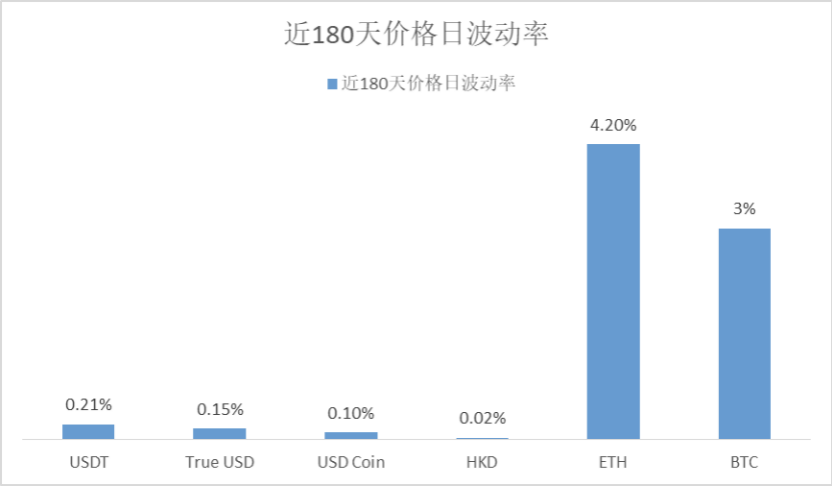

Volatility

At present, the fiat reserve-backed stablecoins on the market mainly use the US dollar as the anchor fiat currency, such as USDT, TUSD, GUSD and USDC. The chart below shows the daily volatility of each stable currency and Hong Kong dollar against the US dollar. The daily volatility of the stablecoin is approximately 5-10 times the exchange rate of the Hong Kong dollar and the US dollar, and between 5% and 10% of the crypto assets. Although stablecoins can already be used as a value storage or payment method in the crypto asset ecosystem, the stability of stablecoins compared to foreign exchange currencies is still somewhat different.

Figure 7: Daily price volatility of stablecoin, Hong Kong dollar and crypto assets for nearly 180 days (%)

trend

From the above statistics, it can be found that the compliant fiat reserve currency has gradually become the USDT's biggest competitor. At the end of 2019, USDT issuer Tether was once again in dispute over the adequacy of fiat currency reserves. The dispute revolves around Tether's solvency and liquidity. Tether has acknowledged that the balance of fiat currency reserves is insufficient.

Unlike Tether, USDC is issued by a regulated financial institution. The issuing company Circle behind USDC has payment licenses in the US, UK and EU. The characteristics of USDC's transparency and security, multi-national regulatory credit endorsements, and a more standardized financial audit mechanism have all become bright spots in the competition. After the USDT's insufficient fiat currency reserves, from October 2019 to February 2020, the average daily USDC transaction volume increased by more than 500%. The volume of Paxos and TUSD also increased by 300%.

In the future, we can expect a competitive landscape of "one super and many strong" in the stablecoin ecosystem. Despite frequent compliance issues with Tether, USDT still dominates the market. There are two main reasons:

- User inertia. Cryptocurrency investors themselves have a high tolerance for risk. Most users pay more attention to the operational experience such as convenience and mobility. At present, USDT is the most important legal currency deposit channel for users, and users' trading inertia is strong.

- Ecologically complete. USDT is listed on almost all exchanges, with sufficient liquidity and a good trading medium, and the exchange has a large reserve of USDT. If the USDT market collapses, the exchange will face severe losses.

Application of stablecoin

Crypto Asset Trading

Currently, the largest use case of stablecoins is crypto asset trading, as the largest medium for fiat currency deposits. The main places to buy digital currencies are major trading platforms, and many of these trading platforms do not support direct conversion of digital currencies into digital currencies. Users need a relatively stable digital currency as an intermediary to exchange. For traders, stablecoins are more cost-effective, procedures and processes are simpler, there are many exchanges supported, and there is no need to involve banks or other intermediary structures.

Crypto asset traders often convert crypto assets into stablecoins to temporarily “lock in” profits, thereby shifting their exposure to relatively stable assets, especially when the crypto asset market is volatile. Similarly, crypto asset miners convert their crypto assets into stablecoins to reduce their directional risk to the mined crypto assets.

Pay

The stablecoin payment application is divided into two parts: First, the global stablecoin led by Libra. Second, private stablecoin issuers, such as Coinbase, Paxos, and Terra. The first is limited in length and will not be discussed here. We have analyzed it in a special article. Currently, privately issued stablecoins are more used for crypto asset transactions, but attempts in the retail payment field have gradually increased.

Coinbase Commerce's payment service Coinbase Commerce added USDC, which it co-developed, to one of its payment channels in May 2019, and has completed more than $ 50 million in retail payments. Coinbase aims to drive the retail payment customer base through the USDC crypto asset transaction customer base.

Paxos has partnered with debit card publishers Spend.com and Crypto.com. Users holding Paxos stablecoins can be used directly for daily payments. Consumers pay through Paxos to enable partner merchants to receive payment immediately, eliminating merchants' settlement risk using credit card systems.

Regulatory issues related to stablecoins

Stablecoins have the characteristics of many crypto assets, as well as the attributes of traditional finance. The multi-financial nature of stablecoins increases the complexity of regulation. The regulatory issues involved in stablecoins can be divided into three parts: the establishment of legal entities, financial anti-money laundering and tax issues.

Legal entity

At present, the legal entity of stablecoins has not yet reached a conclusion. The legal entity of stablecoin is firmly established in a clear and complete contract between the user and the stablecoin issuer. The contract should disclose the rights and obligations of both parties, including:

- Whether the internal relief mechanism guarantees sufficient liquidity for users.

- Establish the equity and legal structure of stablecoin issuers.

- Establish the financial attributes of the stablecoin and the attribution of the revenue of the fiat currency pool.

Financial anti-money laundering

Stablecoin brings new risks to money laundering and terrorist financing. Although the decentralized nature of stablecoins is not controlled by individuals or groups, stablecoins have the nature of fund transmission and receipt, which is in line with the definition of the Money Service Business (MSB) of the Financial Crimes Enforcement Network (FinCEN) under the US Treasury. The FATF has also established a new regulatory framework for AML / KYC, requiring stablecoin issuers to propose KYC solutions. How to expand business in the field of compliance in the future will become a topic for stablecoin issuers.

tax

Stablecoin poses two challenges to tax regulation.

- The legal entity of the stablecoin is uncertain, so the obligation to tax the stablecoin transaction cannot be determined. For example: The price of stablecoin fluctuates in the secondary market. Users have capital gains in the process of purchasing and redeeming stablecoins. Should they declare capital gains tax? The different tax treatments across jurisdictions complicate the tax treatment of stablecoins.

- The stablecoin has become one of the tax avoidance channels. Although judicial institutions in various countries can regulate the flow of stablecoin issuers, the flow of funds in their accounts is difficult to identify. The transfer of funds in stablecoin accounts involves gift tax and inheritance tax. It is difficult for regulators to track Ultimate Beneficial Owners of a transaction for taxation.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Discussion on anti-counterfeiting, anti-intrusion and tampering, and blockchain technology to improve the security of drone operations

- Super Planet Token GDP Price "Zeroed" Issuing Convertible Bonds With Annual Interest Rates Up To 250%

- Former CFTC Chairman: Satoshi Nakamoto's white paper does not include concepts aimed at breaking away from government or regulatory networks

- Coins Story | Do you still love Bitcoin after the plunge?

- Foreign media: Binance plans to acquire well-known data service provider CoinMarketCap for $ 400 million

- QKL123 market analysis | Crude oil broke $ 20 in the intraday market, the smoke-free smoke war spread to the capital market (0331)

- Lightning Labs launches digital authentication method based on Lightning Network, users do not need to enter a password to log in