BCG Boston Consulting Analysis Report: Financial + Blockchain, Going Out喧嚣

Author: He Dayong, Tan Yan, Jia Hua, Lai Wah, Sun Lei

Source: BCG Boston Consulting (BCG_Greater_China)

The world today is experiencing a burst of application in the blockchain, and the disruption of blockchain is different for different financial institutions. For the future development of the blockchain, we must not be arrogant, nor blindly follow the trend, but should eliminate misunderstandings and understand its true value.

The rise of blockchain technology is mainly due to the reduction in storage costs. In the past, technological advances have reduced the cost of many things, making large-scale applications of many technologies possible. For example, in the past, large-scale computers were centrally calculated, and then PCs appeared, bringing large-scale commercial use; storage is the same. In the past, centralized storage, now because of the reduction in storage costs, each record can have 5,700 storages. Blockchain technology is another breakthrough digital technology after the Internet, and its essence is the deliberate squandering of storage space.

- Bitcoin has secretly submitted a listing application to the US SEC. The sponsor is Deutsche Bank.

- Babbitt Column | The Essence of Blockchain: The Essence of Computation and Consensus

- Jia Nan’s four wars IPO, but the time left for it’s transformation is running out.

In the real world, we have multiple ways to guarantee the authenticity and uniqueness of things, such as through signatures, passports and other documents, seals and notaries, trademarks, and so on. But in the virtual world, the data is dotted, and it is difficult to establish continuity. In the virtual world, we can't know many things, and we don't even know whether the other end of the Internet is a person or a dog. How to protect people in the virtual world is unique and true? The blockchain is mainly to solve the problem of continuity in the virtual world in essence, thus largely solving the trust problem in the virtual world. Blockchain technology features include distributed storage, time series, full chain consensus, and smart contracts that trace the original source of digital currency/digital assets to prove their authenticity; and all transactions are verified across the network to ensure unique transactions. It can be said that the blockchain forms continuity without intermediation.

Three major mistakes

In the face of blockchain technology, we are awe-inspiring, but at the same time there are many misunderstandings:

Myth 1: Blockchain is a new, cutting-edge technology

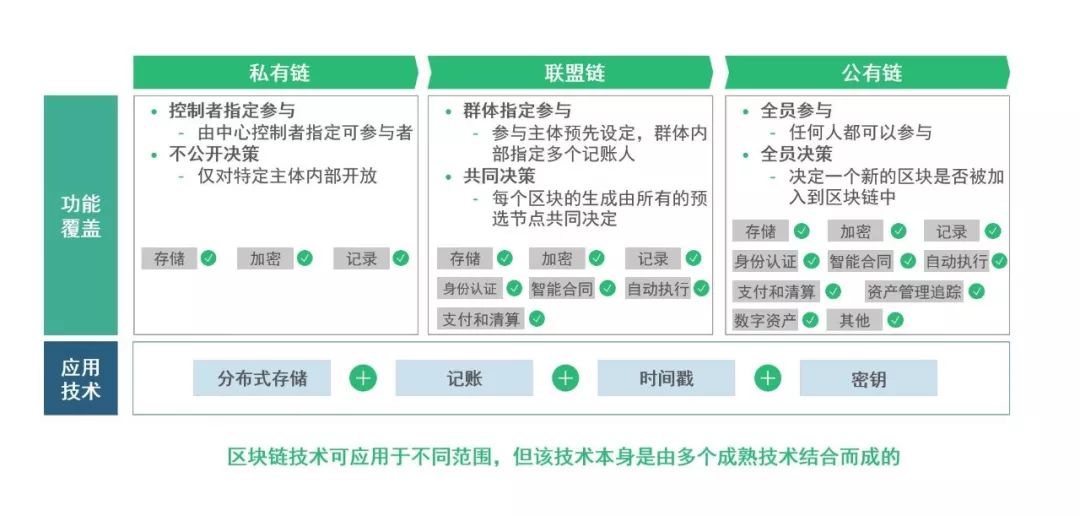

In fact, a careful analysis of the functional coverage of the private chain, the alliance chain, and the public chain reveals that blockchain technology is shared and derived from a variety of mature technologies , including distributed storage, accounting, timestamps, and keys (see figure). 1). Figure 1 | Blockchain technology is shared and derived from a variety of mature technologies.

Source: Literature search; BCG analysis.

Source: Literature search; BCG analysis.

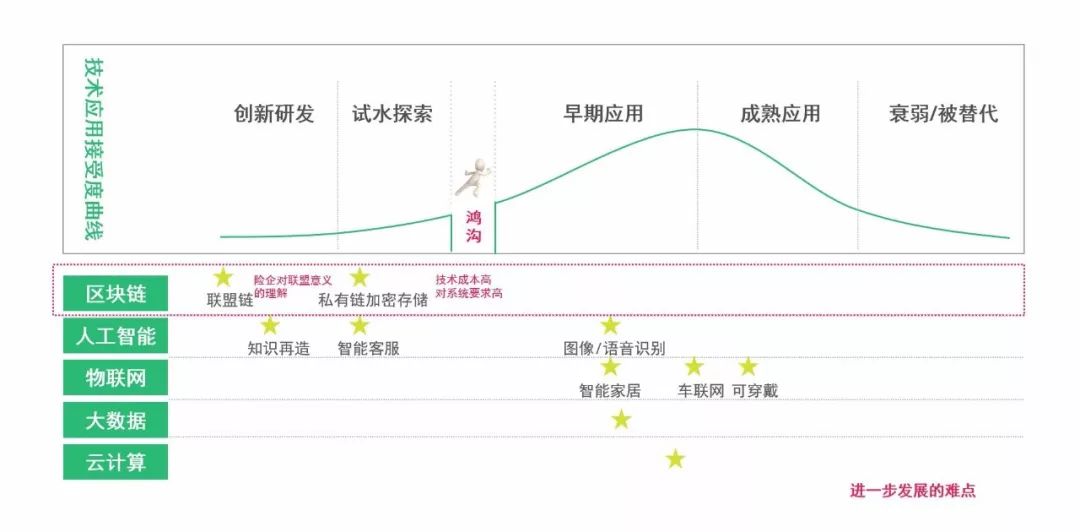

According to the Gartner technology maturity curve, blockchain technology has entered the high expectations of the tuyere. However, the application of blockchain in the financial industry has not yet been fully popularized . Taking the insurance industry as an example, the blockchain technology is still in the early stages of R&D and water testing. It faces two difficulties: first, the understanding of the meaning of the alliance by insurance companies; second, the high cost of the blockchain technology and high requirements for the system. These two difficulties make certain barriers to the widespread use of blockchains (see Figure 2).

Figure 2 | Blockchain technology is still in the early stages of development and testing in the insurance industry

Source: BCG analysis; Gartner database.

Myth 2: The blockchain itself can guarantee the data is true, safe and valuable.

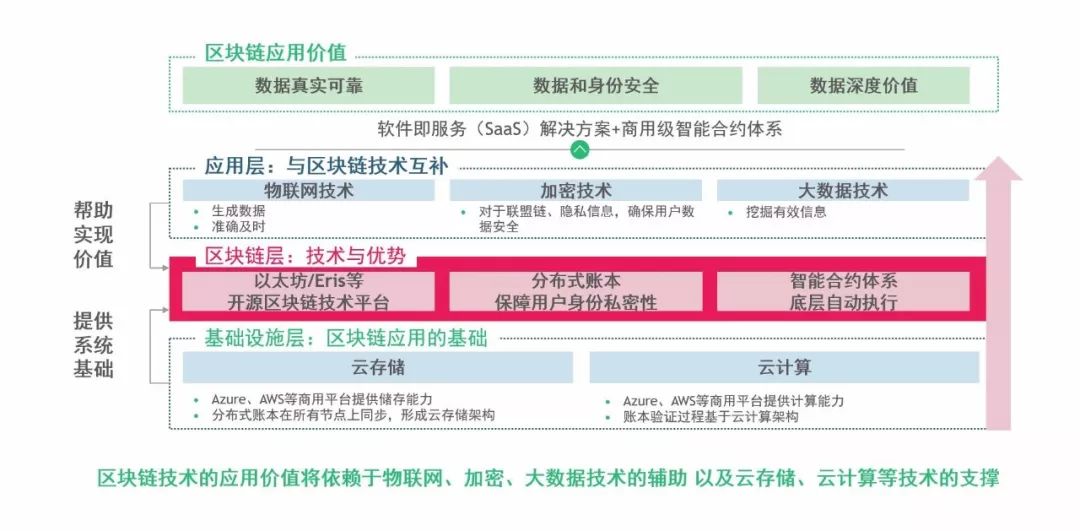

In fact, the application value of blockchain technology will depend on the support of Internet of Things, encryption, big data technology, and the support of cloud storage and cloud computing. At the application layer, the Internet of Things technology generates data accurately and timely, encryption technology ensures user data security, and big data technology can effectively mine information; at the infrastructure layer, the cloud storage platform provides storage capacity, and distributed ledgers are synchronized on all nodes to form Cloud storage architecture, and the book verification process needs to be based on cloud computing architecture. Therefore, blockchain technology is inseparable from the assistance and support of these related technologies (see Figure 3). Figure 3 | The application value of the blockchain is inseparable from the support and support of related technologies.

Source: BCG analysis.

Myth 3: Blockchain can be completely deintermediated

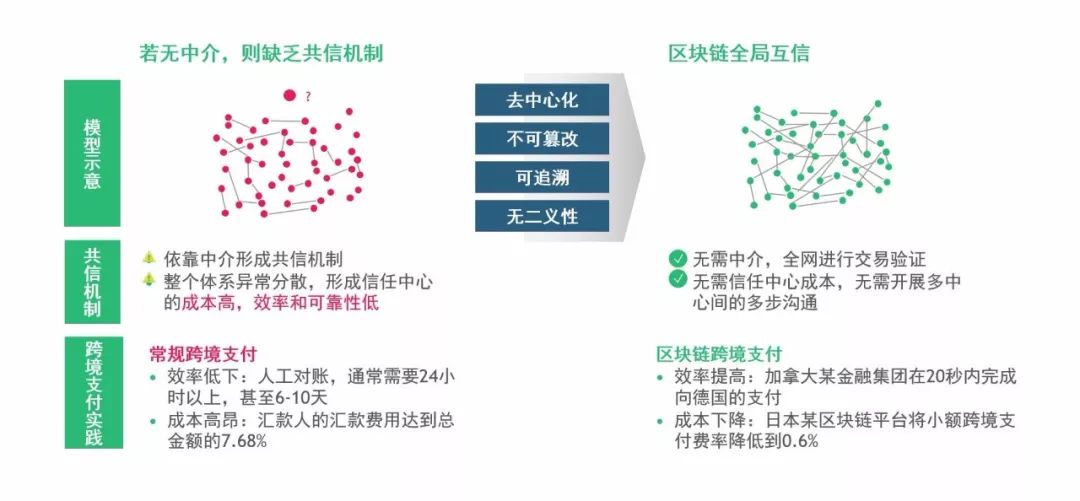

In fact, the mediation value is compressed, but the mediation function cannot be completely replaced. We divide the whole intermediary link into six parts: information collection, information storage/encryption, information matching/exchange, information verification, credit guarantee, and contract execution. The blockchain technology still relies on traditional information collection and credit guarantee links. Intermediary, decentralization does not mean going to an intermediary, taking Facebook Libra as an example (see Figure 4). Figure 4 | Mediation value is compressed, but mediation functionality cannot be completely replaced

Source: BCG analysis.

Avoiding the misunderstanding, we can see that the technical characteristics of the blockchain determine the nature of the blockchain: first, decentralization; second, not tamperable; third, traceable; fourth, unambiguous. Decentralization is the calculation and storage on all nodes, all nodes on the chain have the same rights; can not be falsified, that is, each node has a complete backup of all records, if you want to tamper, you must master more than 51% of the computing power; Traceability means that each record contains a unique timestamp, and each record is connected to the previous one; no ambiguity means that the law, regulations, and operations are represented by codes to avoid the inherent ambiguity of the words. These four technical characteristics determine the nature of the blockchain and determine the basic principles of its value.

Four value principles

From the nature of the blockchain, it can be inferred that the blockchain technology will highlight its value under four conditions, which we call “the four value principles of blockchain technology”: multi-participation, complex transactions, sensitive information transmission, The regulation is highly transparent.

1 multi-participation

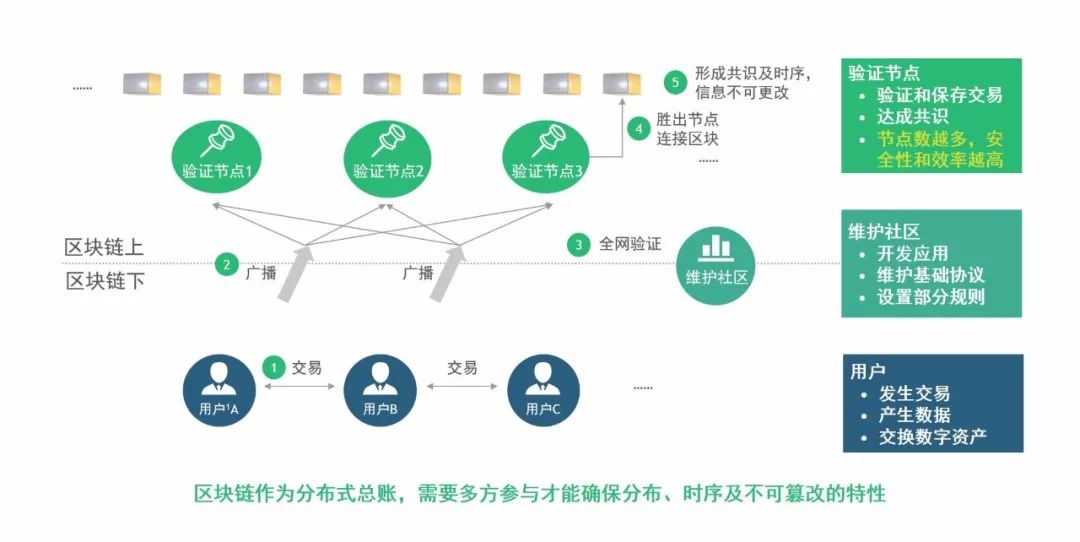

In the past, because of the lack of sharing mechanisms, many intermediaries were needed to function. The decentralized traits of the blockchain can exert great potential and reflect the necessity of the blockchain. The global mutual trust mechanism of the blockchain can effectively coordinate global sharing. The more participants, the lower the mutual trust cost . Therefore, blockchain technology can be better applied to payment systems and digital currency systems (see Figure 5). Figure 5 | In a multi-participatory system, trust centers are often not formed, and blockchains have great potential for application.

Source: BCG analysis.

In fact, only a multi-party participation can form a blockchain . Even a private chain requires multiple verification nodes to be placed on the blockchain. Each user can verify the node, and the verification node can verify and save the transaction. The more nodes, the higher the security and efficiency of the entire blockchain. At the same time, the blockchain acts as a distributed general ledger and requires multiple parties to ensure distribution, timing, and non-tamperability (see Figure 6).

Figure 6 | Blockchain can only be formed by multi-party participation, even for private chains, multiple verification nodes need to be placed on the blockchain

Source: BCG analysis.

[1] The user refers to the transaction user of the blockchain token or digital asset, and can receive or issue the token through the App, but not necessarily as the verification node.

For example, in complex international trade, due to the complexity of participants, such as customs, domestic logistics, freighters, freight forwarders, insurance companies, banks, etc., many services, especially financial services, require repeated certification, while blockchain technology is based on simultaneous sharing. The advantages of process control and risk independence can avoid repeated verification between multiple parties, and use IoT technology to master the entire trade process and real-time underwriting for specific risks (such as maritime transportation), thus greatly improving trade efficiency.

2 complex transactions

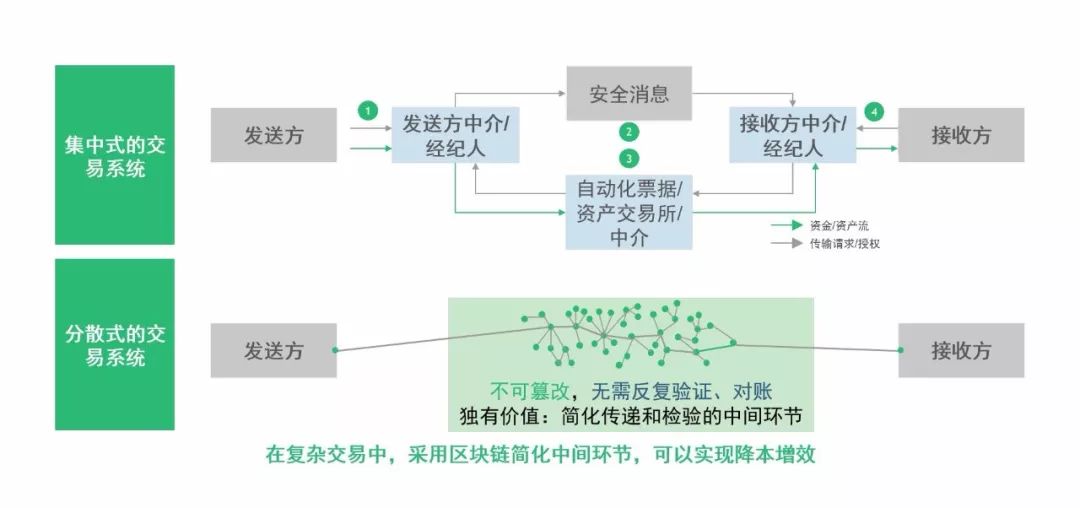

In some scenarios, the process is complicated due to the trust problem, and there are many situations where information is asymmetric and inefficient. The distributed system of blockchain technology cannot be tampered with, and everyone can see it through their own authority. In this case, the value and necessity of the blockchain are reflected (see Figure 7). Figure 7 | In a complex trading scenario, the participants are complicated and inefficient due to trust issues, and the value and necessity of the blockchain is highlighted.

Source: “Future Financial Services”, World Economic Forum.

The most typical example of this is stock trading. Stock trading has the characteristics of multi-layer, real-time, dynamic and large-volume transactions. Take the NASDAQ exchange as an example. Prior to the application of blockchain technology in 2015, due to the brokerage system and multi-tiered custody, a transfer may involve more than a dozen intermediaries, which took about three days, and the error rate was basically For 20%, subsequent manual corrections are required, resulting in a large amount of back-end reconciliation and higher processing costs. After the blockchain technology, because the two parties can read and write a common error-free database, the entire reconciliation cost is saved, and the transaction is written in computer code, which reduces the possibility of errors, and the data is visible to the organization and facilitates supervision. In the case of complex transactions, the role of the blockchain is obvious.

3 sensitive information transmission

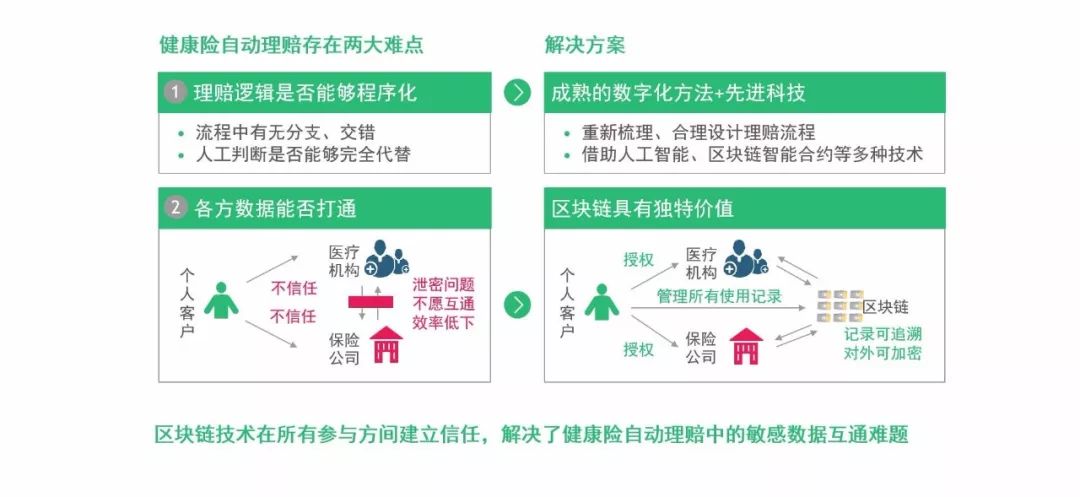

In the past, the transmission of sensitive information required a variety of verifications, the information was of low credibility and was difficult to authorize, resulting in poor continuity of information usage. However, after applying the blockchain technology, all the information is verified, and the participants open and trust each other, and the sensitive information is more authentic and reliable. In the scenario of sensitive information transmission, blockchain technology opens up relevant parties, greatly improving credibility and value is immeasurable. The blockchain has unique advantages in terms of confidentiality and flexibility in transmission. After implementing GDPR (General Regulations on EU Data Protection) in Europe in 2018, blockchain based on cryptographic privacy protection can better reflect value and strengthen information. Confidentiality. Taking insurance as an example, the blockchain can be applied in the field of automatic insurance claims. At present, the automatic insurance claims are mainly whether the claims logic can be programmed and whether the data of the parties can open up two difficulties. The blockchain technology establishes trust between all participants and can solve the sensitive data intercommunication in the automatic claims of health insurance. The problem (see Figure 8).

Figure 8 | In the field of automatic insurance claims, the blockchain can open sensitive data related to all parties and has unique value.

Source: BCG analysis.

4 highly transparent to regulation

In applications that require a high degree of transparency in regulation, the characteristics of the blockchain are equivalent to giving the regulator a universal key , which makes the blockchain of great value. This is in line with the customs lock principle of US Customs. When I was traveling, I knew that I had to lock the suitcase, but the customs needed to open the suitcase and finally solve it through a special customs lock. In terms of supervision, the blockchain is similar. If the regulator joins the blockchain, it can see more transaction information under the premise of ensuring security, which has great deterrent to anti-money laundering and internal transactions.

The three major risk blockchain technologies have received much attention, but it should be noted that in the development process, they also face certain risks.

1 scale

For blockchain technology, scale brings certain challenges while bringing certain benefits. At the same time, scale itself is also facing some resistance. The larger the scale, the more obvious the effect of blockchain technology to reduce costs; on the other hand, the larger the scale, the lower the marginal trust, that is, the higher the trust cost. In addition, too large a scale can lead to weak computing power. It is also a problem that the participants in the blockchain can be united in one heart and one mind. The expansion of the industry often relies on alliances, and alliance members are also competitors, and they are mutually restrained.

2 security

Blockchain is not absolutely secure, and the risk of hacking is always there. The blockchain uses encryption algorithms, but the information still needs to be encrypted. If a hacker successfully masters more than 51% of the computing power of the whole chain, he can preempt a chain of longer, forged transactions like a race, thus manipulating the block. chain. Therefore, it is necessary to maintain the blockchain in a timely manner and monitor it at all times, especially for sensitive information and high-value digital assets.

3 regulatory attitude

China has introduced a number of blockchain supervision policies, and has carried out blockchain supervision from multiple dimensions and multiple links. The main directions are: ICO financing behavior and financing penetration channels of blockchain projects, and manipulation of market and unprofitable projects. , with the "blockchain" as the scam project. On February 15, 2019, the Regulations on the Management of Blockchain Information Services issued by the State Internet Information Office was officially implemented. So far, China has basically completed the three-level supervision structure of the blockchain, that is, the network information office is the main body of the blockchain information service. The Ministry of Industry and Information Technology is the main body of the blockchain technical standards, and the local industry associations conduct self-discipline. Supervision. At present, national regulators are more supportive of blockchain technology, but for example, the central bank is both a setter, a regulator, and a competitor of digital currency. If the local currency is threatened, will it continue to support it? It is very likely that the digital currency will be stopped. For the application of blockchain, the attitude of supervision is always an uncertain risk. The application of blockchain needs to follow the multi-participation, complex transactions, sensitive information transmission, and high-transparency value principles to give full play to its advantages. At the same time, it should cope with the three core risks of scale, security and regulatory attitudes, and constantly improve its technology and model.

The application of blockchain in the financial industry and the technical nature of the prospective blockchain bring its unique value. Therefore, in the application of the financial industry, different financial institutions have different subversive capabilities. On the whole, it is more subversive for intermediary financial institutions, and it brings chain and point optimization to product-providing financial institutions. In terms of subversion, from strong to weak, it is payment, banking, securities, and insurance.

1 payment

The application of blockchain technology in the field of cross-border payment has solved major problems such as international interbank transactions, reconciliation and liquidation . A financial service institution in the United States has introduced cryptocurrency, which is a one-to-one exchange of US dollars to realize large-value payments between banks or countries, and immediate transaction settlement between institutional clients. A credit card giant and blockchain technology companies have jointly developed a blockchain-based cross-border payment platform to help address industry issues such as high cost of payment processing, liquidity management, insufficient standardization, and bank-to-domestic clearing system connectivity . In June 2019, Facebook released the Libra white paper on the digital currency project. As a cryptocurrency that anchors a basket of low-risk assets, Libra has a natural advantage in terms of value stability and data security. At the same time, the principle of blockchain value of multi-participation and complex transactions also empowers the concept of global currency in the era of digital economy. In terms of the clearing system , blockchain-based algorithmic ledgers eliminate the cumbersome process of arranging multiple sub-books for cross-border transactions, and use Libra's participants to work together to help cross-border trading networks improve clearing settlement efficiency and reduce transaction costs. In terms of credit system , the economic future of the chain born with Libra as the currency ruler may be derived from more complex fields such as asset management and insurance, and the blockchain can not be falsified in multi-level nested and multi-party transactions. Can significantly reduce the crisis of trust.

However, with the withdrawal of payment giants such as PayPal and Visa and Zuckerberg's fight against Capitol Hill, Libra is also under pressure from countries to supervise boycotts. On the one hand, the possibility of transnational capital alliances dividing the central bank's coinage rights and affecting the implementation of monetary policy has triggered concerns about monetary sovereignty; on the other hand, the decentralized and anonymized chain transaction characteristics have also increased regulation for foreign exchange control and funds. The difficulty of monitoring.

2 banks

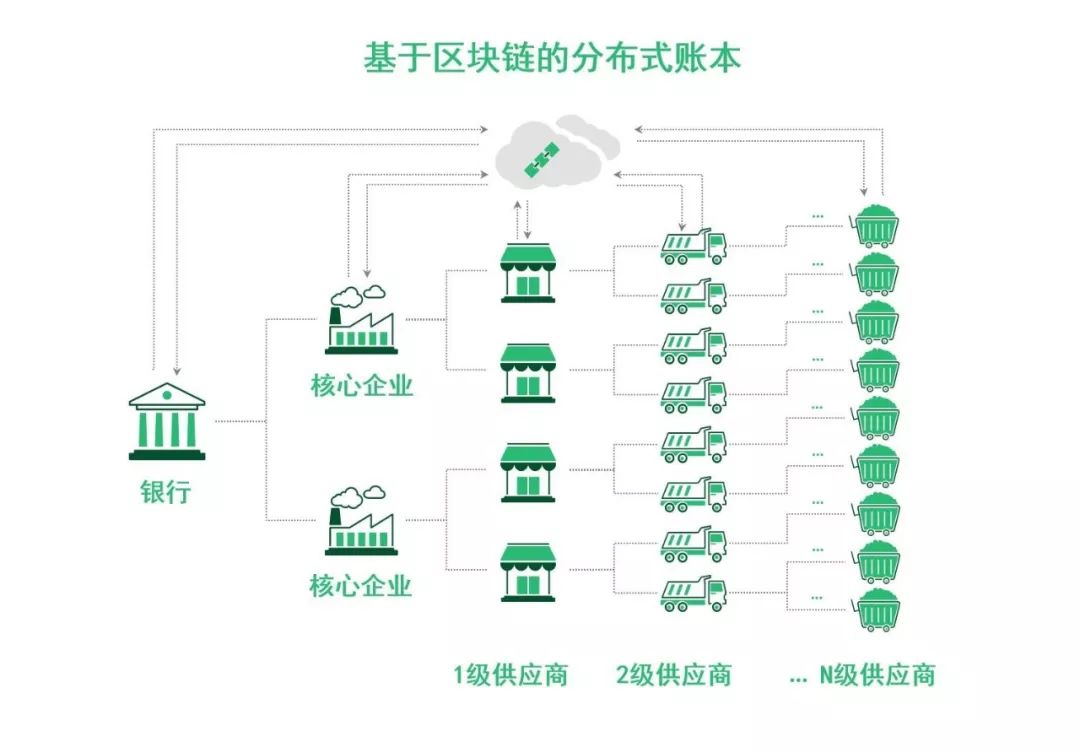

Blockchain technology can be applied to all aspects of the bank's value chain, helping corporate banks , retail banks and many other business lines to develop new business models, reducing costs and increasing efficiency while also preventing risks more effectively . In corporate banks , combined with electronic bills, smart contracts and other technologies, the blockchain-based supply chain financial business model is being widely studied and applied (see Figure 9). The transaction information of the core enterprise and its suppliers at all levels will be permanently recorded in the open distributed ledger in a verifiable manner, so that the core enterprise's credit can be effectively transmitted to different levels of suppliers, reducing fraudulent activities such as forgery transactions. risks of. Banks can differentiate pricing for different levels of suppliers and build a broad and stable customer base. At the same time, the digitization of the entire process makes the cost lower and more convenient and faster.

Taking a domestic joint-stock bank as an example, the bank launched a supply chain receivables service platform based on blockchain technology, and went deep into manufacturing and electronics industries to provide financing services for upstream and downstream suppliers of core enterprises. The platform builds distributed ledgers based on blockchain technology and directly connects with Zhongdeng.com to realize automatic registration of accounts receivable changes. There is no need to open an account when the supplier is financing, and the transaction activity does not need to be reviewed again, making the supply chain financial service more efficient, lower cost and more controllable.

Figure 9 | Corporate Banking, the blockchain-based supply chain financial business model is being widely studied and applied

Source: BCG analysis.

In retail banking , people are exploring the application of blockchain in data storage, identification, and KYC . For banks, establishing a data sharing and storage platform based on blockchain technology can not only save the cost and inconvenience caused by paper storage, but also enable the authorized parties in the chain to grasp the latest customer data information in real time and improve Risk scoring and anti-money laundering work results, reducing compliance costs; for customers, the simplification and efficiency of KYC processes will reduce customer time investment, avoid repeated submission of information, and enhance customer experience.

Unlike the mature applications in the public business, most of the blockchain applications in retail banking are currently in the R&D and proof-of-concept phase, but many banks have applied for patents to help the future, such as Barclays Bank for a brand new The KYC process for identity information storage based on the private chain has been patented.

In addition, for the monetary system , central banks are testing blockchain digital currency technology . Once promoted, users will share a monetary system and may form a new banking market (see Figure 10).

Figure 10 | Outside the existing banking system, the digital currency that countries are exploring may have a disruptive impact on the banking industry

Source: BCG analysis.

3 securities

The application of blockchain technology in the securities market can reduce agency agency costs in the four stages of securities issuance, pre-transaction, transaction execution, and post-transaction , improve post-transaction processing efficiency, and even replace existing systems . In the securities issuance process , at this stage, it is necessary to rely on the intermediary to provide services, and human intervention has moral and error risks. In the case where information transparency cannot be guaranteed, information collection and verification are inefficient and costly. Based on the blockchain technology, securities can be issued on the blockchain, and the blockchain can be used to connect the two parties, and the necessary information can be verified by multiple parties to reduce risks and costs.

Before the transaction , there is still a high cost of information collection and risk management at this stage. Using blockchain technology, market participants can share information on the blockchain, jointly verify and selectively open according to smart contract conditions, while ensuring security and reducing costs.

After the execution of the transaction and the transaction , the manual operation is still the main stage, and the error risk is high. The mediation, settlement, delivery, depository, custody and other services are completed by means of intermediary, which is inefficient and costly; the supervision is complicated and the information transmission efficiency is low. In terms of cost reduction, in the future, blockchain can be used instead of intermediary for transaction and post-processing, through programmatic certification, to reduce the risk of errors; reduce intermediate links, replace human operations, and reduce processing costs. In terms of efficiency , natural verification, delivery, and recording can be realized on the blockchain, and all parties can be verified by consensus. The transaction information is completely traceable, non-tamperable, open to supervision, and avoids the efficiency reduction caused by intermediation.

4 insurance

The blockchain will have three impacts on the insurance industry: tapping new markets, reducing costs and increasing efficiency. In the mining of new markets , there are some fragmentation, scenes, and decentralized insurance. Fragmentation insurance requires real-time tracking and segmentation coverage. In terms of time and space, the blockchain provides guarantee for its certainty; almost any scenario can be designed in the future, because blockchain technology insurance will become more scene-oriented; future insurance can be based on point-to-point insurance, insurance companies only need Provide platforms, data and other services to the insured.

In terms of cost reduction , limited time and space underwriting, accurate pricing, and the use of alliance blockchain, Internet of Things and other technologies can help insurance companies reduce investigation costs and reduce potential risks. In terms of policy management, the policy can be traced back and the cost of repeated verifications can be reduced. In terms of claims, automatic claims data interconnection, smart contract execution, reducing data check and underwriting costs.

In terms of increasing efficiency , the distribution negotiation process can be simplified. Taking the negotiation of a complex reinsurance industry as an example, the blockchain can greatly increase the efficiency of the negotiation process. For pricing, one-time underwriting, long-term tracking, and avoidance of repeated, the policy follows the insured will become a reality due to blockchain technology. In terms of policy management, timely tracking of policy restrictions, insurance transactions, pledges, swaps, reinsurance, etc. can be tracked by the provisions of the policy, improve efficiency and avoid post-inspection inefficiencies.

The future of the 5 blockchain

Throughout the development and evolution of blockchain technology, it can be found that the world is experiencing a burst of application in the blockchain (see Figure 11). Blockchain agreements and common standards are being widely developed, and regulators are constantly ensuring compliance while encouraging the healthy development of the blockchain industry. The application of blockchain began to emerge in a number of industries outside of finance, and the blockchain ecology began to breed unicorn companies. In the future, blockchain will be used in many industries, and new business models will emerge in the intersection of advanced analytics, the Internet of Things and blockchain-based smart contracts .

Figure 11 | Blockchain is rapidly evolving

Source: BCG analysis.

It should be noted that the blockchain will still face several challenges in its approach to large-scale applications.

On the market side , the standards between stakeholders have not been unified and there is no coordination mechanism. In order to apply the blockchain, companies need to adjust internal processes and provide relevant training advice.

In terms of technology , there are many blockchain platforms, which makes selection difficult. Many companies still don't understand what the blockchain can solve, and they are still in the stage of “making a blockchain for the blockchain”. The blockchain mainly handles distributed P2P transactions, and processing efficiency needs to be improved (VISA processes about 2,000 transactions per second, while Bitcoin can only process 7 transactions per second).

In terms of supervision , the standards are not uniform. The US Securities and Exchange Commission (SEC) classifies tokens as securities, ICO investors are subject to relevant regulatory policies; China bans ICO; Switzerland is loosely regulated and attractive to blockchain start-ups. Data protection laws can cause problems, blockchain nodes may cross jurisdictions, and EU new GDPR may raise legal and regulatory issues.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Why is the hash public key not resistant to quantum computing threats?

- Inside the ICBC internal digital wallet: China leads the currency trend for 3000 years

- Jianan Zhizhi prospectus full interpretation: 99% of revenue comes from mining machines and related sales, future growth bets on AI chips

- David Marcus: Libra's anti-money laundering standard is higher than other payment networks

- Bloomberg: The $5 billion encryption loan market is just a credit bubble that is about to burst?

- Vitalik: On the two-way bridging of eth1 and eth2

- Which block is the first benefit to the blockchain?