China Blockchain Investment and Financing Census Report: The financing amount is only a quarter of that in the United States, and the most popular in digital asset related fields

Author: Zhao Yue Zero One think tank

▪ There is still a gap in the development of the China-US blockchain industry. The amount of Chinese blockchain company / project financing is slightly higher than that of the United States, and the financing amount is only a quarter of that in the United States.

- Blockchain landing application inventory: five major areas of application tell you "what can the blockchain do"

- Regulatory review: China reorganizes, US expands regulation, India delays decision

- "Development Map of China's Blockchain Industrial Park" Released: Insight into the Development of the Park in Five Dimensions

▪ The agglomeration effect of the blockchain industry is beginning to appear. Blockchain companies / project financing are mainly distributed in the Bohai Rim, Yangtze River Delta, Guangdong, Hong Kong, Macao and Sichuan-Chongqing regions; Beijing has the largest amount of financing, accounting for 45%, and Hong Kong has the highest average single financing amount, reaching 262 million yuan.

▪ The scale of the blockchain industry is expanding. Blockchain companies / projects have gradually shifted from start-up financing (before round A) to mid-to-late stage financing, but still mainly concentrated before round A.

▪ Digital asset-related fields are still the most popular with capitalists, with digital asset-related financing accounting for 29%; digital asset-related industries are also the most “fund-absorbing” funds with a financing amount of 2.3 billion yuan. In addition, public chain projects have received increased attention.

▪ 68% of the 25 active investment institutions are new institutions focusing on the blockchain field, and they are mainly invested in five major industries including exchanges / trading platforms, industry websites & media, entertainment and social networking, blockchain communities, and digital currency wallets. None of them Institutional investment entities apply related industries.

With the increasing attention and attention of government departments, the blockchain has also been favored by the capital side. 2018 has become the "explosion year" of the blockchain industry. According to the incomplete statistics of the Zero One Think Tank, in 2018, the number of Chinese blockchain companies / projects reached 349 and the amount of financing reached 17.3 billion yuan.

On October 24, 2019, the Political Bureau of the Central Committee of the Communist Party of China conducted the eighteenth collective study on the current status and trends of the development of blockchain technology. General Secretary Xi Jinping pointed out that blockchain should be used as an important breakthrough in independent innovation of core technologies. This has given the blockchain a very high strategic significance and social value from the national strategic level. It is a cardiotonic agent for the blockchain industry, making the blockchain once again the focus of popular debate.

Overnight, blockchain has once again become a hot spot for capitalists. On October 28, 2019, blockchain concept stocks broke out collectively, with 40 stocks trading on a daily limit.

In order to observe the investment and financing situation of the blockchain industry in the past year (November 2018 to October 2019), Zero One Think Tank analyzed from the five dimensions of overall financing situation, geographical distribution, round distribution, field distribution and investor perspective. Provided an overview of the financing of Chinese blockchain companies / projects. The data shows that the development of blockchain companies / projects is gradually gradual, and capital investment in the blockchain industry is becoming more and more rational.

I. Overall financing situation: The capital side's investment in blockchain companies / projects is becoming more rational

According to incomplete statistics of the Zero One Think Tank, from November 2018 to October 2019, a total of 175 financing events occurred in the Chinese blockchain industry, and the total amount of publicly disclosed financing reached 4.189 billion yuan (converted at the opening exchange rate on October 31, 2019) , The same below).

The capital side's investment in blockchain companies / projects is gradually becoming rational. Compared to November 2017 to October 2018, the number of financing events decreased by 50% year-on-year, and the amount of financing decreased by 75% year-on-year. From November 2017 to October 2018, the number of Chinese blockchain companies / project financings reached 349, with a total financing amount of 17.078 billion yuan.

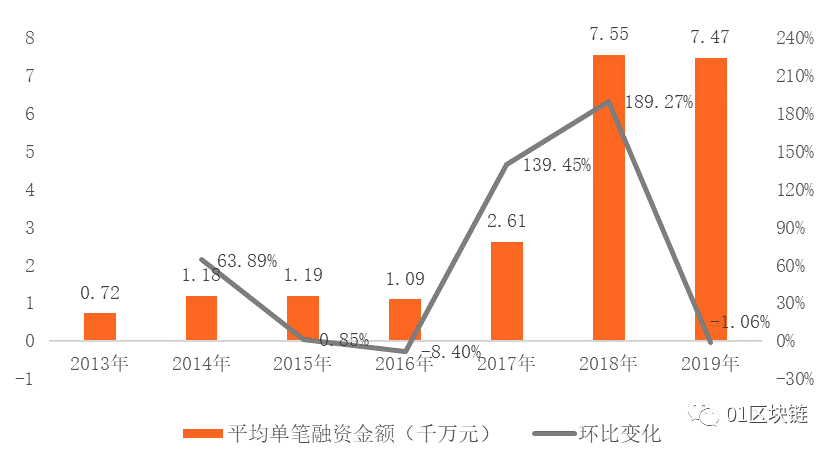

(1) The amount and amount of financing dropped significantly, and the average amount of single financing remained above 70 million yuan

Since 2013, the amount of financing and the amount of financing in the Chinese blockchain industry have generally shown an upward trend, and the changes in the amount of financing and the amount of financing have been highly consistent.

Among them, from 2013 to 2015, the amount and amount of financing in the blockchain industry have remained stable; since 2016, the amount and amount of financing in the blockchain industry have begun to rise significantly. 2018 is the "explosion year for blockchain project financing" "The number of financings was as high as 349, with a growth rate exceeding 340%, and the amount of financing was 17.3 billion yuan, with a growth rate of 876%. In 2019, the development of the blockchain industry has returned to rationality, and the amount of financing and the amount of financing have dropped significantly.

Figure 1 Financing of China's blockchain industry from 2013 to 2019

Source: Zero One Think Tank

Note: 1. The data for 2019 are from January 2019 to October 2019;

2. The financing amount only includes the amount of public disclosure.

From the perspective of the average single financing amount, from 2014 to 2019, the single financing amount of the Chinese blockchain industry is in the tens of millions, and the single financing amount is generally increasing year by year. Among them, in 2018, the single financing amount was the highest, reaching 75.5 million yuan; in 2016, the single financing amount was the lowest, being 10.9 million yuan, a decrease of 8.4% from 2015; compared with 2018, the single financing amount in 2019 was not Major changes have taken place and remain above 70 million yuan.

Figure 2 Amount of single financing from 2013 to 2019

Source: Zero One Think Tank

Note: 1. The data for 2019 are from January 2019 to October 2019;

2. Average single financing amount = publicly disclosed amount / publicly disclosed financing amount of projects.

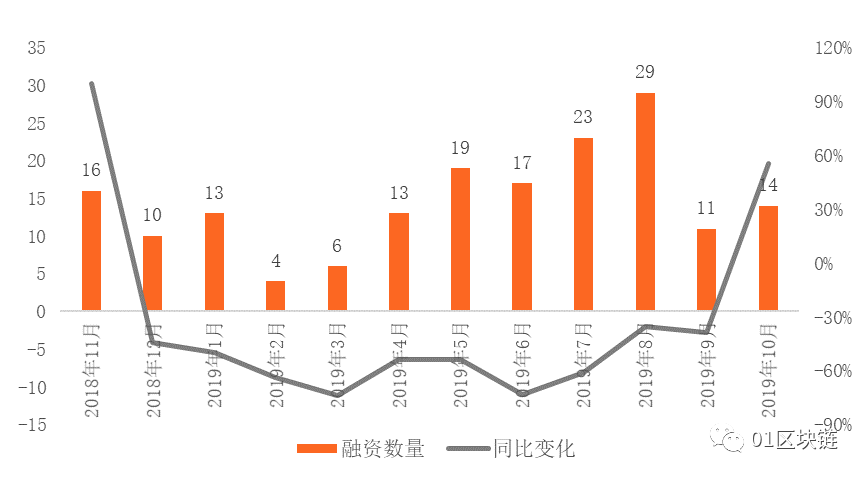

(2) The amount of financing in a single month decreased by about 30% to 80% compared with the same period last year.

From November 2018 to October 2019, the number of financing events in China's blockchain industry generally showed an upward trend. Among them, from February to August, the number of Chinese blockchain companies / project financing has shown a clear upward trend, with the largest number of financing in August, 29; in September, the number of blockchain project financing dropped sharply, compared with the previous quarter. Down 62%, down 39% year-on-year.

In addition, compared to the same period of last year, except for November 2018 and October 2019, the amount of financing in other months showed a different decline, with a decline between 30% and 80%. Among them, in March 2019 and June 2019, the amount of blockchain project financing fell by more than 73% year-on-year.

Figure 3 China's Blockchain Project Financing Volume and Changes from November 2018 to October 2019

Source: Zero One Think Tank

Note: 1. The data for 2019 are from January 2019 to October 2019.

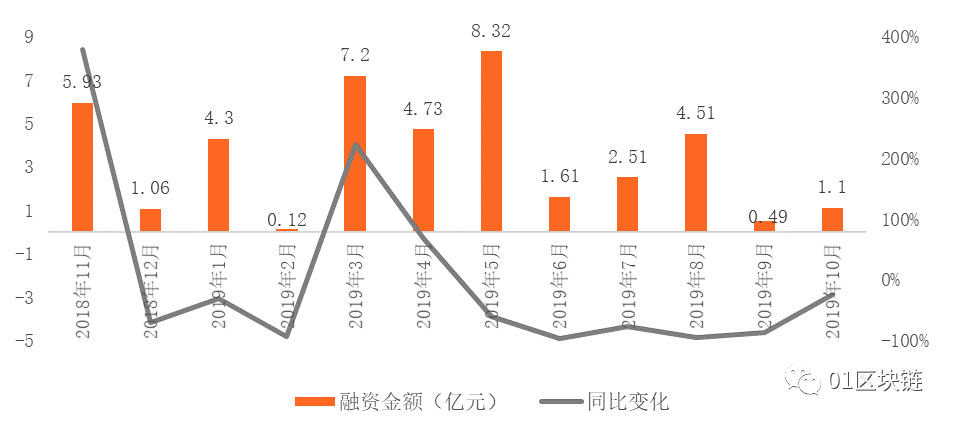

(3) The year-on-year decrease in the amount of financing in a single month is between 24% and 96%

In the past year, the total amount of financing publicly disclosed by the Chinese blockchain industry each month has not reached the level of 1 billion. Among them, in May 2019, the highest amount of financing for blockchain companies / projects was 832 million yuan, accounting for 20% of the total financing for the past year; in February 2019 and September 2019, the financing amount did not exceed 50 million yuan. The development of the blockchain industry is sluggish.

From a year-on-year change, compared with November 2017 to October 2018, the overall financing of blockchain companies / projects has shown a downward trend. Except for November 2018 and March 2019, the year-on-year decrease in the amount of financing in the remaining months was between 24% and 96%.

Figure 4 China's Blockchain Project Financing Amount and Changes from November 2018 to October 2019

Source: Zero One Think Tank

Note: 1. The data for 2019 are from January 2019 to October 2019.

From the perspective of the distribution of financing amount, excluding companies / projects that have not disclosed the financing amount publicly, over 62% of the blockchain company / project financing amount is above the tens of millions.

The number of projects with financing amounts between 10 million and 100 million was the largest, accounting for over 50%; the number of projects with financing amounts above 100 million was relatively small, accounting for only 12%.

Figure 5 Distribution of financing amount of China's blockchain projects from November 2018 to October 2019

Source: Zero One Think Tank

Note: 1. Excluding blockchain companies / projects that have not disclosed the financing amount publicly;

2. 100 million to 1 billion includes 100 million; 10 million to 100 million includes 10 million; 1 million to 10 million includes 1 million.

"Mining giant" Jianan Yunzhi and cryptocurrency project Proxicoin tied for the top 10 in financing amount, with a funding amount of 704 million yuan; the public chain project PERLIN ranked second; the investment and financing service platform immediately financial services and blockchain open source The platform AERGO ranked third; the investment agency TDE received a strategic investment of 197 million yuan, ranking fourth; the fifth ranked were the entertainment and social project NewStar, the vehicle data service platform DACH, and the cryptocurrency exchange kucoin; crypto The currency exchange BHex received 106 million yuan investment from Huobi Global Ecological Fund, OKEX Digital Information and Genesis Capital, ranking sixth.

Table 1 Blockchain companies / project financing amount Top10

Source: Zero One Think Tank

(4) The amount of financing in China is slightly higher than that in the United States, and the amount of financing is only a quarter of that in the United States.

Comparing the financing situation of blockchain companies / projects between China and the United States in the past year, a total of 175 financing incidents occurred in China, and the publicly disclosed financing amount was 4.189 billion yuan; a total of 147 financing incidents occurred in the United States, and the publicly disclosed financing amount reached 16.845 billion USD , 4 times the amount of financing in China.

In terms of the amount of financing, except for February 2019, June 2019 and September 2019, the number of Chinese blockchain companies / projects was higher than that of the United States.

In terms of financing amount, in March 2019, the amount of financing of Chinese blockchain companies / projects was higher than that of the United States. This situation mainly occurred because Jianan Yunzhi obtained a strategic investment of 704 million yuan. In May 2019, the U.S. blockchain company / project financing amounted to 7.367 billion yuan, 9 times that of China, mainly because the US cryptocurrency exchange Bitfinex raised 7.04 billion yuan through ICO.

Figure 6 Comparison of Sino-U.S. Financing from November 2018 to October 2019

Source: Zero One Think Tank

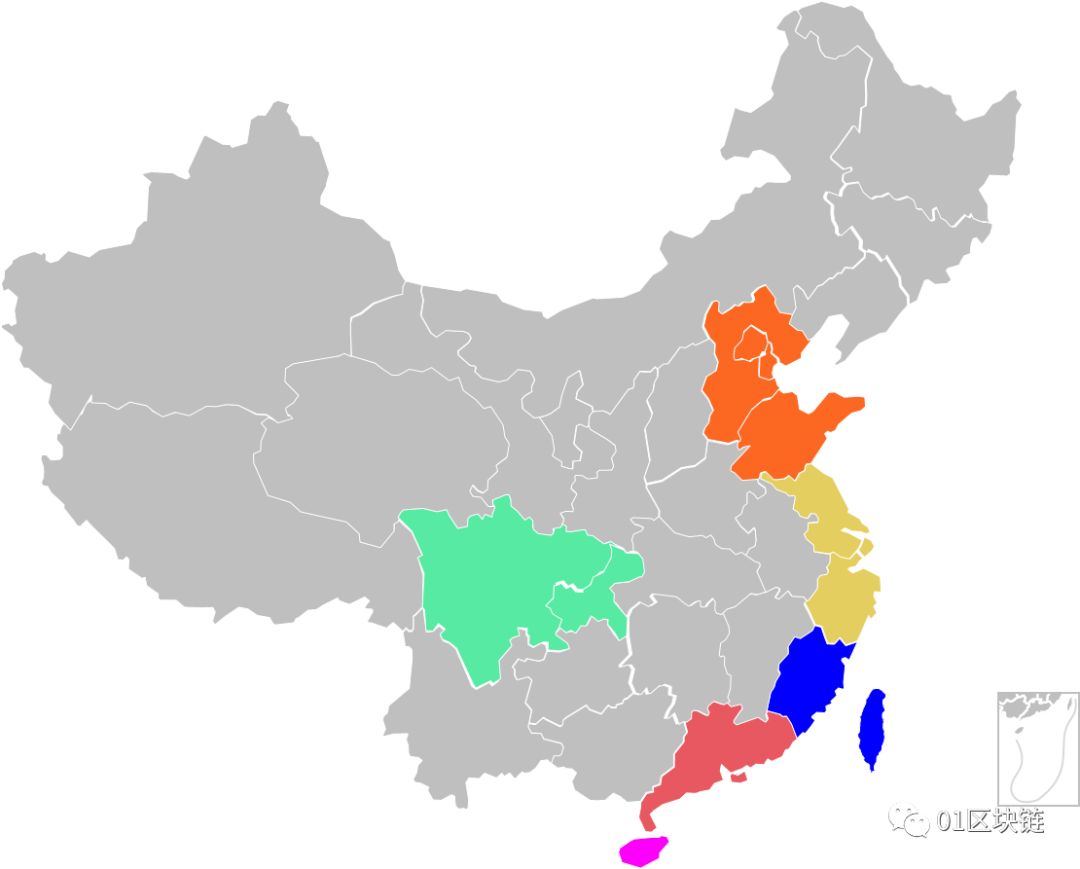

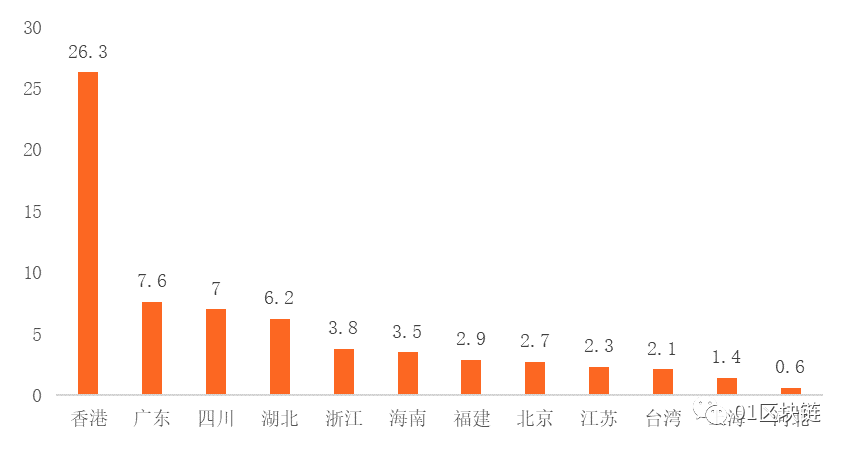

Geographical distribution: the agglomeration effect of the blockchain industry is beginning to appear

From the perspective of geographical distribution, Chinese blockchain companies / project financing are mainly concentrated in the Bohai Rim region, the Yangtze River Delta region, Guangdong, Hong Kong, Macao and Sichuan-Chongqing regions. These regions have developed economies, active innovation and entrepreneurship, and a sound industrial foundation, and have greater policy support for blockchain companies / projects. Taking Sichuan as an example, with the advantage of low electricity prices, nearly 50% of the world's mining activities are distributed in the Sichuan region.

Figure 7 Regional distribution of Chinese blockchain companies / projects

Source: Zero One Think Tank

(1) Beijing has the largest amount of financing, and Hong Kong has the largest amount of financing

In the past year, Chinese blockchain companies / project financing have been concentrated in Beijing, Shanghai, Zhejiang, Hong Kong and Guangdong.

Among them, Beijing blockchain companies / projects have the largest amount of financing, accounting for 45% of the national financing amount; Hong Kong blockchain companies / projects have the highest financing amount, reaching 1.313 billion yuan, followed by Beijing with a financing amount of 1.145 billion yuan. Although Shanghai has the second largest number of blockchain projects in the country, the amount of financing is relatively low, ranking sixth in the country.

Figure 8 Geographical distribution of Chinese blockchain companies / project financing from November 2018 to October 2019

Source: Zero One Think Tank

(2) The amount of single financing in Hong Kong topped the list, reaching 262 million yuan

Excluding areas where the amount of financing was not disclosed, it can be seen that the average single financing amount in Hong Kong is far ahead of other regions, at the level of 100 million yuan, reaching 262 million yuan; the average single financing level of 10 regions, including Guangdong, Sichuan, and Hubei At the level of tens of millions; there are more blockchain companies / projects in Beijing and Shanghai, but the single financing amount ranks behind.

Figure 9 Average Single Financing Amount of Blockchain Companies / Projects by Region from November 2018 to October 2019 (Unit: 10 million yuan)

Source: Zero One Think Tank

Note: The average single financing amount in a certain area = the total amount of publicly disclosed financing in a certain area / the amount of publicly disclosed financing.

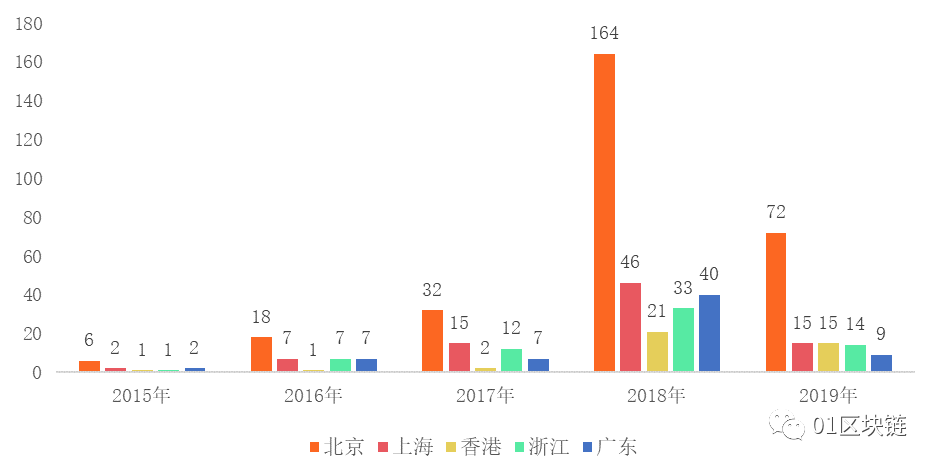

(3) Blockchain companies / projects in Beijing, Shanghai, and Zhejiang saw significant declines in financing

Select five regions where Beijing, Shanghai, Hong Kong, Zhejiang, and Guangdong have active financing of blockchain companies / projects. Through comparison, it has been found that in the past five years, the ranking of financing amount in each region has been relatively stable. Beijing has been the region with the largest number of financing, followed by Shanghai. In 2018, 164 blockchain project financings occurred in Beijing, accounting for 47% of the national financing volume.

Figure 10 Geographical distribution of Chinese blockchain companies / project financing in the past 5 years (by financing amount)

Source: Zero One Think Tank

Note: 1. The data for 2019 are from January 2019 to October 2019.

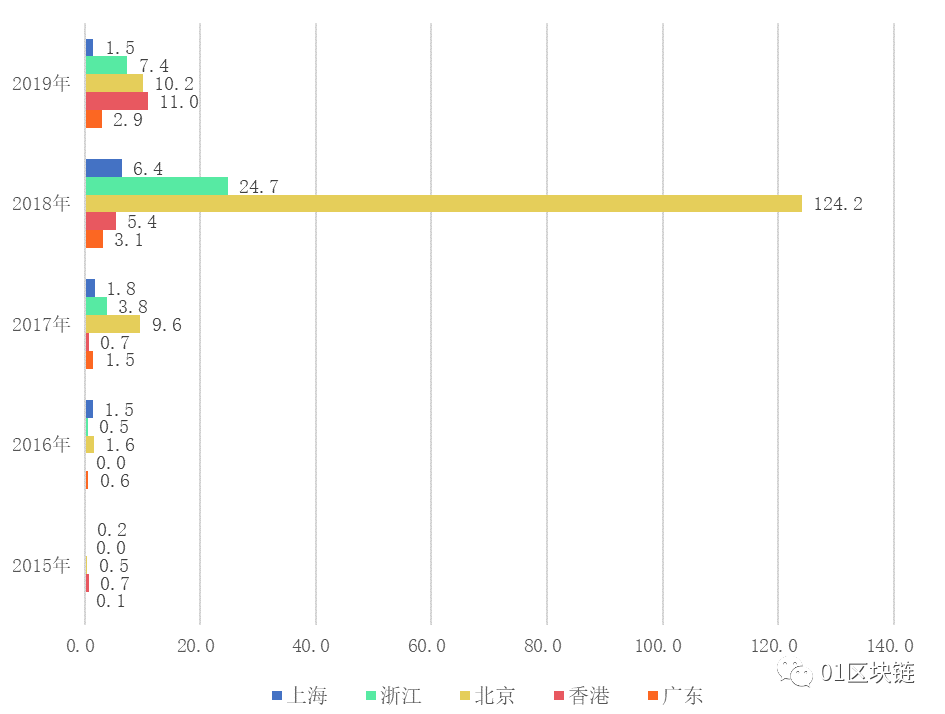

Looking at the financing amount of the above five regions, except for 2019, Beijing is the region with the highest financing amount of blockchain projects.In 2018, the national blockchain project financing amount was 17.298 billion yuan, and Beijing ’s total financing amount exceeded 71%. ; Compared to 2018, in 2019, the amount of financing of blockchain projects in Beijing, Zhejiang and Shanghai declined significantly, of which Beijing fell by 82%; Zhejiang fell by 70%; Shanghai fell by 76%.

Figure 11 Geographical distribution of China's blockchain project financing in the past 5 years (by financing amount)

Source: Zero One Think Tank

Note: 1. The data for 2019 are from January 2019 to October 2019.

3. Financing rounds: The development of blockchain companies / projects is still in its infancy

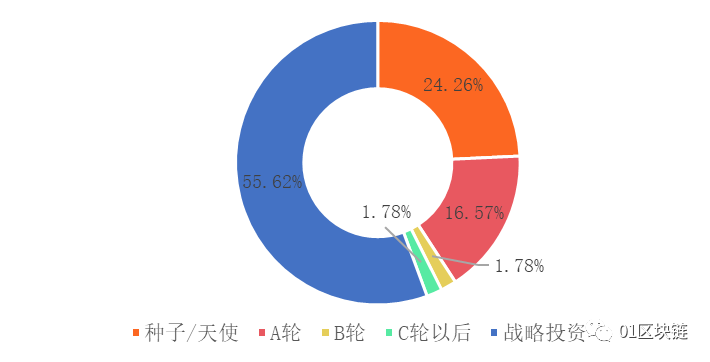

(1) Financing was mainly concentrated before round A, and only 6 rounds of financing occurred after round B

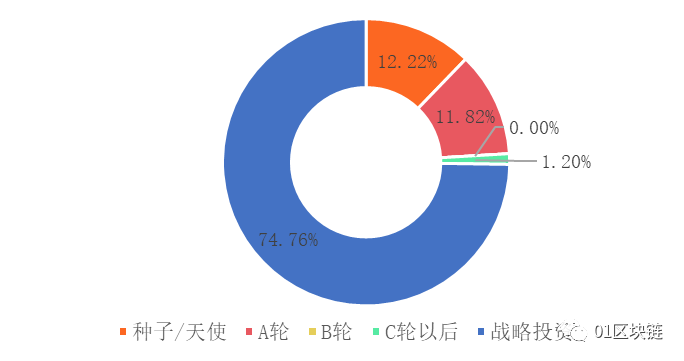

After excluding ICO, M & A, and projects without disclosed financing rounds, in addition to strategic investment, from November 2018 to October 2019, Chinese blockchain companies / project financing were mainly concentrated before the A round, the seed / angel round and the A Round blockchain projects account for over 40%. This shows that the development of Chinese blockchain companies / projects is still in its infancy.

Figure 12 Distribution of financing rounds of Chinese blockchain companies / projects from November 2018 to October 2019 (by number of financing)

Source: Zero One Think Tank

Note: Round A includes Pre-A, A, and A +; round B includes Pre-B, B, and B +; round C includes CG and Pre-IPO.

From the publicly disclosed financing amount, in addition to the strategic investment, the total amount of funding raised by the seed / angel round is higher, followed by round A. Since the amount of seed / angel round financing is more than round A, the seed / angel round is a single The financing amount is lower than the A round. The average single financing amount of the seed / angel round is 15.96 million yuan, and the average single financing amount of the A round is 23.52 million yuan.

Figure 13 Distribution of financing rounds of Chinese blockchain companies / projects from November 2018 to October 2019 (by financing amount)

Source: Zero One Think Tank

Note: Round A includes Pre-A, A, and A +; round B includes Pre-B, B, and B +; round C includes CG and Pre-IPO.

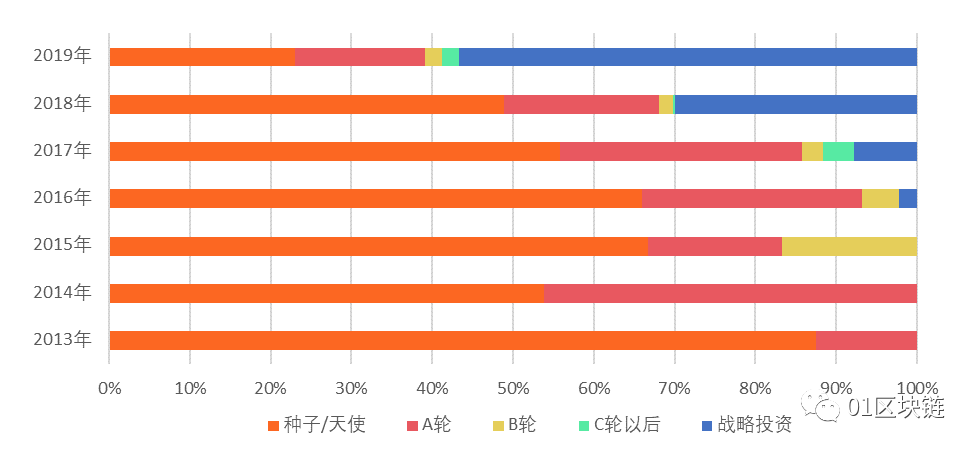

(2) The transfer of financing from the start-up period (before the A round) to the middle and late stages

Since 2013, China's blockchain companies / projects have gradually shifted from early stage financing (before A round) to mid-to-late stage financing, and the scale of the blockchain industry has gradually expanded.

In terms of financing volume, in 2013 and 2014, all Chinese blockchain companies / project financing were concentrated in the seed / angel round and A round. In 2019, the proportion of seed / angel round and round A financing dropped to less than 40%. The number of B rounds of financing has also been decreasing year by year, from 17% in 2015 to 2% in 2019. From 2013 to 2016, Chinese blockchain companies / project financing were mainly concentrated before the B round, and no financing after the C round occurred.

Figure 14 Changes in the distribution of financing rounds of Chinese blockchain companies / projects (by the amount of financing)

Source: Zero One Think Tank

Note: Round A includes Pre-A, A, and A +; round B includes Pre-B, B, and B +; round C includes CG and Pre-IPO.

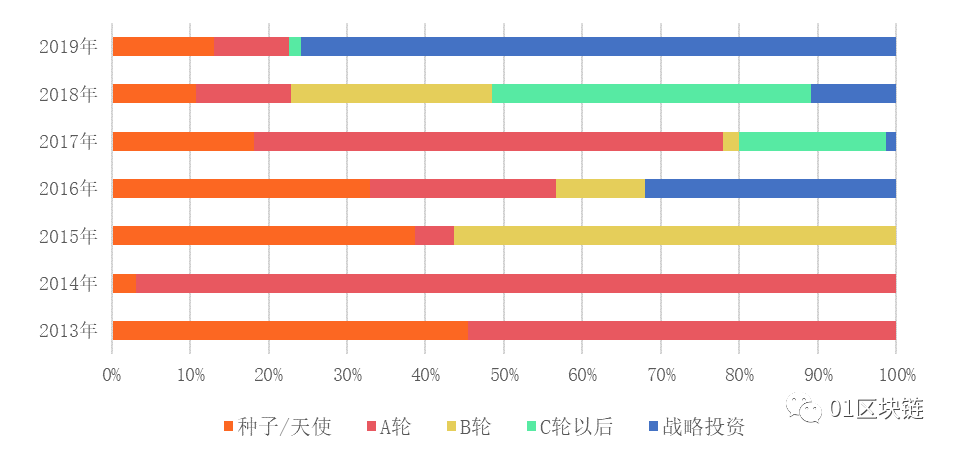

From the amount of financing publicly disclosed in recent years, the seed / angel round of financing has gradually declined, from over 40% in 2013 to less than 15% in 2019. Starting from 2017, the proportion of financing after the C round has increased, and it has dropped significantly in 2019, mainly due to the completion of Pre-IPO by Bitmain in 2018. Investors including Tencent, CICC and SoftBank China invested a total of 7.04 billion .

Figure 15 Distribution changes of financing rounds of Chinese blockchain companies / projects (by financing amount)

Source: Zero One Think Tank

Note: Round A includes Pre-A, A, and A +; round B includes Pre-B, B, and B +; round C includes CG and Pre-IPO.

4. Financing field distribution: Digital asset related fields are most favored by capital parties

By observing the distribution of the blockchain industry's financing field, we can see the enthusiasm of the capital side for each industry in the blockchain, the development level of each industry, and the future development trend of the industry.

Combining with the development of the blockchain industry, Zero One Think Tank has divided the blockchain industry into seven first-level industries, which are infrastructure technology & solutions, digital asset related, financial applications, physical applications, other on-chain applications (except digital Asset-related), industry services, and others. Among them, more than 60 secondary industries are included in the seven primary industries.

Figure 16 Blockchain Industry Map

Source: Zero One Think Tank

(I) Digital asset-related financing accounts for 29%, while physical application-related financing accounts for only 11%

From the perspective of the amount of financing of the primary industry, digital assets are still the most popular application scenario in the blockchain industry, and enterprises' ability to land in the real economy and financial applications needs to be improved.

Among them, the number of financings in the digital asset-related industry was the largest, with 51 transactions, accounting for 29%, and the number of service-related financings in the blockchain industry followed, with 46 transactions, accounting for approximately 26%. Other on-chain applications and physical application-related industries accounted for 17%, 14%, and 11%, respectively. The financial application scenario performed poorly and only received 5 financings, mainly because the current application of blockchain in the financial industry is mainly concentrated in banks.

Figure 17 Distribution of Blockchain Tier 1 Industry Financing from November 2018 to October 2019

Source: Zero One Think Tank

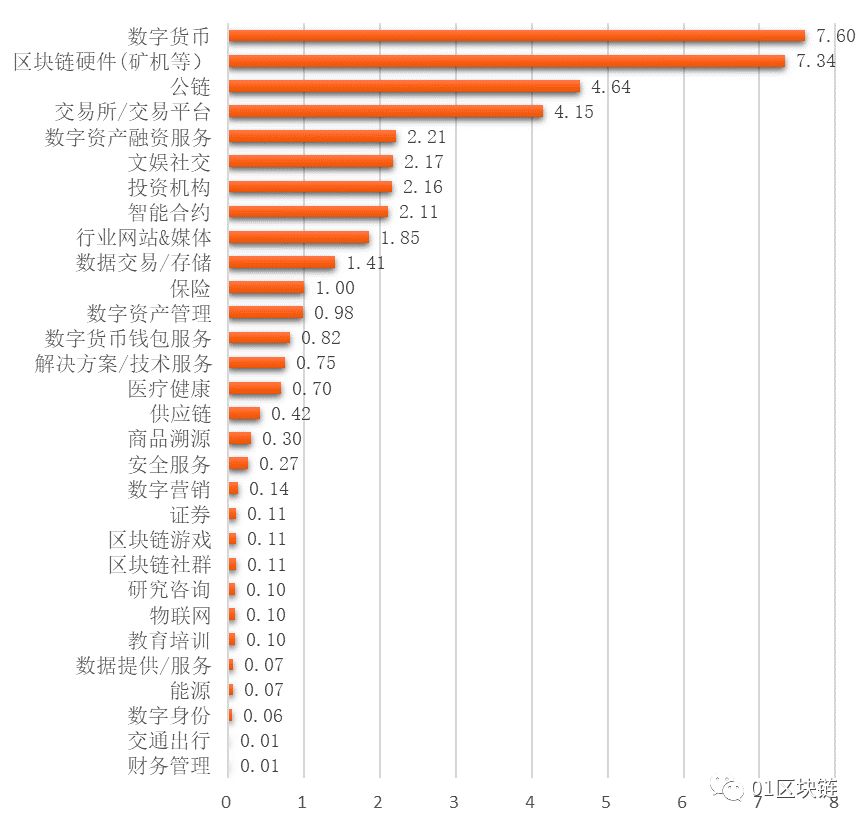

From the perspective of the distribution of financing in the secondary industry, industry websites & media, exchanges / trading platforms and solutions / technical service providers are most favored by capital parties.

The number of industry website & media financing accounts for 17%. Among them, the blockchain media Mars Finance received 3 financings in 2019, CoinVoice received 2 financings, and the decentralized application of the ecological portal fun technology gained 2 financings. The amount of financing from exchanges / trading platforms accounts for about 14%. The cryptocurrency exchange kucoin received 2 financings in November 2018. Solution / tech service provider financing accounted for 10%.

Figure 18 Distribution of Blockchain Secondary Industry Financing from November 2018 to October 2019

Source: Zero One Think Tank

(2) The digital asset-related industries are the most “gold-absorbing”, and the public chain project attracts more attention

From November 2018 to October 2019, the digital asset-related industry is the most "gold-absorbing" blockchain application industry, and the amount of financing is much higher than the other five major industries.

Figure 19 Distribution of financing amount of the first-tier industry in the blockchain from November 2018 to October 2019

Source: Zero One Think Tank

This feature is easier to see from the distribution of financing amounts in secondary industries. Among the top five secondary industries in terms of financing amount, except for the public chain, the other four industries belong to digital asset related industries.

According to the publicly disclosed financing amount, although there are only 3 financings in the digital currency related industry, the financing amount ranks first. The blockchain hardware industry ranked second, mainly due to the fact that "mining machine giant" Jia Nan Yunzhi obtained a strategic investment of 704 million yuan. The financing amount of exchanges / trading platforms ranks third. Cryptocurrency trading activities are banned in Mainland China. Most of these exchanges / platforms are registered in foreign countries and Hong Kong.

In addition, the amount of financing for public chain projects in infrastructure and facilities & solutions is also high, indicating that China's emphasis on public chain projects has begun to increase.

Figure 20 Distribution of financing amount in the secondary industry of blockchain from November 2018 to October 2019

Source: Zero One Think Tank

V. Investor perspective: the emergence of emerging investment institutions has promoted the outbreak of the blockchain industry

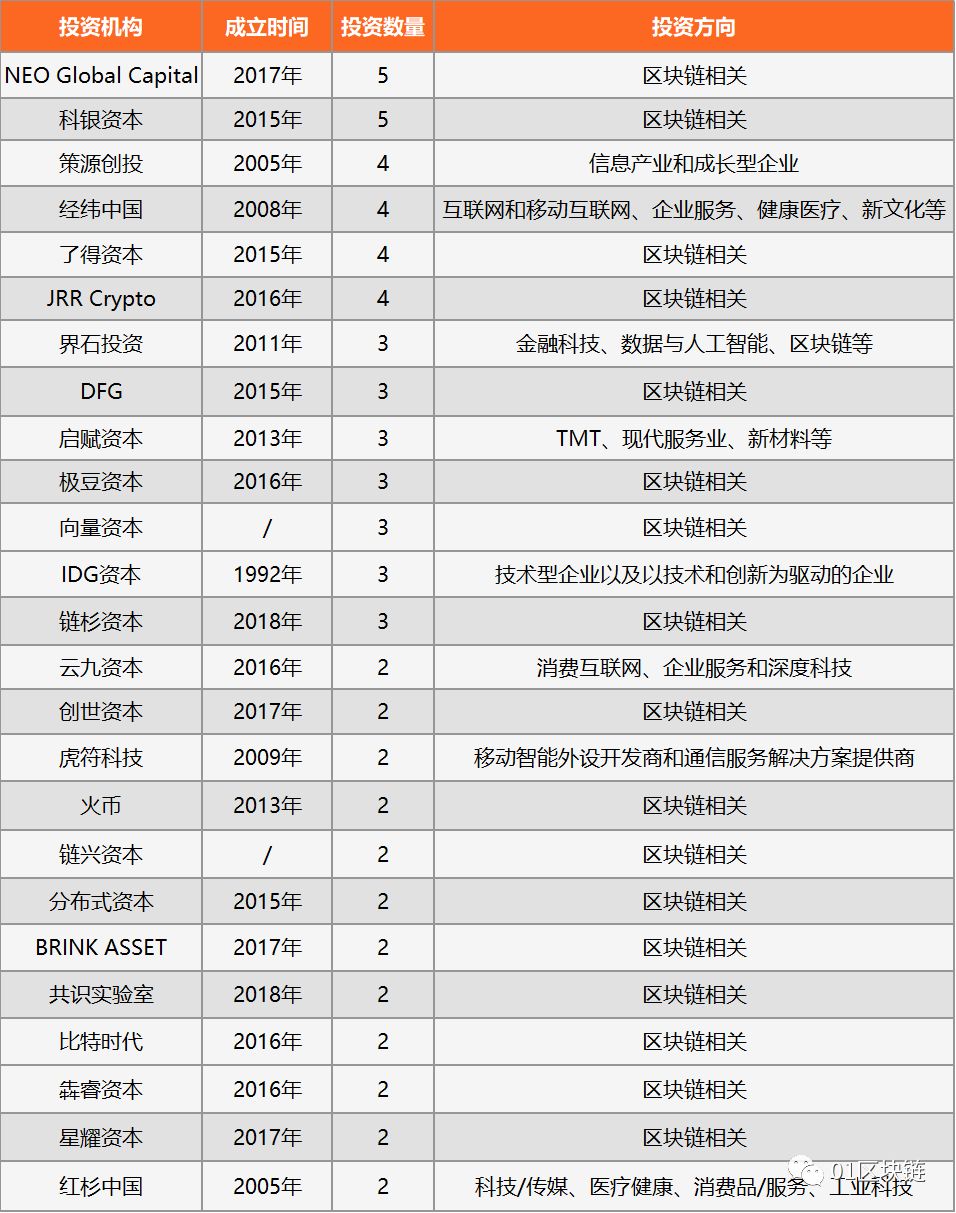

(I) 68% of the 25 active investment institutions are emerging institutions focusing on the blockchain field

The investment institutions of Chinese blockchain companies / projects are mostly emerging investment institutions focusing on the blockchain field.

From the distribution of 25 active investment institutions from November 2018 to October 2019, it can be seen that 17 are emerging institutions focusing on blockchain investment, and these institutions were established after 2015. The emergence of these emerging institutions has promoted the outbreak of financing of Chinese blockchain companies / projects. The analysis of the amount of financing and the changes in the amount of money previously analyzed can well confirm this conclusion. From 2016, the amount of financing of Chinese blockchain companies / projects And the amount began to increase significantly.

In addition to emerging investment institutions, traditional investment institutions such as Jingwei China, IDG Capital and Sequoia China are also active, investing in 4, 3 and 2 respectively.

NEO Global Capital and Ke Yin Capital are the most active investment institutions, investing 5 in each. Ceyuan Ventures, Led Capital and JRR Crypto all invested 4 funds. Among them, the founder of Led Capital was Ellipse, which had invested in more than 100 blocks such as EOS, Quantum Chain, Gongxinbao, Bubi and VeChain. Chain company / project. In addition, Huobi has also been more active in the blockchain sector. Huobi Investment's Lianxing Capital has launched two investments, and Huobi and Huobi Global Ecological Fund each invested one.

Table 2 Blockchain companies / project investment active institutions from November 2018 to October 2019

Source: Zero One Think Tank

Note: Huobi includes Huobi and Huobi Global Ecological Fund.

(II) Application fields of none of the 25 active investment institutions

From the perspective of the investment fields of 25 active investment institutions, five major industries, such as exchanges / trading platforms, industry websites & media, entertainment and social networking, blockchain communities, and digital currency wallets, are the most popular investment areas for these investment institutions. It is worth noting that none of the 25 investment institutions invest in application fields.

Exchanges / trading platforms remain the most popular on the capital side. Among the established investment institutions, Jingwei China invested 3 investments in the industry; IDG Capital made 2 investments.

The emerging investment institution DFG's investment direction is the most specific. All three investments from November 2018 to October 2019 were invested in industry websites & media. The invested institutions include CoinVoice, Bochain Finance and Alpaca Blockchain.

Figure 21 Investment field distribution of 25 active investment institutions

Source: Zero One Think Tank

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Will Upbit's $ 50 million loss bring Defi's "prosperity"?

- Tucao Series | Blockchain Games on Steam

- Twitter staged "year-end drama", Ethereum founder Vitalik Buterin became industry leader

- How the Macro Economy Affects Bitcoin Price

- Comment: The premise of regulation is to clearly define the precise meaning of digital assets

- Four keywords take you back to the major events in the mining circle in 2019

- The recent outbreak of a new ransomware has broken the heart for "promotion" of Bitcoin