Detailed DCEP future use scenarios-low-cost cross-border payments

Author: Joyce Lin, senior technology media, community representatives Conflux, former executive editor CoinDesk China, in-depth observation of the block chain industry.

The Central Bank's statutory digital currency (DCEP) is near, and the traditional legal currency will gradually disappear, albeit at a very slow pace. But until now, most of the related discussions of DCEP are still around the abstract theoretical level. Here, through a series of articles, I will try to discuss more specifically what DCEP is and its possible use scenarios in the future.

As mentioned last time (Café | Detailed DCEP future use scenarios-high concurrent retail payments), the forthcoming Central Bank of China Digital Currency (DCEP) is primarily aimed at providing more convenient retail payments. But this is also the place where many people are most puzzled about the entire DCEP. After all, China is already the most developed place in the world for electronic payment. Alipay and WeChat payment have a high penetration rate, and DCEP has limited space to improve convenience. Is it really worth the trouble?

Mystery hidden in the next stage of the goal of the former People's Bank of China Zhou Xiaochuan: make digital currency used for cross-border payments and remittances for international financial institutions. Promoting the internationalization of the renminbi through a completely new path, playing a role in the Belt and Road countries and the global economic connection, is where DCEP may play its greatest value.

- Research | How Blockchain Solves Financing Problems

- Half a year of research and development can't beat BM's mouth? Isn't Voice worth looking forward to?

- Perspective | How will blockchain develop with the development of quantum computing and AI

Why is RMB internationalization so important? How can it be achieved through DCEP?

"The Connery Problem"

The current basis of the international monetary system comes mainly from the Bretton Woods Agreements signed by countries around the world in 1944, when most countries joined the international monetary system centered on the US dollar.

The Bretton Woods Agreement strengthened post-war international economic cooperation, the international monetary order was rebuilt, and international trade was restored to free and smooth, and its contribution was not significant. However, this also makes the US dollar a veritable global currency. With the status of the global currency, the United States can easily influence the world economy through various monetary policies and tools, or it will regulate its own domestic economy.

For example, under the dollar-based system of the global economy, all cross-border trade and payment will actually pass through the layer-by-layer banking system. Eventually, the Global Interbank Financial Telecommunications Association (SWIFT) and New York Clearing House Interbank Payment System "(CHIPS) can be used for settlement before the transaction can be completed. SWIFT was once blocked by the United States as a means of trade sanctions and was not allowed to pay for oil in US dollars. Anyone who dared to have economic dealings with Iran would be implicated, causing the latter's economy to be hit hard.

Another example is that after the financial tsunami in 2009, the Federal Reserve launched a quantitative easing policy (Quantitative Easing, QE), which injected a lot of liquidity into the market. However, this move was questioned as a result of the QE devaluing the US dollar and exporting inflation to other countries, which indirectly led to the consequences of real estate bubbles in emerging markets in Asia.

All these unfair situations, as John Connally, who was then the Minister of Finance of the Nixon Administration in 1971, said: "The dollar is our currency, but it is your problem." our currency, but your problem) Regarding the bossy mindset of the United States, other countries, even if they are willing to challenge, suffer from the fact that there is no better alternative, and they can only continue the dollar system.

(Photo: John Connally | Source: wikipedia)

But China is already the second largest economy in the world and the largest creditor country in the United States. Expanding the international voice is a goal that the renminbi must achieve.

Therefore, the significance of DCEP cross-border payment is far more profound than the appearance of "convenience".

Low-cost cross-border payment use cases

Having said that, "convenience" is still the key word.

Because of the internationalization of sovereign currencies in the 21st century, naturally it can not just copy the old path of the physical dollar, but must be more convenient and easy to use than the dollar to succeed. DCEP absorbs the experience of the development process of cryptocurrencies, which can reduce payment costs, time costs, labor costs, improve transparency, and have potential advantages over traditional fiat currencies in many aspects, which shows the possibility of supporting the internationalization of RMB.

What might DCEP cross-border payments look like?

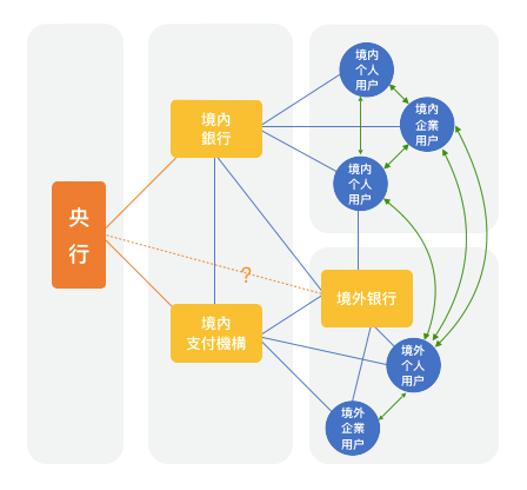

In the past, the RMB cross-border payment had a CIPS system (Cross-border Interbank Payment System), but it was based on bank accounts. Overseas banks need a RMB business, so businesses or individuals can use banks to complete cross-border payment processes. Although the specific details of DCEP are not known, ideally, as long as the user has a DCEP wallet, it can even directly communicate between domestic and foreign users without going through a bank (see the figure below). However, according to the information released so far, the central bank issues DCEPs only through specific domestic commercial banks and payment institutions. Will overseas banks one day also directly exchange digital currency with the People's Bank? It seems that the possibility is still small.

(Figure: DCEP's Cross-border Payment Use Scenario | Source: Author)

But this still means that the threshold for cross-border payments using DCEP will be significantly lower than in the past. Because the blockchain is non-tamperable, transparent, and traceable, digital currencies naturally have cross-border advantages and can effectively expand the use of the RMB overseas.

A possible scenario is that a Taobao merchant wants to pay a sum of money to an overseas upstream manufacturer. At this time, as long as he holds the equivalent DCEP RMB, he can directly make cross-border trade payments to the manufacturer through online payment (as shown above). Process). The key difference is that in this payment process, the payee can theoretically receive the payment immediately, instead of having to wait for several days as in the past with SWIFT. At the same time, it also means that the payment cost is greatly reduced, and the handling fee may be as low as 10% to 20% in the past. In other words, the time and money costs have been reduced, and the focus is on the entire system being more autonomous and controllable.

And what does this use scenario mean for the domestic blockchain industry?

The first is the cross-border payment bridge will be a new system. Compared with Chinese users, the penetration rate of overseas digital payments is relatively low. Related digital currency wallets, digital currency custody, payment and settlement platforms will bring a lot of system development requirements.

Followed by technical output. China may now be the first major country to launch a central bank digital currency. Once DCEP is successfully implemented, other countries will inevitably follow up and try to launch their own version of CBDC, and the Chinese blockchain industry with relevant successful experience will have the absolute advantage of technology output.

However, when the euro came out in 1999, it was once considered a strong challenger to the dollar. But the subsequent development was that the economy of the euro zone was trapped, the euro was weak, and the gap between the dollar and the dollar was getting wider. Although use cases such as DCEP's cross-border payment are expected to take a new path to promote the internationalization of RMB, this is only the beginning.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Zhang Jian: FCoin is expected to be unable to pay approximately 7000-13000 BTC

- Analysis of CBDC International R & D (3): Who will master the "Adamian" of CBDC?

- Viewpoint: Are traditional valuation methods really effective? (on)

- Five biggest misunderstandings about Eth2.0: ETH2.0 will never be launched? Will this fork produce two kinds of ETH tokens?

- Libra thinking about anchoring the US dollar as a single currency launch? The reason behind it is not simple

- Data Analysis | Do you really understand the computing power, block rate, and profit of the Filecoin network?

- Bitcoin is soaring, industry investment is heating up, and the air has come … you urgently need a cheat for customs clearance!