Ethereum in-depth comment: new address number forecast price trend valuation is afraid of historical low

Comment summary

In 2017, 1CO brought about chaos and promoted the development of Ethereum. According to the standard Metcalf index, the current Ethereum price is historically low compared to value.

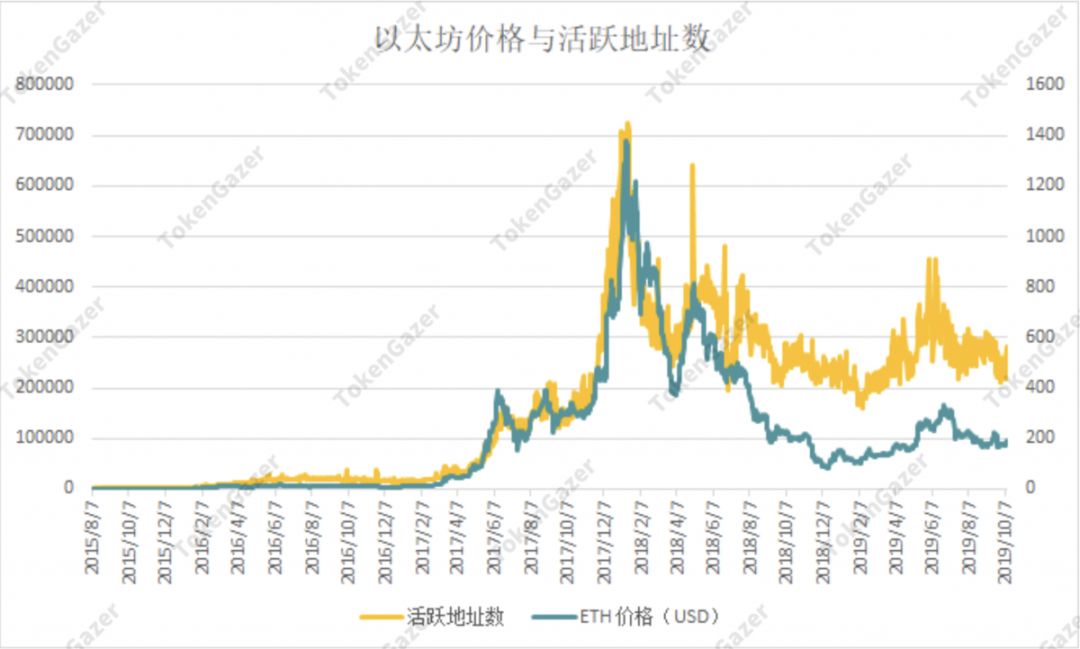

The number of active addresses and new addresses in Ethereum has dropped significantly with the end of the bull market in 2017, but the decline in the number of active addresses in Ethereum is small compared to the price. At present, the activity of the entire network is much higher than the network activity at the same price level in the early 2017 bull market.

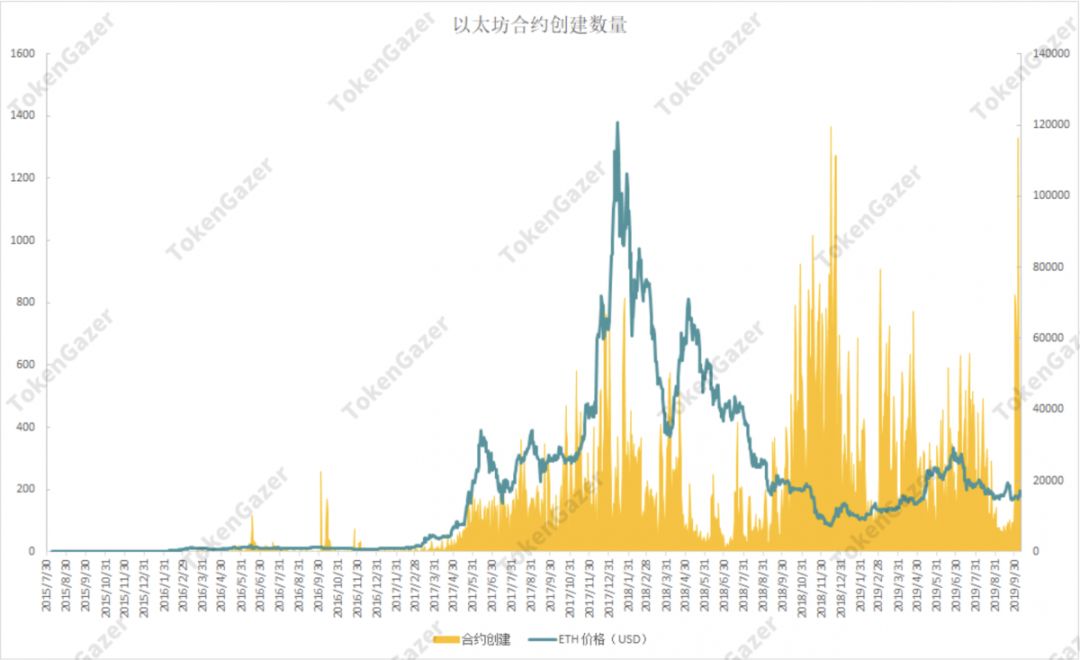

Since August 2018, the creation of the Ethereum contract has been at a very active level. Although the market is relatively sluggish, it has not affected the development of the Ethereum ecosystem.

- Exclusive Interpretation | Tencent Blockchain White Paper on Libra, Face Up or Downward Strike?

- Academic Direction | How does Bitcoin drive breakthrough innovation in accounting?

- Viewpoint | Blockchain is a digital social governance system for AI smart new species

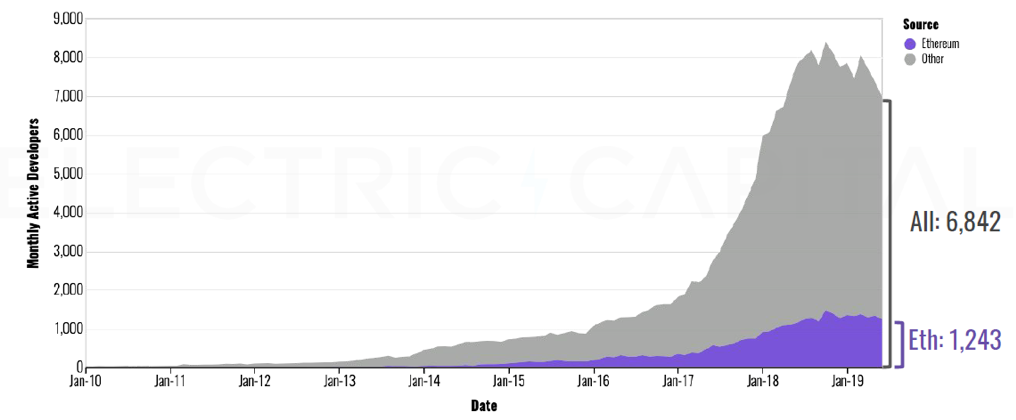

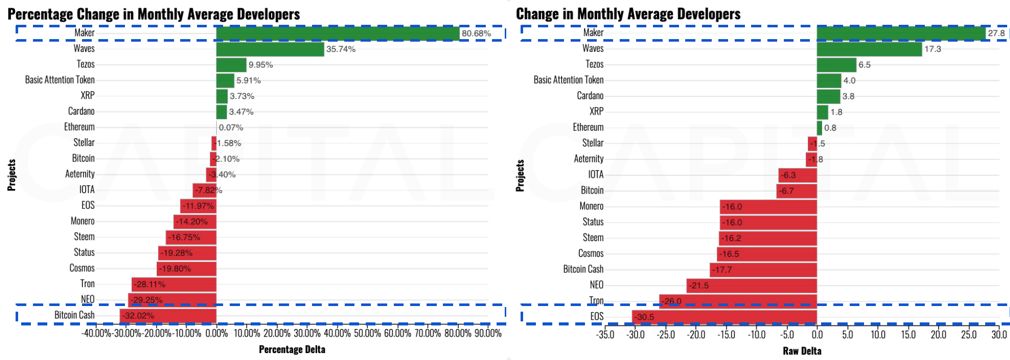

In the first half of 2019, the number of developers in Ethereum continued to grow steadily as the number of developers of the entire encryption ecosystem declined. Ethereum has the largest number of developers in the entire encryption ecosystem, accounting for more than 18% of the total number of developers. The number of MakerDAO developers in their ecosystem has grown the most in the entire encryption ecosystem.

Since 2017, the DEX project has become more diverse and richer, and IDEX still holds the largest market share in the decentralized trading market. But as new projects grow, their market share is compressed. The most recent growth is Uniswap, with trading volume close to Bancor, which has the second largest market share.

Ethereum's DeFi ecosystem is growing rapidly, and the largest DeFi Protocol Maker plans to launch a multi-mortgage mechanism in November 2019 to open its growth ceiling. The composability of the DeFi ecosystem is worthy of attention.

Many new public chains have been/will be launched, creating competitive pressure on Ethereum. From the development of relevant data, Ethereum 2.0 is still very competitive.

The specification of Ethereum 2.0 has been completed, and the transfer from Ethereum 1.0 to Ethereum 2.0 will not have much impact on its ecology. Before the completion of the upgrade, the ecological construction of other high-performance public chains and the attraction of Ethereum eco-developers to the inevitable competition faced by Ethereum, the smooth and timely implementation of Ethereum 2.0 is essential.

The value and price of Ethereum

We use the standard Metcalfe index to reflect the relationship between Ethereum's value and price: the higher the relative value of the price, the higher the Metcalf index; the smaller the relative value of the price, the smaller the Metcalf index. In our calculations, the value of Ethereum is measured by the number of active addresses. According to the Metcalf index, we divide the above picture into the following stages:

- The first stage: Ethereum in the early days because the number of active addresses is very low, the entire market value is basically based on imagination, at this time the standard Metcalf index is very high;

- The second stage: the standard Metcalfe index declines with the construction and development of Ethereum, and the price and value tend to converge;

- The third stage: In the early days of the bull market in 2017, when the fundamentals of Ethereum did not change significantly, the price began to soar, resulting in a sharp rise in the standard Metcalfe index;

- The fourth stage: the market fever brought about an increase in the number of participants, and the number of active addresses in Ethereum increased. As the price growth of Ethereum slowed down, its standard Metcalf index began to decline;

- The fifth stage: After the arrival of the bear market, although the number of active addresses in Ethereum has decreased, the standard Metcalfe index has continued to decline compared to the smaller price decline;

- The current stage: the standard Metcalfe index is at a relatively stable low level, and has certain commonalities with the second stage.

We believe that although 1CO brought a lot of chaos in 2017, causing excessive market enthusiasm, but after the enthusiasm, there are still projects that have settled down, and some users have settled down – these are also seen in our subsequent chain and ecological analysis. . From the perspective of the standard Metcalf index, the current Ethereum price is lower than ever before, which does not necessarily mean that the Ethereum value is underestimated, but means that in the standard Metcalf index From the perspective of eliminating other risks such as technology, it is safer to hold Ethereum than ever before. Below we specifically examine the ecological development that truly supports the value of Ethereum.

Ecological development

The development of the Ethereum ecology can be reflected from the data of its multiple chains. From the relevant data, we have investigated the overall situation of the Ethereum ecology. At the same time, we also examined the development of different areas of the Ethereum ecosystem based on specific DApp data.

Address activity / address addition

The number of active addresses in Ethereum can be seen as the “day activity” of Ethereum, reflecting the use of the Ethereum network by ordinary users and developers.

Let us first review the changes in the number of active addresses during the entire development of Ethereum:

It can be seen that the active address of Ethereum has grown violently in the 2017 bull market – which is easy to explain, and the high prices have driven people's trading sentiment, which has increased the active address of Ethereum. At the same time, there is also a new Ethereum address, which to some extent represents more users to join, we can see this in the picture below.

With the end of the bull market in 2017 and the arrival of the bear market, we have seen a significant decline in the number of active addresses and new addresses in Ethereum. However, it is worth noting that the decline in the number of active addresses in Ethereum is not as large as the decline in prices. More precisely, although the price of Ethereum dropped to the level of the early bull market in 2017, the activity of the entire network was much higher than the current network activity. The number of active addresses and new addresses in Ethereum has remained stable this year.

Add new addresses or pre-emptive metrics

We observed that the number of new addresses in Ethereum has a certain pre-emptiveness with respect to the market price of Ethereum. This situation is more obvious when Ethereum turns from a larger uptrend to a downtrend:

In the above picture, when the bulls turn to bears in 2017, the number of new addresses in Ethereum will fall 7 days earlier than the current price; and in the recent Ethereine rally, the number of new addresses in Ethereum has occurred 24 days ago. A big drop. We believe that the number of new addresses represents the hot participation of the network, as a pre-emptive indicator of price, has a certain degree of confidence. When such a reversal signal is observed, investors can cooperate with other indicators for joint verification.

Smart contract creation

By examining the contract creation of the Ethereum network, we can see that in the first half of 2018, Ethereum and contract creation volume were in line with the price trend, but in the second half of the year, the contract creation volume began to increase, even surpassing the 2017 bull market. Case. Since August 2018, the creation of the Ethereum contract has been at a very active level. It can be said that although the market price has an impact on the ecological development of Ethereum, the overall impact is not great, even we can draw “The conclusion that the Ethereum ecology can be better developed when the market is relatively calm.”

According to the cryptocurrency developer report released by Electric Capital in the first half of 2019, we can see that although the number of developers of the entire encryption ecosystem has declined, the number of developers in Ethereum is only slowing down, still higher than in 2018. There are more developers in the first half of the year. Ethereum has the largest number of developers in the entire encryption ecosystem, accounting for more than 18% of the total number of developers.

DeFi becomes a trend

In the Ethereum ecosystem, the number of Maker developers is the largest in the entire encryption ecosystem, both in terms of growth and growth. Maker is the largest DeFi application in the Ethereum ecosystem, and the current DeFi application is the mainstream of the Ethereum ecosystem.

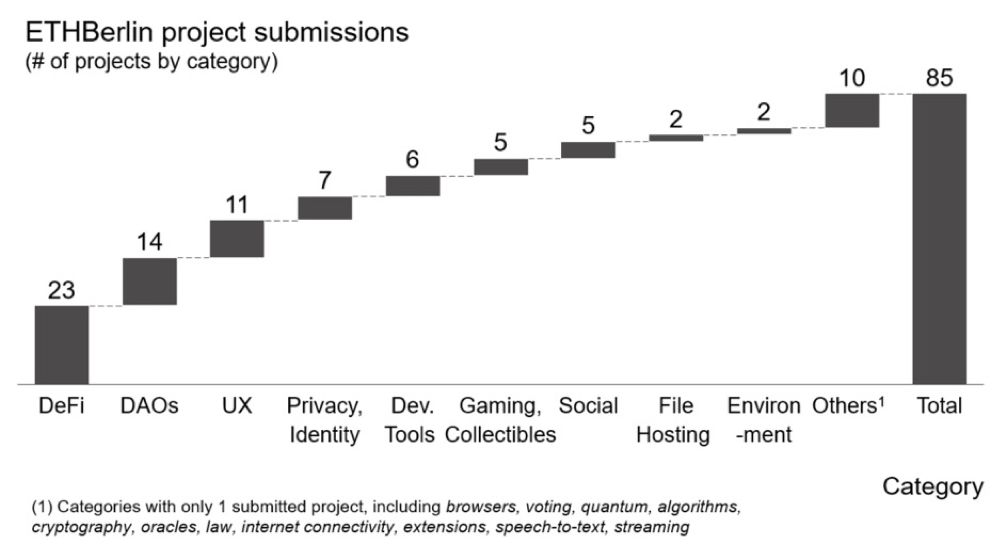

Recently, the Ethereum hacker in Berlin, the participating developers submitted a total of 85 projects, although most of these projects will not continue, but there may be individual projects will be precipitated and continue to develop. The largest number of these projects is the DeFi class, followed by the DAO.

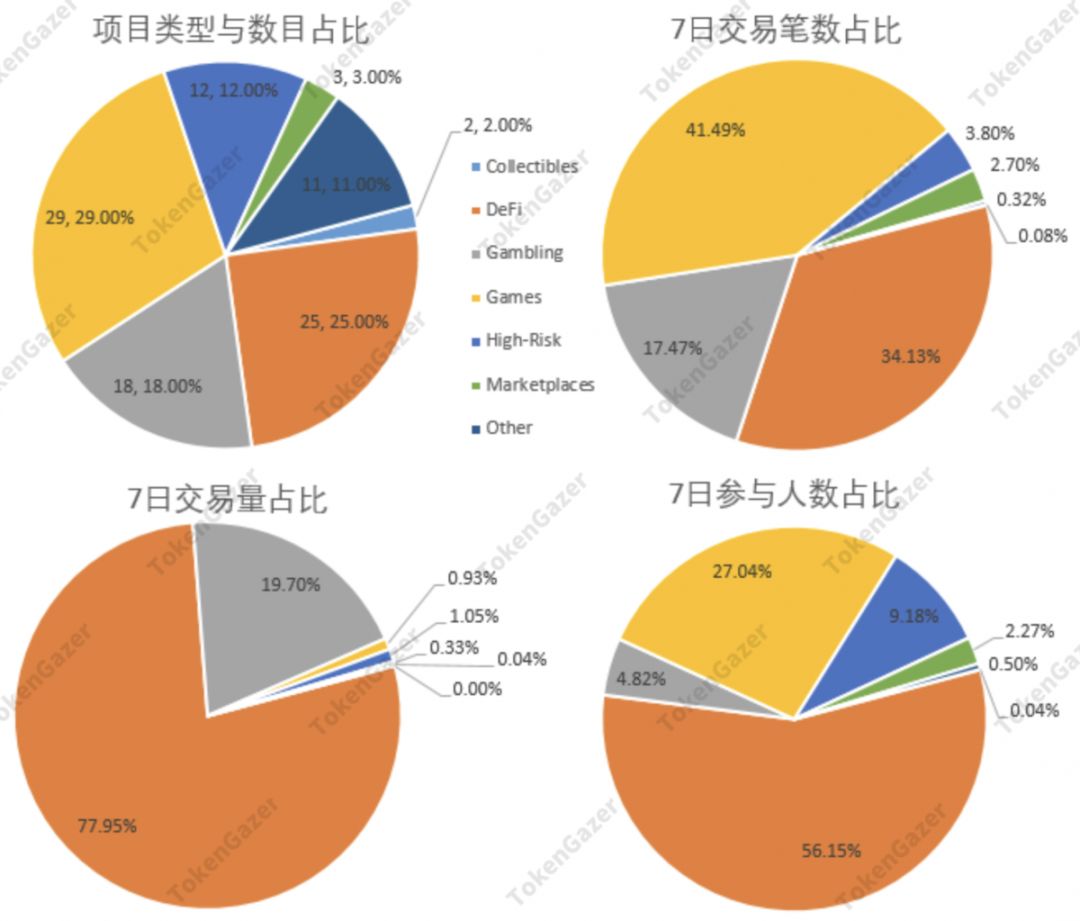

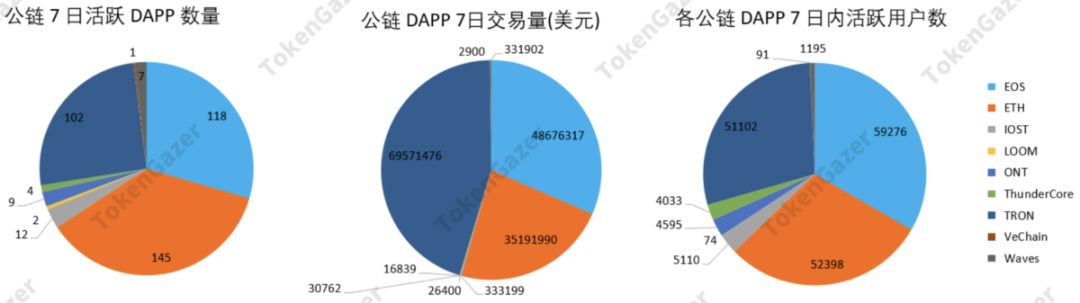

We examined the chain data of the active DApp in Ethereum within 7 days:

The most popular DApp in the Ethereum ecosystem is the game category, followed by the DeFi category, the betting category and the collection category; in terms of the number of transactions, it is still the most frequently used game application. But in terms of volume and user engagement, the DeFi class application dominates.

DEX development

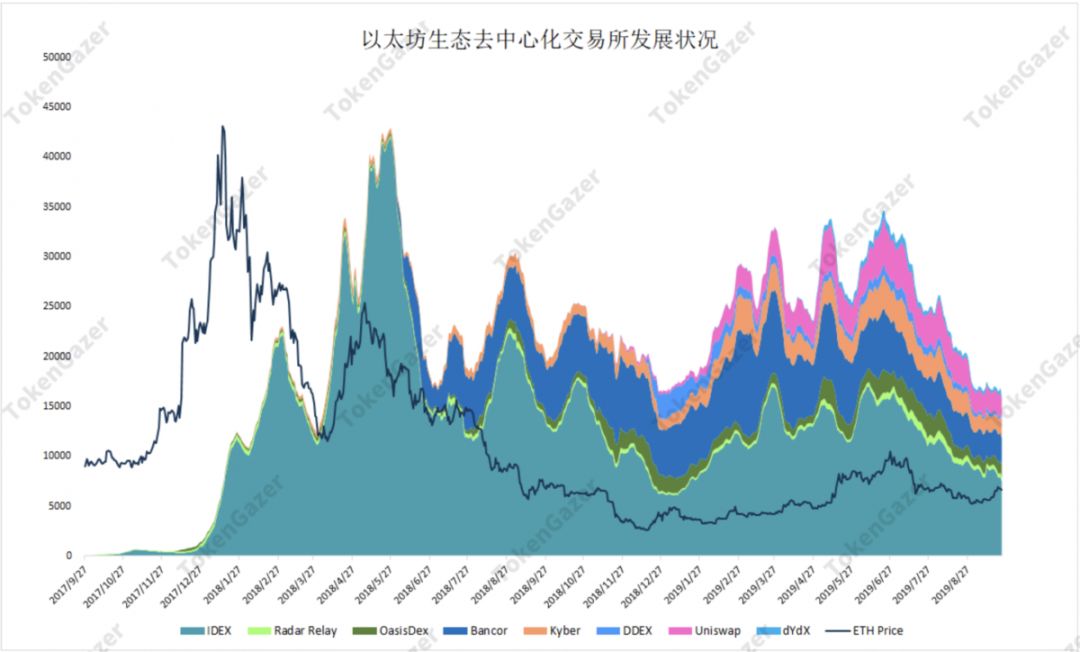

The Decentralized Exchange (DEX) has an important share of the DeFi ecosystem. We first looked at the development of DEX in the Ethereum Ecology.

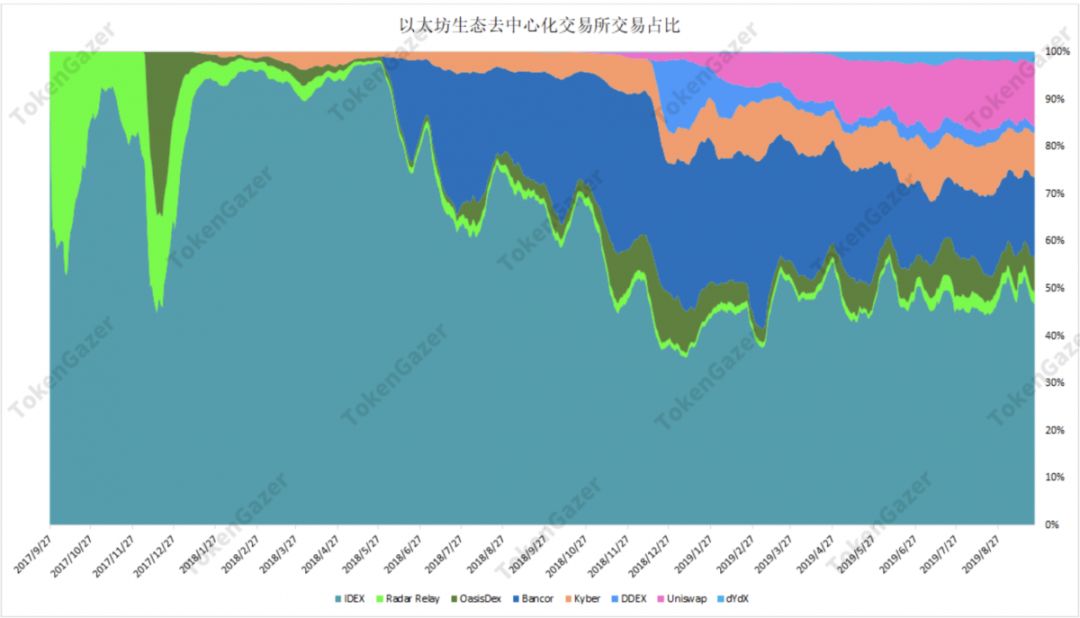

It can be seen that the development of DEX began in the early stage of the most frenetic phase of the bull market in 2017, but the amount of trading was actually after the reversal of the market. At that time, only Radar Relay, IDEX, Oasis DEX, IDEX occupied a major market share. With the decline in Ethereum prices, although IDEX's trading volume has also fallen, at the same time, the development of the new DEX has made the trading volume in the entire DEX market not fall like the price – with the development of the ecology, Other DEXs such as Bancor, DDEX, Uniswap, and dYdX have emerged.

We see that IDEX's market share has been squeezed after Bancor's launch. Subsequently, with the development of other DEXs, IDEX's market share has further declined, and the current market share is relatively stable. In addition to IDEX, the current market share is Bancor, Uniswap, Kyber, notable is Uniswap, which showed rapid growth after the end of 2018, and the market share now exceeds Bancor's trend.

The provision of Unswap liquidity does not depend on the pending order, but the transaction price is calculated based on the currency locked in the agreement and a certain formula. Therefore, the transaction depth depends on the locked currency. The Uniswap agreement provides incentives for liquidity providers, and this model facilitates its growth. More than 55,000 ETHs have been locked in Uniswap, and there are other DeFi applications that, like Uniswap, provide services by locking ETH into protocols. In a well-developed situation, this model allows Ethereum to effectively capture the value of its ecological growth, and we examine the development of such agreements/applications.

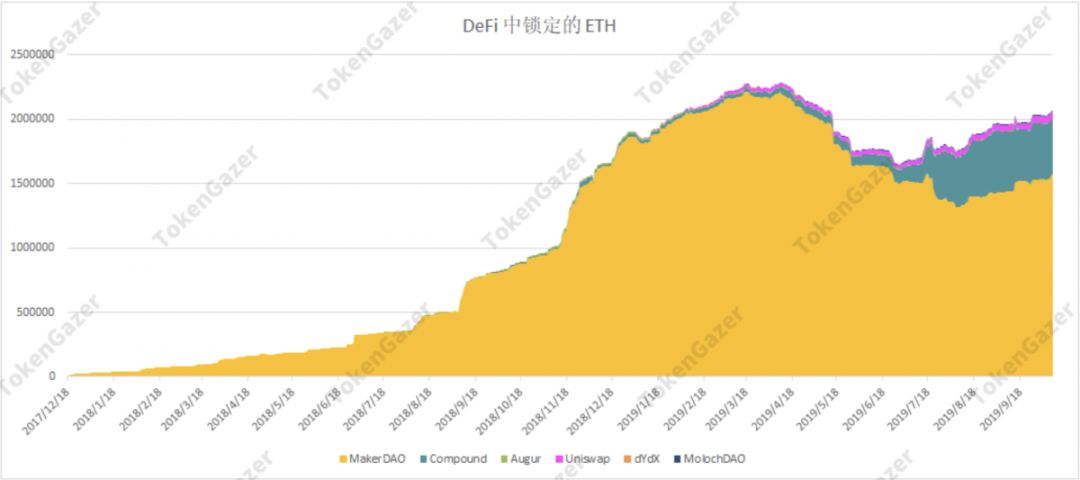

Lock ETH's DeFi

The above graph shows the changes in ETH locked in the DeFi application over time, showing the development of DeFi and the Ethereum's need for ETH as an asset. It can be seen that since the end of 2017, the ETH locked in DeFi has grown from scratch. At present, the entire DeFi ecosystem has locked more than 2% of the total circulating ETH, and the projects are becoming more and more abundant. It can be said that DeFi has a long way to go. growth of.

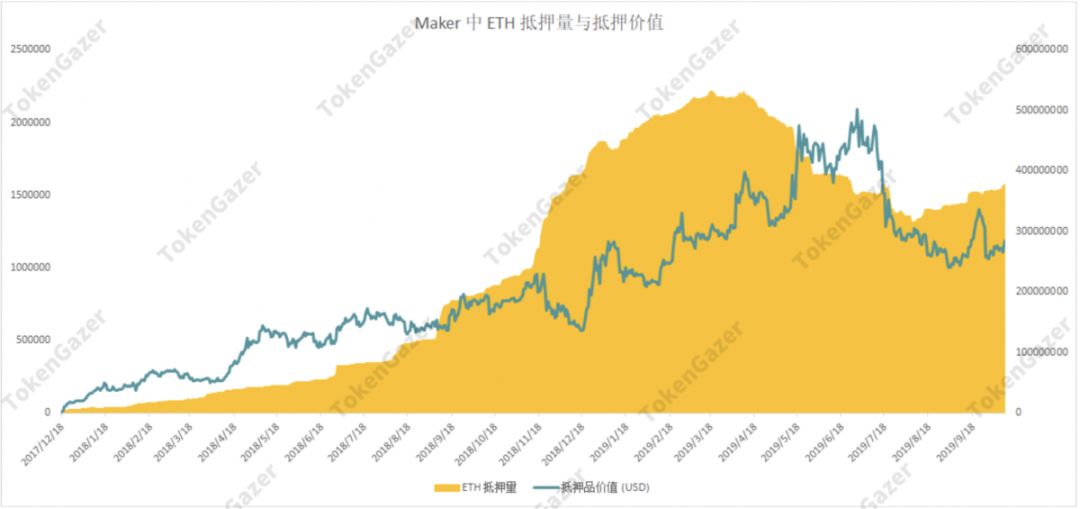

Maker has locked the largest number of ETHs in this type of application and has a very high growth rate. But we also saw that ACE-locked Ethereum declined from March to the end of June. In fact, this decline does not mean a decline in the development of Maker. In the Maker Agreement for Single Collateral, MakerDAO sets a debt ceiling for risk management purposes. Its risk management team believes that in the case of a single collateral, the debt limit of the Maker agreement should be $100 million. In March of this year, the price of ETH showed a large increase. Although the overall mortgage rate of the system increased, the increase in DAI supply led to the growth of Maker close to the debt ceiling. At the same time, the price of DAI was also increased due to the increase in supply. A certain degree of anchoring occurred. For the purpose of regulating the supply of DAI, MakerDAO continues to increase the system's lending rate, resulting in a decline in ETH mortgages in the system.

From the above figure, we see that during the decline of ETH mortgage, the value of collateral in the Maker system is still increasing. At the same time, MakerDAO has formulated a series of policy to cut interest rates because the price of collateral ETH has dropped significantly since June. The number of ETHs mortgaged in the Maker agreement began to grow. It is worth noting that MakerDAO will launch multi-collateral in November this year, when the $100 million debt limit set by the Maker agreement due to risk control will be significantly increased, and the ceiling of Maker growth will increase.

The figure above shows the current distribution of ETH in major DeFi applications. In fact, the current DeFi ecosystem has many other protocols/applications, such as Synthetix, InstaDapp, dYdX, etc., in addition to the protocols shown above. The development of DeFi has led us to focus on the composability of Ethereum applications – for example, Sythetix combines Maker and Kyber, InstaDapp combines Maker and Compound – and this composability is helping Ethereum build itself relative to other companies. Chain of moats.

Comparison with other existing public chain ecosystems

Compared with other public chains that are already running, the number of active DApps is still the most in Ethereum, but in terms of transaction volume, TRON and EOS are more, the reason is related to performance, and the latter two are more supportive for large transactions. Gaming and other applications. Among all the public chains, the DApp with the most trading volume in the past 7 days is WINK on TRON, about $36 million, it has been on the 1EO of the currency security; and the largest application MakerDAO on Ethereum is not an application that requires frequent transactions. In terms of the number of active people, Ethereum is also slightly lower than the latter two. We believe that the implementation of Ethereum 2.0 and the implementation of the new public chain will have a greater impact on the above pattern. Below we examine the progress of Ethereum 2.0 and market competition.

Ethereum 2.0

Implementation of Ethereum 2.0

Ethereum 2.0, the Serenity version of Ethereum, is a chain developed by independent Ethereum 1.0 and will include a series of upgrades such as sharding, PoS and eWASM. During the Wanxiang Blockchain Conference in September, Vitalik stated that the Ethereum 2.0 specification was completed and began to do third-party analysis. The upgrade from Ethereum 1.0 to Ethereum 2.0 will be implemented in multiple phases:

Phase 0: Beacon Chain (no fragmentation)

Phase 0 is the launch of the Ethereum beacon chain, which will be completed in early 2020. The beacon chain is the foundation of Ethereum 2.0, which manages itself and its shards. It uses Casper the Friendly Finality Gadget (FFG) to achieve finality, with the main data as the evidence (Attestation) , including voting on fragmented blocks and PoS voting on beacon blocks.

In phase 0, all user transactions and smart contract calculations will still run on Ethereum 1.0. After implementation in phase 0, there will be two chains at the same time: the Ethereum 1.0 chain and the Ethereum 2.0 chain. Users on the Ethereum 1.0 chain will be able to lock their ETHs in the contract and get the same amount of ETH on the beacon chain in Ethereum 2.0. At a later stage, they can pledge 32 ETHs into certifiers for Ethereum 2.0 and receive verification awards at Ethereum 2.0.

Phase 1: Basic sharding (without EVM)

The slice chain can run in parallel and trade with each other, and the key to scalability is the Ethereum 2.0. In the first phase, the state of the Ethereum 1.0 chain will be transferred to a shard on the Ethereum 2.0 chain, ensuring that information from the Ethereum 1.0 chain will be available in Ethereum 2.0 in the future.

The fragmentation chain at this stage is only trial run for the construction, validity and consistency of its data, and does not actually use fragmentation for expansion. At this stage, the fragmentation chain does not implement state execution and account balance. . Crosslink is used in the beacon chain block to indicate the current state of the shard over a period of time. Crosslink is a set of valid signatures for the block on the slice chain, which represents the latest state of the blockchain chain and is the basis for asynchronous communication across slices.

Phase 2: State execution

In Phase 2, the data in the slice chain will no longer be a simple data container, but will reintroduce the smart contract and replace the EVM with eWASM. Each shard manages eWASM-based VMs, supporting accounts, contracts, status data, and more. In addition, state leases may be introduced at this stage, and contract developers and users will pay for eWASM storage. Phases 1 and 2 are scheduled to be completed in the fourth quarter of 2020.

Phase 3: Under-Chain State Storage

Phase 3 will shift the state of the chain to the chain as much as possible to minimize the state of the chain. Maintaining and retrieving the state under the chain in Phase 3 will be a key design constraint for DApp.

Phase 4: Cross-segment trading

Implement interaction between contracts on different shards. At present, various proposals for interoperability of fragmentation contracts do not seem to solve the contradiction problem of synchronization and expansion, which is one of the most challenging stages.

market competition

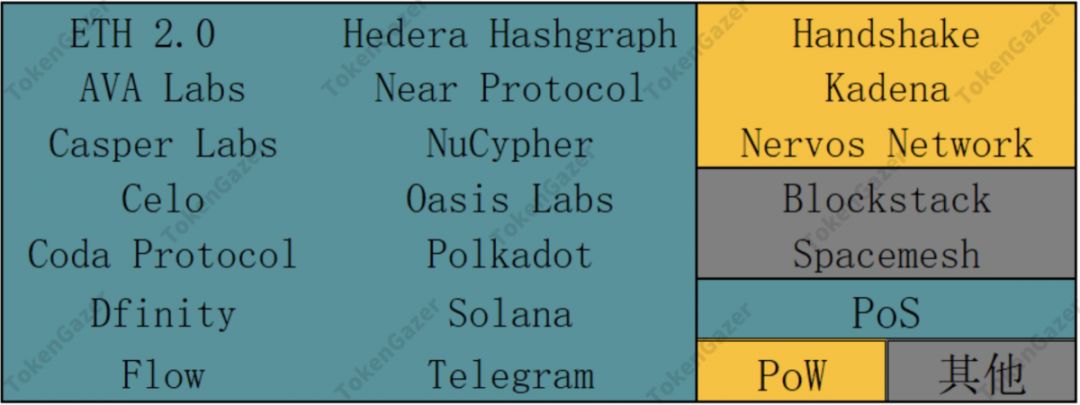

In the past year, new public chain projects have been launched or are already launched – the Near Protocol team is strong and praised by Vitalik; Blockstack has attracted developers to develop many DApps; Polkadot is able to compete with all chains; Handshake is rebuilding Internet security vulnerabilities; Telegram has been secret development, but if it is completed successfully, it can use its 300 million users to drive the network effect of TON, etc. – these projects form a competitive trend for Ethereum, and the upgrade of Ethereum There is no time to delay.

The above chart shows the recent launch/coming public-link projects. It can be seen that, including Ethereum 2.0, most new/expected networks use PoS to protect against Sybil attacks – there are 15 (79%) plans. PoS is used, and only 3 projects plan to use PoW (HandShake, Kadena, Nervos). Spacemesh is special, it plans to use a mechanism called time-space proof (PoST); Blockstack also plans to adopt other solutions. This shows to some extent that developers are more recognized for PoS.

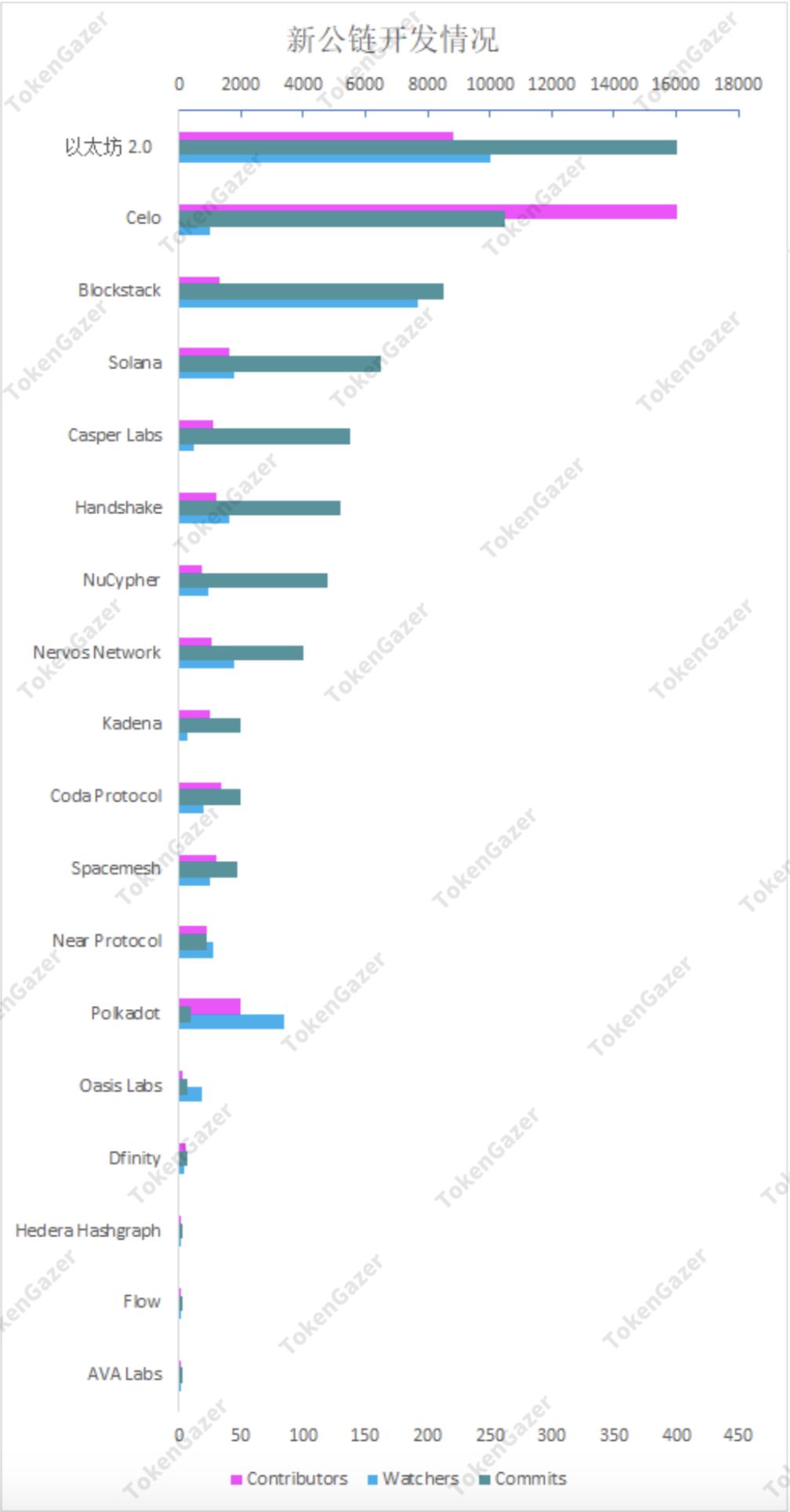

The development community is very important to the public chain. We compare the development of these projects with the influence of the project in the Github developer community (Commits, Watchers, Contributors) and the influence in the developer community. As shown above, Ethereum 2.0 is the most Commits and Watchers project in all of the above public chains, and the number of Contributors is second only to Celo. It can be seen that from the perspective of development, Ethereum 2.0 has strong competitiveness in these projects. It's important to note that not all GitHub repositories are public, such as Hedera and Dfinity, which is one of the reasons why Commits are so low.

Migration of existing ecology to Ethereum 2.0

From the above discussion, we know that the competitiveness of Ethereum is also reflected in the ecology it has accumulated. Therefore, in the process of upgrading Ethereum from 1.0 to 2.0, ecological migration is also crucial because it is a different chain. This part has more discussion on ethresear.ch, and Vitalik also gave his explanation. The overall conclusion is:

- From Ethereum 1.0 to 2.0, developers do not need to make complex, fundamental changes to their contracts;

- From Ethereum 1.0 to 2.0, the upgrade may be completed without the user's feeling;

- After upgrading to Ethereum 2.0, in the case of fragmentation, the composability of Ethereum's ecological applications will not be affected.

The specification of Ethereum 2.0 has been completed, and the discussion based on this can eliminate many people's concerns – Ethereum 2.0 will not cause resistance or impact on the development of existing ecology. According to the plan, the third phase of Ethereum 2.0 will be completed by the end of 2020, when the ecology of Ethereum will be transferred to Ethereum 2.0.

During this period, the ecological construction of other high-performance public chains and the attraction of Ethereum eco-developers are the inevitable competition facing Ethereum. Recently, Aragon chose to build a new chain with the Cosmos SDK, which is an ecological loss for Ethereum; MYKEY has brought more than 50,000 new accounts to EOS based on its accumulation in the community and subsidies. It also brings more traffic entries to applications in the EOS ecosystem. Through these developments, although Ethereum still has the developer and ecological advantages, Ethereum upgrade 2.0 is a “golden time window” that other public chain competitors will not give up. Therefore, the smooth and timely implementation of Ethereum 2.0 is essential.

in conclusion

Although the market enthusiasm in 2017 caused a bad market reaction, it also made the Ethereum ecology have more projects and users. According to the standard Metcalf index, the current Ethereum price is historically low compared to value.

In the downturn of the market, the creation of the Ethereum contract was in a very active level, and the Ethereum ecology was well developed. During this time, the DEX project was more diverse and richer. Although IDEX still occupies the largest market share of decentralized trading, its market share has been compressed as new projects have grown. The most recent growth is Uniswap, with trading volume close to Bancor, which has the second largest market share. The DeFi ecosystem has also grown rapidly, and is currently targeting Ethereum, which accounts for more than 2% of circulation. The largest DeFi Protocol Maker plans to launch a multi-mortgage mechanism in November 2019, which will open its growth ceiling.

In the past one or two years, many new public chains have been/will be launched, which creates competitive pressure on Ethereum. However, from the development of relevant data, Ethereum 2.0 is still very competitive. The Ethereum Ecology is an important competitive force. According to the specifications of Ethereum 2.0 and Vitalik, the transfer from Ethereum 1.0 to Ethereum 2.0 will not have much impact on its ecology. But before the upgrade is completed, other high-performance public chains may compete for the developers and users of Ethereum to weaken or even replace Ethereum's leading position. Therefore, the smooth and timely implementation of Ethereum 2.0 is essential.

Copyright Information and Disclaimer

Unless otherwise stated herein, all content is original and researched and produced by TokenGazer. No part of this content may be reproduced in any form or in any other publication without the express consent of TokenGazer.

TokenGazer's logos, graphics, logos, trademarks, service marks and titles are TokenGazer Inc.'s service marks, trademarks (whether registered or not) and/or trade dress. All other trademarks, company names, logos, service marks and/or trade dress ("Third Party Trademarks") mentioned, displayed, quoted or otherwise indicated herein are the exclusive property of their respective owners. . You may not copy, download, display, use as a meta-tag, misuse or otherwise utilize a mark or third-party mark without the prior written permission of TokenGazer or the owner of such third party mark. .

This document is for informational purposes only and all information contained herein should not be used as a basis for investment decisions.

This document does not constitute investment advice or assist in determining specific investment objectives, financial conditions and other investor needs. If investors are interested in investing in digital assets, they should consult their own investment advisors. Investors should not rely on this article for legal, tax or investment advice.

The asset prices and intrinsic values mentioned in this study are not static. The past performance of an asset cannot be used as a basis for future performance of any of the assets described herein. The value, price or income of certain investments may be adversely affected by exchange rate fluctuations.

Certain statements contained herein may be TokenGazer's assumptions about future expectations and other forward-looking statements, and known and unknown risks and uncertainties that may cause actual results, performance or events and statements and Suppose there is a substantial difference.

In addition to forward-looking statements as a result of contextual derivation, there are words of “may, future, should, may, can, expect, plan, intend, anticipate, believe, estimate, predict, potential, predict or continue” Similar expressions identify forward-looking statements. TokenGazer is not obligated to update any forward-looking statements contained herein, and Buyer shall not place excessive reasons on such statements, which merely represent opinions prior to the deadline. While TokenGazer has taken reasonable care to ensure that the information contained herein is accurate, TokenGazer makes no representations or warranties, either expressed or implied, including the liability of third parties, for its accuracy, reliability or completeness. You should not make any investment decisions based on these inferences and assumptions.

Investment risk warning

Price fluctuations: In the past, digital currency assets have single-day and post-price fluctuations.

Market acceptance: Digital assets may never be widely adopted by the market, in which case single or multiple digital assets may lose most of their value.

Government regulations: The regulatory framework for digital assets remains unclear, and regulatory and regulatory restrictions on existing applications may have a significant impact on the value of digital assets.

Welcome to TokenGazer's official website: tokengazer.com to view the primary market depth research, secondary market rating reports and quantitative research, project valuation deviation data, investment strategy analysis and past exchange data analysis.

Editor in charge: TokenGazer

This article is the original content of TokenGazer, please indicate the source.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Bitfinex parent company submits a search application to the US court, intending to recover the frozen 880 million US dollars

- The World Internet Conference is coming. I found a blockchain company in Wuzhen.

- In the questioning, how does Libra's currency basket fall? Single anchor instead of integrated anchoring?

- The currency will be added to the legal currency transaction pair. The first supported legal currency is the Russian ruble.

- Exclusive interpretation | Tencent blockchain released 3 editions of white papers in 3 years, these landing applications are the most concerned

- Pick up IEO! Can Sthum's new gameplay at Bithumb Global Station create the next wave?

- After the 18 million bitcoins were dug up: these “18 million” milestones are also worth remembering