How does the secret whale "liquidator" help DeFi run smoothly?

Written by: Tom Schmidt, Junior Partner, Dragonfly Capital, Blockchain Investment Fund

Compile: Zhan Juan

Source: Chain News

- Bitcoin hashrate continues to climb, rising 167% over the past year

- Babbitt Site | Li Lihui: We should be more wary of global digital currencies, and super-sovereignty and super-banking will lead to financial disruption

- Facing quantum computing threatens digital currency to grow in confrontation

What is liquidation?

In the past two years, some decentralized lending agreements, including MakerDAO, Compound, dYdX, etc., have been released on Ethereum, allowing anyone to lend or borrow crypto assets without trust. Although these agreements differ in terms of listing methods, assets provided, loan terms, etc., the basic loan structure is the same. The borrower writes the collateral into a smart contract. In return, the borrower can borrow another asset from the lender in a smaller amount than the collateral. This form of secured loan is one of the most primitive financial instruments, dating back to the medieval Venetian banking industry, in contrast to unsecured, credit-based loans that consumers are more familiar with.

When the value of the collateral exceeds the value of the loan, a secured loan works well, giving borrowers access to liquidity without having to sell assets that are usually less liquid. However, when the value of collateral falls, rational borrowers have the incentive to abscond with loan assets, which may make the lender's assets insolvent. After all, why pay 100 DAI to redeem $ 99 worth of ETH?

For more traditional forms of secured loans, such as car equity loans or real estate mortgages, this is not a problem, as the value of these assets is often less volatile than crypto assets. However, when using ETH as a mortgage, its value can plummet within seconds.

Without liquidation procedures, mortgage loans may be risky

To reduce this risk, loan agreements typically require at least 115% of guarantees, leaving sufficient buffers before the value of the collateral falls below the value of the loan. If the value of the collateral falls below this level, the borrower can simply make up or sell the collateral to repay the lender and maintain the solvency of the financial system.

But this brings another series of problems. Transactions on Ethereum are not free. In addition, if the borrower is liquidated, he will not incur any additional costs, so no one has the incentive to participate in the liquidation and maintain the system's solvency. In order to reward individuals for the costs and risks that they incur when guaranteeing insufficient loans in liquidation, and to restrain borrowers from falling into a situation of insufficient guarantees from the beginning, the loan agreement will add additional costs to the liquidation and shall be borne by the liquidators themselves. In this way, anyone can pay off the debt of the borrower and thus receive a considerable bonus, thus paying for it by selling the collateral at a discount to the liquidator, while maintaining the solvency of the financial system.

Liquidators save lenders and maintain market solvency

Liquidator's life

Although different protocols differ in mechanism and terminology, they basically require the same components:

- A robot that monitors Ethereum's pending transactions and finds liquidation eligible loans

- A decentralized exchange that can be used to immediately sell clearing collateral and guarantee the profit of the clearer

- A smart contract that allows automatic settlement and sale of collateral in one transaction

Some protocols provide their own off-the-shelf tools to achieve the above functions, while others rely on a thriving self-made clearing robot ecosystem. The easiest way to understand these players and their role in the DeFi ecosystem is to browse through successful clearing cases in some of the most popular loan agreements.

Compound

In DeFi, Compound provides the most direct loan and lending experience, and its settlement process follows this simplicity. Let's take a closer look at the process of a liquidation.

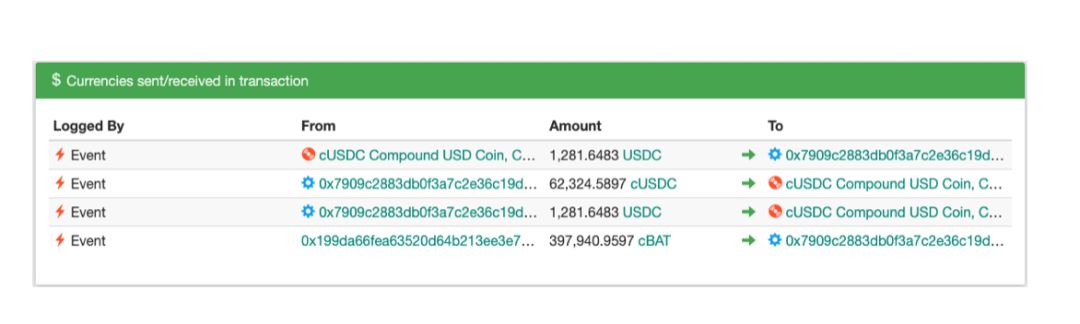

The liquidation involves two participants, one is our liquidator ( 0x64a ), we call it "Alice", and the other is our borrower ( 0xb5b ), we call it "Bob".

Bob borrowed a USDC loan from Compound and used ETH as collateral. This is usually done in order to use the borrowed USDC as a leverage to buy more ETH in a license-free manner. Unfortunately, the period of the loan coincided with the sharp decline in the price of ETH, which caused the borrower's collateral value to fall below the collateral ratio required for ETH ( 133% ). Because different assets have different qualities, price stability and liquidity, Compound assigns different guarantee ratios for each asset ( currently the highest REP ratio is 200% ).

Alice notices that Bob's guarantee ratio is lower than required-it can be guessed that this is either by monitoring contract status or using Compound's convenient liquidBorrowAllowed function-and calling liquidateBorrow in Compound's USDC market contract triggers the liquidation process.

- Compound first pays Bob any outstanding interest he receives from his collateral ( after all, this might make him exceed the required guarantee ratio )

- Compound uses the market price in their oracle to verify that Bob is in default

- Compound transfers the required loan asset ( USDC ) amount from Alice to the cUSDC market contract.

In this way, Alice received Bob's ETH collateral at a fixed discount ( currently 5% ) relative to the market price. The ETH collateral is returned as cETH, and the liquidator can either continue to earn interest from the debtor's ETH or redeem cETH as ETH on Compound. In this case, Alice got about $ 7 ETH for free through her own efforts.

When this particular liquidator holds cETH, other liquidators use smart contracts to automatically redeem and sell their c tokens, locking in the 5% profit they get from the transaction.

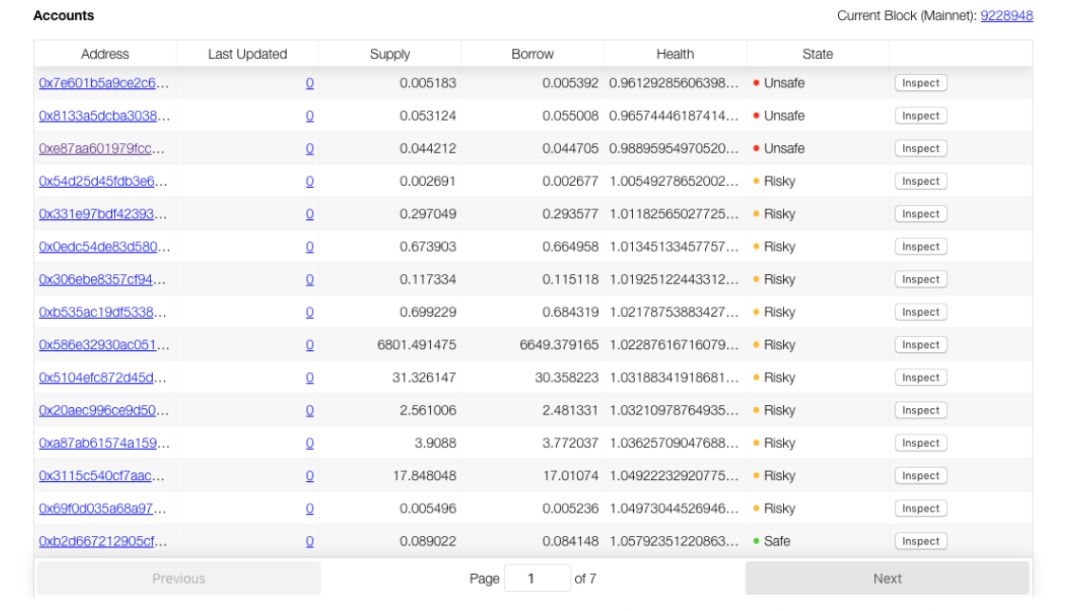

At first glance, one might suspect that such liquidation was done manually, especially considering that Compound has not released any open source clearing robots, and the clearing tracking dashboard is not too popular. However, when looking at the time distribution of the liquidator's activity, we can clearly see that it is active around the clock, so it is likely to be a robot.

Some lucrative undersecured loans are waiting for liquidators

More sophisticated robots will perform actions such as quickly borrowing money from Compound to clear other accounts. We saw this in this particular clearing, where the address redeemed its USDC loan and used it to clear the USDC loan of another account, easily earning 5% in one transaction.

Maker

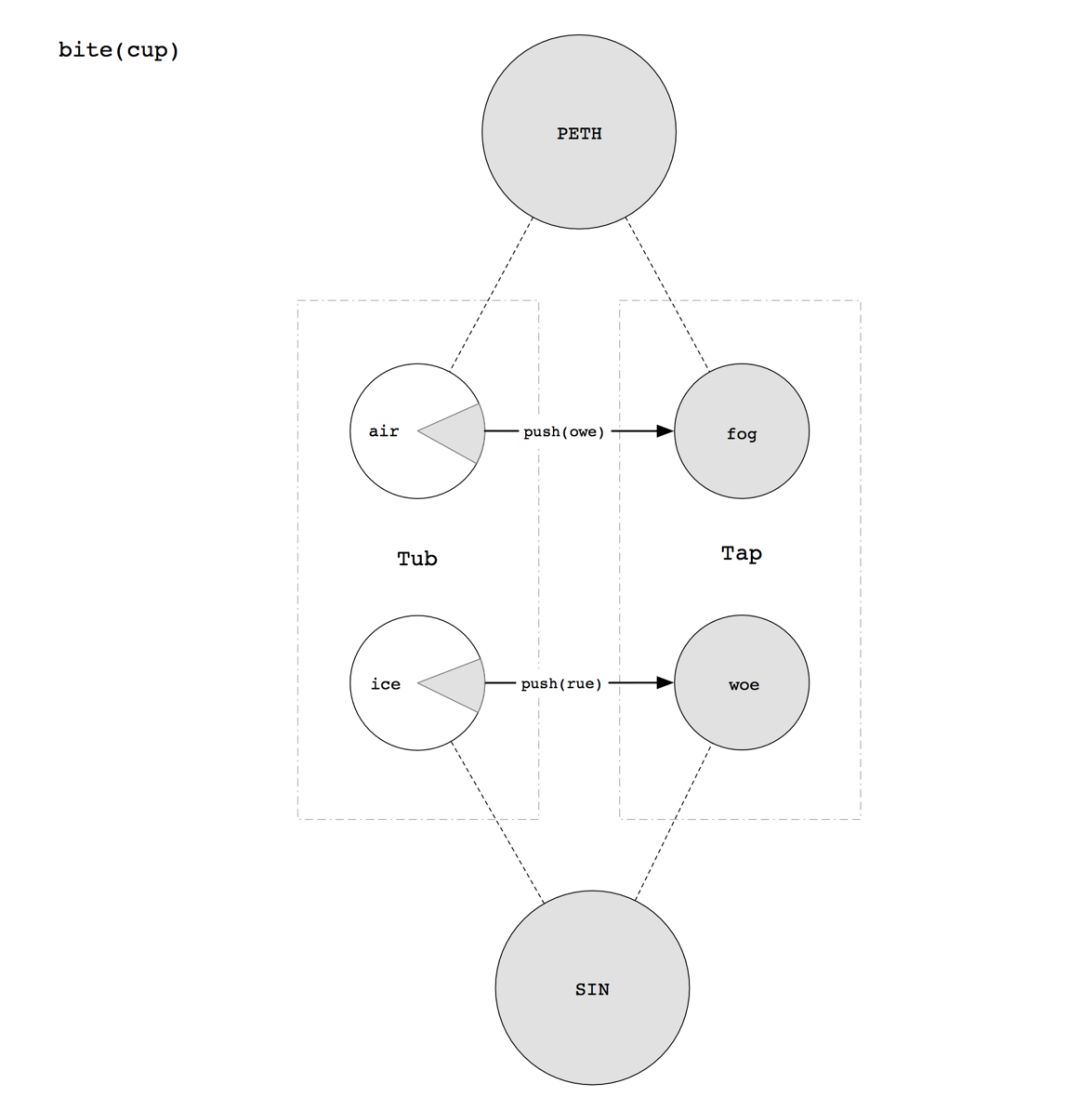

Maker's liquidation process is less straightforward because it is divided into two separate steps: first "bite" and then "bust". It's like the process of a car being liquidated: first it is taken back, and then it is auctioned to pay off the owner's debt. In the Maker system, loan recovery is triggered by calling bite, while liquidation is triggered by calling bust on their smart contracts.

Let's clear CDP 17361 through two transactions. The first and second transactions involve three participants: the recycler ( 0xc2e ), we call it Ralph; the borrower ( 0x9c3 ), we call it Brittany; the liquidator ( 0x5a2 ), we call it Larry.

Brittany borrowed 8.5 DAI with her 0.1 ETH as collateral, which made her loan fully meet the 150% guarantee ratio required by Maker. When the loan was lent, the market price of ETH was $ 170. Unfortunately, on December 27th, ETH dropped to around $ 125, leaving this mortgage bond ( CDP ) margin slightly insufficient, which caused Ralph to call bite on this CDP and take ownership of this CDP from SaiTub ( the contract Hold all valid CDPs ) to SaiTap ( the contract clears the recovered CDPs ).

By this time, the system was still under-guaranteed. In the Maker system, there are more outstanding DAI than ETH to support the value of DAI at the required ratio. Fortunately, as the liquidator, Larry discovered the CDP and paid 8.5 DAI, and bought the 0.067 PETH ( Ether Pool ) included in the CDP, which is equivalent to 0.07 ETH. This made DAI out of the market, increased the guarantee ratio, and maintained the system's solvency. With the efforts of Larry, he was able to buy ETH at a price of about 121 USD / ETH, which is a good discount based on the market price. Larry could immediately sell back DAI at Uniswap to lock his 0.002 ETH profit.

It's worth noting that although Ralph spent money on gas, which was risky for CDP and startup liquidation at Bite, he didn't actually make money from it, and Ralph got a nice 3% discount on ETH. His efforts paid off!

Although there are a large number of robots that will automatically "bite" and "bust" CDP in order to profit, only half of the "bite" of robots will profit from liquidation!

Not included in the compiler

So, are there a lot of "good Samaritan" robots in the free "bite" CDP?

Although a small part seems to do this, most robots cannot find a suitable price when performing unbust "bite" in order to throw discounted ETH during liquidation. For example, transaction 0x8b2 bites a CDP, obtains an ETH-DAI quote from Maker, compares it to the best price on a decentralized exchange ( DEX ) such as Oasis, and decides that it is best not to take a risk and let CDP stay In SaiTap. Another reason may be insufficient default tools provided by Maker. Although Maker provides a “ bite-keeper ” that can “bite” CDP, and an “ arbitrage-keeper ” that clears on a decentralized exchange for profit, but Some additional work is needed to merge them into a unified robot. With the transition to multi-collateral DAI, the system has turned to collateral auctions, and Maker's auction-keeper robots can participate in it, and the opportunity to purchase and liquidate collateral will be profitable.

Some of the largest robots use more advanced strategies, including:

- Spin-off CDP for redemption, exit ( exit ) CDP on ETH, and eat more debt via boom ( destruction ) on DAI to maximize returns

- Use gas tokens to bid more than other robots in gas auctions by using gas below the market price

- Spread ETH sales across multiple DEXs ( such as dex.ag or 1inch ) to minimize slippage and maximize the amount of DAI they get

dYdX

The settlement process of dYdX is a bit similar to Compound, but the difference is that dYdX does not expose a tokenized interface to its lending agreement like Compound does through its cToken. Instead, dYdX creates a series of trading accounts for each address in its main separate margin contract, and tracks the credit and debt ( ETH, DAI, USDC, etc. ) of each account in each market it supports.

Unlike Maker with bite and Compound with liquidBorrow, dYdX does not have such an explicit function signature. It has a single operate function and uses different "operation types", among which operation type 6 is responsible for clearing the borrower's account. Liquidators can buy collateral from borrowers at a discount of 5% and get the same healthy spread as Compound.

The dYdX contract itself also supports atomic transactions, allowing users to provide funds, clearing and withdrawing assets in one simple step. However, in the process of liquidation, the user himself will also have insufficient guarantees, thus putting himself at risk of being liquidated!

Fortunately, dYdX thought about this problem and provided its own agency contract, allowing users to both liquidate borrowers while maintaining their accounts within a secure guarantee ratio. This move has proven to be very popular, with more than 90% of the liquidation going through this agent. Therefore, it is not surprising that the dYdX clearing robot uses this agent by default.

dYdX is also different from other agreements in that the agreement has built-in fast borrowing, which allows the liquidator to borrow the required assets, liquidate and repay the loan in one transaction in an atomic manner, without using an external agency contract, so that Realize real free profits. Coupled with their accessible, off-the-shelf clearing robots, it may explain why dYdX clearing has become so competitive over the past few months, which we will mention later.

Although some dYdX settlements look similar to other protocols, when you look at them through traditional chain analysis tools, you will find that other protocols look difficult to understand because no token transfers actually occur and no actual exchange occurs. Only when we look directly at the function call can we see what is happening behind the scenes.

Here, we still have the liquidator Laura ( 0x679 ) and the borrower Brad ( 0xa0d ), but unlike other examples, Brad deposits DAI and lends ETH, which may be to short ETH. When Brad's collateral was lower than the required collateral ratio, Laura suddenly shot and bought 53.45 ETH at 7573.97. The actual price was $ 141.70 / ETH, which was about 4% higher than the market price at that time, and a profit of $ 289.05.

How much money does the liquidator make?

Leaving aside the technical details, it's more interesting to observe what these designs put into practice, especially when working with those profit-seeking members. The idea of running a clearing robot to generate returns and support these networks has attracted many individuals and funds, but as we have seen time and time again, there is no free lunch in the crypto space, and clearing is no exception.

Profitable

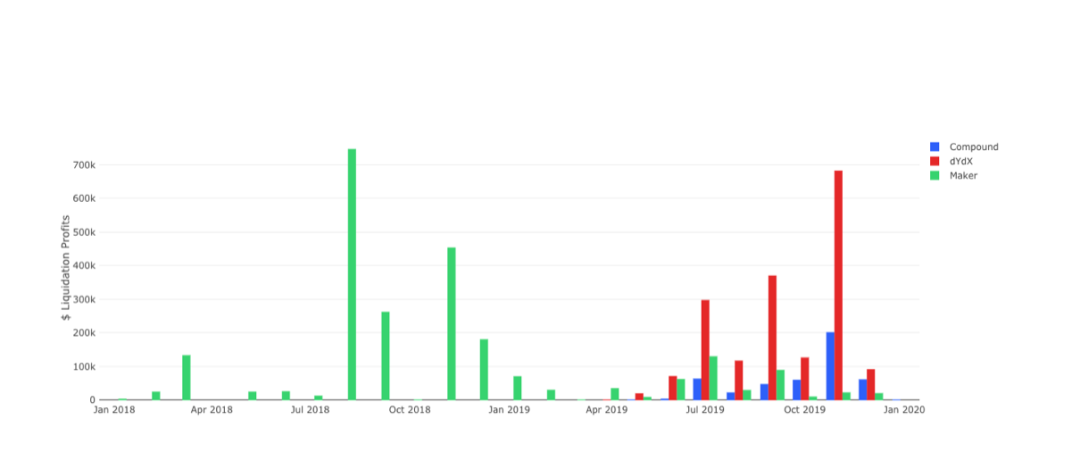

It is undeniable that the foundation of the concept of "generalized mining" in DeFi is valuable. Individuals can earn large sums of money by clearing loans on DeFi. Although the amounts vary based on clearing fees, assets, and market fluctuations, we have found that these agreements have brought liquidators close to $ 1 million in net profits in some months. During the validity of these agreements, we saw liquidators earning nearly $ 5 million in profits. In some cases, we have even seen some liquidators earn more than $ 100,000 in a single settlement!

Profitability of liquidators in the above agreements in recent months

But competition is rapidly increasing

Liquidators are attracting attention because of the low barriers to entry, high profit margins, and readily available tools, which in turn can attract competition and reduce the profitability of existing liquidators. We can see this effect in several ways.

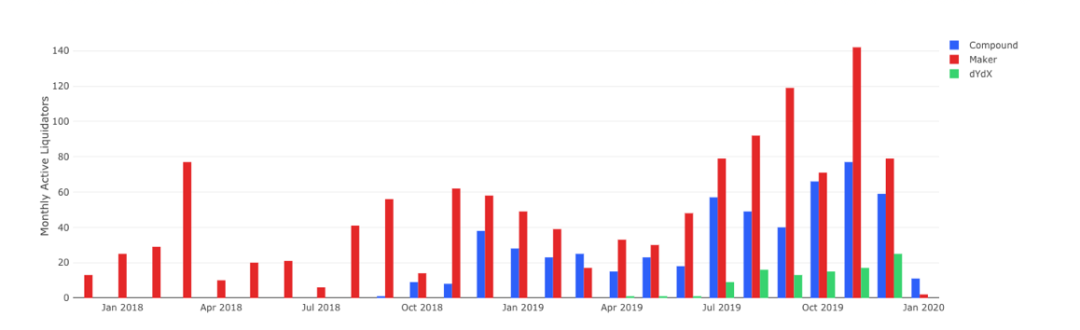

First of all, it is simple. Since the introduction of these agreements, the number of unique addresses attempting to liquidate agreement loans has increased significantly, from the 25-month living liquidator in January 2018 to the 142-month living liquidator in November 2019. Although liquidators may share or rotate addresses, causing some duplication, the overall trend is clear.

In recent months, the monthly liquidator in the agreement

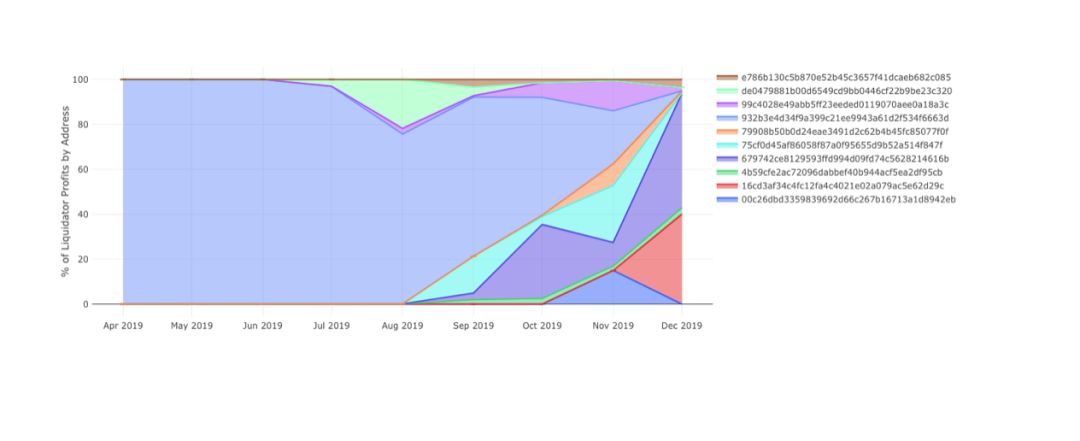

Looking at the changes in liquidators' profit share over time, we can also see this competition. We can see that as the new rising stars start to win in the competition and win the liquidation bonus, the "old school" liquidators are slowly being squeezed.

The profit share of each liquidator's address on dYdX changes, and the old school liquidators are slowly defeated

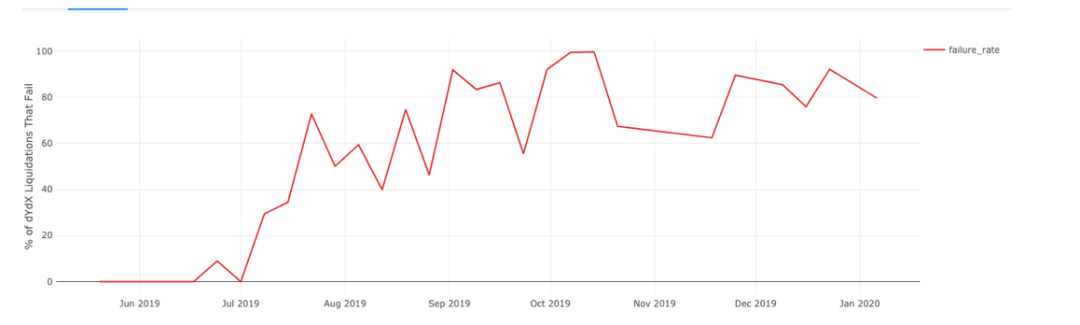

Looking at the gas price auction between the liquidators to grab a huge profit can prove this again, which is very similar to the auction between DEX arbitrage robots. Each clearing can only have one winner, which means that after each clearer's transaction is mined, the winner not only loses the clearing bonus, but also wastes a certain amount of ETH in the failure of clearing calls. If just looking at the list of failed dYdX clearing transactions is not enough to convince, we can also observe that over time, the proportion of successful dYdX clearing calls has dropped significantly, which indicates that competition in this field is increasing.

dYdX clearing call success rate is getting smaller and smaller, indicating increased competition

Borrowers are getting smarter

But liquidators are not only facing competition from other liquidators. Borrowers themselves are using new tools to protect themselves from liquidation from the start. DeFi Saver ( formerly CDP Saver ) monitors user loans and "discharges" them when they are at risk by selling borrowed assets, buying more collateral, and re-guaranteeing the loan in one transaction This is very similar to Maker's own cDP-keeper.

Although DeFi Saver had problems protecting CDPs during periods of severe network congestion, we can see that it was properly launched and started lifting CDPs during the ETH price drop, saving 3% of the liquidation penalty for the owners of these CDPs.

When the price of ETH drops, DeFi Saver starts and protects CDP

What is the future of liquidation?

Now that we have a vision for 2020, what are our predictions for the future of the clearing field?

Reduce profits and transfer to dynamic systems

First, let's take a step back and re-examine what we will have a liquidation penalty. The purpose of these penalties is to encourage borrowers to maintain solvency and to encourage liquidators to step in and stabilize the financial system when the borrowers are nearing default. As we have seen so far, punitive measures are very effective in both areas. The question now is what the optimal liquidation penalty should be—a static amount that does not change over time, assets, and borrowers may be the next best option—we believe that this issue should be determined by the market.

We've seen the ecosystem moving in this direction, and Maker is moving from SCD's fixed-price collateral sales to multi-collateral Dai's full collateral auctions. In this case, the liquidation penalty is not so clear, and the form of "minimum bid increment" ensures a certain gap between the real market price and the auction price. Given that MCD is already building a competitive clearing ecosystem, we may see that the “minimum bid increment” will gradually decrease over time, effectively reducing the liquidation penalty and letting the market decide that collateral should be paid s price. Although this is not a loan agreement, we can compare the rebalanced auction of Set Protocol to that they sell part of one asset in exchange for part of another asset, and then let the market determine what the exchange rate should be through auction.

I expect that more loan agreements will shift to auctions or variable fee systems in the coming year, which means that borrower fees will be reduced and liquidators' profits will be reduced.

Unsecured loan

So far, we have discussed secured loans with remaining collateral to be liquidated, but secured loans are only the first step in establishing a decentralized financial ecosystem. We believe we will also see an ecosystem of credit-based unsecured loans in DeFi, enabling more people to start using these protocols and build more use cases. In this area, liquidation will become less or irrelevant, and if this form of loan starts to eat away at the market share of mortgages, it will put the current liquidation market at risk.

in conclusion

The liquidator's story follows the pattern of many other crypto stories: license-free access to some financial instruments that help an ecosystem of anonymous global innovators design new products and strategies, and thus gain millions of dollars reward. These unknown heroes helped the DeFi loan market expand to nearly $ 750 million while building confidence in lenders, which is critical for DeFi to reach the next million users. There will be new DeFi options and synthetic asset markets coming online next year, and I expect to see more operators like liquidators who work hard to keep things running behind the scenes, and thus get rich returns.

Thanks to Haseeb Qureshi, Brock Elmore, Antonio Juliano, Calvin Liu, and Teo Leibowitz for editing earlier versions of this article. The author authorizes Lianwen to translate and publish the Chinese version of this article.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Will it pull back after the rally? How long can this wave of market last

- SEC: IEO may be unregistered securities, the relevant exchange may need to apply for a stock exchange

- Really sweet! Big data shows that 2020 blockchain will become the world's most popular hard skill

- Science | Exploring Validator Costs for Ethereum 2.0

- Demystifying the data on the Bitcoin chain in 2019: Global miners' annual total revenue is about $ 5.2 billion, and Coinbase has become the "gold king"

- Popular Science | Eth 2.0 Staking Logic

- 2019 Blockchain Security and Privacy Ecology Memorabilia