"Insurance + blockchain": I have a chain, who is coming to the league?

In October 1347, the captain of the Italian merchant ship "Saint Collera" found the wealthy businessman George Lek Velen. The merchant ship was about to cross the Mediterranean reef and hurricane belt, and transported a batch of valuable cargo from Genoa to Machoca. The captain signed an agreement with Lek Velen: the captain pays a sum of cash. If the merchant ship arrives in Machoca, the money will be owned by Luckville, otherwise he will bear the loss of the cargo on board.

This is the world's first “policy” and is currently in the Genoa Museum in Italy. Although not perfect, it has the basic elements of insurance: there are insurable risks, a certain fee, and an agreement to reach a contract.

At the time, this behavior was extremely risky. Lek Velon does not know the statistics of the merchant ship distress. He can only bet on the instinct, or that it is just a willful game for the rich.

Today, for insurance companies with risk control and asset management as the core, this is entirely gambling. The empowerment of science and technology in the insurance industry cannot be accomplished without the perfection and precision of the wind control model. For the insured, spend money to buy peace of mind, and seek a guarantee; for insurance institutions, a large number of funds to bear the accident of a few people.

- Getting started with blockchain | Why does EOS recharge to the trading platform and need to fill in the notes but not present?

- Internet vs blockchain revolution: the origin of the giant company

- The blockchain grew up in the classic "spoken war", who made it? Who makes you sad?

But throughout the contract period, there are many uncertainties and fraudulent behaviors, all of which stem from the “information asymmetry” between the insured and the insurance institutions.

The blockchain technology has the characteristics of “distributed database”. The participating parties can jointly maintain the same account book, which can effectively solve this problem in the business, thus helping the insurance institution to better formulate the insurance risk control model.

Insurance market trapped beast

Until the end of 2016, the insurance density (per capita insurance premium) and insurance depth (the ratio of premium to GDP) in China's insurance market remained only 329 US dollars and 4.2%, compared with the global insurance market's premium density of 689 US dollars and 6.2%. There is still a big gap in the depth of premiums. Therefore, from the perspective of industry development space, insurance products also have huge growth potential.

"One person is affected by the disaster, and everyone shares it." The important appeal of the human destiny community is to confront risks and solve risks. This mode of thinking has continued from ancient group behavior.

Around 2500 BC, it was recorded in the form of cuneiforms in the Hammurabi Code, the earliest human law on insurance: the king of the Babylonian kings ordered monks, judges, village chiefs, etc. Taxes, as funds for relief fires.

In the fifteenth century, the demand for insurance in Spain and other countries with high frequency and high-risk navigation activities in the wave of large-scale waves directly contributed to the birth of the first marine insurance code. Therefore, to this day, in the countries of the marine legal system, residents have a strong sense of insurance, but still have not reached a consensus in the entire human society.

In China, the insurance industry is still in a slightly embarrassing position.

In February 1979, the People's Bank of China National Branch Presidents Meeting was held in Beijing, making major decisions to restore domestic insurance business. Only 40 years ago, the domestic insurance industry resumed domestic business. In China, insurance is a young industry. The industry is in a relatively backward state regardless of the practitioners, policies, and technologies.

Compared with foreign markets, there is still a huge room for growth. Financial technologies such as ABCD will be a springboard for the rapid growth of the insurance industry. PricewaterhouseCoopers presented in the 2019 Insurance Industry Trends, in front of solutions such as cheaper and more efficient artificial intelligence, blockchain, cloud/SaaS, robotic process automation (RPA) and intelligent process automation (IPA) It is obviously not appropriate to continue to rely on slow and slightly clumsy old systems and equipment. New solutions must be relied upon to improve risk screening and help reduce costs.

Blockchain + insurance case

How does the blockchain empower the insurance industry? Wang He, executive director and vice president of China People's Insurance Co., Ltd., believes that the blockchain has five characteristics: sociality, uniqueness, timeliness, security, and efficiency, which can help the insurance industry to rebuild trust and improve efficiency.

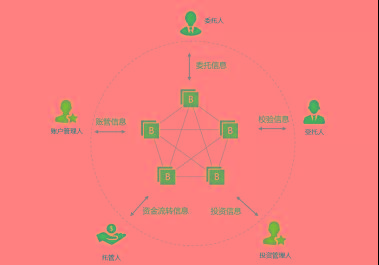

1. Reinsurance blockchain: insurance alliance

Reinsurance is insurance insurance. In June 2018, China Re Group and Zhongan Technology jointly issued the “Reinsurance Blockchain White Paper”. The report analyzed the two major pain points of the reinsurance business. On the one hand, the information sides of the transaction are asymmetric, and there is moral hazard : the original policy. The data is controlled by the direct insurance company. It is difficult for the company to obtain contract information and there is operational risk. The reinsurance company cannot obtain data in real time. The wind control model only relies on estimation and there is a risk of lag error. There are many reinsurance claims participants, and the process is complicated. Benefits may exacerbate the insufficiency of reinsurance information.

On the other hand, the reinsurance industry has a low level of informationization. Contract signing, trading, underwriting, reconciliation, etc. are all manually counted and entered into the data. There are problems such as repeated entry, information distortion, inefficient data mining, and inaccurate risk control model.

The person in charge of the blockchain product operation of Ping An Financial Accounts said that they are also using the blockchain to solve the problem of reinsurance. "There are many reinsurance business participants, including direct insurance companies, reinsurance companies, insurance brokers, etc. It is a typical scenario of 'multi-participants, large amount of data, difficult information synchronization, and disputed data ownership.'

“The same insurance institutions, there is a competitive relationship between direct insurance and reinsurance companies, and they are not willing to share the full amount of information.”

He introduced that the blockchain application has inherent advantages in the field of reinsurance. First, as a distributed database, all participants jointly maintain a ledger, which solves the problem of information asymmetry, and errors can be detected and processed in real time. Second, the cryptographic nature of the blockchain enables data sharing.

At present, the blockchain reinsurance platform has been commercialized.

Regarding the technical architecture, the person in charge said that the difference in financial account-books lies in its data privacy protection scheme, which enables the “sharing” of data to be available while protecting data privacy and security.

According to Xie Danli, Technical Director of Blockchain of Ping An Financial, Ping An FiMAX adopts a full encryption scheme. All participants in the blockchain network must encrypt the data and then upload it to the blockchain through the encrypted node. Network, the owner of the data has the right to control the integrity of the data.

In addition, he added that Credit Book has independently developed 3D Zero Knowledge Proof (3DZKP) and field level licensable decryption scheme. 3DZKP can complete the verification of a string of ciphertexts "+, -, *, /" within 3 milliseconds, ensuring that the third party can verify the legality of the book data in a state where it cannot be decrypted in all the cipher texts of all books. Correlation with data to enable cross-validation of data in the case of encryption.

2. Commercial health insurance: blockchain is a stepping stone

In foreign countries, the proportion of life insurance, health insurance and old-age insurance in life insurance is almost one-third. However, according to data from the China Insurance Industry Association, domestic health insurance accounts for only 12% of the life insurance business, and there is a large room for growth in the market. There are many factors restricting the development of commercial health insurance. The most important point is that it is difficult for insurance companies to obtain accurate health information of the insured, and it is impossible to formulate accurate wind control models and insurance products.

Any data-related business is sensitive, and health data is particularly relevant to personal privacy. In general, personal health data comes from the collection of medical institutions. Given the risks, benefits, and safety issues, healthcare organizations are reluctant to share data. However, these data are key to the development of insurance companies.

A blockchain that superimposes cryptography or an effective solution. Under the premise that the data does not leave the medical institution, the insurance company enters the database through the black box algorithm and applies the ciphertext data to calculate the desired result. However, it is not easy to open the door to the hospital. More problems are not in technology but in business model.

The practice of Sunshine Insurance is to obtain data through user authorization.

In August 2018, Sunshine Insurance launched a block-based female-specific disease insurance product. According to public reports, the product can authorize the insurance company to go to the relevant hospital or medical examination institution to view the personal medical report data through the user's health introduction letter. Successful authorization and effective reporting, giving users the appropriate value feedback.

This part of the authorized data "its data usage rights are registered in the blockchain, and will be permanently owned by the customer after the authorization. Under the authorization of the individual, it can be used freely and conveniently in different scenarios to achieve the function of data circulation. ""

3. Insurance Pass: Data knows you but doesn't know you

In October 2018, Zhongan Insurance launched the first insurance asset certificate product “Flying E-Life” on the Open Assets Agreement.

Song Wenpeng, technical director of Zhongan Technology Blockchain, told Zinc Link that the blockchain world must be connected with the real world in order to generate greater value. The Open Asset Protocol is a generalized abstraction of real-world assets that is designed to describe real-world assets of all kinds.

He introduced that the formation of “flying e-life” is divided into three steps: the first step defines the detailed product intelligence contract, and the detailed life cycle of the product, “flying e-life” includes a main insurance seven insurance, each Attached insurance contains a product state machine, such as flying to enjoy the life insurance, claims, surrender, renewal, reinsurance, etc.; the second step when the user purchases to enjoy the e-life, will form an insurance certificate (a Equity voucher) directly maps an instantiated policy; in the third step, the user can view his or her voucher list through a visualized voucher wallet.

He added that the most intuitive experience for users is that airline delays automatically claim.

As for the data privacy issue, Song Wenpeng believes that data privacy protection is carried out in a pass-through manner, and all or part of the privacy data is stored according to the data attribution. Only the Hash after the data is confirmed is saved, and the data based on the data confirmation is opened, and the data is returned to the user to the maximum extent.

4. Funding

Fun Chain Technology and Agricultural Bank, Taiping Insurance have landed a blockchain-based pension escrow project. According to Qi Lizhong, co-founder of Fun Chain Technology, in the blockchain system, the trustee initiates the payment operation and distributes it to the three participants. They will perform their respective operations and then write a smart contract: when completed After the party's confirmation, the funds can be placed. The entire process changed from serial to parallel, and the time was reduced from 12 days to 3 days.

In addition to shortening the business cycle, multi-center maintenance of the same ledger improves the transparency of the entire process, intelligent contract implementation process automation, encryption technology to ensure data security and credibility.

Li Lizhong told Zinc Link that in addition to ABC and Taiping Insurance, it is still considering the project with other institutions. Nowadays, the industry is in an open stage, and each is in a political position. The business cannot interact and is in a state of fragmentation, forming multiple chains.

How to open up various platforms to form an alliance will encounter many difficulties in terms of governance technology and business level. Li Lizhong believes that the fun chain plays two roles in it. First, the technology integration, the interesting chain can support our platform to integrate with more than 30 other platforms, cross-chain communication, and the second is for all walks of life, more is to Cooperate in the treasury business.

In addition, according to the introduction, Fun Chain Technology's “insurance + blockchain” application also includes “credit insurance” for SMEs based on supply chain finance, which not only slows down the risks of supply chain finance, but also utilizes blockchain to realize supply chain. Layers of credit in the financial system.

Data is the core problem

As can be seen from the above cases, the application of blockchain in the insurance industry is mainly to solve the problem of inter-institutional collaboration, mainly based on B-end applications. On the one hand, technology is inherently low-level, and end users are hard to perceive and do not need to perceive. Moreover, the decentralization of the blockchain also determines that it is suitable for collaboration between multiple agencies, rather than for C-side interaction, because the center must be a large organization.

Financial technology is the most widespread scene of the blockchain. Among them, the bank has the strongest momentum. In contrast, the pace of the insurance industry is slightly slower, and the resistance is even greater when pushing new technologies such as blockchains.

The insurance industry, especially the domestic insurance industry, is in an awkward position. Insurance itself has a short industrial chain and cannot provide enough back-end data for products. It needs to be combined with other industries and scenarios to capture data from it. However, the current insurance awareness of enterprises and individual users is lacking, and insurance is not a necessity, so the data formed is limited.

Without data, there is no precise wind control model, and insurance is worthless. Therefore, “insurance companies want data for everyone”, including peer data, data from other industries, and user data.

In order to share data between organizations, in addition to technically solving data security, privacy, governance and other issues, a set of business models including data ownership and income distribution should be recognized by the participants. Do not solve this problem, empty chain, no participants, why blockchain?

Technical problems can always be solved, but the business model of multi-interest distribution is difficult to find the balance point. This is a proposition that is difficult to understand in any technical era.

Text: Chen Haining

Editor: Wang Qiao

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Want to send coins? Samsung is also coming to join in the fun.

- Blockchain has entered the era of “Hundred Schools of Contention”, here is the judgment of more than ten of the strongest brains.

- Research | IEO is accelerating to the stage of exhaustion?

- Two minutes to see the change in the market value of cryptocurrency in 6 years: the currency diversity is enhanced, Bitcoin is always king

- Babbitt column | What is the cross-chain across?

- Xiao Feng: The Internet of Things business needs to form a closed loop, which must complement the blockchain.

- Tentative, conservative, fried leftovers, Tencent this game actually dominated the list for 15 days