Interpreting the intent-centered landing challenges starting from UniSwapX and AA

Interpreting landing challenges from UniSwapX and AAAuthor: Shijun

Recently, in the article “Intent-Based Architectures and Their Risks” by LianGuairadigm, a well-known Web3 venture capitalist, “intent-centric protocols and infrastructure” ranked first among the top ten trends in the encryption field. This has attracted industry attention to the Intent-centric architecture and this track, combining the Bob the Solver project at the ETHCC conference in Paris and years of exploration by Anomo and DappOs. Its core goal is to significantly improve the user experience and completely eliminate the complex transaction details, making it seen as a new engine for the popularization of Web3.

In the Token2049 hackathon competition, the author also worked with the AstroX wallet technical team (a ToB-side service focused on high ROI growth products) to implement the second-place project in the DeFi track based on the intent concept: Ethtent. This article will discuss Intent-centric starting from the author’s own implementation of Solver and the application of ERC4337 and UniSwapX.

What is “intent”? Can it be so beautiful? What are its applications? What are the challenges in implementation?

- Summary of The Biography of Musk Want to Learn from Ma Yilong? Are You Crazy? Note Ma Yilong is a Chinese martial arts actor known for his unique fighting style. The original text is making a playful reference to learning from someone like Ma Yilong while discussing the biography of Elon Musk.

- Shanghai Metaverse’s major application scenario ‘Hero’s Post’ has a follow-up. Baidu, Alipay, and others are competing for it, and the achievements are being realized.

- CEX Reserve Proof Investigation, which one has the highest risk?

1. Review of What Intent-centric Is

Just as the concept of account abstraction is even more advanced than the development of Ethereum itself, the specific concept of “intent” can be traced back to the design concept of the DEX Wyvern Protocol in 18 years. The core point of its concept is that, unlike the emphasis on traditional transactions, for ordinary users, what they have been pursuing is actually the consistency and accuracy of the results, not the seamless execution process.

Assuming a scenario where I want to complete a swap of a certain token.

-

In traditional transactions: I need to carry out 3 transactions, transfer ETH as gas, give an approve authorization transaction, and then submit the swap transaction;

-

In intent-based transactions: I only need the user’s signature, stating that I am willing to use X tokens to swap for as many Y tokens as possible, quickly, and with a 1% fee.

We can understand intent-centric protocols as a set of signed contracts that allow users to outsource the transaction process to a third party without giving up complete control over the transaction.

Users only need to specify their intent, and a signature can complete all operations.

That is, a transaction = how you specifically do it; intent = what you want, but you don’t have to worry about how to achieve it.

Compared with the development process of the traditional Internet, it has undergone the same experience, from service providers selling what they have to matching what users need, and then to intelligent service platforms. Looking back at the evolution of the Internet over the past 20 years, the core trajectory is:

Early vertical services (various portal entrances, users looking for numbers, workers, and services themselves);

Mid-term service aggregation platforms (such as 58.com, which aggregates traffic to match service providers with user needs);

Late-stage intelligent platforms (combining algorithmic matching and recommendation to improve intent accuracy, such as Didi’s intercity ride-sharing, customized services).

It can be said that the concept of Intent-centric is indeed beautiful, and the development process of web2 has also verified that this is the key path to expanding the user base. But can it really be so beautiful? Let’s start with the market application.

2. Typical Applications of Intent-centric

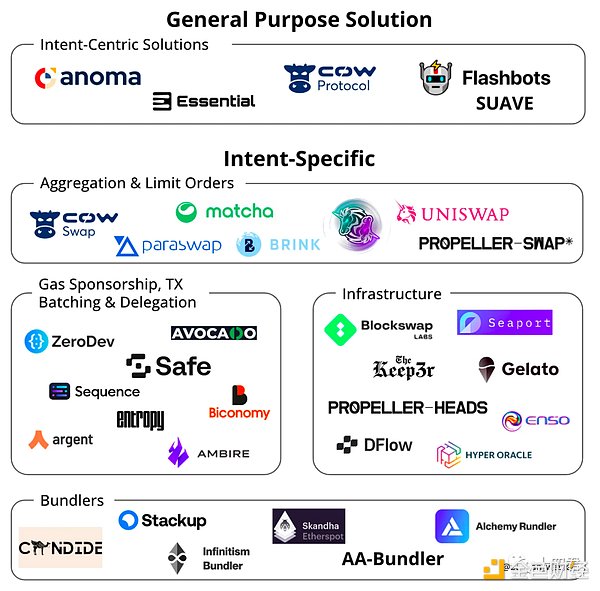

Although the concept of being intent-centric has just been proposed, the number of projects involved is no longer small, or many of the projects themselves are centered around user intent. In this article by Bastian Wetzel, various mainstream projects are also classified.

As can be seen in the following figure, many protocols are not actually general intent solutions, but specific intent solutions, such as Uniswap, Seaport. This is also the inevitable development path for intent-centric solutions compared to the vertical solutions done by web2.

ERC-4337, on the other hand, is an infrastructure that assists intent, and the existence of bundlers reduces the necessity of users’ original gas.

But our core goal is still to explore the business models of these projects and whether they are sufficient to support the implementation of intent. In my opinion, the most cutting-edge project currently running on the ground is UniswapX, which focuses on the implementation of intent around transactions, and ERC4337 will serve as the necessary infrastructure for intent. 2.1 Intent-centric from the economic design of UniSwapX.

After the announcement of UniSwapX, I participated as a filler and a quoting participant in the RFQ system. The reason why I say it is one of the most cutting-edge and implementable intents is that it is the most mature system that directly solves the economic incentive problem of intent opponents.

2.1.1 Why do we need UniSwapX?

Summarizing the development of Uniswap V1-3, it can be said that past AMM protocols have faced specific issues such as user costs, transaction prices, transaction routes, routing services, and LP incentives. Now, the market situation of Swap can be said to be completely surrounded by MEV in the on-chain memory pool, and almost every large-scale Swap transaction is facing sandwiching. Users always trade at the worst price, and the profits are taken by MEV.

The launch of UniSwapX is an attempt to tackle these problems from another dimension by completely changing the AMM transaction mechanism.

2.1.2 What is UniSwapX?

By definition, UniSwapX is a new permissionless, open-source (GPL), auction-based routing protocol for trading across AMMs and other liquidity sources.

In fact, there are three types of trading market operation models for Web3, in addition to the AMM model:

On-chain order book model for on-chain matching and trading.

Off-chain order book model for on-chain matching and trading.

UniSwapX has transformed from the AMM model of Uniswap V1-3 to the off-chain order book model for on-chain matching and trading.

2.1.3 How does UniSwapX work?

From the user’s perspective, if the scenario is that the user wants to trade ETH<=>USDT at a price of around 1900 (allowing a 2% slippage), all they need to do is:

Select an order and set a time limit for the order based on the price decay curve (e.g. exchange 1 ETH for 1950U within 1 day, with a minimum of 1850U)

Sign the order and publish it to the order book service cluster

Wait for the transaction to be discovered and completed by the Filler

For the user, that’s all they need to do.

From the Filler’s perspective, they are the ones actively completing user transaction orders. They have ample funds, proficient information cross-chain services, and a service provider that monitors the entire chain and DexPool status. They need to:

Scan the pools of various protocols on the chain to build the basic data needed for real-time order calculation

Scan the Mempool to estimate the future price change trend

Scan the dedicated network of RFQ Fillers to get priority trading rights by providing quotes

Scan the order information on the public network of Fillers and analyze the optimal trading path

If the revenue conditions are met, participate in the bidding (every minute counts, as the later the transaction is on-chain, the lower the ending price in the Dutch auction mode)

Analyze the bottom line of bidding from other Fillers and prioritize their bidding in the next profitable order (even if my single income may decrease, I will get more order volume)

So why does he have such motivation for trading? This brings us back to the economic model of UniswapX.

2.1.4, How to evaluate the intent design of UniswapX

The key issue in implementing the intent itself is the willingness to publish it.

In the past, DEX faced many limitations compared to CEX, such as transaction costs, MEV, slippage, impermanent loss, etc. In the future, they will be confronted by a more professional group of Fillers to compete with the MEV group, gradually taking a piece of the pie in the technical competition, and finally returning to the hands of the users, forming a positive development cycle (more users using UniswapX, more Fillers receiving fee dividends).

Furthermore, the complexity of on-chain transaction splitting and routing will be dispersed into backend systems, so users only need to submit orders as the party A without having to worry about the complicated routing issues.

Therefore, this is a virtuous economic cycle where both parties benefit, and a sound economic model will always be implemented.

Further reading: https://research.web3caff.com/zh/archives/10004?ref=shisi

2.2 Viewing intent-centric from ERC4337

In the application diagram mentioned above, the bottom part is the section centered around the account abstraction AA. For systems like UniswapX, since the transactions themselves are submitted by Fillers, users can complete cross-chain transactions without the need for gas.

However, throughout the entire transaction cycle, users still need to submit an approve transaction to allow UniswapX’s on-chain contract to deduct funds from the user. If they want a purely intent-based transaction model (completely without user-initiated transactions), ERC4337 is still needed as the account entity and integration design of LianGuaiymaster.

In simple terms, ERC4337 is an infrastructure.

On-chain, the entryPoint contract is used to verify the user’s signature for authentication, ultimately driving the user’s CA account as the identity subject.

Off-chain, UserOperation is signed by the user as an instruction, transmitted through the Bundlers network, and batched by Bundler for on-chain execution.

The optimization core of this mechanism is the ability to enhance local functionality through the highly customizable CA, such as social recovery wallets, or project parties paying gas fees on behalf of users, supporting USDT as a gas payment method, and other functions.

However, today we will analyze the value of 4337 to intent from a business model perspective.

Looking back at why UniswapX is considered to have a good business model, it is because both parties involved in the token transaction (users and fillers) benefit from it, with only MEV being the losing party. But if we think about it, ensuring the profit and willingness of the counterparty through fees is only one type of business model, and in the future, most “intent” applications will directly generate revenue through B2B or charge renewal fees to customers, but the main product’s service is not limited to fulfilling the “intent”.

Just like payment systems such as WeChat Pay or Alipay, they do not charge fees for C2C transactions, but generally charge a 0.6% fee when merchants withdraw funds (which also needs to pay the underlying transaction system).

In the past decade’s mobile internet war, the focus was mostly on achieving high user numbers, and the closed loop of revenue could be placed after the user base.

Therefore, there will be more DApps in the future, and in order for users to experience and use their DApps, they will be happy to provide users with servers that exempt them from gas fees. This is similar to the Lens social protocol, where on Polygon, in order to cultivate users’ usage and content ecology, they first pay tens of thousands of dollars in gas fees for users every week. And compared to the subsidy cost of tens of millions of dollars consumed daily during the previous ride-hailing war, this is just a drop in the ocean.

Therefore, the most standardized, most universal proxy payment mechanism, and the most trustworthy platform credit system will inevitably be the LianGuaiymaster system on ERC4337 (derived from meta-transactions but beyond meta-transactions).

It is a special smart contract account that can pay gas fees for others. The main payment contract needs to perform some verification logic for each transaction and check during the transaction. The LianGuaiymaster contract can check if there is enough approved ERC-20 balance in the “validateLianGuaiymasterUserOp” method, and then use “transferFrom” to extract it in the “postOp” call.

In summary, this is a gas-free solution that is more universal than meta-transactions, without non-standard confusion and forward compatibility issues (meta-transactions require contract modifications for support).

3. What are the challenges of implementing Intent?

In conclusion, intent is indeed promising, and it will inevitably continue to develop and optimize. Apart from the challenges of the business model, what are the core technical difficulties in its implementation?

3.1 Contradictions with AI integration

Although many analysis views of intent believe that the transaction intent analysis capability provided by AI is an optimization point for user experience, the author has worked in the security strategy industry before, and one of the major insights gained during that time is that interpretability and reconstructability are the most important aspects of AI application in strategy scenarios. For example, in the case of account suspension, if accurate reasons for the strategy hit cannot be provided, it will be difficult to justify once the user complains. Similarly, for any financial system, the pursuit of stability and consistency is the top priority, and no institution can guarantee that AI will not act maliciously once it has control over asset permissions.

Therefore, AI can only serve as an auxiliary tool for intent analysis for a long time, and the analysis of on-chain data requires a deep understanding of the operating principles of blockchain. Otherwise, false reports are likely to occur.

3.2, Anti-Dos Risk of intentPool and Solver Matching Problem

For intentPool, similar to the memory pool of ERC4337, it will also be a major bottleneck. First of all, intentPool cannot reuse the memory pool mechanism of current Ethereum clients (Geth, Eirgon), and must be built separately.

Even with BundlerPool of ERC4337 as a reference, there are still advantages and disadvantages in MemPool design.

Decentralized memory pool mode: There is a problem of propagation mechanism because for many applications, executing intent is a profitable activity. Therefore, nodes operating the intent pool have the incentive not to propagate in order to reduce competition when executing intent.

Centralized memory pool mode: It solves the problem of propagation mechanism, but cannot avoid centralized auditing and intervention.

In short, it is not easy to design an intent discovery and matching mechanism that is both compatible with incentives and not centralized.

3.3, Intent Privacy Risk

Signing has an irrevocable feature, even if an expiration time is added to the signed content, there is still a problem of low-cost cancellation of the signature before this expiration time (all cancellations must be made by sending transactions on-chain).

Therefore, some standard and privacy-preserving general intent solutions such as Anomo have emerged.

Protecting privacy is difficult to achieve through the EVM system, so there are currently more cutting-edge developments around new privacy-preserving intent languages, such as juvix, which are used to create privacy-focused decentralized applications. It can be compiled to WASM or compiled to circuits using VampIR for private execution on Anoma or Ethereum.

4, Conclusion

In fact, it is very gratifying to see the concept of intent becoming popular. Finally, web3 is not so self-indulgent, and it has begun to explore ways to break through the bottlenecks that truly serve real users. Only by starting from the most practical needs of users, rather than indulging in high-level narratives, and providing intimate services, can we gradually win the favor of a wide range of users.

In the future, the pattern of Intent will either be similar to UniswapX, where revenue subsidies are created for the counterparty from transaction fees, or from the perspective of the overall system user hierarchy, there will be a small number of high-paying high-value customers and a large number of users who do not pay but are important for the ecosystem.

So, the intention of this matter is to optimize the experience of the product itself, rather than intending for the sake of intention.

Moreover, DeFi will also be the first stage for Intent to flourish. More than 20 DeFi protocols have already cooperated with DappOS. In addition, Brink Trade has developed an Intent Engine, which can include operations such as Bridge, Swap, and Transfer in a single signature within an intent. Furthermore, well-established protocols such as CowSwap, 1inch, Uniswap, and LlamaSwap are continuously expanding their functions to meet the users’ diverse intentions.

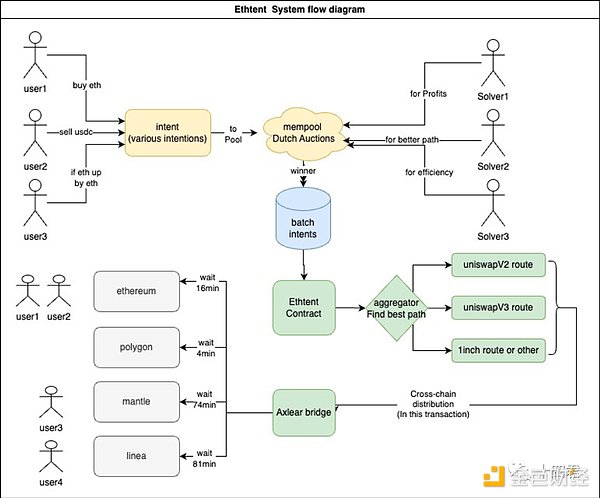

In the hackathon competition at Token2049, I participated in the DeFi track and solved an Intent solver (Ethtent system) for a cross-chain Swap + strategy-assisted investment scene, as shown in the figure below.

It’s also worth mentioning that, in fact, it is not difficult to implement a vertical intent with fixed requirements on the existing infrastructure of EVM. The real challenge lies in the future emergence of a market for intent solvers or a collaborative framework called a collaboration standard. This framework should enable different solvers to further combine and reuse in order to achieve standardized solutions for intents, and also allocate economic models to satisfy the intentions of both parties.

Standardization often requires top-down standard definitions. Currently, it seems that DappOS and Anomo are at the forefront of this path, which is worth looking forward to.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Token2049 Chronicles Rising in the East, Falling in the West, Industry Gossip and Business Insights of Conference Organizing

- My latest experience of being scammed once the identity information is submitted, data leakage is only a matter of time.

- Battle for AI Talent Frenzy at the Beginning of the Year, Confusion at the End

- A different approach, friend.tech may be the community artifact for NFT artists.

- Official publication of ‘The Musk Biography’ How does the book describe Dogecoin?

- Can Binance Launchpad, which has dominated the market for over 4 years, continue to shine?

- One year after the Ethereum merge, what changes have occurred in the MEV supply chain?