Value capture and quantification: on encrypted capital and encrypted goods

Translator's words

"Value" is a topic that has been discussed in the encrypted world for a long time, repeated, and discussed.

Is there value, what is the value? How to capture value?

What is Value Capture? What kind of encryption project can have Value Capture capability?

The volatility of value judgment is like the volatility of encrypted assets, rising and falling.

- The first Chinese-American presidential candidate in 50 years, still a cryptocurrency enthusiast

- Getting started with blockchain | The phone or computer with the wallet installed is broken, is the currency gone?

- Proficient in IPFS: one of the system startups

Think about it, people who have been in the field of encryption for a long time, whether it is bitcoin maximism or more POS, are sure of somewhere in the value of encryption.

However, the "value" mentioned by everyone seems to be largely unconstrained or the consensus fluctuates greatly.

Controversial places focus on the following:

- Time measure of value: In the long run, the more unified the recognition of the value of encryption, but the confidence is not firm in the short term, and it is greatly affected by various environments. Confidence is often nothingness.

- The process of value formation: Why can the forked bitcoin retain its value due to the "divisibility" of the encrypted network? Under what circumstances will the value be lost due to the fork?

- Comparison of the value of different projects: Which consensus mechanism, governance method, Layer1 or Layer2 is more valuable. Some people believe in the value of Staking, some believe in the value of digital gold storage, and some people think that the exchange medium is optimal.

In the early days of a new thing, this phenomenon is normal and reasonable. It is precisely in the cycle of “question-discussion-practice-discussion-questioning” that the recognition of certain viewpoints will eventually produce a network effect, and the scope of consensus will be continuously expanded, and the value identity will move from the edge to the mainstream.

I don't think that the discussion of value belongs to the temple, only economists and developers can grasp it. The discussion of value and the use of foot voting are more generated in the various characteristics of cryptocurrencies, such as anti-censorship, non-tampering, no access, decentralization, global reachability, etc., people are attracted by these characteristics. , thus entering the world of cryptocurrency. Demand creates value, and the evolution of humans from the physical world to the digital world necessarily creates the need for encryption.

The future of cryptography economics may be the observation and refinement of this phenomenon of human beings, and its rationality comes largely from historical self-certification. Compared to what we predict to happen in the future, it is more important to think carefully about what has happened now. Some things may have happened, but we didn't realize it. We don't know if we don't know it is the most terrible.

Going back to the value question, I think what has happened is that the identification of certain cryptographic values can give a somewhat less accurate and rigorous answer to some extent. Theory must lag behind practice.

For example, imagine that bitcoin was created in a parallel world, but it was destroyed for some reason. Since Bitcoin has been created as a technology, there will be someone who will improve and create it. It may not be called Bitcoin, but there must be a similar function of cryptocurrency to undertake this function, with the strongest computing power and the longest chain. In fact, to some extent, all human memory and history guarantee its value.

The author of this article, Chris Burniske, is a partner at the Placeholder Foundation and author of the book cryptoassets. From a very early stage, Chris Burniske has long-term observation and in-depth study of the valuation theory of cryptocurrency. Valuation is a quantitative form of value understanding. Although its accuracy cannot be assessed, the classification framework provided in this article is very useful for us to meaningfully explore and think under certain dimensions of common assumptions and term definitions.

There are several points in my translation of this article:

- Value capture comes from receiving value from resources with a continuous stream of value.

Some people say that holding Bitcoin also has a network effect and can capture value, but Bitcoin relies on "there is someone else who wants to own Bitcoin" in the market. The value capture mentioned here is closer to having equity and is actively involved. Staking is part of participation, governance is participatory, and Keeper on MakerDao is also involved. Participation in the construction and operation of encrypted networks through internal mechanisms can be seen as value capture.

So is the bitcoin miner's value captured? I think it's just that most people are not qualified for this job. The POS consensus allows ordinary people to participate.

- BTC is a value store, from encrypted goods to value storage, which is a squid hopping gate for most POWs, and only a handful of lucky ones can be done. Although the author did not explain why POW is inherently a cryptographic commodity – another one that is not explicitly stated is that POS may be an encrypted capital CA – but I still agree that BTC is SoV. Some people say that value storage is a pseudo-proposition, and the value storage is extremely unstable. I think BTC and gold are very similar.

- Many cryptocurrencies have mixed values (according to the author's classification). From another perspective, it can be argued that the asset classes and research of existing economics are mostly generated and developed in the physical world and do not adapt well to the digital world. We use these inconvenient rulers to measure cryptographic assets, perhaps because of the confusion of value.

- The author re-evaluated the cryptographic assets based on the classification. My understanding of the valuation is very simple and I did not focus on it.

In order to facilitate understanding, this article is still translated in the first person when it is translated. If you want to understand the author's intentions more accurately, please refer to the reference link at the end of the article, which lists two other articles by the author of this article. At the same time, it is highly recommended that the encrypted asset valuation series translated by the NPC source plan, a total of five articles (see [Reference Link 5]), can be used as a cross-reference to the same topic.

This is a very hardcore article. It doesn't matter if you read it for the first time. It is recommended to keep it in your collection. Since the translator does not have enough economics, there may be many mistakes in the translation, hoping to see a better translation.

The following is the original translation

This article can be seen as a re-exploration of the definition and valuation of cryptographic assets since I wrote the White Paper on New Assets in 2016.

This article describes the two main sets of cryptographic assets we see today: encrypted capital and encrypted goods. We discussed the differences in value capture and valuation models between these two types of cryptographic assets. We expanded and revised the crypto-asset valuation theory that I proposed in 2017. One of the most important mistakes is that I put the model of MV=PQ. Used in all cryptographic assets, and now I think this equation applies only to non-production cryptographic assets (ie cryptographic goods) and not to production-type cryptographic assets.

This distinction is not very rigorous at the technical level, mainly to provide two main directions for future asset valuation work. Although it was eventually compiled into text, I came up with discussions with Placeholder Fund colleagues Joel, Brad, Alex, Mario and the broader encryption community.

The main crypto assets we are currently seeing are naturally close to capital assets, but many early examples, such as Bitcoin, are closer to cryptographic goods, and some of their subsets are commodity currencies. In the emerging field of cryptographic assets, some assets are similar to equity, some assets are similar to debt, and many assets have singular functions and different combinations of value streams, so they cannot be identified by previously defined cryptographic asset types. Joel has written an article on the governance of encrypted networks as capital to explain why governance assets have value.

TLDR version:

- Encrypted assets can be divided into capital assets CA, consumable/convertible assets C/T, and value storage assets SoV.

- The value of productive capital in encrypted capital is calculated by discounting the net cash flow of the supplier.

- Non-productive capital (encrypted goods) whose value is priced by MV=PQ. Among them, PQ = annual trading volume. Note that “annual value to the supplier” and “traffic volume” are two separate indicators that serve as key indicators of encrypted capital and encrypted commodities, respectively.

- Integrating a consensus model to evaluate cryptographic assets is the basis for improving efficiency and stabilizing the volatility of the crypto market.

Super class of assets

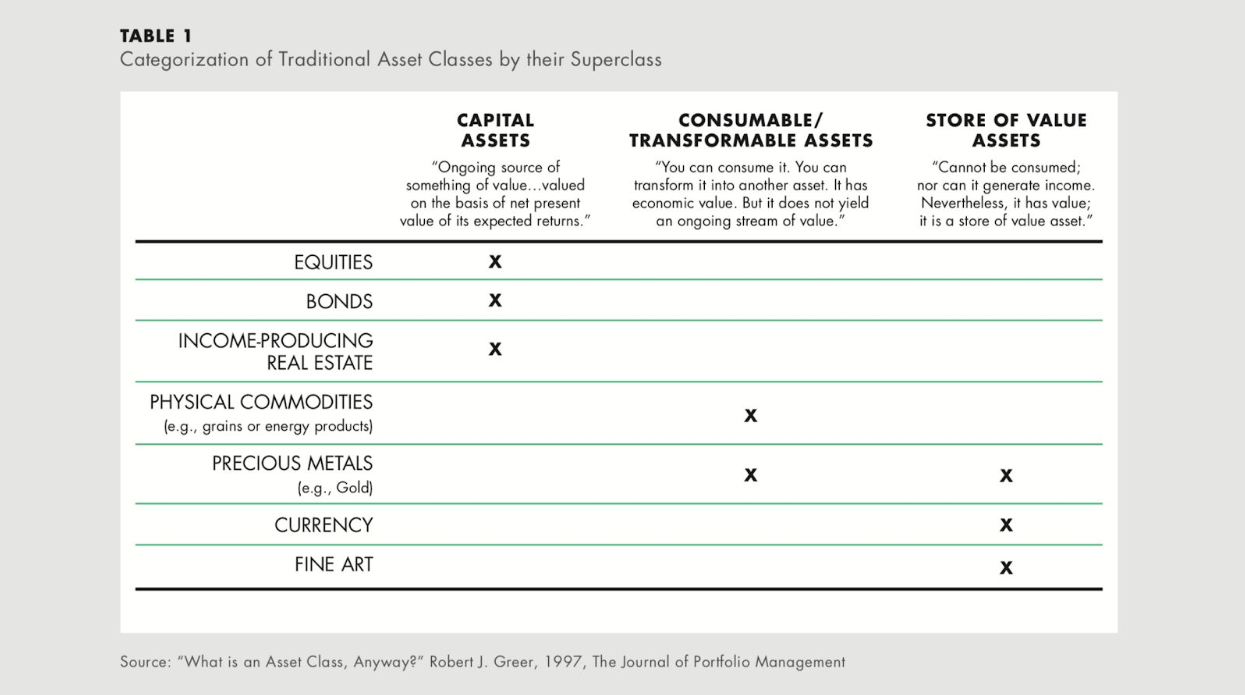

The definition of asset superclass comes from the article by Robert Greer in 1997, "What exactly is an asset class? 》.

Capital Assets (CA): is a “continuously valuable resource…valued according to the net present value of its expected return,” such as stocks, bonds, and leased properties.

Consumable/Transformable Assets (C/T): You can consume this asset or convert it to another asset. It has economic value, but it does not produce a continuous stream of value. Oil, wheat, and natural gas all fall into this category. Some precious metals and scarce goods also belong to C/T but at the same time have socially acceptable storage values (overlapped with the third superclass).

Storage Value Assets (SoV): Cannot be consumed or generate revenue, but it has value and is a storage asset of value. Such as art, collectibles, and French currency are pure SoV assets, while the SoV superclass also partially overlaps scarce consumable/convertible assets.

The same asset can span multiple superclasses. Historically, gold has been a typical blend of C/T and SoV assets. However, we see a combination of capital assets and consumable/transferable assets (CA+C/T) showing explosive growth in the area of cryptographic assets. This is a new phenomenon.

However, this does not mean that the "CA+C/T" cryptographic assets should follow existing securities regulations, as most of these assets require proactive participation to obtain value streams. And as the SEC recently pointed out, digital assets are often analyzed in the Howey test. The main problem is whether its buyers have expectations for reasonable profits (or other financial returns) based on other people's efforts. The so-called "other people's efforts" in the field of encryption, compared with traditional companies, the boundaries are more blurred.

Even if the encrypted capital of “CA+CT” is considered to be securities and thus regulated by the SEC, the “CA+CT” assets still include the supply side and capital in the value stream, as opposed to the investors in the stock passively waiting to obtain profits from the system. The value-added part of the service. Although subtle and vague, this inclusive transformation is an important part of confronting pure capital configurers. I say this as a capital configurator to see how unbalanced the current competition is.

Careful readers may ask, why not use equity to capitalize the network? The main reasons why crypto assets are better than equity are as follows:

- Software-based governance enables finer regulation and faster development than paper-based stocks.

- Capital allocators are more difficult to passively expand the value stream, and it is difficult to capture too high a value stream at the beginning because of capitalizing the system. Laborers can add leverage through capital. In short, this is a very unfair competitive environment between capital and labor. Although we have to focus on the expansion of passive value – how service providers serve large capital allocators. (Translator's Note: This is not very clear, personal understanding is contrary to the stock market, in the encryption capital market, laborers have a certain advantage in the early stage, but in the POS consensus network, Staking is more important for how to passively capture value .)

- The real risk-taking people gain benefits, which is the best economic behavior advocated by Taleb in Skin in game thinking.

- Given that each protocol has the potential to operate globally, such as the TCP/IP protocol, the potential geographic expansion of these networks is much faster than the size of the company's deployed services.

2. Capital Assets (CA)

Capital assets are production assets, and holding these assets can get "valuable things." You should be immediately aware of the difference between it and Bitcoin, and the holders of Bitcoin are not getting future benefits. We traditionally believe that “valuable things” are cash flows, but in fact should be an open explanation for this area.

Any encrypted network that needs to acquire the value stream generated by the network itself by having native encryption assets, they produce capital assets rather than commodities.

Corresponding to the field of encryption, any asset that can be pledged, borrowed, or anything else that can promise to acquire a value stream can be considered encrypted capital. Sustainable value streams come from transaction costs and asset inflation, and sometimes the latter is not required. If we believe that these assets can effectively and sustainably coordinate resources and coordinate existing societies and contracts (such as stocks), we must make the assumption that, assuming that the network provides valuable services, it will generate stable transaction costs. .

We usually use the NPV model to calculate this kind of future value by the amount of online traffic to the supplier. Some people use the Dividend Discount Model (DDM) to understand that the difference is that instead of discounting the company's future dividends, you will get the net present value of all value streams attributable to the supplier over time. Others prefer to use the Cash Flow Discount Model (DCF), but I prefer to use the term value stream discount (DVF).

Until the spring of 2019, most of the crypto assets currently on the market belong to capital assets. If the asset is completely encrypted capital and there are no consumable/convertible applications, then the “liquidity problem” will not be a problem at all. The valuation model at this time does not need to consider liquidity.

On the other hand, if the asset itself has utility beyond the supply-side coordinator, then its non-pledge, non-generating assets, can be divided into consumable/convertible categories. At this time, we must consider whether we should introduce liquidity considerations. The CA+C/T valuation model is a mixed equation where the part of CA is the DVF model and the C/T part is MV=PQ. In this case, I think the asset value comes mainly from DVF, not M=PQ/V, which makes the liquidity problem from the C/T part no longer important.

In the "CA+C/T" portfolio, I think CA captures most of the value, but C/T should not be ignored, because they have unlimited programmability, we will see C/T offer A variety of utilities, some of which are more obvious examples such as discounts, accessibility and reputation.

3. Consumable/convertible assets (C/T)

In the asset classification framework mentioned above, the C/T type is “you can consume it, you can also convert it, and it has economic value but does not produce a continuous stream of value”. Therefore, there is no value stream shifting from primary assets to governance, and the capital attributes of these assets disappear. Instead, they are more like commodities.

In my opinion, pure workload proves that POW assets can be considered as encrypted goods. And MV=PQ is still the best model for pricing these assets.

POW assets are the most important C/T assets I can think of in the field of encryption. They create digital native goods in a way that is safe and accessible to the book. One of the mistakes I made in the early days was in the INET model of cryptographic asset valuation, assuming that because the network deployed goods as a service, the original asset that started the service was the commodity. As described in the previous section, examples in most markets indicate that they are actually capital assets.

To reiterate, the key to distinguishing between the two is whether the internal assets of the system must be pledged to participate, and if necessary, the assets are necessary to accept the value stream, and thus become capital assets. If internal assets are not one of the inputs to production, then it should be more like what we call encrypted goods.

So far, the best way to value crypto products comes from Rustam Botashev of HashCIB. This is based on the methodology of Brett Winton and my research work at ARK Invest.

(Translator's Note: The following part is an excerpt from the valuation calculation part of Rustam Botashev. Since it cannot be accurately translated, please refer to the original link)

The MV=PQ formula is the basis of the above model and has been controversial in the encryption industry and even in the wider economy. Some people complain that it is only symbolic, while others complain about the accuracy of the model input data. For physical goods, the data required by the model is more opaque and more dispersed than the encrypted product, so the practical value of this formula is even smaller. With the data sharing, open and free access of encrypted networks, we hope to better measure the role of the MV=PQ model in the field of encryption. This means that we can use more perfect data sources and more reasonable assumptions in the model, but if we don't fully understand how humans have historically interpreted the value (or lack of value) of highly used goods, the key driving force behind them And change, we will still get lost in the formula.

Although the entire industry is trying to speculate on pure consumable/convertible cryptographic assets (the commodity is highly volatile!), the superposition of SoV super-class goods can be considered a good indicator of diversified wealth in the long run. . If commodities can function well over time, society will be highly dependent on the annual supply inflation rate of commodities and the predictability of inflation in its supply over the next few years. Saifedean Ammous expresses this very well in his new book Bitcoin Standard.

Although people will care about the current supply inflation rate, the ability to change the supply inflation rate (or lack of capacity) in the future does not seem to matter. This ability can be considered as the hardness of the commodity. The more difficult it is to produce a new supply that dilutes the stock of existing commodities, the higher the hardness of the commodity is considered, and the more likely it is to be a SoV asset that transcends the time dimension. Because people can believe that the share of the scarcity rights they hold will not be significantly diluted.

“Soft goods” such as oil, whose supply can generate new supplies of the same order of magnitude as existing stocks each year. And "medium goods" like silver can add 20% of the supply. Then the annual increase in the production of “hard currency” like gold is about 1-2% of the stock. If Bitcoin sticks to its monetary policy, then its reaching the 21 million capacity ceiling will converge to an annual inflation rate of 0%, which can be called perfect hardness. Obviously, this perfection exists only with the digital world.

Anyone who creates and invests in a consumer product that is consumable/convertible should be aware that encrypted goods do not have any cryptographic capital characteristics. A very small amount of encrypted goods can be a reliable SoV asset, which is no exception in the encryption market. For those encrypted goods that do not reach the SoV asset premium, their value capture prospects are worrisome.

This is already very certain, and this is one of the reasons why the term “Utility Tokens” has become contemptuous. In my opinion, the term "functional token" is too vague to be used. If this functional token is a consumable/convertible asset, but does not become a reliable path for SoV, it will suffer from violent value fluctuations, making it difficult to capture value. Conversely, if it has a pledge-based supply-side adjustment capability and is of the type of encrypted capital, then if the network can provide on-demand services, the value capture of the network is promising.

One final point: goods are often considered the bottom line of marginal cost. In the bear markets of 2014/2015 and 2018/2019, we have seen the claim that Bitcoin miners are close to their marginal cost around $200 (2014) and 3,000 (2018). About $200 is the bottom of the bitcoin price in 2015, and $3,000 may be the bottom of the current 2018/2019 bear market. If the miner refuses to sell bitcoin at a price lower than the cost of production, this may be enough to make the market buy one-way. However, because of the difficulty adjustment, in theory, Bitcoin also faces the death spiral of production costs. This makes some theoretical factors hopeful in practice.

We must note that there are several points in the encryption of goods that are different from physical goods:

- In the digital world, there is no natural loss and destruction of goods that exist in the physical world (except for the loss of private keys). This allows encrypted goods to accumulate over time, but also requires mandatory destruction or manufacturing scarcity to carefully control the supply of assets.

- The marginal cost of most physical goods declines as the size of the system increases; as more capital is invested in the production process, economies of scale result in more unit goods being produced. Bitcoin and other POW projects, on the other hand, have more marginal costs as more people mine. The reason is that when more resources are used for mining, the newly produced BTC has a fixed supply productivity that is fixed. Moreover, when Bitcoin increases by 210,000 blocks, its mining output is halved. If the network size remains the same, then the marginal cost of each bitcoin doubles. This phenomenon can be used to explain why the bull market in the encryption market is ushered in after each production cut (2013, 2017).

4. Value Storage Assets (SoV)

Pure value storage assets (SoV), whose value is notoriously capricious, because they are based on human whimsy, and there is no underlying model to confirm the rationality of their changes. For this reason, it is difficult to clearly point out what its valuation model is. This feature also makes the SoV part of C/T+SoV difficult to evaluate. For Bitcoin's SoV potential, we generally think Bitcoin may have a share of the gold market. But even the total market value of gold is a change target. Moreover, these assets are also very good reflexive tools, showing the inflationary effects of the supply of fiat money, and their value storage capacity will also increase with the continued inflation of the national currency supply.

5 Conclusion

The most criticism of the above valuation conclusions is that these theories are too complicated. This is true, but for comparison, I don't think it's more complicated than evaluating RedHat or Salesforce's valuation.

The existing model for evaluating listed companies has cost analysts for decades, and modern stock valuations began after Graham and Dodd published Securities Analysis, which appeared as an asset class . The time is over 300 years late .

The cryptocurrency is younger, Bitcoin is only 10 years old, and we are still in the process of developing valuation and pricing models, and we definitely hope that the process of similar standard valuation models will happen on cryptographic assets. We can reach a consensus on the mathematical model and only dispute the input of the model parameters. Based on current developments, it is believed that progress in this area will be an order of magnitude faster than the securities market.

I hope that when clarifying the difference in value capture, you should stop thinking that all crypto assets are zero-sum games. Less quarrels, more construction and better analysis. We will see the huge heterogeneity of the three crypto asset superclasses, which are land that produces programmable value. After all, it is about to gain share from the entire world as a whole, and it will expand and even redefine the world.

(Finish)

Translation: realthinkbit@orange book volunteer

Reference link

1. "Value Capture and Quantization: Encrypted Capital and Encrypted Commodities" (original paper)

Https://www.placeholder.vc/blog/2019/4/26/value-capture-and-quantification-cryptocapital-vs-cryptocommodities

Author: Chris Burniske

2. "New Asset Class"

Https://research.ark-invest.com/bitcoin-asset-class

Author: Chris Burniske

3. "Encrypted Asset Valuation"

Https://medium.com/@cburniske/cryptoasset-valuations-ac83479ffca7

Author: Chris Burniske

4. "Corporation of Encrypted Networks as Capital"

Https://www.placeholder.vc/blog/2019/2/19/cryptonetwork-governance-as-capital

Author: Joel Monegro

5, NPC translation encryption valuation series five

On the Value of Token as an Exchange Medium

https://mp.weixin.qq.com/s/KhUOHLg7XCNdhrcuYmVIMg

"When we talk about the valuation of crypto assets, what are we talking about? 》

https://mp.weixin.qq.com/s/9Wr9ro6J_N4Oj4DDeBR0_A

"An Entity Investor's View of Encrypted Assets"

https://mp.weixin.qq.com/s/FZD86_2Y8F68VQAtZcvmjQ

"On Value, Circulation Speed and Monetary Theory"

Https://www.jianshu.com/p/e010fc2464f7

"Efficient Market Valuation Framework for Encrypted Assets Based on BS Option Theory"

https://mp.weixin.qq.com/s/9s583cUEAfuMY26wzoWvww

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Opinion: The best use case for Bitcoin is as an anti-corruption tool

- Depth: How to ensure the safety of the Bitcoin network when there is no mine to mine?

- During the year, six listed companies were continuously “named” because of the “blockchain” supervision letter.

- Large factory enclosure, small factory group: blockchain standard gunshots

- Tens of millions of EOS have been unlocked, and the price of the currency has not fallen, but what is it?

- Useful way – the initial solution of BYSTACK application

- Bitwise: There are only 10 Bitcoin exchanges with real trading volume