Viewpoint 丨 Can blockchain restore Japan's lost two decades?

Source: BlockMania

As the first country to announce Bitcoin as a legal payment method, Japan has changed its conservative image in the field of blockchain innovation and digital currency, and actively promoted the introduction of relevant policies and industry support. What is the reason behind this? How did Japan become a fertile ground for blockchain development? BlockMania AMA Live Issue 36 and BlockMania's "Global Perspective" Issue 1, the theme of this issue is "Can Blockchains Help Japan Regain Lost Twenty Years?" The sharing guest is the founder of Chainage, Jason. How to support the development of the blockchain, how active the Japanese financial innovation is, and what natural advantages does Japan have for the development of the blockchain.

The following is a full review of this AMA:

What noteworthy policies has Japan introduced for blockchain?

Japan has always been a mecca for blockchain entrepreneurs. Japan is also a country with a deep affinity with the blockchain. Satoshi Nakamoto, the creator of Bitcoin, has a Japanese name. As far as I know, as early as 2017, the Japan Financial Services Authority FSA issued an exchange license for virtual currencies and took the lead in legalizing Bitcoin payments.

- Crypto funds die in batches, but these ten are still making high-frequency shots

- Views | What impact will the central bank's digital currency have on Alipay and WeChat?

- 2020 spotlight: PlusToken, a $ 2 billion Ponzi scheme, may become a cloud over bitcoin prices

Blockchain, the Japanese government is the first country in the world to supervise the blockchain at the national legislative level, and the FSA of Japan directly issues licenses to exchanges, etc., facing the new economic and new challenges with a super positive attitude. Restore the lost "Heisei era".

https://www.chainage.jp/fsa

From this address, you can see many policies and administrative actions of the Japan Financial Services Agency. The Japan Financial Services Agency is equivalent to the combined management agency of China's Securities Regulatory Commission, Banking Regulatory Commission and Insurance Regulatory Commission. Such frequent administrative intervention (note: not forbidden) can only indicate that the blockchain and digital asset industries are expected to develop in a more healthy direction. For Japanese websites, you can use Google Translate to see the content. Basically, the translations are similar. Recently, the hottest STO is about to land in Japan.

Reference link: https://www.sbigroup.co.jp/news/2019/1001_11681.html

One of Japan's most aggressive and largest financial groups on the blockchain, SBI, just announced the establishment of the STO Association on October 1. Participants in the association include most of the Japanese securities companies.

Why are Japanese regulators relatively friendly to blockchains? Is this regulatory friendliness good for all industries or for innovative technology industries?

First of all, the Japanese government has stricter and clearer policy guidance on blockchain finance, and secondly, companies are leading the world in the innovation of blockchain finance.

Many well-known large companies have developed in Japan. For example, Binance, the world's largest exchange, has grown and developed in Japan. Later Huobi was also exploring Japan in depth and spent 5 billion to buy a license in one go.

Major domestic financial institutions and Internet companies are also actively involved in the blockchain industry, and the industry's development momentum is in the ascendant. From this point of view, the official attitude of Japan to the blockchain is very friendly, and Japanese companies and communities generally have a high degree of acceptance of the blockchain, which has created a good external environment for us.

This kind of regulatory friendliness still cannot be interpreted as being friendly to innovative technology. The traditional entrepreneurial environment in Japan is still very rampant. Blockchain, fintech, is the key word for Japan.

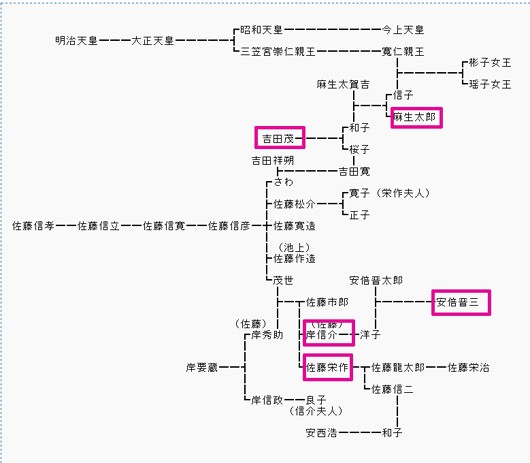

Let's take a look at this picture, the relationship between Shinzo Abe and the relationship between Taro Aso and the royal family. Currently, Taro Aso is Minister of Finance and Deputy Prime Minister of Japan. It is the confidant of Abe Shinzo's confidant, good relatives and brothers, naturally in the lifeline department. Therefore, the policy of the Financial Services Agency is directly supported and supported by the Japanese government. In other words, the Japan Financial Agency, which is directly managed by the Japanese government, strongly supports the development of blockchain, especially in financial innovation. It is a friendly signal.

You just mentioned that blockchain as a fintech is strongly supported in Japan. Is Japan's current financial innovation active?

2. Ordinary banks are generally divided into urban banks, local banks, and trust banks. For example, Mitsubishi Bank that you usually see, Mitsui Sumitomo Bank falls into this category.

3. Small and medium-sized financial institutions. Here are some credit vaults and credit combinations, similar to the state of Chinese cooperatives. They are a historical product, but they still exist.

4. Agricultural, forestry and fishery financial institutions, similar to the above 3, are a special existence, agricultural synergy and fishery synergy. A proper analogy is that 3 is the land and urban version, and 4 is the agricultural and fishery version of the cooperative.

5. There are many securities and financial institutions, the most famous of which are Nomura Securities, etc. There are more than 200 first-class securities companies in Japan, more than 2,000 second-class securities companies, and other securities companies. These securities companies are also the most active outside of the aforementioned banks.

6. Insurance companies also belong to financial institutions, such as Mitsui Marine Insurance and Sumitomo Life Insurance.

7. NoBank, this category belongs to P2P companies similar to China, as well as credit card companies, money lenders, financial leasing companies, and other non-bank non-securities and non-insurance financial companies are included here, including the now popular Tripartite payments also belong here.

8. Government financial institutions, Japan Policy Finance Treasury, Japan Policy Investment Bank, etc., similar to China's National Development Bank and Belt and Road Bank, banks that implement national policy financial functions.

Among the above-mentioned major financial institutions, they are extremely eager for financial innovation. There have been two major shocks from China and the world. One is the QR code scanning of Alipay, which has become popular in Japan. Yes, but QR payment is the most NB in China), the other is the blockchain. All major financial institutions hope to carry out financial innovation through foreign technologies and solutions to solve the problem of industrial aging. Hope to overtake the curve.

Here are two of the most representative examples. One is PayPay, which appeared as the ace QR payment of Sun Zhengyi Softbank Group, which basically swept the Japanese QR payment market. The other is the BitFlyer digital asset exchange, which directly opens the yen to digital asset transactions. Unlike some places that require one conversion with OTC and various stable currencies, it directly trades yen to BTC.

In addition to these two heads, other large, medium and small companies are actively carrying out various financial innovations. With the outbreak of 5G in Japan in 2020, many good projects will emerge in the visible range.

Refer to the companies in the STO Association established by the SBI just mentioned. It can be seen that major Japanese companies are actively willing to embrace blockchain financial innovation.

Many active or retired officials will mention blockchain in the conference speech, giving the impression that "Japanese officials know and welcome blockchain." What do you think of this phenomenon?

Although not like China, Japan does not have the above book, but Japanese officials are basically studying hard, trying to learn the blockchain overnight, and giving some chestnuts, members of the Japanese parliament have become at least three virtual currencies Alliance, pull each other, join. A new type of currency is being used by members of the House of Representatives, Naoya Takemoto, members of the House of Representatives, and members of the House of Representatives Kiyoshi Kihara, and members of the House of Representatives Hiroyuki Hirai. These three were established in 2018, and the follow-up continues. Retired government officials in active service often talk about blockchain related matters on official and unofficial occasions, which is already the norm. Please refer to a video of Libra in the US Congress about Libra. I remember the original words probably want to express this meaning: if we do n’t do it, China will do it, and we wo n’t be able to catch up later, this sentence Words also apply to Japan.

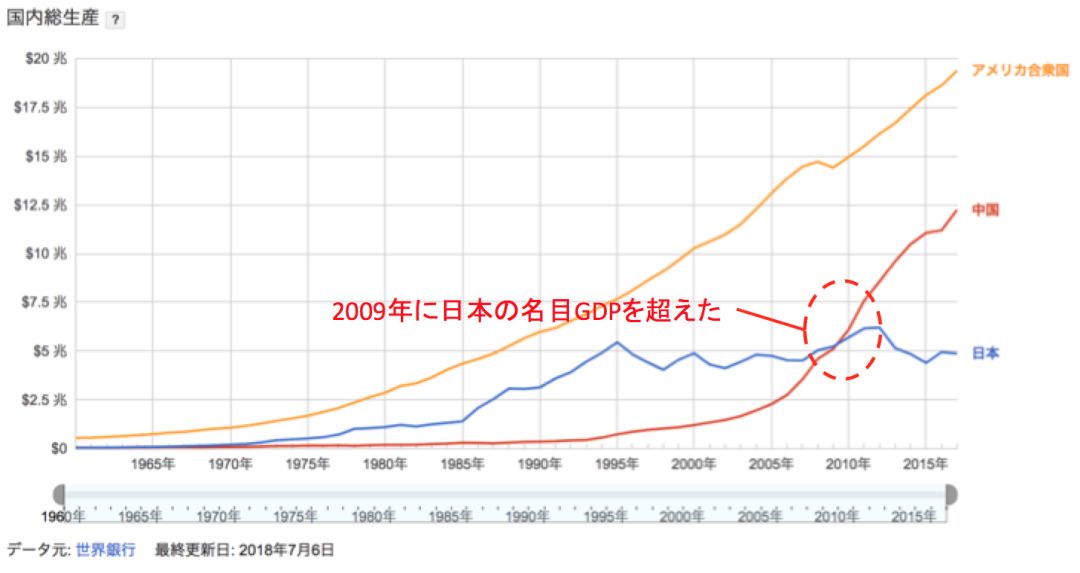

Insert a picture here to describe this background situation. The yellow lines are the United States, blue Japan, and red China. We know that China's GDP exceeds that of Japan. This is an indisputable fact. But what happened within five years, not only exceeded, it was doubled! What does it feel like? Yesterday, the two children were more than one meter high, and everyone was on par. Today they met, good guy, two meters! Don't look up, you can't see it! This is Japan's condensed feeling of China's development. Some Japanese who are unwilling to look up simply can't see China's development, and some can see China's development, so hurry up, while China is still banning virtual currency, hurry up, catch up, legislative protection, Endorsement of policies, do your best!

This is how I look at this phenomenon. (Purely personal)

What is the current attitude of Japanese regulators and the public towards digital currency transactions?

Let's take a look at this PDF file. This is an electronic manual issued by the Japanese Finance Agency to the general public. From the overall word, you can see that the Japanese Government Finance Agency released to the public: speculation, no problem, please look for legal institutions! Make money, no problem, legal tax payment prohibits money laundering!

The openness and friendliness of digital currencies are from top to bottom and are consistent across the country. As a developed country, the Japanese people have a relatively large investment capacity and demand.

There are two huge potential purchasing powers in this world. The first is that there are "Chinese aunts" who can directly control the trend of the gold market. The second is that the investment commonly known as "Mrs. Watanabe" in Japan can control the foreign exchange market.

After Japanese women get married and have children, most of them do not work at home. "Mrs. Watanabe" refers to these 50-70-year-olds. Her husband has a successful career, the child has grown up, the money saved, the investment is rampant, what good projects How about it? real estate? When the bubble economy collapsed last time, you could lose money, stocks? The pants that fell during the financial crisis are gone. This huge force is slowly entering the digital asset industry.

Watanabe's investment is not a blind act, they will learn to manage it (not to say that Japanese uncles and young people do not speculate in coins), but that Watanabe's wives have more "household financial rights". The power of domestic affairs accounts for a large proportion of the country's GDP, so this force cannot be underestimated. And normal Japanese men are also investing in digital assets.

As for young people, it has been developed that some companies directly pay BTC for their wages (you can choose whether you want BTC or JPY) and there are not a few. If you don't buy coins, you won't be fashionable anymore. You will buy more or less.

Unlike the crazy gambling nature of South Korea, Japan is a benign development under government supervision and government promotion.

What do you think of the socio-economic and cultural soil for the development of blockchain in Japan?

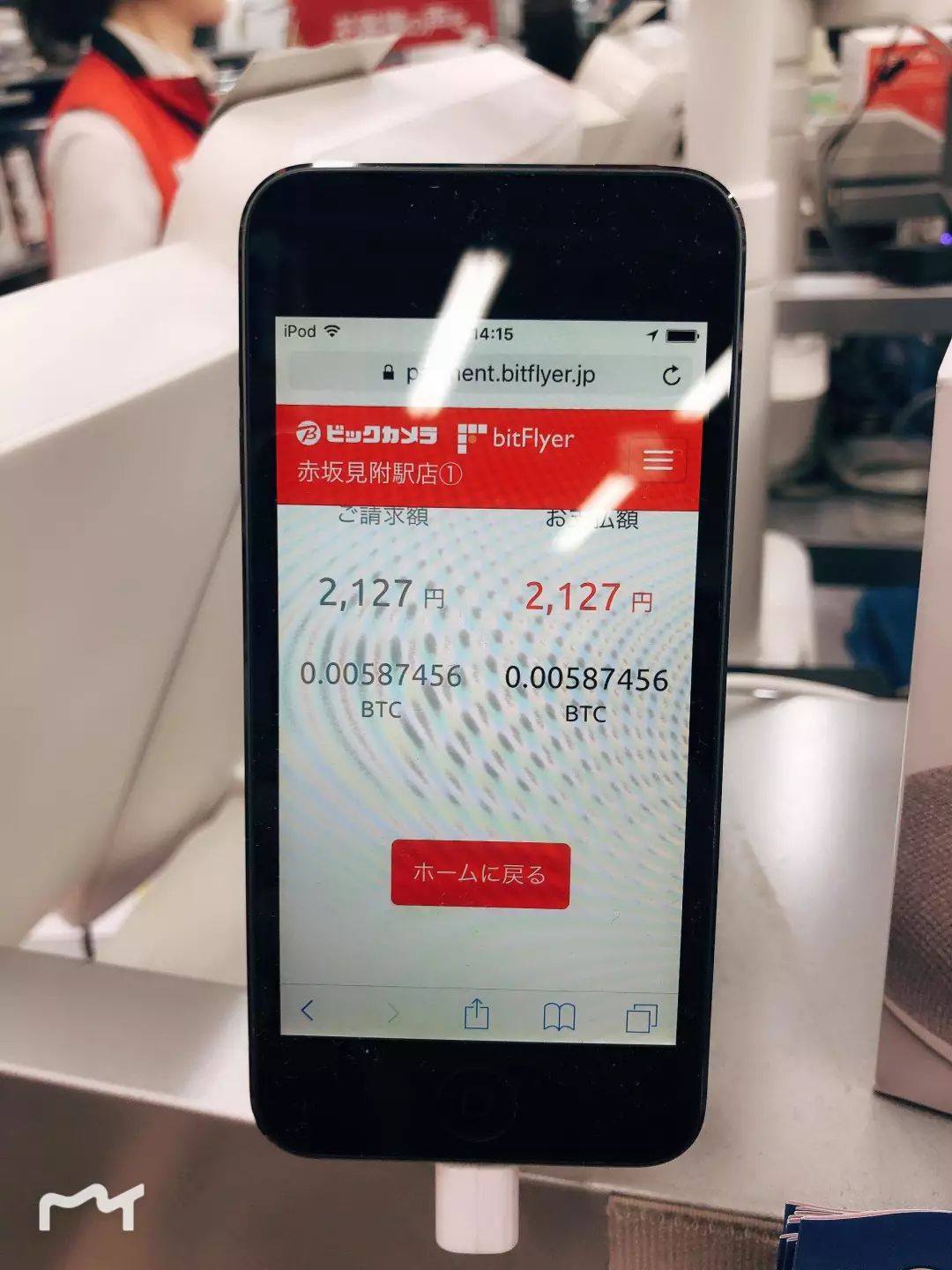

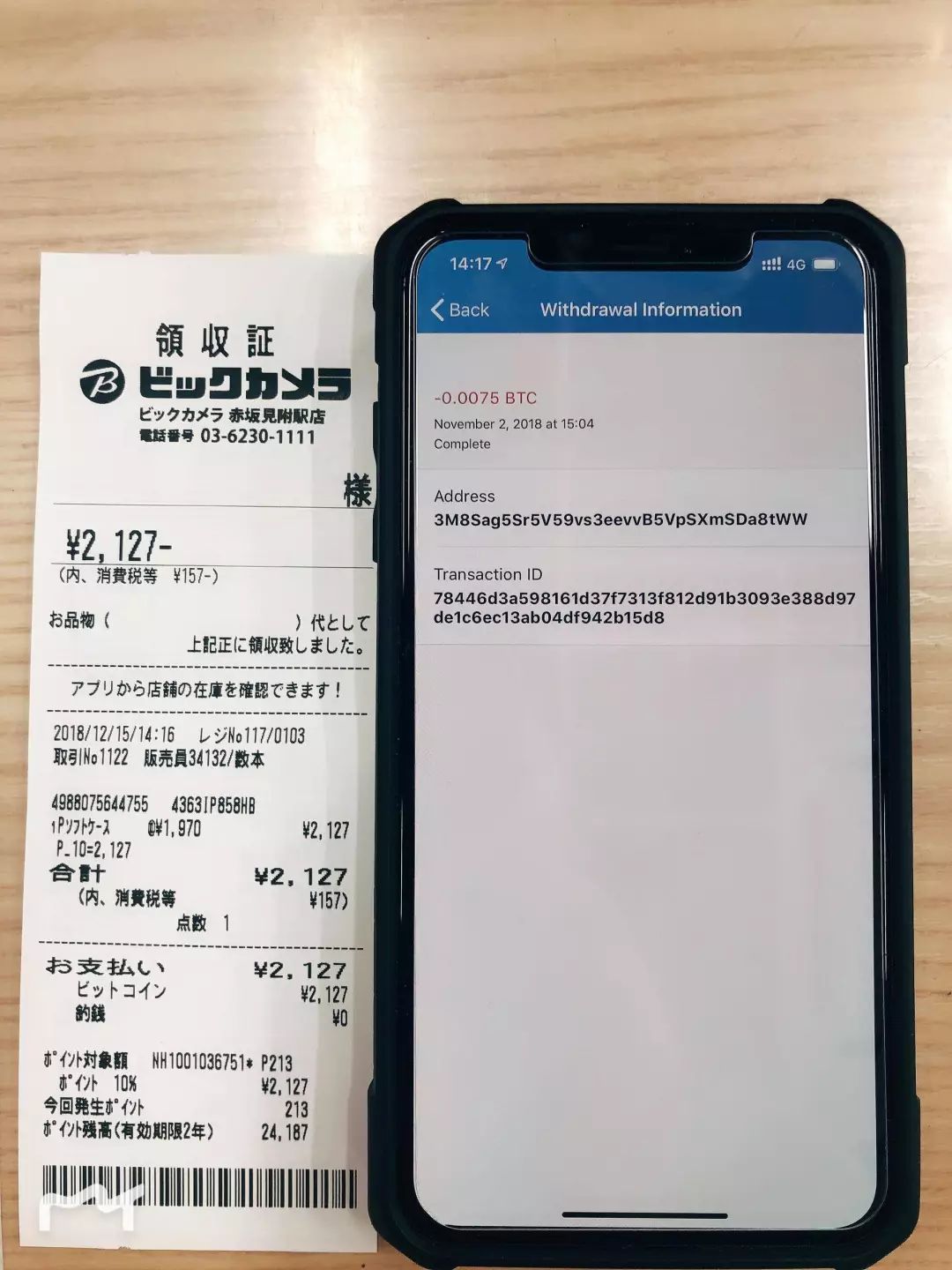

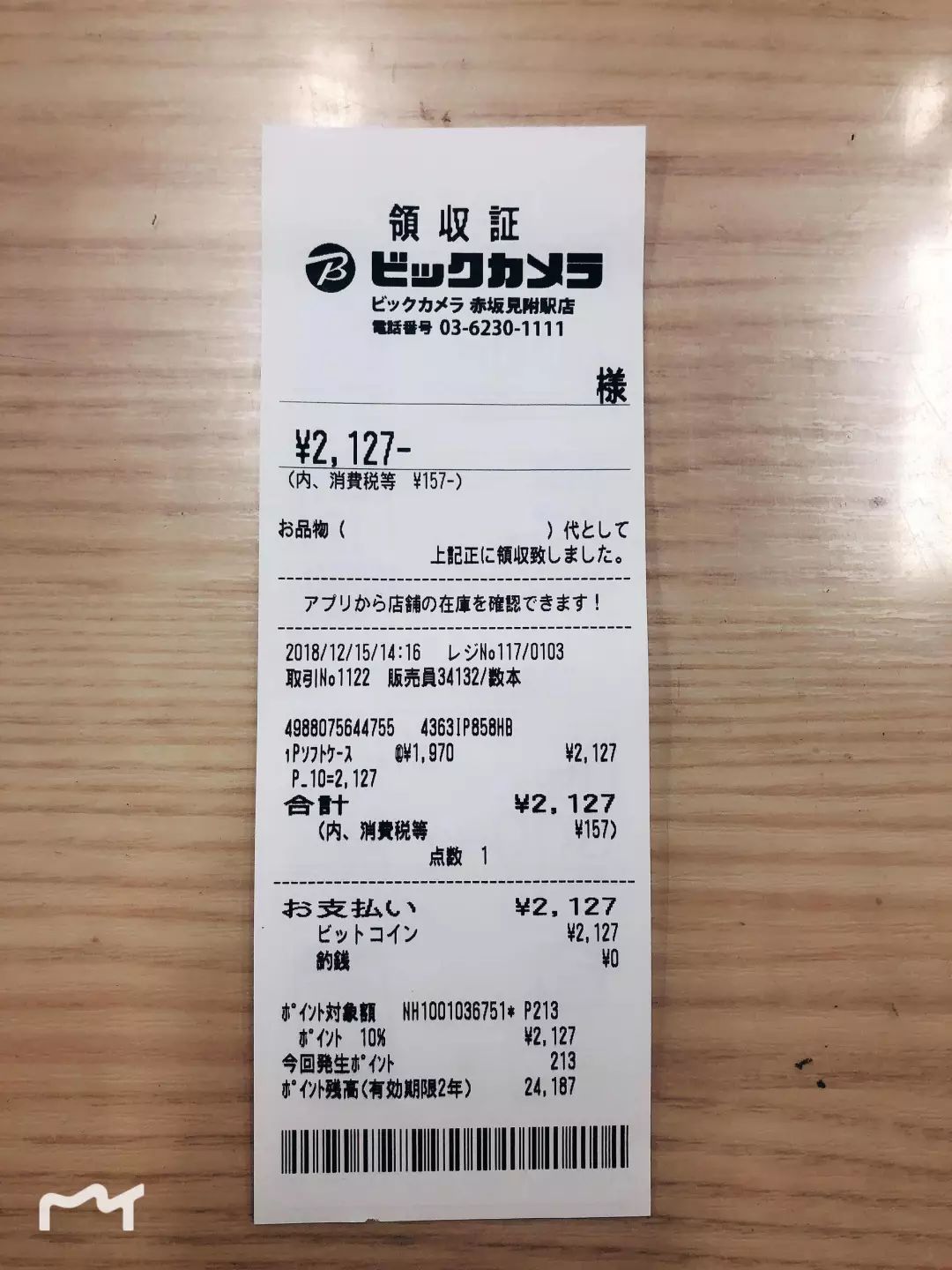

Please take a look at this set of pictures. This set of pictures is a full process photo of an iPhone case that I bought using an offline store using BTC. This group of pictures was taken a year ago, exactly a year ago, on December 15, 2018, what kind of state does BTC make up in Japan? . In addition, in order to meet the 2020 Tokyo Olympics, Japan plans to increase its cashless settlement ratio to 40% within 10 years, and Japan has legalized Bitcoin payments last year, so this has created a peculiar phenomenon. Cognitively, cash-> aggregate payment-> digital currency payment should be developed gradually, but after Japan has passed the first step, they are parallel in the second and third steps: cash-> QRpay + BTC.

However, we can see that a world that does not require bank deposits is coming. In this way, the traditional charging model of banks will be difficult to sustain, and the pressure to use blockchain to cut costs will conflict with the interests of vested interests. In the field of fiat currency, the vested interests are very powerful, and digital currencies will threaten their survival, so how to survive the intermediary agencies is the main problem they are facing now.

Finally share a picture, the Internet is an information revolution, and Blockchain is a value revolution!

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Dry Goods | Revalidation Proof vs. Error Proof

- Talk to Microsoft China's chief innovation technology consultant: Can the development of blockchain applications be simplified?

- Japanese retail giant Rakuten announces allowing users to use points for bitcoin, etc., boosting cryptocurrency adoption

- The world after the Bitcoin inflection point

- Du Xiaoman Releases DeFi White Paper

- Research: 10% Bitcoin allocation in portfolio, which outperforms traditional asset portfolios

- Regulatory review: new US crypto bill, proposal to unify Muslim cryptocurrencies, European Central Bank's European chain