Views | What impact will the central bank's digital currency have on Alipay and WeChat?

Author: Dr. senior macroeconomic analyst at GF Securities Zhoujun Zhi

Source: Digital Fiat Research Institute

Editor's Note: The original title was "Contingent Impact of Central Bank Digital Currency on the Financial System"

Report summary

- 2020 spotlight: PlusToken, a $ 2 billion Ponzi scheme, may become a cloud over bitcoin prices

- Dry Goods | Revalidation Proof vs. Error Proof

- Talk to Microsoft China's chief innovation technology consultant: Can the development of blockchain applications be simplified?

First, DCEP may have three effects on third-party payment institutions.

1) DCEP may pose a challenge to third-party payment service businesses.

2) There is uncertainty about the impact of DCEP on third-party payment institutions' sales of cargo-based asset management products.

3) Under the DCEP system, it may be difficult for third-party payment institutions to directly obtain payment big data information, so related business such as credit information and risk control derived from the payment big data in the original model may be affected.

Second, DCEP may have two direct effects on commercial banks.

1) DCEP may affect the source of funds on the debt side of banks and increase the cost of liabilities. In order to buffer the impact of DCEP on the liabilities of banks, the central bank may initiate multi-dimensional measures, such as not counting interest on DCEP.

2) DCEP may affect two types of intermediary services: payment clearing and settlement and digital currency custody. According to the current patent information, DCEP not only affects traditional small retail payment settlement, but may also be applied to large payment settlement scenarios. According to patent information, in the binary operation mode of DCEP, bank accounts are tied to digital wallets, and digital wallets are hosted in commercial banks. In the future, commercial banks may consider hosting digital wallets as a new intermediate business.

Third, DCEP may have three effects on central bank regulation.

1) If DCEP interest is calculated, DCEP interest rate can be used as a new type of price tool, and it can even be used to break the zero interest rate lower limit. It is worth emphasizing that we are only studying the logic of DCEP to achieve negative interest rates and how to broaden the monetary policy boundary for the central bank based on the theory. It does not point to the follow-up of negative interest rate policy operations after DCEP promotion.

2) The DCEP "token" bookkeeping method and convenient information recording may reduce the supervision cost of the central bank.

3) DCEP may facilitate the tracking and control of capital flows, which will help the central bank develop more effective structural control policies.

Fourth, DECP may have two effects on the currency derivation mechanism.

1) Or restructure the underlying currency structure and affect the currency multiplier.

2) May improve the efficiency of counter-cycle operation and reduce the characteristics of pro-cycle.

appendix:

1) Third-party reserve structure and deposit requirements

2) Derivation of currency multiplier after DCEP promotion

3) The use of payment contracts under the DCEP system to achieve funding

Foreword

The previous topics in this series have successively discussed the nature of the credit currency system, the central bank's digital currency framework and its specific operating mechanism, focusing on how the central bank's digital currency is compatible with the characteristics of "decentralized" and "centralized" currencies, and how it can be used in traditional currencies. The derivation framework is grafted with digital information technology to achieve effective digital currency placement, trading, and withdrawal. On this basis, this article attempts to further analyze and answer two questions that the market is more concerned about. First, how will DCEP affect the behavior of financial institutions? Second, what changes will DCEP bring to the traditional currency derivation mechanism.

Since DCEP is positioned to replace M0, there is no doubt that DCEP will have a profound impact on the payment field in the first place. At present, China's institutions licensed by the central bank to operate payment services can be divided into two categories. One is financial institutions, mainly commercial banks, and the other is non-financial institutions, which mainly refer to third-party payment institutions. This article explores the impact of DCEP on payment institutions, and analyzes the behavior of these two types of institutions. In addition, changes in the payment field will inevitably affect the central bank's currency regulation paradigm. Therefore, this article explores the impact of DCEP on financial institutions and focuses on three types of institutions-third-party payment institutions, commercial banks, and central banks. The first three parts of this article analyze the impact of DCEP on the business behavior of these three types of organizations.

What changes does DCEP bring to the traditional currency derivation mechanism? The fourth part of this article answers this question and focuses on two main points. One is how DCEP will restructure the underlying currency structure and affect the currency multiplier, and the other is how DCEP reduces the financial procyclical characteristics inherent in the traditional currency derivation mechanism. The main reason for analyzing the above two points is that the currency derivation mechanism has a wide connotation and involves all aspects of the financial system and the central bank's regulatory framework. It is unrealistic to try to clarify the impact of DCEP on the currency derivation mechanism. However, DCEP directly affects the restructuring of the central bank's basic currency structure and affects the proportion of "currency exit from circulation". In addition, DCEP will reduce the endogenous financial procyclical characteristics of the traditional currency derivation mechanism, which is almost inevitable. When the derivation mechanism affects, it is necessary to pay attention to the above two points. What other impacts and extent of DCEP will require further research and discussion in the future.

I. The impact of DCEP on third-party payment institutions

DCEP is likely to affect third-party payment and settlement services, sales of funds and asset management products, and big data information services. It is worth emphasizing what kind of cooperation mode the central bank and third-party payment institutions will adopt in the future, and how large-scale the promotion and use of DCEP will have different impacts on the three types of business of third-party payment institutions.

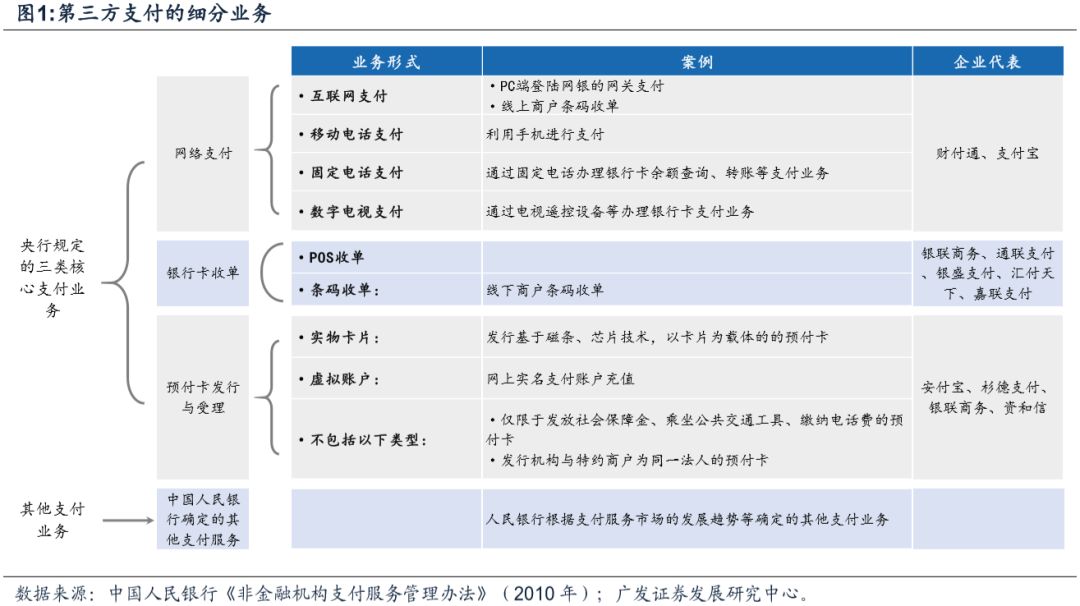

(I) Three types of business of third-party payment institutions

There are three types of third-party payment institutions that may be affected by DCEP in the future. The first is the payment services permitted by the central bank, including online payment, prepaid card issuance and acceptance, etc .; the second is the sales of asset management products that leverage the flow advantage of payment platforms. Into the sales port of money funds; the third is credit-related and risk-control related businesses derived from the payment of big data, such as microcredit and sesame credit scores.

The core business of third-party payment agencies is payment services. At present, the payment services approved by the central bank for non-financial institutions mainly include three types: online payment, bank card acquisition, and prepaid card issuance and acceptance. Compared with the payment services provided by commercial banks, the most distinctive payment service of third-party institutions is network payment services. One of the classic realistic scenarios is mobile payments [1]. The biggest difference between mobile payment services and other electronic payments lies in two points: First, providing software and hardware facilities to facilitate payment. Such as two-dimensional code and code scanning equipment. Second, set up a virtual account to transfer transactions between virtual accounts to achieve faster transaction payment. The specific transaction settlement is realized by the network connection platform. In addition, third-party payment agencies also record transaction payment information with virtual accounts as account names.

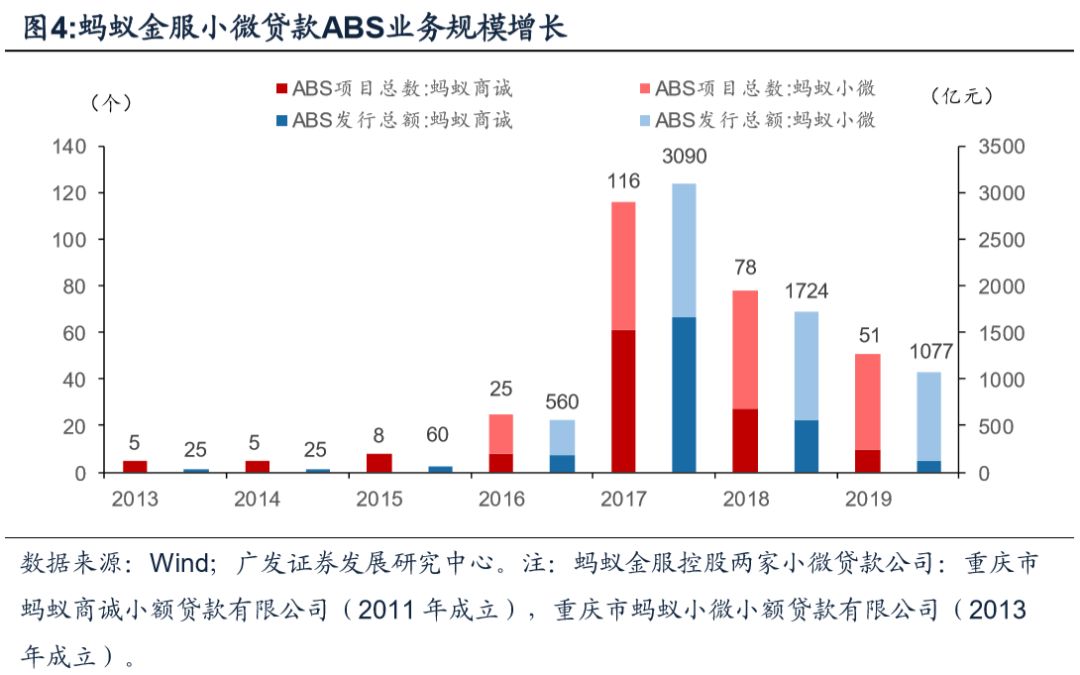

Another important type of business for third-party payment institutions is the use of payment platforms to sell money funds and other asset management products. Convenient third-party payment attracts a large number of payment behaviors and generates transactional big data information. In order to take full advantage of big data traffic, third-party payment institutions have access to sales portals for money funds and other asset management products. Take “Yuebao” as an example. After the establishment of Yu'ebao Currency Fund (predecessor), it was connected to Alipay, and the fund scale expanded rapidly. At the peak, Yu'ebao's scale reached 1.69 trillion (the first quarter of 2018), accounting for 23% of the total market share of the money fund at that time.

Third-party payment agencies leverage big data to leverage credit-related and risk-control related businesses. The advantage of payment flow lies not only in the establishment of a convenient cargo base and other sales channels, but also the development of unique advantages in credit reporting and risk control. Third-party payment institutions have actively promoted two types of business in recent years using transactional big data information. The first is to expand microfinance products such as cash loans, and issue consumer loan ABS based on this. The second is to develop third-party credit reporting and provide risk identification services for commercial banks and users based on personal credit status analysis. Take Ali's Sesame Credit as an example. After obtaining the user's authorization, the Alipay platform will pass personal transaction data to Sesame Credit, and analyze the personal transaction data to score the user. Commercial banks can cooperate with Sesame Credit. Similarly, after the user authorizes, the bank uses the Sesame score as a basis for providing follow-up services to residents, such as online card issuance and risk control [2].

We believe that the most important of the three types of business of the three-party payment institutions is payment services, and the latter two types of businesses are rooted in the advantages of the payment flow platform. The most important reason for the rapid promotion of third-party payment institutions and the accumulation of transaction payment flow advantages is that third-party payment improves the public payment experience. 1. Compared with cash payment, electronic payment methods such as scan code payment reduce the tedious steps of change, rounding and authenticity verification. 2. Compared with the bank account method, the third-party payment collection interface is unified. Even if the merchants and residents have different account opening banks, the unified payment interface can still be used in subsequent payment processes without considering specific details such as inter-bank transfers.

(2) The impact of DCEP on third-party payment business

According to the currently known central bank digital currency positioning and dual-layer operation model [3], the central bank's digital currency eventually moves to the retail end, and its position in the currency derivation mechanism is equivalent to M0. Considering that the actual carrier of DCEP is a form of mobile APP, PC-side network payment, etc., its use experience on the C-end is similar to the existing third-party payment experience, and DCEP has high payment convenience, so it may The three-party payment business poses certain challenges. In other words, DCEP can not only replace the cash in circulation (M0), but also may affect the current third-party payment.

Judging from the existing patent information, it is highly likely that the central bank's digital currency will be hosted in a commercial bank in the form of a digital wallet. The specific technical implementation path of the central bank's digital currency may be completed by market competition and optimization [4]. Based on this clue, it is speculated that whether there will be other areas of cooperation between the central bank digital currency and third-party payment systems, such as the design and promotion of digital currency APP ports, it is worth our attention. According to the current information, we believe that after the promotion of DCEP, the existing third-party payment business model may face three changes.

1. Due to higher payment convenience and higher credit endorsement, DCEP may pose a challenge to the payment service business of third-party payment institutions. DCEP is designed to fuse electronic and cash payments, and to absorb current cutting-edge payment technologies. As a result, the existing payment convenience advantages of third-party payments are no longer prominent. For example, payment methods such as bank card payment (debit card, credit card swiping), APP scanning (Alipay, WeChat), mobile phone based near field communication (NFC), etc. currently scattered among different payment channels will be integrated by DCEP in the future. In addition, the current electronic payment method supports single-offline payment in most daily life scenarios, and DCEP can allow both parties to the transaction to be temporarily offline in each scenario [5]. As another example, according to the current patent release information, in the future, DCEP will support at least chip card swiping [6] and mobile phone near field communication [7] on the client side. It can be seen that the central bank's DCEP payment convenience is extremely high. More importantly, DCEP enjoys central bank credit endorsement, which is more secure than third-party payments.

Second, the specific implementation of the central bank's digital currency and the promotion mechanism are not clear, and the impact of DCEP on the platform's sales of asset management products is still uncertain.

It can be intuitively found from the data that due to enjoying the payment traffic bonus, the scale of asset management products after access to third-party payment platforms tends to grow relatively quickly. Whether it can continue to enjoy the traffic dividend by relying on the trading platform depends on whether the DCEP client can still access the asset management product sales port in the future. If the third-party payment institution is qualified to develop and operate the digital wallet client of the central bank, or if DCEP directly uses the existing third-party payment APP as the client and allows the asset management product sales interface to be retained, the cargo base and other data associated with the platform The impact of product sales and scale is small, otherwise the impact will be greater.

3. In the DCEP model, third-party payment institutions have a high probability of losing their transaction accounting qualifications and transaction data information, and their credit information and risk control services developed by leveraging big data services may be affected.

At present, third-party payment institutions have cooperated with some financial institutions. With the permission of consumers, they use transaction payment big data information to score consumers. As a basis for financial institutions to provide services such as card issuance, such businesses are mainly based on three-party institutions. Based on the acquired transaction information. Regardless of how the final central bank digital currency client APP is designed, taking into account design requirements such as controllability and anonymity (that is, only the central bank or residents themselves can obtain transaction information under certain circumstances), DCEP will most likely pay the payment services of third-party payment institutions. Form a partial replacement. Once the transaction flow of the third-party payment platform users and the information advantage obtained are reduced, the big data services based on transaction data will also be affected synchronously.

In addition to the three possible impacts of the above-mentioned DCEP on third-party payment institutions, there are two more notable ones.

1. Regardless of the specific mechanism of the final landing, the C-terminal user experience in DCEP and traditional payment systems may remain largely unchanged, but the paths and technologies used to implement payment settlement behind the two systems are completely different. Under the traditional electronic account-based payment system, when using the services of a three-party payment institution, there are two steps of payment and settlement at each stage. Payment is the change of funds in the payer's bank account and the three-party virtual account of the payee, which is performed by the internal accounting system of the banking system and the internal payment of third-party payment institutions. Clearing and settlement refers to changes in the funds in the bank reserve account and the three-party agency reserve account, which requires the online payment system. In the DCEP system, regardless of the specific expression adopted by the final client, the transaction payment is realized based on the "token" system. "Payment is settlement" in the "token" system, just send the digital currency in the digital wallet client of the payer to the digital wallet of the payee.

In the future, third-party institutions may focus on the C-end payment experience of digital wallets and attract customers through differentiated competition. Of course, we can't rule out whether other central banks and third-party payment structures will reach other win-win cooperation models based on traffic and other factors. The specific impact may be another situation.

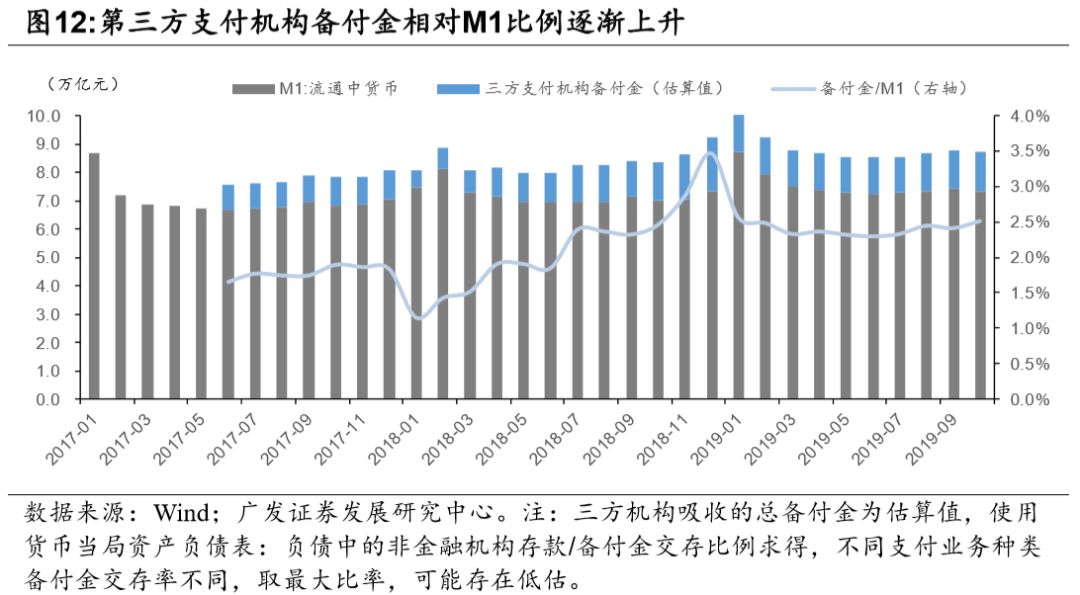

2. Before and after the promotion of DCEP, third-party payment institutions cannot use reserve funds. At present, the reserve account of the third-party payment institution has about 1.5 trillion yuan of funds [8]. If DCEP replaces third-party payment in the future, the size of the third-party reserve fund will decrease, does it mean that the amount of funds available to the third-party payment institution? cut back?

In fact, the reserve account is currently frozen on the central bank's liability side, and third-party payment institutions cannot use the 1.5 trillion reserve account funds. With the introduction of DCEP, a possible change is that the reserves deposited by the three parties have been reduced due to partial replacement, and the DCEP issued by the central bank has increased, and the underlying currency structure will therefore change. We will elaborate on this in Part IV.

The impact of DCEP on the traditional business of commercial banks

DCEP may have two direct impacts on commercial banks, one is the interest rate and scale of bank deposits; the other is the intermediate business income brought by digital currency custody.

(1) Two types of traditional business models of commercial banks

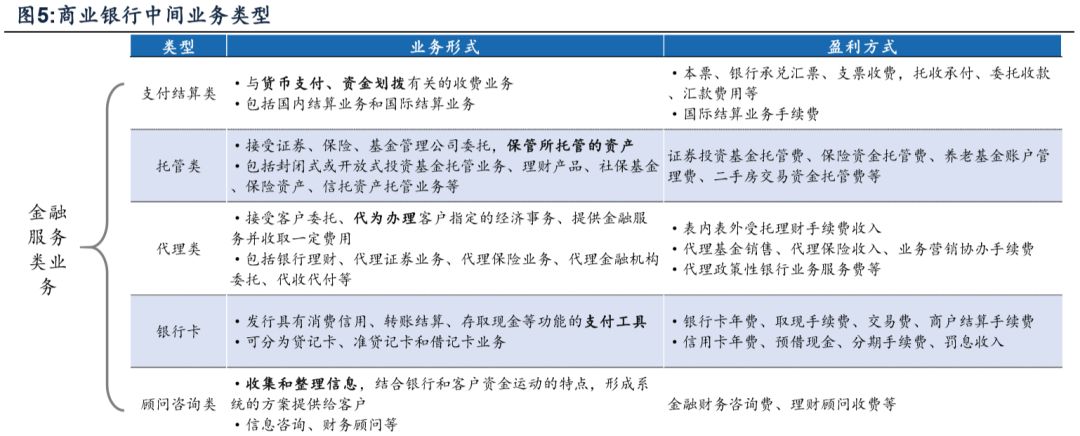

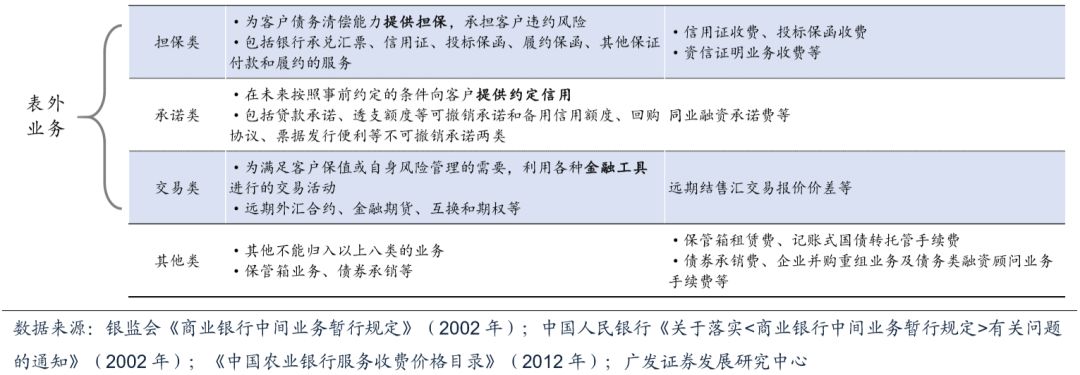

Banking operations can be broadly divided into interest margins and intermediate businesses. The interest margin business refers to the business in which a commercial bank acts as a financial intermediary to carry out fund integration and withdrawal activities, which is included in and affects the balance sheet. Intermediate business refers to the business that does not affect the on-balance sheet assets and liabilities of a commercial bank, but forms non-interest income of the bank [9].

The interest margin business is a traditional business of commercial banks. The operating status of the interest margin business is directly affected by the cost of the liability side and the revenue of the asset side. Finally, the net interest margin can be used for observation. It is generally believed that factors such as interest rates and credit risks faced by banks are important factors affecting the net interest margin of commercial banks. If a commercial bank is regarded as a fund bidder, the deposit interest rate can be regarded as the fund's selling price, and the loan interest rate can be regarded as the fund's buying price. The bank can obtain a profit by setting a bid-ask spread. But at the same time, there are credit risk, liquidity risk, and maturity mismatches in deposit and loan cash flows. Banks need to consider credit risk and returns comprehensively, set reasonable interest margins to resist risks, and determine business strategies for interest margin businesses.

Intermediate business can be roughly divided into two categories, financial service fee-based intermediate business that does not form off-balance-sheet assets and intermediate business that forms off-balance-sheet contingent assets. Among them, the intermediate business that is closely related to the future DCEP mainly involves two types of payment clearing and settlement and custody. 1. Banks provide a variety of debit and credit payment settlement and settlement tools. For example, by providing payment instruments such as bills of exchange, promissory notes, checks, and exchanges, a certain fee is charged to the receiving and paying parties. Merchants will be charged during the POS payment process. 2. Banks can be used as fund custodians for securities products, for example, providing securities investment accounts and pension account services.

(II) The impact of DCEP on commercial banks

DCEP's dual operating model is the key to banking business. The so-called "central bank-commercial bank" dual operation mode refers to the binding of bank accounts and digital wallets, which are equivalent to being hosted in commercial banks. The dual operation mode of DCEP may have two effects on traditional banking business.

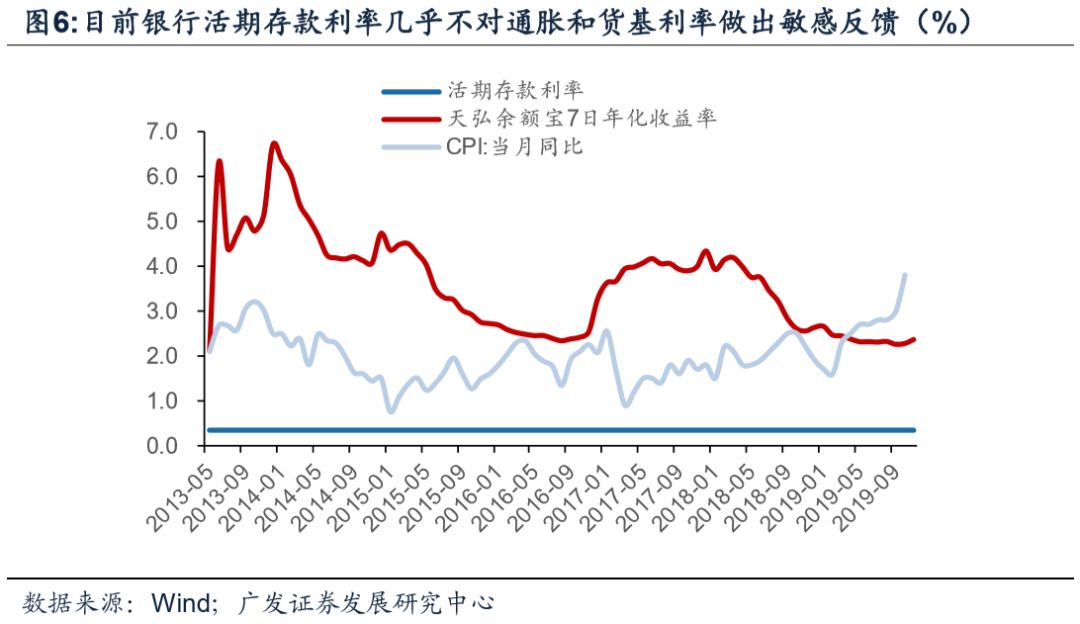

I. DCEP may affect the source of funds on the liability side of banks and affect the cost of liabilities. For residents, whether it is time deposits, wealth management products, or money funds, redemption and withdrawal always face certain restrictions, which is not as convenient as demand deposits. Therefore, residents are always willing to hold a certain amount of low-interest demand deposits. This convenience premium can be evidenced by the decoupling of past demand deposit rates from inflation and money fund rates. However, after the promotion of digital currency by the central bank in the future, residents may convert bank demand deposits into DCEP and deposit some funds in digital wallets, instead of fully converting cash into central bank digital currency. In other words, it is possible that DCEP will replace the electronic payment of demand deposits instead of just cash. The case that can be referred to is that before and after the expansion of third-party payment scale, the proportion of cash in the base currency remained at about 20%. However, the proportion of third-party reserves increased and the proportion of excess reserves decreased by the same amount [10]. Because DCEP is a central bank liability, not a bank liability. The expansion of DCEP may correspond to the "disintermediation" of bank current deposits to a certain extent. In addition, the speed of conversion between bank deposits and DCEP has led to a reduction in the stability of general deposits. In order to stabilize the source of demand deposits, banks may have an increase in interest rates on liabilities.

Of course, in order to avoid a greater impact on the bank's debt end, the central bank has several possible countermeasures. For example, DCEP does not carry interest and reduces its attractiveness [11]. Or set a certain commission fee for the exchange of bank deposits to DCEP, which is similar to the current commission fee for current deposit withdrawals.

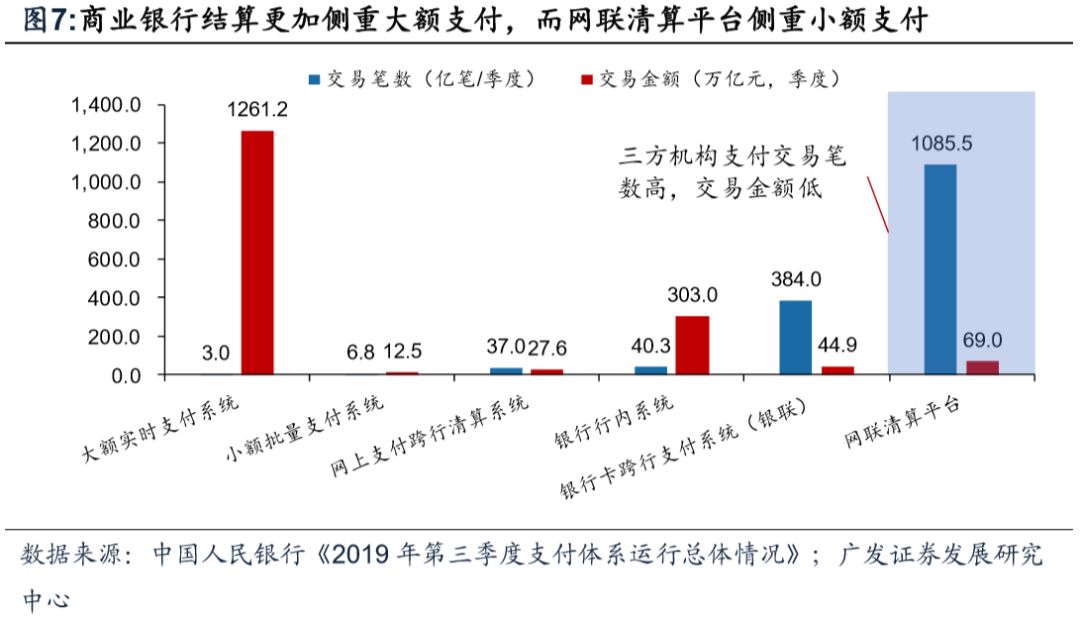

2. DCEP may affect two types of intermediary services: payment clearing and settlement and digital currency custody. 1) Compared with third-party payment institutions focusing on small retail payment services, the bank's clearing and settlement business provides large payment and clearing services for banks and businesses, which may be an area where it has certain advantages. If DCEP only replaces small retail payments in the future, the size of commercial banks' large payment clearing and settlement will not be affected much. However, according to the current patent information, the central bank's digital currency can also be applied to large payment clearing scenarios. For example, banks can transfer funds between DCEP business banks, which serve the function of the original interbank clearing account [12]. In this case, the scale of bank payment and settlement business will be affected. 2) In the binary operation mode of DCEP, digital wallets are hosted in commercial banks, and bank accounts and digital wallets are bound to each other [13]. This custody model is quite similar to the existing account custody business model of commercial banks. In the future, commercial banks may consider hosting digital wallets as a new type of intermediate business, charging customers using wallets certain custody fees, or promoting wallets through low-cost policies to attract customer traffic to carry out other value-added services.

In addition to the two types of intermediate businesses mentioned, commercial banks can also provide other digital currency derivative services. Digital currency circulation management services may contribute a certain proportion of revenue to the bank in the future [14].

3. DCEP may have an impact on the efficiency of central bank regulation

DCEP may improve the efficiency of the central bank's control policies in three aspects. First, if DCEP calculates interest, DCEP interest rate can be used as a new type of price tool, and it can even be used to break the zero interest rate lower limit. Second, the DCEP "token" bookkeeping method and convenient information recording can reduce central bank supervision costs. Third, DCEP can be loaded with specific functions, which helps the central bank to carry out structural regulation more effectively.

(1) The central bank's regulatory mechanism affecting currency derivation

Generally speaking, the central bank influences the expansion of commercial banks' banks through two perspectives. One is monetary policy aimed at cyclical regulation, and the other is macro-prudential policy aimed at risk prevention. In terms of specific mechanisms, the former specifically affects the amount of excess reserves and statutory deposit reserve ratios to influence the extent of bank expansion. As for the bank expansion structure, it is not the focus of total monetary policy control. It can be said that the aggregate monetary policy aimed at cyclical regulation does not care about the specific business behavior of banks; compared with the cyclical regulation policy, macro-prudential policies more specifically affect the specific bank expansion behavior of banks.

In order to explain that the central bank's policy control logic mainly includes two types of cyclical monetary policy and macro-prudential financial supervision, we may first briefly review the principle of currency derivation.

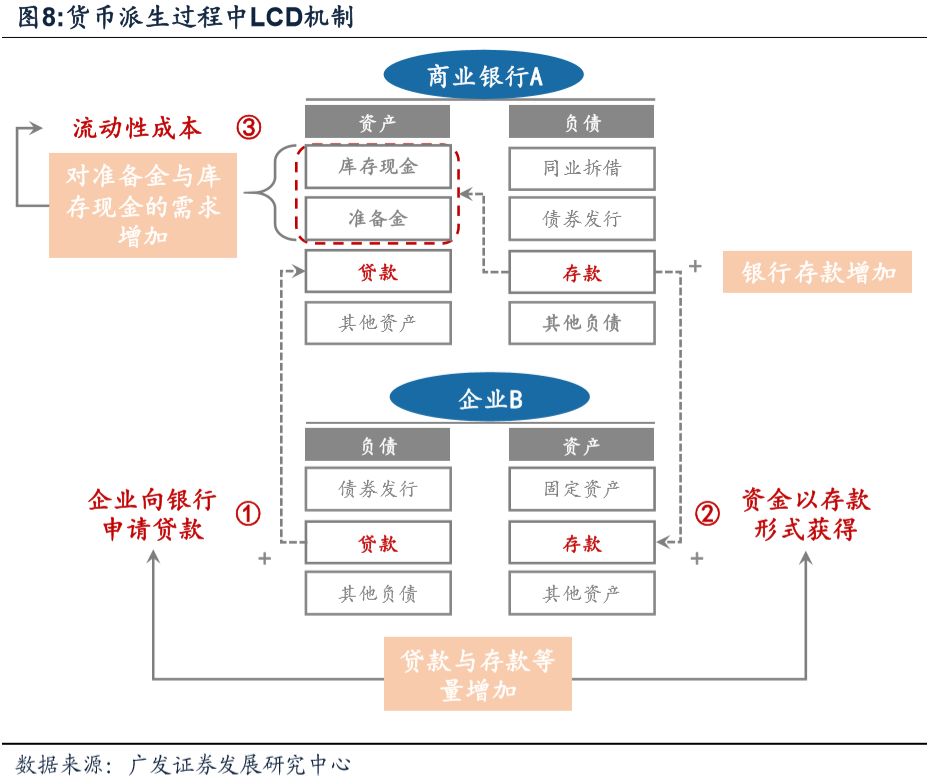

As a bank liability, the currency derivation process is also a process by which commercial banks and the physical sector expand their tables. From the perspective of a specific individual commercial bank, we can say that bank deposits are "deposited" by enterprises or residents. Retrospective of this deposit may be the physical sector withdrawing cash from other banks and depositing it, or direct bank transfer. The question is how was the original deposit created? A better understanding is to make a difference between all the inter-bank businesses, excluding inter-bank holdings, deposit transfers, cash withdrawals from one bank to deposits in another bank, etc., so that we can think more clearly about the initial The question of "how deposits are created". Obviously, after all the inter-bank business is rolled out, the creation path of bank deposits becomes clear-each expansion of the bank's balance sheet is driven by the asset side and the debt side. Corresponding to the real situation, the process of creating deposits is also a process of credit growth, which is essentially the process of credit expansion of banks and the physical sector: the physical sector borrows a credit → the entity's debt expands and the bank expands → the company's access to credit means it receives a sum Deposits → corporate asset-side deposits expanded and bank liabilities expanded simultaneously. This process is called the Loan Creates Deposit (LCD) mechanism.

Money cannot be created indefinitely because the bank needs to expend costs ("liquidity costs" and regulatory costs) each time it expands its balance sheet. Since credit-driven deposit expansion, it seems that money creation is nothing more than a simple bookkeeping of the bank's balance sheet, and logically, money can expand indefinitely. The question now is, can banks expand their tables indefinitely? First of all, it can be affirmed that when the credit conditions of the entity are insufficient, the bank will carefully consider putting credit on it, so from this point of view, the state of physical assets determines the degree of currency creation to a considerable extent. In fact, there is another important change in the process of commercial bank expansion. It is easy to be ignored. After each LCD process, the commercial bank will closely follow the business adjustment actions of the two asset terminals. The legal deposit reserve is paid for deposits, and the excess reserve held is reduced; the second is assuming that the cash holding ratio is unchanged (affected by factors such as current payment conditions), the scale of public withdrawals will also increase after the expansion of deposits, and bank cash inventories will increase (That is, cash held by banks). This means that after each LCD, commercial banks will face excess reserves and cash loss from inventory. Banks can ask the central bank to cash out excess reserves as cash on hand. If the excess reserves are regarded as the liquidity of a commercial bank, the commercial bank will need to pay a certain "liquidity cost" after each LCD. Not only that, but further considering the various regulatory constraints faced by banks in the process of expanding their tables, each LCD not only requires the bank to bear the "liquidity cost", but also other regulatory costs. The classic example is that loan expansion will consume capital. This means that given the constraints of liquidity and regulatory conditions, banks will eventually be unable to expand their tables indefinitely, and the currency creation process will eventually converge.

By regulating the cost of bank expansion, the central bank can achieve the regulation and structural impact on the total bank expansion. Among them, the central bank mainly adjusts the rhythm of the expansion of the overall scale of commercial banks through the supply of liquidity, and influences the bank's structural expansion through the setting of regulatory conditions. The process of currency creation is the process of bank expansion. Since a commercial bank consumes liquidity and supervision costs every time the bank expands, currency creation is not unlimited, and it is restricted by the amount of liquidity and regulatory conditions. For the central bank, it is precisely by adjusting the cost of bank expansion, that is, the cost of liquidity and supervision costs can affect the bank's expansion, which affects the total amount of money created and which credits the currency is derived from. With regard to the supply of excess reserves, the central bank can adopt two methods of expanding and non-expanding. The so-called expansion method refers to placing excess reserves by purchasing assets or increasing claims on financial institutions, and conversely recovering the reserve; the so-called non-expand method refers to changing the reserve structure by reducing the reserve and statutory "freezing" The reserve is thawed to excess reserves, and the effect of upgrading is reversed. In terms of regulatory conditions, the central bank can achieve more direct and more structure-oriented bank expansion regulation by setting specific regulatory conditions. For example, financial inter-bank regulatory requirements limit the expansion of inter-bank assets and liabilities, and also restrict the overall expansion of banks. Another example is to set structural or targeted credit scale assessment requirements to guide banks to expand their table structure. Of course, under the current regulatory hierarchy, supervision that focuses on micro and specific details sinks to the CBRC, and the central bank is mainly responsible for the top-level design of supervisory policies and macro-prudential supervision.

(2) DCEP may improve the efficiency of central bank regulation

The continuation of this series, "Contingent Operating Mechanisms for DCEP," states that DCEP may have three significant features. The first is to replace M0, so it can capture the cash payment information of the physical sector that was not available in the traditional electronic payment system. The second is to record based on "tokens" to more clearly and efficiently capture the information and currency of each currency transaction. Load specific functions to facilitate the implementation of targeted currency placement by the central bank.

The above analysis illustrates how the central bank influences bank expansion through liquidity (base currency) supply and regulatory assessments. In addition, we know that the central bank's regulation and control purpose has two points, one is to regulate the overall bank expansion process of commercial banks, and the other is to regulate the structural behavior of commercial bank expansion.

Based on the characteristics of the DCEP payment system, the central bank's control methods, and the purpose of control, we deduced that the future DCEP system may improve the central bank's control efficiency in three aspects.

1. If DCEP interest is calculated [15], DCEP interest rate can be used as a new type of price tool, and it can even be used to break the zero interest rate lower limit. 1) Logically, DCEP can achieve differentiated interest calculation. At present, the central bank pays an interest rate of 1.62% on the statutory deposit reserve of commercial banks, and an excess reserve interest rate of 0.72%. It cannot pay interest on cash. After the launch of DCEP, not only can interest be finally calculated on "cash", but because DCEP has recorded detailed information on the owner of the currency [16], logically the central bank can price differentiated interest rates for different currency holders. For example, the DCEP payment interest rate on the inventory held by a commercial bank is analogous to the excess reserve interest rate and can even be used as the lower limit of the interest rate corridor in the interbank market. In the same way, the “in circulation DCEP” held by individuals can also pay interest, even differentiated interest rates. 2) An important reason for the existence of the zero interest rate lower limit is that cash is always an alternative in asset allocation, and cash has zero nominal interest under the traditional monetary system. If the digital currency replaces M0 in the future, the scale of M0 will decrease. At this time, negative interest rates will be given to the central bank digital currency. Even if the income is low or even negative, people will have to hold central bank digital currency. In this case, the negative DCEP interest rate will reconstruct the asset pricing system.

Second, the information recording method in the DCEP "token" bookkeeping method is more convenient, or it may reduce the supervision cost of the central bank. In the traditional payment and regulatory framework, the central bank and other financial regulatory agencies need to use statistical indicators, financial statement data, and on-site and off-site inspections, which are costly and time-efficient. In particular, to track the specific flow of a particular currency, it is necessary to "disassemble" all the books of the currency circulation path, and the supervision efficiency is low. DCEP's information recording model based on "tokens" means that the central bank registration center records detailed information such as digital currency ownership and transaction flow, without the need to check the compliance of securities and accounts, and the cost of supervision is reduced. Based on this, we believe that after the promotion of DCEP in the future, the central bank will be able to track currency flows in a more vertical direction and improve regulatory convenience.

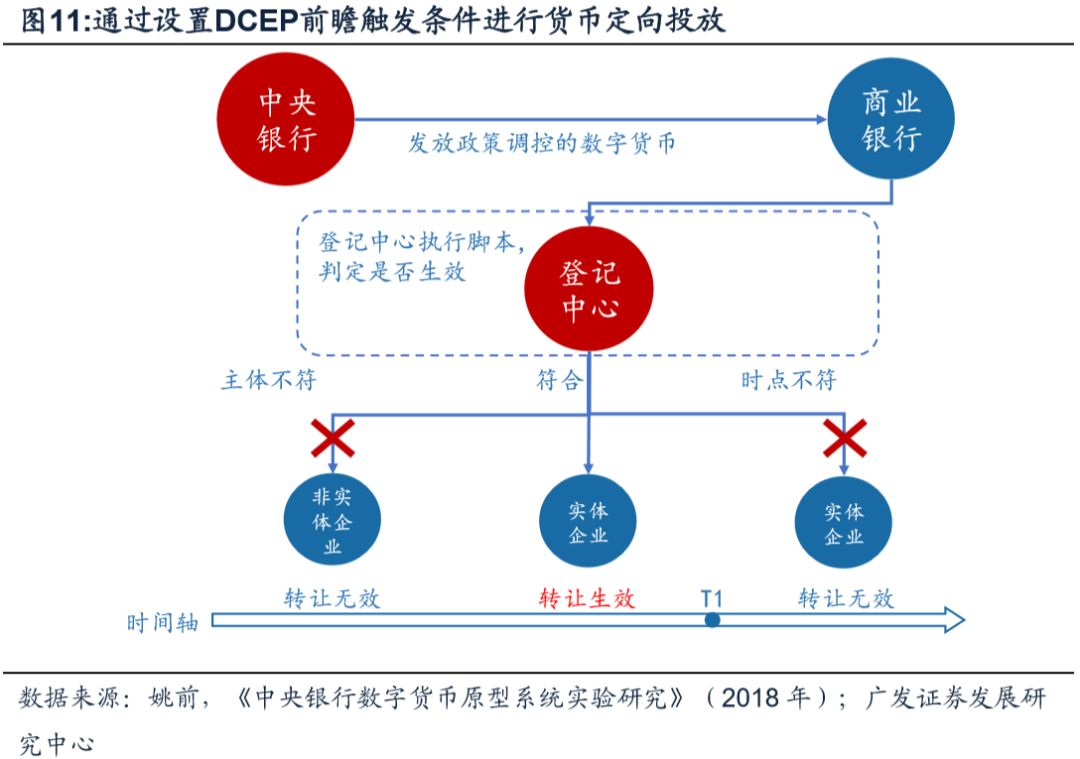

3. DCEP may facilitate the tracking and control of capital flows and help the central bank to carry out more effective structural regulation. Under the original system, traditional monetary policy focused on aggregate regulation, and structural regulation functions were weak. The transfer of wide money from the central bank to wide credit requires financial institutions such as banks as transmission intermediaries. If there is a failure in the market pricing mechanism, the credit structure will often deviate from the optimal state, and the central bank's structural regulation of credit is often inefficient. First, the DCEP system can more effectively capture the flow of funds. Based on the technical feature of DCEP, more flexible capital pricing can be reached between the central bank and commercial banks, thereby incentivizing banks to return to the optimal state in credit structure. For example, the central bank may auction different liquidity prices for different bank credits, thereby avoiding the issue of incentive incompatibility caused by the inability to track the funding direction. Secondly, according to the patent information provided by the central bank (four "forward-looking condition trigger" designs), the central bank can load specific functions on the DCEP expandable and programmable fields, from the main body controlling the credit placement of commercial banks [17], interest rates [18 ], Time [19], that is to effectively achieve the four structural regulation. Not only that, the central bank can also adjust the ex post settlement interest rate of credit according to the economic environment in which the credit is placed, and the accuracy of structural regulation is further improved.

There are two other points worth noting about the impact of DCEP on central bank efficiency.

First, whether the negative interest rate can be implemented effectively and whether it is necessary will depend on the current financial system structure and economic status of a country. Especially when the mainstream overseas developed countries implement zero or negative interest rates, the economy and finance have shown some negative effects. Whether China needs to implement negative interest rates is a topic worthy of further discussion. This article explores the possibility of DCEP interest rate calculation and implementation of negative interest rates, based on purely logical analysis. The purpose is to explore whether DCEP can theoretically broaden the monetary policy boundary for the central bank.

Second, at present, the open market operations of first-tier dealers and inter-bank settlements between financial institutions can only be completed through the central bank reserve account. The central bank reserve account is embedded in the large-value real-time payment system, which has restrictions such as running time. DCEP's transaction bookkeeping and calculation methods are very different from traditional electronic payments, and are more efficient. In the future, DCEP can not only replace M0, but also logically become a supplementary form of excess reserves. And higher payment and settlement efficiency means that the financial industry's liquidity reserve friction is reduced, and the financial industry's behavioral efficiency can be improved as a result.

Fourth, the impact of DCEP on the traditional currency derivation mechanism

DCEP adopts the "central bank-commercial bank" secondary operation mode, which means that DCEP adopts the traditional credit currency derivation mechanism. The main body of currency creation still lies in the banks and the physical sector, and the central bank only plays a regulatory role. In addition, there is no essential difference between the DCEP placement model and the traditional base currency placement, especially the excess reserves and cash. The specificity of DCEP compared to traditional base currencies will affect the traditional currency derivation mechanism. We believe that the impact of DCEP on the traditional currency mechanism can be basically divided into two aspects. One is to affect the base currency and currency multiplier of the currency derivation mechanism; the other is to overcome some defects of the traditional currency derivation mechanism and help reduce risks.

(I) Restructuring the basic currency structure and affecting the currency multiplier

While DCEP continues the traditional currency derivation mechanism, it may have two effects on the traditional currency derivation mechanism. 1. The new string shape feature of DCEP means that the central bank's basic currency structure will be restructured. Second, the DCEP accounting, transaction payment and settlement characteristics mean that the currency derivation mechanism with DCEP participation will have a currency multiplier different from the traditional model.

1. The DCEP system will restructure the basic currency structure of the central bank.

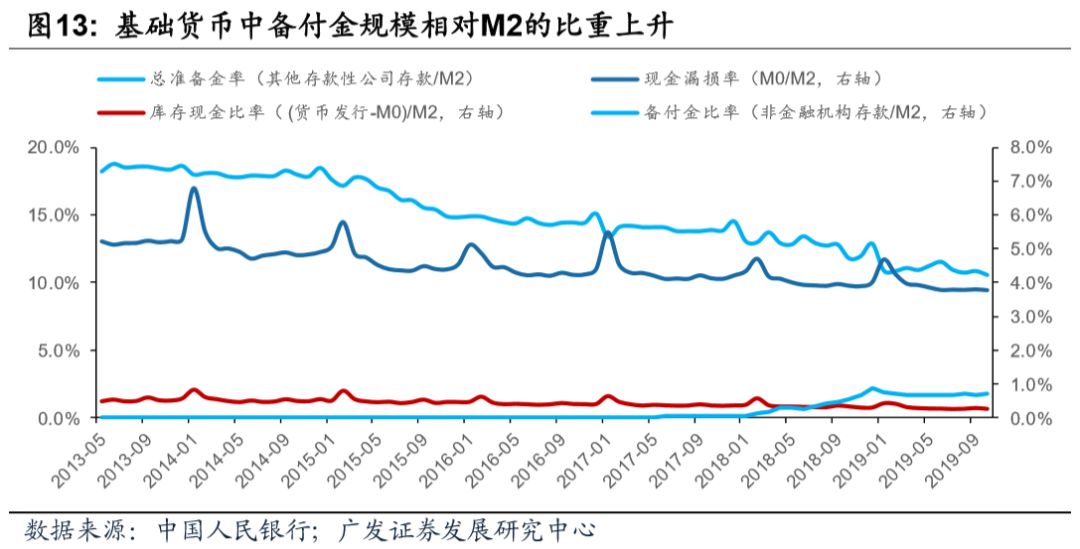

1) The central bank records the central bank's digital currency in the "base currency" account on the liability side or opens a new subdivided account. In the traditional model, the central bank's basic currency structure is divided into two parts. One is the reserve reserve of financial institutions (mainly commercial banks) in the central bank, which includes the excess and statutory components. The other is currency issuance, that is, cash printed by the central bank. Depending on whether the cash remains in the commercial bank or is held in the physical sector, currency issuance is divided into cash on hand and cash in circulation (M0). The basic currency structure of mainstream countries is better. Later, due to the provision of deposits by third-party payment institutions, the People's Bank of China set up a sub-item in the base currency, which is called "non-financial institution deposits". The central bank digital currency can be used as cash, logically as an excess reserve or a third-party reserve. Based on the DCEP payment purpose, the future central bank base currency account, or a new subdivision to specifically record the central bank digital currency: For example, under the subdivisions of M0, excess reserves, non-financial institution deposits (recording of reserves by third-party payment institutions), sub-accounts are set up to record DCEPs that are ready to be paid to residents in inventory.

2) After the large-scale promotion of DCEP, it may have an impact on the scale of traditional M0, excess reserves, and reserves of third-party institutions. First, at the level of interbank wholesale, the convenience of DCEP payment means that the tendency of financial institutions to choose traditional electronic payment for interbank settlement has decreased, while the tendency of using DCEP for interbank clearing and settlement has increased. As a result, inter-bank use of DCEP has increased, and excess reserves in the form of bookkeeping have been reduced. Non-bank financial institutions directly use their DCEP to make payments, and commercial banks have overbooked the "clearance form" of excess reserves in payment clearing houses. Gold will also fall. Secondly, at the retail level, currency in circulation, cash at commercial banks, and reserves from third-party payment institutions all decreased. The three types of funds are mainly used for settlement and settlement between residents. In the case of faster payment and settlement, there is no need to take a "preventive reserve" for payment settlement, and this part of the funds will also decrease.

Second, the currency derivation mechanism in which DCEP participates, the currency multiplier may be changed from the traditional model. There are two positive and negative mechanisms for the impact of DCEP on the currency multiplier. The final result depends on the strength of the two mechanisms.

1) The convenience of transaction payment is improved, the reserve motivation of entities holding cash or banks holding excess reserves is reduced, and the currency multiplier may increase. As the central bank's digital currency system clears faster, it reduces the total amount of funds in transit and reduces the amount of funds deposited in virtual accounts of third-party institutions. At the same time, the DCEP bank vault replaces interbank clearing accounts and reduces the funds in the clearing account. When the base currency is unchanged, both of them lead to a decrease in funds used for payment, an increase in funds used for credit, and ultimately an expansion of the currency multiplier. The central bank can meet a larger range of funding needs through smaller reserves.

2) The DCEP leakage rate in the base currency becomes larger, and the currency multiplier may decrease accordingly. If the central bank's digital currency payment is widely used, or if the central bank pays DCEP interest, it will cause the DCEP / deposit ratio to increase and the currency multiplier to decrease.

After the final promotion of DCEP, whether the currency multiplier increases or decreases depends on the comparison of the above two forces. Of course, as mentioned earlier, the statutory deposit reserve ratio affects the currency multiplier to a large extent, and the reduction or increase in the future will increase the difficulty of observation.

(B) improve the efficiency of counter-cyclical operations and reduce the characteristics of pro-cyclical

There are two risks to the traditional currency derivation mechanism, one is the moral hazard of third-party payment institutions, and the other is the endogenous procyclical nature that traditional mechanisms cannot overcome. The currency derivation mechanism in which DCEP participates can improve the above two defects to a certain extent.

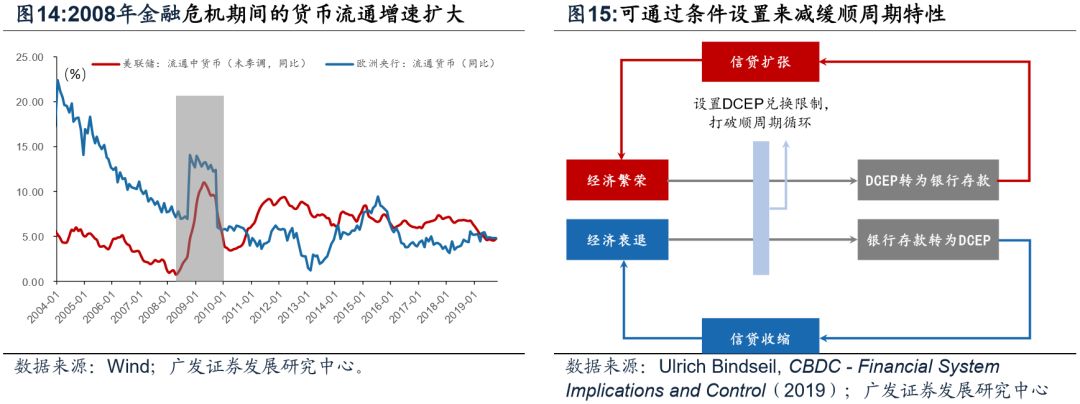

First, DCEP may help reduce the pro-cyclical characteristics of currency derivation, and especially it can effectively respond to extreme liquidity risks.

1) Or improve the efficiency of the central bank's counter-cyclical regulation and smooth the procyclical behavior of financial institutions. The procyclicality of monetary policy means that during the period of economic prosperity, upward asset prices, physical demand and bank credit expansion spirally strengthen each other; conversely, during economic recession, downward asset prices, physical demand and bank credit shrinkage also strengthen each other. This is why the central bank must carry out counter-cyclical regulation and intervention in the economy under the traditional credit currency system. However, in fact, each cycle is accompanied by structural characteristics, and the central bank cannot tend to invest liquidity in a specific entity sector through total currency easing, thus deteriorating the effect of counter-cyclical regulation. After the promotion of DCEP, the central bank can more easily observe the flow of money, and the second can guide banks to expand their table structure, which improves the efficiency of counter-cyclical policy regulation. The result is a reduction in the risks associated with the procyclicality of currency derivation mechanisms.

2) The procyclical behavior of the extreme case table may be suppressed to a certain extent. When an economic crisis occurs, residents ’risk appetite quickly drops, bank deposits are withdrawn and cash is held, and bank deposits are lost. In extreme cases,“ runs ”will occur. If DCEP is widely held by residents in the future, logically, the conversion speed between bank deposits and DCEP will be faster than the conversion speed between bank deposits and cash. It seems that the pro-cyclical problem may be much more serious than the existing banknote minting conditions. However, in fact, compared to cash, the supply efficiency of DCEP can be higher. For example, temporarily opening a discount window during the crisis, providing DCEP "rediscounting", etc., for banks to quickly inject DCEP for residents to "cash out"; Low negative interest rates prevent residents from further demand for DCEP conversion. Of course, the digital currency environment places higher requirements on the central bank's emergency policy.

Second, DCEP helps reduce the moral hazard of third-party payment agencies.

1) In the past, there were two possible contingent moral hazards in third-party payments. In the past, the central bank has two main concerns about third-party payment institutions. First, the settlement business of the three-party institutions replacing banks is not completely transparent, or there is a risk of "shadow payment clearing". That is, the internal clearing of virtual accounts masks the actual transaction information of residents, making it difficult for the central bank. Supervision of illegal transactions such as money laundering [21]. 2. Payment institutions usually deposit reserve funds in custodian banks and charge high interest rates on agreement deposits, but they may also embezzle them and even invest in high-risk assets [22], similar to the “shadow banking” model [23].

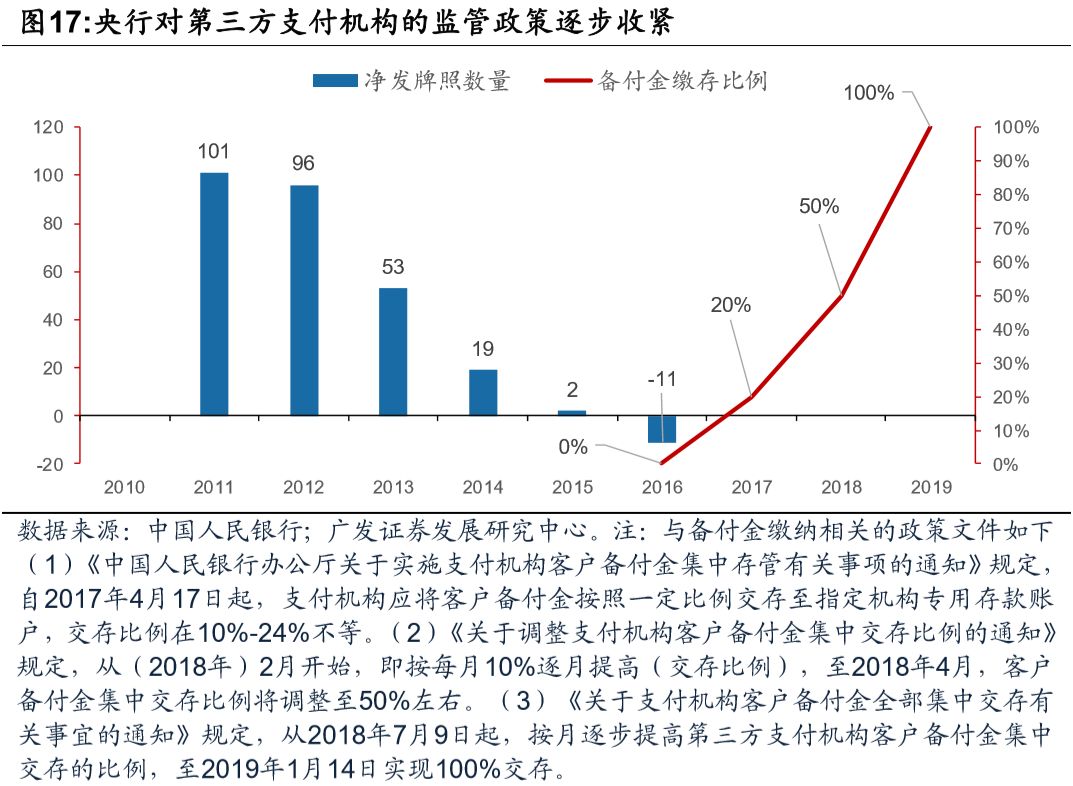

2) In recent years, the central bank has tightened its third-party payment supervision policy. Since 2010, the central bank's supervision of third-party payment institutions has gradually tightened. First, the third-party payment institution “disconnected directly from the commercial bank” and reported the transaction information to the network for settlement and settlement. Second, third-party payment institutions open equipment payment accounts in the branches of the central bank and pay 100% of reserves. In the end, the central bank reduced the risks associated with misappropriation of reserves and opacity of third-party payment information.

risk warning:

The progress of DCEP exceeded expectations, and DCEP finally achieved the framework beyond expectations.

appendix:

Appendix 1-Third Party Reserve Fund Structure and Deposit Requirements

There are three main sources of third-party agency reserves. 1. As third-party payment institutions provide payment services to customers, users may store some funds in virtual accounts for subsequent use (such as Alipay balance and WeChat change). Second, third-party institutions usually delay the settlement of merchants (such as offline bar code payment). After a certain period of time, funds are transferred to the merchant's bank account, so there will be a certain amount of funds in the reserve account. 3. Alipay and other institutions provide guarantee services for transactions between users and merchants (such as Alipay confirming receipt and repayment within 7 days), and also generate deposit funds in their own accounts.

Beginning in April 2017, the reserve fund will be deposited by the depository bank on behalf of the payment institution into the central bank. In 2018, the reserve fund of third-party payment institutions will be directly deposited into the central bank by 100%. Because the central bank temporarily does not pay interest on reserves, payment institutions cannot collect interest on reserves. In addition, neither commercial banks nor third-party payment institutions have the right to use the funds in the centralized deposit account, nor can they divert funds for investment and gain.

Appendix 2-Derivation of Currency Multiplier after DCEP Promotion

The text analyzes the impact of DCEP on the composition of the base currency and the total supply of money. The conclusion can also be quantitatively described by Friedman-Kagan's currency multiplier theory. The derivation of the money supply can be divided into two steps.

First, it is assumed that the base currency is unchanged, and that the four sub-items of the base currency as a percentage of the deposit remain stable, and the multiple relationship between the money supply and the base currency is analyzed. It can be seen from the formula that the currency multiplier is inversely related to the cash withdrawal rate c, the DCEP withdrawal rate p, the reserve withdrawal rate f, and the reserve rate r.

Second, rewrite the relationship between the base money and the money supply. It is easy to see that the money supply is directly proportional to the base currency and inversely proportional to the various determinants of the multiplier.

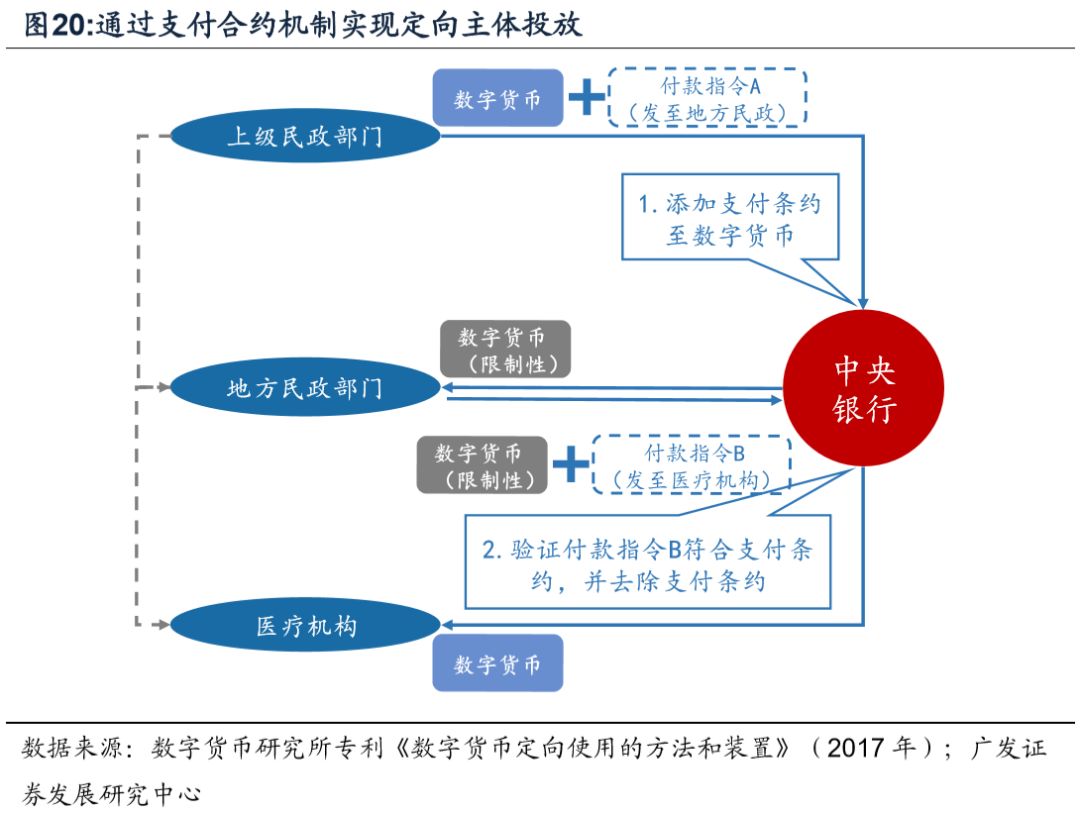

Appendix 3-Using Payment Contracts to Realize Funding under the DCEP System

Under the DCEP system, targeted funding can be achieved through "payment contracts". Take a specific case in the patent of the central bank, where the higher civil affairs department allocates funds to local medical institutions as an example [24]. The whole process is roughly divided into two steps:

In the first step, the superiors allocate funds to lower-level departments. First, the higher-level civil affairs department sends digital currency to the local department, and at the same time attaches conditions to the payment instruction, requiring that the funds must be paid to the local medical institution next time. Subsequently, the central bank added additional conditions to the DCEP after receiving the digital currency and payment instructions. In the end, the central bank sent this batch of conditional digital currencies to the local civil affairs department.

In the second step, subordinates deliver funds to specific objects. Local civil affairs departments transfer funds to beneficiaries and send digital currencies and instructions to the central bank. After the central bank receives the digital currency and payment instructions, the central bank immediately checks whether the payment object is consistent with the additional conditions. If the payee is indeed the required "local medical institution", clear the application extension field on the original digital currency and send the digital currency to the medical institution. Medical institutions receive unconditional digital currency, and their subsequent payers are not restricted.

From this example, it can be seen that monetary policy can use the DCEP feature to achieve a “directional” investment function similar to fiscal policy, so that monetary policy can obtain a stronger structural control function and better achieve fairness in the allocation of monetary resources.

[1] According to the classification of the "Overall Situation of the Payment System Operation" of the central bank, starting from the second quarter of 2018, the data of bar code payment business of brick-and-mortar merchants was adjusted from online payment to bank card acquisition for statistics.

[2] Sesame Credit Website Personal Credit-Sesame, https://www.xin.xin/#/detail/1-2

[3] Fan Yifei, "Several Considerations on Central Bank Digital Currency" (January 25, 2018)

[4] Yi Gang, speech at the first press conference of the Press Center to celebrate the 70th anniversary of the founding of New China (September 24, 2019)

[5] Printed the patent of the Institute of Science and Technology, "Methods and Systems for Payment of Digital Currency" (2016)

[6] Patent printed by the Institute of Science and Technology, "Method and System for Payment of Digital Currency Using Visual Digital Currency Chip Card" (2016)

[7] Printed the patent of the Institute of Science and Technology, "Methods and Systems for Payment of Digital Currency" (2016)

[8] The balance sheet data of the central bank in November 2019.

[9] China Banking Regulatory Commission, Interim Provisions on Intermediate Business of Commercial Banks (2002)

[10] Of course, the factors that reduce the statutory reserve ratio will also affect the composition of the base currency.

[11] Mu Changchun proposed at the third "China Finance Forty People Yichun Forum" that "Because the digital currency of the People's Bank of China is a replacement for M0, interest is not paid on cash and it will not cause financial separation. Media will not have a big impact on the existing real economy. " (August 10, 2019)

[12] Patent of the Digital Currency Research Institute, "A Method and System for Settling Banks Using Digital Currency" (2017)

[13] Patent of Digital Currency Research Institute, "Binding Method and Binding System for Digital Currency Wallet" (2017)

[14] Yao Qian, "Electronic Banking from the Perspective of Digital Currency" (2017)

[15] Fan Yifei and other central bank officials have emphasized on different occasions that in order to avoid the phenomenon of bank deposit disintermediation, there is a high probability that the central bank's currency will not carry interest (ie, give a positive interest rate) in the future. This article discusses the central bank's digital currency interest calculation operation, based on pure logical analysis and derivation.

[16] Yao Qian, "Experimental Research on Digital Currency Prototype System of Central Bank" (2018)

[17] Patent of the Digital Currency Research Institute, "Digital Currency Management Method and System Triggered by the Condition of the Main Stream" (2018)

[18] Patent of the Digital Currency Research Institute, "Methods and Systems for Digital Currency Management Triggered by Loan Interest Conditions" (2018)

[19] Patent of the Digital Currency Research Institute, "Methods and Systems for Digital Currency Management Based on Temporal Conditions" (2018)

[20] Patent of Institute of Digital Currency, "Methods and System for Digital Currency Management Triggered by Economic Conditions" (2018)

[21] Yao Qian, "Optimization of Fiat Digital Currency to the Current Currency System and Its Issuance Design" (2018)

[22] Zhou Xiaochuan, Speech at the Press Conference of the Fifth Session of the Twelfth National People's Congress (March 10, 2017)

[23] People's Bank of China, China's Financial Stability Report 2019

[24] Patent of Digital Currency Research Institute "Method and Device for Directed Use of Digital Currency" (2017)

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Japanese retail giant Rakuten announces allowing users to use points for bitcoin, etc., boosting cryptocurrency adoption

- The world after the Bitcoin inflection point

- Du Xiaoman Releases DeFi White Paper

- Research: 10% Bitcoin allocation in portfolio, which outperforms traditional asset portfolios

- Regulatory review: new US crypto bill, proposal to unify Muslim cryptocurrencies, European Central Bank's European chain

- Lenovo Group Blockchain Puzzle

- Everbright and Zhongying interconnected and blew up, exploding A-share "currency-related" companies