When the insurance industry encounters blockchain

Insurance broker's troubles

Xiaobian's friend H, a veteran insurance broker, specializes in helping clients configure insurance products for various insurance companies in China. H often spoke to me about his work: every time I help my clients, I want to find a lot of health information, including medical reports, cases, medical check-ups, relevant documents for hospitalization, etc. Check the customer's health status, compare the terms of each insurance product, and then determine which insurance policy the customer meets; each customer's health status is different, so the preparation before the insurance is very complicated, if the customer's health Or the occupation does not meet the conditions, and it is impossible to successfully insure. It is hard to please. These customer information is much more obvious, and they are becoming doctors. Every time I hear him say this, I will think that if the blockchain technology can be implemented in the insurance industry as soon as possible, the efficiency of insurance brokers will be greatly improved, and the operation of insurance companies will be greatly improved.

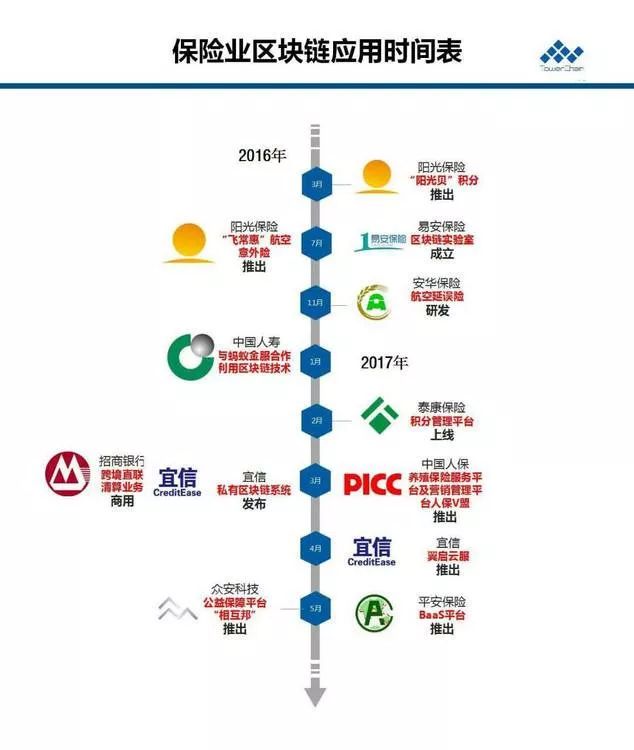

In fact, blockchain technology should be applied in the financial field. In addition to payment, insurance is the most promising. Since 2016, a number of insurance companies including China Ping An, Sunshine Insurance, Zhong An Insurance, Minsheng Life Insurance, Taikang Insurance, etc. have already entered the blockchain field for layout. From the characteristics of the insurance industry and the advantages of blockchain technology, the combination of the two can promote the development of the insurance industry. Blockchain technology will promote the insurance industry in terms of integrating resources, information storage on the chain, risk control and intelligent claims. development of.

- Blockchain Industry Weekly: Total market capitalization fell 2.11% from last week, 70% of the top 100 projects fell to varying degrees

- Mars Finance "POW'ER 2019 Global Developer Conference" was successfully held in Beijing

- After the cross-chain, where is the next vent of the blockchain?

Three major pain points in the insurance industry

Reverse risk selection. The premise of commercial insurance to provide people with protection is that the loss ratio is controllable, and the insurance company screens qualified target customers through the insurance notice. The insurance notice is mainly for health notification and occupational notification. The customer must read the notice before applying for insurance. If the health status is uncertain, the insurance company should be informed truthfully, and the insurance company can only be insured if its own conditions meet the content of the notice. For many people who are unfamiliar with insurance, the notice seems to be just like the product manual. In fact, the customer is the best channel for the insurance company to understand the customer. The health of the customer or the occupation does not meet the insurance conditions. There will be several situations: 1 the customer gives up the insurance, 2 the customer informs the insurance company about the situation, 3 the customer conceals The situation is insured. The insurance company will carry out a nuclear insurance notice for the customers who have been informed, and the result is nothing more than deferred underwriting, increased premium coverage or refusal. For customers who conceal the real situation, it is more difficult to deal with. Many insurance companies will not carry out strict underwriting when the customer is insured, and will conduct detailed insurance investigation when the client applies for claims. Once these reverse-selected customers request claims, they are often rejected by the insurance company, resulting in tight relationship between the insurance company and the customer, and disputes. Moreover, some policyholders will obtain the upper limit of the law theorem by repeatedly insuring accident insurance and life insurance. The total amount of insurance, and then deliberately create an accident to swindle, which is very bad. Customer adverse selection actually increases the operating costs of the insurance company and brings a lot of potential risks.

Invalid customer information. Insurance companies rely heavily on citizens' medical information for the underwriting of health insurance products, which are stored in hospitals. According to domestic laws, hospitals must keep 15 years of outpatient medical records, and hospitalized cases must be kept for 30 years, and all must be electronically archived for people to inquire. Even so, it is very troublesome for insurance companies to inquire about this information. There are a large number of hospitals in the country, and there are more than 1,300 hospitals in the light. In order to protect the privacy of patients, case information is not shared between hospitals. Therefore, insurance companies need to These hospitals cooperate to access medical information; when it comes to claims, the hospital sometimes asks the insurance company to obtain the authorization of the customer to access the customer's medical information. At present, only some large insurance companies have the strength to reach in-depth cooperation with major hospitals in China, and small and medium-sized insurance companies are still difficult to achieve. Not only medical information, but also the professional information provided by the user when insured accident insurance is mainly based on the user's truthful filling and notification. It is difficult for the insurance company to verify during the underwriting phase.

There are obstacles to information sharing between peers. For insurance companies, their customers will not share customer information. However, due to the consideration of underwriting, insurance companies actually need the exchange of customer information. Generally speaking, insurance companies are not covered by customers who are refused insurance by other insurance companies. For example, if a customer is insured by insurance company A and is insured by insurance company A for health reasons, then he is insured at insurance company B. B will not be covered by similar heavy-duty insurance products. If the customer does not tell the truth, the insurance company is not easy to find, so it is very important for the insurance company to communicate with each other. There are some informal information exchange channels between the insurance companies, but obviously this is not enough.

“Blockchain+Insurance” addresses industry pain points

The pain point of the insurance industry is fundamentally a matter of information asymmetry, which makes the overall operational efficiency of the insurance industry low, and the shared information necessary for the industry has conflicts with the privacy of customers and the vested interests of the organization. If the blockchain technology is used, the contradiction will be solved. We can make such an idea for the blockchain enabling insurance industry:

A chain of alliances is established within the insurance industry. The Banking Insurance Regulatory Commission and all insurance companies are nodes on the chain. The key information of all policyholders, insured and beneficiaries is stored in an encrypted manner on the chain. And can't be tampered with, customer privacy can be guaranteed. All nodes can query the customer's policy status, underwriting and claims information, and blockchain technology can prevent the function of anti-counterfeiting. The insurance company can understand the customer's underwriting claims in other companies without touching the customer's key information. Happening. Insurance companies have mastered more customer information through the alliance chain, which is convenient for their own underwriting, can effectively avoid over-insurance of customers, or fail to inform the truth. Blockchain technology can well solve the dilemma of information asymmetry between insurance companies, insurance companies and customers. As a customer, you can also check your policy status and claim status on the chain with the authorization of the insurance company.

The information exchange between insurance companies and medical institutions and enterprises is a key link in the operation of insurance companies. The insiders have proposed to store all the medical information stored in the hospitals on the chain, and to share information under the premise of protecting patient privacy. However, it is a huge project for medical institutions across the country to store all patient medical records in a high-volume project, and the cost of deployment will be very high. However, if the insurance industry alliance is the leading factor to grasp the customer's medical information and career information from the bottom up, it will save costs while realizing the storage in the customer information chain. In the work, the insurance company can input the medical information and occupation information required by the customer during underwriting and claim settlement into the alliance chain, so that other nodes in the chain can obtain the information directly in the chain when querying the customer information, thereby effectively Reduce the cost of underwriting. When a customer has repeatedly insured or made multiple claims, the insurance company can review the previous underwriting and claims records and re-submit the new underwriting or claims records to the chain. In the case of authorization, insurance brokers can also record information about potential customers into the insurance industry alliance chain. Over time, customer information on the alliance chain will continue to expand and become a huge customer information base. The insurance company collects medical information and occupational information according to the customer's situation from bottom to top, and then carries out chain encryption storage to realize sharing in the industry. Under the premise of protecting user privacy and controlling costs, the insurance company's operational efficiency is effectively improved. The best channel for future insurance companies to know customers may no longer be insurance notices, but industry alliance chains.

Through the above measures, blockchain technology can solve the three major pain points of the insurance industry to a large extent. At present, domestic insurance companies are still in the process of blockchain technology, competing for the situation of rivers and lakes, and foreign counterparts have begun to form alliances in the blockchain field. Insurance giants Allianz, Swiss Re and Zurich Insurance jointly launched the blockchain industry alliance B3i to solve the problems of inefficiency, value loss and credit risk in the traditional insurance industry. At present, the insurance company members of the alliance chain have already There are 18 homes.

The domestic regulatory authorities also want to solve the dilemma of information asymmetry in the insurance industry. Starting from 2018, the Banking Regulatory Commission has begun to implement a unified policy registration platform to record all policy information of all insurance companies nationwide. However, the user information recorded on the policy platform is very limited, and does not involve the customer's medical information and career information; in order to achieve comprehensive, secure, encrypted, and interest-segregated user information sharing in the industry, only the block can be used. Chain technology to achieve. The blockchain technology empowers the insurance industry not only to solve the problem of information asymmetry, but also to use the intelligent contract function of the blockchain. The insurance company can also intelligentize the underwriting and claims, and gradually realize the automatic operation; the information flow on the alliance chain can also be Help insurance companies and reinsurance companies reduce the cost of information exchange between the two parties, and improve the efficiency of the compensation and risk transfer. It is believed that in the future, with the continuous development of blockchain technology and decentralized finance (DeFi), “blockchain+insurance” will be the future development direction of the future insurance industry.

At that time, Xiaobian's friend H will no longer have a headache for dealing with customer information. What he has to do is to search in the insurance industry's alliance chain, so easy!

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- IDC Report: Blockchain solution spending will reach $15.9 billion by 2023

- What happened to the blockchain game "Encryption Cat" that used to be a smash hit?

- DEX is in a rush, and the competition with the centralized exchange is bound to win?

- Korea develops a blockchain-based unlisted securities trading platform, with the participation of the Korea Stock Exchange

- License Chain vs. Public Chain: The "Best Rule" for Local and Global Digital Securities

- Ethereum's smart contracts exceed 200,000, ranking the dominant position in the Defi ecosystem

- Technical Perspectives | Information Value and Identity System in the Blockchain World