Institutional running into the blockchain: Who are, what, what is the impact?

One of the most mentioned words this year should be the institution's entry. Everyone has already heard the news of many institutions entering the market, including asset management agencies, investment banks, social giants, etc., big and small can really be said to be a lot. Different institutions have different appeals and different purposes.

Which institutions have entered the market and why are they coming in? Is it a threat, is it afraid to miss it, or is it a trend? And what the institutions do.

Institutions have the advantages of resources, talents, and technology. Understanding their trends is of great benefit to us in understanding the encryption industry. This article will take you through the dynamics of the US institutions in the technology sector.

- Who is competing for C? Read the encrypted payment contest

- How to design a self-adjusting consensus agreement?

- Market Analysis: Bitcoin starts to oscillate, funds back to the altcoin

(The media reports on a small part of the "Institutional Admission" headline)

In the blockchain/encryption industry, in 2019, it can be said that the year of "institutional approach".

Although institutions are often cited as catalysts in the field of encryption, its entry has been slow. After all, these are large organizations with significant risk values, so they want to be cautious in accepting new innovations and opportunities.

However, we finally saw the real power from traditional technology and financial institutions – Square, Microsoft, Fidelity and Facebook are all announcing their entry into this field.

It is undeniable that institutions and companies have entered the market two years after the last encryption of the bull market. But why did they choose now? What does this mean for the future?

First, afraid to miss

From a high-level perspective, there are several reasons why organizations are seeking to enter the blockchain: research and development, growth opportunities, and in many cases, FOMO (fear of missing).

For many organizations, they are researching and developing to understand the technology and gain a view of the landscape as a whole. As more and more companies decide to experiment in this area and seek early growth and income opportunities and resist devastating risks, the competitive pressures of institutions have increased dramatically.

In addition, innovation within large enterprises is an important part of retaining talent, as more and more talents leave Wall Street and become the technical role of encryption startups.

We are also witnessing large-scale demographic changes in the financial services sector. Financial institutions are currently serving an ageing customer base and, in many cases, trying to capture the mindset and wallet share of younger, more tech-savvy customers. In order to understand these demographics, cryptographic assets are a trend that deserves attention.

FOMO is the main reason – no one wants to "miss this boat", which could be a huge growth opportunity, or ignoring it may put risks on their business model. This has also led to a well-thought-out analysis of the field, as well as some so-called “innovation theaters” – to use “blockchains”.

More and more institutions are accepting this area, which will bring positive factors to the industry. However, when we move from the pilot phase and the POC (proof-of-concepts) phase to serious implementation, products and services, the details are important.

Moreover, as an industry, it is important to encourage the best use cases for the adoption of the technology, rather than simply creating a new internal database.

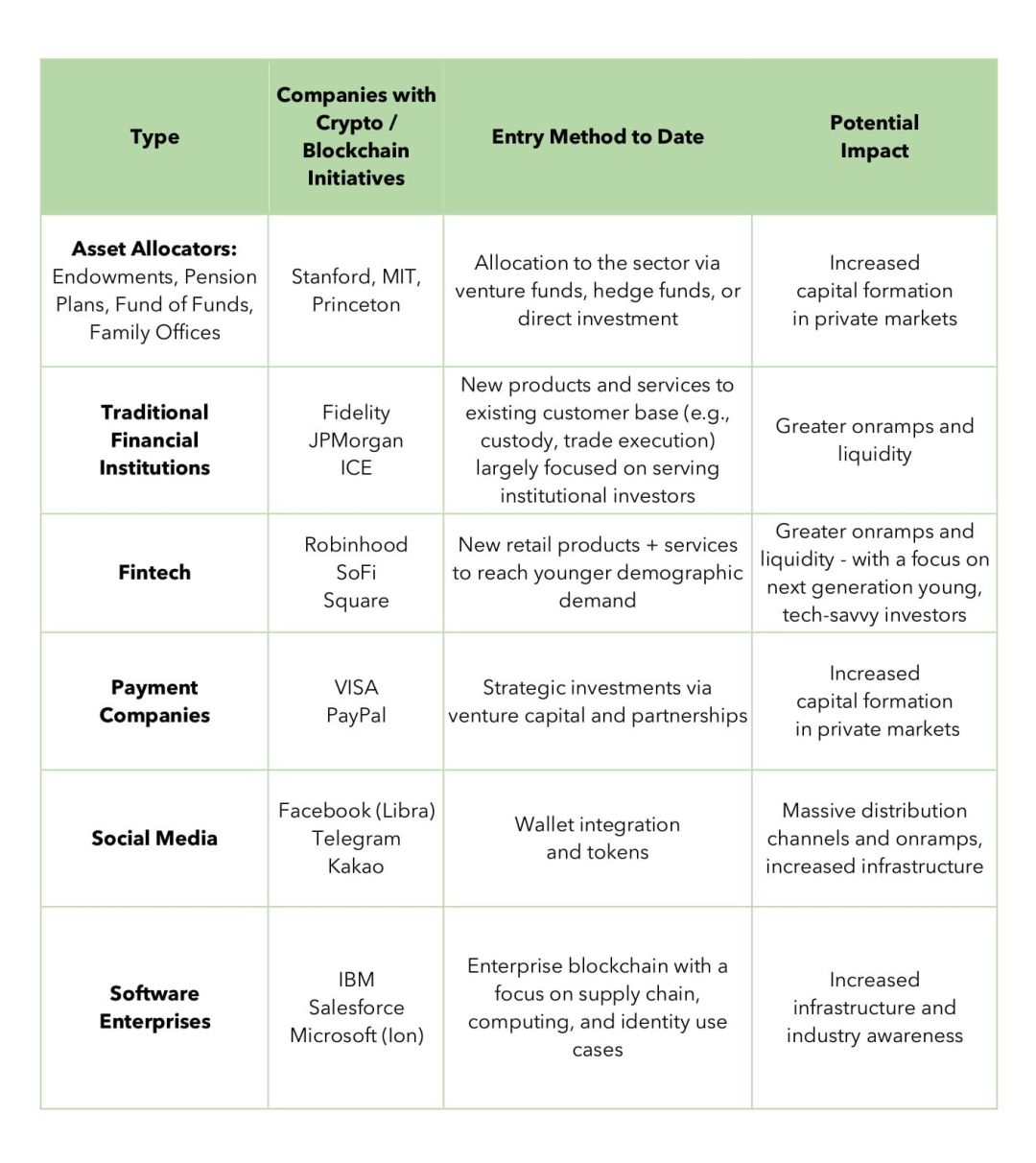

2. Who are these institutions?

The term agency is too broad—actually, we see many types of companies entering the field. For the sake of simplicity, the table below mainly classifies institutions and businesses in the United States. It is not comprehensive, it is more representative.

Although we have a large number of players entering this field, they cannot be treated equally. Instead, these organizations either have a far-reaching impact as “innovation projects” or remain isolated.

To understand the underlying outcomes, we considered their existing customer base, the market trends and risk tolerance they face, and the talent within these organizations, how these talents shape the internal perspective of encryption.

Asset allocation

Investment role: fund, family office, endowment fund, pension plan

Investment forms: venture funds, hedge funds and direct investment

Example: Stanford, Massachusetts Institute of Technology, Princeton University

As crypto assets become a new asset class, asset distributors have to think around the entire technology and domain.

Cambridge Associates recently released their report "Venture into the Unknown", which evaluated the cryptographic asset allocation strategy and advised investors to consider configuring digital assets.

Their advice stems from the belief that blockchain investments can be compared to early Internet investments, filled with young, risky technologies that could ultimately spur the next round of capital inflows.

From an asset configurator's perspective, investment in the industry begins to play an important diversification role in its portfolio strategy. Considerations include: which type of investment is appropriate for its strategy (eg, venture capital and hedging), the type of investment manager (emerging professional or life commissioner), and the liquidity status of the asset class (with higher token liquidity, But there is no initial public offering).

Since the bull market in 2017, the agency's dedicated cryptographic venture capital and hedge funds have raised more than $1 billion (Blockchain Capital $150 million, A16z $300 million, Paradigm $400 million, Dragonfly $100 million, etc.). Asset allocation is an important indicator of market growth and the rate of capital formation in any new industry.

Traditional financial institution

Investment role: custodian, exchange, broker, asset manager and bank

Investment form: trade and execution services, custody, over-the-counter OTC

Example: Fidelity, ICE (Bakkt), JPMorgan, DRW

Traditional financial institutions are cautiously observing this area, with some institutions ignoring and others tending to enter this field.

Until recently, many cryptographic assets pose serious threats and opportunities for existing businesses in traditional institutions. Regardless of their status, it is almost a strategic surveillance area within every financial services organization.

Historically, financial services have been slow to respond to the digitalization that prevails in other industries.

However, with the rise of online robotics consultants and digital banking, financial technology has begun to erode the products and pricing strategies of traditional institutions. These institutions are facing similar trends: an ageing investor base, compression of all product and service costs, reduced brand loyalty in millennials, outdated infrastructure, and increased customer demand for more cryptographic education and access.

From a strategic plan, organizations are always looking for opportunities to diversify their sources of income through large growth markets and high-margin products. This requires a balance between risk tolerance and the ability to make quick decisions and leverage existing infrastructure to adapt to the market.

As Matt Walsh, a partner at Castle Island Ventures, said, the best institutions will cut into the “Innovation Theatre” and really try to understand how they use it.

On the one hand, institutions like Fidelity have an in-depth understanding of the entire ecosystem (mining, trade execution, regulation, etc.) and take steps to provide regulatory and final execution services.

On the other hand, tokens issued by companies like JPMorgan Chase are more conservative, and they enter the field by creating internal tools for POC, rather than generating revenue-generating or customer-facing products.

Financial Technology Fintech

Investment role: technology-focused, financial service provider

Investment form: brokerage services, portfolio management

Example: Robinhood,Square,SoFi

Fintech maintains a good relationship with encryption technology — both have a common goal of using technology to reach people who are unable to use the bank, as well as products that are cheaper and more accessible. This overlaps with the demographics of young, tech-savvy, and financially inferior consumers. This background, combined with lightweight operations and an updated technology infrastructure, makes it very capable for financial technology companies to capture cryptographic benefits.

Initially, we saw brokerage products like Robinhood and POS systems like Square entered the field for the first time. In fact, Square's latest annual earnings report shows that they received $166 million in revenue from Bitcoin in 2019, with a net profit of $1.69 million.

The motivation here is not to subvert, but to focus more on how to use technology and assets to stimulate new growth and meet customer needs.

Payment company

Investment role: credit card company, payment processor, remittance service

Form of investment: strategic investment through venture capital and partners

Example: VISA, PayPal

Paying or becoming a "transaction medium" is one of the original use cases of encryption algorithms.

Over time, we have realized that the payment channels in most developed countries actually work very well and may not be able to introduce cryptocurrencies for some reason.

The most frequently criticized (encrypted payment) is the traditional size problem, for example, the blockchain cannot handle the scale of the millions of transactions that Visa handles.

More importantly, however, the extra friction of converting from legal currency to cryptocurrency and then converting it to French currency (called the “last mile problem”) on the other side of cross-border remittances is largely beyond today’s encryption. Handle any value brought by the payment.

Of course, in one scenario, crypto-payments start to make more sense, that is, people hold digital assets separately and are able to trade more freely.

At this point, one of the main issues that payment companies need to consider is how the macro trends in holding and trading digital assets affect their business models. In other words, how their existing customers will use digital assets in the future and how this will affect their market.

Some scenarios include: Consumers often use multiple digital wallets, conduct business in French and cryptocurrencies, or choose to self-serve some or all of their digital assets.

So far, payment companies have been slow to respond to the potential of cryptocurrency. However, if these macro trends accelerate, it will not be surprising that many agencies will significantly increase their participation after identifying appropriate opportunities.

social media

Investment role: communication app, social network

Investment form: wallet infrastructure, token

Example: Facebook Libra, Telegram, Kakao

The overlap between social media and cryptographic assets is one of the most noteworthy trends today.

There are two angles to think about this.

First, from an encryption perspective to a social media platform. In terms of encryption, the adoption of digital assets by social media has the potential to open up distribution channels on a large scale globally. This is important for attracting new users, building infrastructure, and spreading acceptance and awareness.

Facebook's Libra is not seen as a competitor to Bitcoin, but rather as a portal for more users to adopt Bitcoin.

The second perspective is how the adoption of digital assets will change the social media business model. Social media platforms are shifting from sharing user-generated information to providing user-generated products and services.

Instagram has built social media businesses and its latest in-app purchases with thousands of influencers.

With the launch of Libra, Facebook is aggressively developing financial services to complement its vast advertising technology business.

Similar to how direct social messaging or “DM-ing” competes with Millennials e-mail, will social media digital wallets compete with brokers and banks around the world?

On the other hand, social media giants represent what the encrypted missionaries are trying to object to (ie, centralized monopolies): centralized power, unequal access to consumer data, and privacy controls. Therefore, the way social media companies accept encryption will be very important.

If successful, it can move the model from a centralized power to an open platform, providing users with greater privacy protection.

Software company

Investment role: SaaS, infrastructure

Investment form: enterprise blockchain, supply chain use case, identity authentication

Example: Microsoft, Salesforce, IBM, Amazon

Software companies have traditionally fallen into the trap of innovation.

From their perspective, they are trying to understand how public and private chains are useful for their business model. In many cases, this has led to the application of private-chain POCs, and that's it.

However, the use of technology in this area (and other technologies such as artificial intelligence and machine learning) as a way to maintain competitiveness and relevance is actually a lot of pressure.

Microsoft is a good example. It announced a bitcoin-based distributed identification tool.

I hope that the industry can see such a plan to work with the open source community and understand the app of the public agreement, rather than focusing on the closed private chain.

3. Where are we going?

There are a large number of institutions that are entering the field of encryption, and each organization has its own perspective and value proposition.

The industry has seen more than $1 billion in allocations to dedicated crypto funds, which will stimulate the next wave of startups and capital formation in the field.

As more and more organizations enter, we will see more liquidity and online large-scale distribution channels and utilities-focused products and services.

Perhaps most importantly, professionals within these organizations will be forced to understand the field and debate and learn about its strengths. This will transform the blockchain and cryptocurrency from the buzzword and POC stages into truly understood and incorporated into the strategic product roadmap.

This area is slowly entering the mainstream, and as projects like Libra continue to roll out, more institutions will be involved.

Thanks to Spencer Bogart, Derek Hsue, Aleks Larsen for their helpful feedback.

-END-

Author: Noelle Acheson

Translation: Aile Bull, a special author of the Blockchain Learning Society.

Disclaimer: This article is the independent view of the author and does not represent the position of the blockchain study (public), nor does it constitute any investment advice or suggestion.

Source: https://medium.com/@kinjalbshah/institutions-have-arrived-who-what-and-why-920f00fc00e8

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- "Moving brick arbitrage" scam reappears, a user is deceived 885 ETH

- Analysis of the Internal Relationship between Facebook Libra Project and Sino-US Trade Friction and Coping Strategies

- On June 23, the market analysis continued to touch the bitcoin, and the heavy pressure zone on the top was difficult!

- Looking back at the four bull markets that Bitcoin has experienced, the major lessons that are worth learning

- Staking: The new wave of mining in the PoS era, value investment or the correct way to open

- Market Analysis: BTC is blocked at $11,200, and the risk of short-term retracement increases

- Early comments: BTC broke the million yuan shock adjustment, BCH led the show to lead the mainstream currency