A hundred years of loneliness – the magical realism of the renminbi

Overview Overview

Viewpoint 1 The contradiction between the subordinate status of the renminbi and the sustained growth of high economic growth and liquidity has exerted tremendous pressure on the normal operation of China's economy and macroeconomic regulation. Therefore, China has begun to work hard to make the renminbi “go out”.

Viewpoint 2 Although the SDR and “Belt and Road” attempts are forward-looking and strategic, renminbi payments and settlements under the SWIFT system are still not autonomy. Therefore, the central bank's move to issue digital currency may make DCEP a sword for the internationalization of the RMB and play a major role in the battlefield of RMB internationalization.

Report report

According to the Shenzhen Business Daily on the 17th, the digital currency developed by the People's Bank of China has begun to enter the closed-loop test phase, and China's digital currency is on the verge of coming. In response to this news, the central bank did not respond today. However, the relevant person in charge of the central bank has previously stated that the central bank's digital currency will be very different from electronic payment in some functions, and the final digital currency will be optimized through competition. According to the information disclosed publicly, the central bank's digital currency is likely to be born in Shenzhen, a demonstration area for reform and opening up. Whenever it goes online, the landing of the central bank’s digital currency is already on the nail.

At present, there are roughly three speculations about the structure and implementation of the central bank's cryptocurrency (DCEP).

First, the central bank directly provides deposit accounts to the public and issues a digital token that can be stored in a digital wallet (similar to existing cryptocurrencies). The central bank plays the role of a commercial bank, and the public can trade and hold the central bank's debt.

- Babbitt column | People may be wrong in the search for blockchain 3.0

- The market is getting colder, the exchanges are getting stronger and stronger, and the bulls and bears are unimpeded. I am waiting for you in Wuzhen.

- Mining from entry to mastery (3): POW mining logic process

Second, the central bank can also choose to provide reserve accounts to all financial institutions, giving them DCEP's transaction payment rights. Financial institutions will be responsible for agency work such as KYC and data management. This model is not without precedent. China requires payment providers (such as WeChat Pay) to hold their clients' funds in the central bank. In the future, these services can be further extended to DCEP.

Third, the central bank stipulates that commercial bank assets must be fully supported by central bank reserves (in this case, that is, all reserves of DCEP instead of cash notes). This model is more radical and some banking operations have been removed, helping to reduce systemic risk. To ensure that commercial banks are profitable, the central bank can allow them to continue to provide credit services by lending DCEP to other customers.

The author summarizes these three suggestions into three areas: circulation, payment, and borrowing. Regardless of the final, due to the characteristics of the Chinese economy, DCEP will eventually become a sword for the internationalization of the RMB, playing a major role in the battlefield of RMB internationalization.

The difficult internationalization of the renminbi

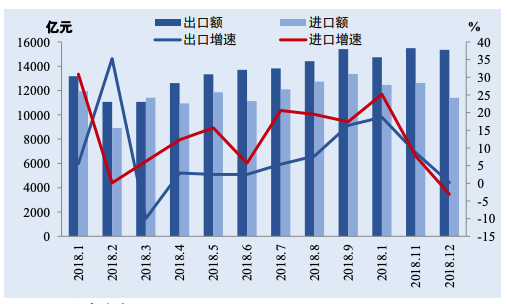

Regardless of whether it is trade or currency, China has never given up its efforts in internationalization. China has become a big country with important economic status in the world. At present, China's total economic output is already the second in the world, and the import and export trade is the second in the world. But before the RMB joined the SDR on October 1, 2016, the international pricing system and credit payment. There is no shadow of the renminbi at all in the system. The real economic power, its currency must be an international currency, and violation of the law will lead to an increasingly large economic dilemma. In 2018, the total import and export volume of China's goods trade was 30.5 trillion yuan, an increase of 9.7% over 2017. Among them, exports were 16.4 trillion yuan, up 7.1%; imports were 14.1 trillion yuan, up 12.9%; trade surplus was 2.3 trillion yuan, narrowing 18.3%. The total volume of imports and exports, total exports, and total imports all reached record highs throughout the year.

China's monthly import and export scale and growth rate in 2018

Source: China's Foreign Trade Situation Report

Source: China's Foreign Trade Situation Report

The internationalization of the renminbi is first of all to get rid of the subordinate status of the entire national economy caused by small currencies; the second is to strive for the international monetary and financial discourse rights and autonomy that are compatible with the size and economic nature of the country's economy. And if China wants to gain the right to speak and autonomy, it will certainly hinder the vested interests, so the road to internationalization of the renminbi is not smooth.

The history of RMB internationalization

To understand the trend of China's economic development, the most important thing to understand is why China will embark on an economic growth mode that is increasingly dependent on foreign countries.

In the early days of reform and opening up, New China was still a low-level economic country. "Insufficient effective demand" is a bottleneck for economic development. If this problem is not solved, it will not be possible to get rid of the state of backward economic development at that time. The state has decided that to achieve rapid economic growth, it must turn its attention to the overseas market.

After the Second World War, the rapid rise of Japan and West Germany gave people great inspiration. In the process of their rise, external demand played an important role in making up for the lack of domestic demand. Then the four small dragons in Asia followed the success to verify a rule. Export substitution (that is, increase of external demand) is an effective way to quickly get rid of the lack of domestic demand in low-level economic countries based on market economy. After China entered the market economy, it also encountered the problem of insufficient effective demand for the first time in 1997. Then it joined the WTO and solved the economic growth of low-level economy through external demand. Therefore, China is running with heavy dependence on external demand. The structure came to the entrance of the economic power.

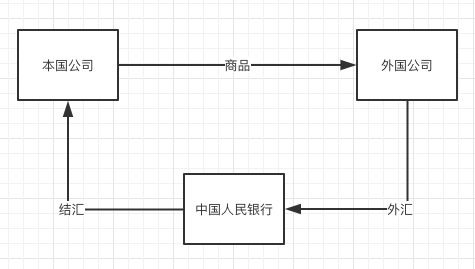

When relying on external demand to solve the bottleneck of economic growth in the low-level period, after the economy enters the path of high growth, the contradiction between high economic growth and continuous expansion of liquidity arises. China's continued balance of payments surplus has led to continued capital input, causing serious import inflation. This is the current basic background of the Chinese economy and the root cause of all problems. Most of the foreign exchange inflows are to be settled (previously the mandatory foreign exchange settlement system). Changes in foreign exchange reserves can effectively affect the changes in the central bank's base currency, which is an important channel affecting the domestic money supply. It reflects the increase in the base currency of the central bank through the foreign exchange channel.

Source: Economics and Management Research (2010, Issue 3)

Source: Economics and Management Research (2010, Issue 3)

These money supply increases due to the increase in foreign exchange, there is no corresponding product. Foreign exchange with increased trade surplus is because the export of products is greater than imports, so the increased local currency (ie RMB) has no corresponding products in the domestic market.

This kind of passive and unrealistic counterpart product currency is a typical manifestation of the subordinate status of the currency. It has exerted tremendous pressure on the normal operation of the Chinese economy and macroeconomic regulation and control. Therefore, only by continuously compressing liquidity can the normal macroeconomic environment be maintained. Therefore, the central bank's efforts to hedge the liquidity of the renminbi continue to increase. But the fundamental problem is not the People's Bank of China, but the continued surplus. Input inflation is entirely caused by external factors. Obviously, the state has realized that this high foreign exchange share will have a serious impact on the domestic economy and gradually begin to solve this problem.

Foreign exchange settlement transaction process

Source: Standard Consensus

Source: Standard Consensus

Obviously, the small-currency economy has put China in a dilemma: in the case that China’s economy is highly dependent on external demand, if it wants to maintain rapid economic growth, it will inevitably continue to have a double surplus, and the pressure of imported inflation will become greater and greater. Input inflation will lead to asset price inflation and price increases; under increasingly serious import inflation, fiscal policy will inevitably adopt more and more austerity measures due to its lag, and look at it with historical perspective. “Reducing capacity by reducing credit is undoubtedly a typical austerity policy. To a certain extent, this kind of policy will lead to a slowdown in economic growth. In order to stimulate the economy, fiscal policy will inevitably make a fuss about "looseness" and "pull domestic demand", but the same problem still exists and has not been resolved.

The idea behind the "difficult dilemma" is actually: on the one hand, it needs to "pull domestic demand"; on the other hand, it needs to "go out" to carry out the internationalization of the renminbi. Just like Dagu’s water control, “blocking is not as good as sparse”. Unblocking the financial channel of the RMB outflow rather than rejecting the inflow of foreign currency, it is in line with the contradictory solution between the big economy and the small currency.

The foundation of RMB internationalization

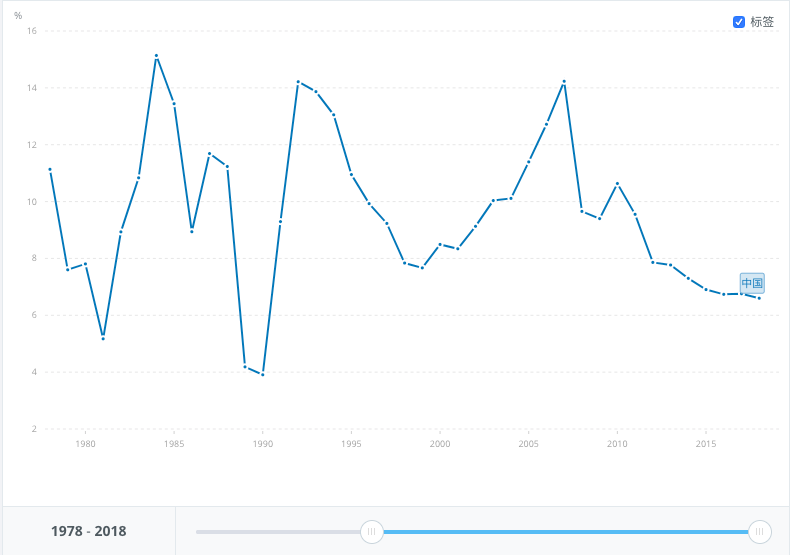

Whether a country's currency can become a world currency, and ultimately its decisive role is the country's comprehensive economic strength. The famous international economist Robert Mundell said that the key currency is provided by the most powerful economy, which is a fact of historical tradition. For the current comprehensive economic strength of China, we can use these figures to make a simple outline. First, in the past 30 years of reform and opening up, China’s annual average economic growth rate has been 9.5%, which is nearly three times the average annual economic growth rate of the same period. Second, by the end of 2018, China's GDP exceeded 90 trillion yuan, converted into a 1:7 conversion to US dollars, equivalent to 12.857 trillion US dollars, lower than the US 20.49 trillion US dollars, ranking second in the world. Third, China's foreign exchange reserves have reached 3.0727 trillion US dollars by 2018, ranking first in the world.

China's GDP growth rate since the reform and opening up

Source: World Bank

Source: World Bank

Since China has implemented the correct reform and opening up policy and the comprehensive economic strength has undergone significant changes, then the currency representing its overall economic value will soon become the world currency and occupy its proper position in the world currency pattern. It is said that the road that the major developed countries have traveled tells people a basic experience.

In the process of China's rapid economic growth, there is a clear feature that China's foreign economic exchanges and cooperation are developing at a faster rate than the domestic economy. In terms of US dollars, the total import and export of goods between China and China in 2018 was US$4.6 trillion, an increase of 12.6%. Among them, exports were 2.5 trillion US dollars, an increase of 9.9%; imports were 2.1 trillion US dollars, an increase of 15.8%. The trade surplus was 351.76 billion US dollars, narrowing 16.2%.

According to the statistics of the World Trade Organization (WTO), China’s exports of goods accounted for 12.8% of total global exports in 2018, which was the same as the previous year; the proportion of imports of goods to global total imports was 10.8%, an increase of 0.6 over the previous year. The percentage point is the highest level in history. In 2018, China's imports and exports to the top four trading partners EU, the United States, ASEAN, and Japan increased by 7.9%, 5.7%, 11.2%, and 5.4%, respectively, accounting for 48.3% of total imports and exports. Among them, exports to the EU, the US, ASEAN, and Japan increased by 7.0%, 8.6%, 11.3%, and 4.4%, respectively.

Source: China's Foreign Trade Situation Report

Source: China's Foreign Trade Situation Report

China is a typical export-oriented economy. As the trading medium of this huge export-oriented economy, the renminbi has received more and more attention from all over the world. If the size of a country's domestic economy is insufficient to prove the inevitability of its currency internationalization, then the size of a country's international economy and the degree of internationalization of trade will fully prove that its currency internationalization has a direct objective basis.

SDR and the One Belt One Road attempt

In order to solve this problem, the state has never given up the efforts of the internationalization of the renminbi. From the establishment of offshore renminbi bank accounts in 2004, to the 2009 cross-border trade renminbi settlement pilot and the signing of the “clearing agreement”, and the “Belt and Road” initiative, which was first proposed in 2013 and officially promoted in 2015, the internationalization of the renminbi is developing rapidly. .

“Belt and Road” is the abbreviation of “Silk Road Economic Belt” and “21st Century Maritime Silk Road”. In September and October 2013, China proposed the construction of “New Silk Road Economic Belt” and “21st Century Maritime Silk”. The road to the cooperative initiative. Relying on the existing dual and multilateral mechanisms of China and relevant countries, and with the existing and effective regional cooperation platform, the Belt and Road Initiative aims to borrow the historical symbols of the ancient Silk Road, hold high the banner of peaceful development, and actively develop with countries along the route. Economic partnership.

Through the regional trade cooperation, the Belt and Road Initiative uses RMB in trade links and the investment projects are settled in RMB, which creates conditions for the overseas export of RMB. In particular, through the investment in infrastructure in the Belt and Road countries, it has objectively stimulated the overseas demand of the renminbi. In the process of circulation, some of the RMB will be held by other countries in the form of foreign exchange reserves. Finally, the overseas RMB will flow back to China in the form of RMB investment and RMB bonds. This RMB, which is circulated through capital openness, will continue to deepen the degree of RMB internationalization.

The Belt and Road Initiative of RMB Internationalization

Source: Standard Consensus

Source: Standard Consensus

Although it is impossible to judge whether it is “One Belt and One Road”, SDR is still due to the slowdown of the world economy and the slowdown in foreign trade growth. However, it is clear that since 2013, the proportion of foreign exchange in China has been declining year by year, and foreign exchange accounts for 2018. Only 39% of the base currency.

Source: People's Bank of China

Source: People's Bank of China

According to the latest official foreign exchange reserve currency published by the IMF, the quarterly data of RMB foreign exchange reserves as of the fourth quarter of last year was approximately US$202.79 billion, accounting for 1.89% of the world's official foreign exchange reserve assets, accounting for 1.62% higher than the Australian dollar and Canadian dollars. 1.84%. In China-Africa trade, the settlement ratio of RMB has risen from 5% in 2015 to 11% in 2017. As China's cooperation with the Belt and Road countries deepens, the degree of internationalization of the RMB has also expanded.

Conclusion

This article is divided into two parts. The first part mainly discusses the problem of large economic small currency in China's economy, the history of RMB internationalization and the attempts of SDR and the Belt and Road. The next part focuses on the SWIFT and the central bank digital currency in the internationalization of RMB. Changes that may be brought about by the clearing and payment system of the RMB in the internationalization of the RMB.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- The first week of Bakkt: not warm, the future can be expected

- Popular Science | Eth2.0 Term Decryption

- Babbitt column | Payment or stored value? BTC's future value path

- Deep adjustment period of mining industry: Bitcoin's overall network computing power has changed rapidly in the short-term mining machine pattern

- Zcash masks address vulnerabilities or reveals full node IP address (with solution)

- About digital asset hosting services, you want to know are here.

- Who is the "Whampoa Military Academy" in the field of blockchain in China?