Analysis of the central bank's digital currency DCEP, which related companies are worth paying attention to?

Source: Huatai Computer Life

Editor's Note: The original title was "Analysis of the Central Bank's Digital Currency DCEP"

We believe that digital currency is another application of technology in the financial field. Moreover, at this time, the integration of IT technology with the financial business itself is more thorough . As a new thing, digital currency has attracted a lot of attention in the market, and everyone's concerns also come from various aspects. Our article is more about starting from the central bank digital currency DCEP to introduce the underlying architecture and operating principles of China's digital currency. The relevant industry chain links and beneficiaries may become clearer after the industry standards are further clarified.

1. The central bank's digital currency DCEP is gradually approaching

- Social influence: unique elements of the digital asset market structure

- CFTC Chairman: Global stablecoin is the only systemic risk

- Santander successfully redeems $ 20 million in bonds issued via Ethereum

At present, the central bank's digital currency is mainly used as a substitute for banknotes, which is a legal digital currency endorsed by the central bank . The issuance of digital currency by the central bank adopts a dual system of central bank and commercial bank, with a centralized management method to achieve controlled anonymity in the form of loosely coupled accounts . As the central bank's digital currency will adopt a centralized management system, we expect that the central bank's digital currency core system design will be based on self-development. However, since the operation will adopt a dual system of central bank and commercial bank, after the relevant technical standards and construction specifications are clarified, the settlement system and payment clearing machine of commercial banks are expected to usher in the need for upgrading. Relevant targets include: Changliang Technology, Hang Seng Electronics, Digital Authentication, Quartet Innovation. Suggested Attentions: Yuxin Technology, Runhe Software, Geer Software, Radio and Television Express, New World, Julong, Lakala.

2. DCEP operation framework: one currency, two banks, three centers

A currency refers to the legal digital currency endorsed and issued by the central bank. The two databases are a digital currency bank library and a digital currency issuance library, which are operated by the central bank and commercial banks, respectively . Among the three centers, the certification center is responsible for managing user information, the registration center is responsible for ownership registration and flow records, and the big data analysis center is responsible for processing and analyzing transaction data and providing data support for the implementation of macro policies.

3.DCEP core technology of central bank digital currency

Digital currency security technology guarantees the security and authenticity in digital currency transactions through technologies such as encryption and decryption technology, security chip technology, and anti-repeating transactions. Digital currency transaction technology provides online and offline two different technical solutions for each link of digital currency business, making transactions free from network conditions. As a platform interface, the trusted guarantee technology provides digital currency participants with various application-related services.

4. The top-level architecture of the central bank's digital currency system

The digital currency system consists of the central bank digital currency system, the commercial bank digital currency system, and the authentication system. It serves the six links of legal digital currency issuance, circulation, management, withdrawal, investment and financing, and interbank settlement. Among them, the central bank digital currency system is used for the generation, issue and ownership registration of digital currencies. Commercial bank digital currency systems are used to perform banking functions on digital currencies. The authentication system is used to provide authentication to the interaction between the central bank digital currency system and the terminal device and the commercial bank digital currency system.

5.Digital wallet may become the carrier of central bank digital currency

The central bank's digital currency can adopt a two-layer structure of a commercial implicit account system + digital currency wallet, which can realize the management of existing bank deposits and digital currency in one account . Digital wallets support dual offline payments, with a wider range of applications, and small retail may become high-frequency application scenarios. In order to strengthen supervision and prevent runs, it is expected that digital wallet transactions will set certain restrictions in accordance with current cash management regulations.

Risk reminder: Digital currency landing progress is less than expected; the application scale of the central bank's digital currency is less than expected

1.The central bank's digital currency is the digital form of RMB

Central bank digital currency mainly replaces M0

The central bank's digital currency DC / EP (Digital Currency Electronic Payment, hereinafter referred to as DCEP), issued by China's central bank endorsement, is the central bank's liability to the public . DCEP is a legally encrypted digital currency with unlimited legal compensation. It is a digital form of RMB and its essence is currency. Different from third-party payment platforms such as Alipay, DCEP aims to replace the currency in circulation, that is, M0, while electronic payment is based on the existing commercial bank account system, which digitizes M1 and M2. Its essence is a payment tool.

Central bank digital currencies are fundamentally different from digital currencies such as Bitcoin in terms of issuance methods, management models, and technical architecture. The legal digital currency is issued by the central bank and endorsed as a credit. Its value is linked to the RMB, which can adjust the total amount of issuance and is within the monitoring scope of the banking system. At the same time, the central bank adopted a centralized management model and a non-pure blockchain technology architecture. Digital currencies such as Bitcoin are based on blockchain technology and based on consensus mechanisms such as the proof-of-work mechanism to ensure system operation. They have the characteristics of decentralization and large value fluctuations.

Figure 1: Comparison of central bank digital currencies and Bitcoin

Source: "People's Bank of China Exploration of Legal Digital Currency", Huatai Securities Research Institute

The central bank digital currency will adopt the "central bank-commercial bank" dual system

As a cash alternative, central bank digital currencies have the characteristics of both paper currencies and fiat digital currencies. First, like paper money, DCEP does not count interest payments and has the basic functions of money: value scale, means of circulation, means of payment, and value storage. Its essence is that the central bank's liabilities to the public are infinitely repayable. At the same time, DCEP has the characteristics of fiat digital currency: non-repeatable spending, controllable anonymity, non-forgeability, system independence, security, transferability, traceability, separability, offline transactionability, programmable Sex and basic fairness.

Central bank digital currency adopts the dual system of central bank and commercial bank

Commercial banks pay 100% of reserves to the central bank. At the time of issuance, the central bank will issue digital currency to the bank vaults of commercial banks, and at the same time deduct the deposit reserve of commercial banks in equal amounts, and then the commercial banks will exchange the digital currency to the public. That is, the central bank is responsible for issuing, and commercial banks cooperate with the central bank to maintain the digital currency issuance and circulation system. On the one hand, cooperation with other commercial banks and institutions can make full use of resources and spread the risks assumed by the central bank. On the other hand, continuation of the current currency issuance system can avoid crowding out commercial deposits, leading to financial disintermediation.

Figure 2: The dual system of central bank and commercial bank

Source: "People's Bank of China Exploration of Legal Digital Currency", Huatai Securities Research Institute

Unlike digital currencies under a decentralized system such as Bitcoin, DCEP adopts a centralized management system. In the process of issuing digital currencies, the central bank maintains an authoritative position and has the highest authority. There are three main reasons for insisting on centralization. First, it is helpful to emphasize that DCEP is a liability of the central bank to the public. The central bank endorses a strong credit guarantee. Second, the implementation of centralized management is conducive to the central bank's macro-prudential and monetary control functions. At the same time, since a two-tier operation system is adopted, the implementation of centralized management can maintain the original currency transmission method and prevent currency over-issue.

DCEP takes the form of loosely coupled accounts to achieve controlled anonymity. The current electronic payment methods, such as bank cards and third-party payment platforms, all adopt the method of tightly coupling accounts, that is, funds must be transferred through real-name bank accounts, but with the increase of people's awareness of information security, electronic payment cannot meet The need for people to pay anonymously. The digital currency of the central bank adopts the form of loosely coupled accounts, which can transfer value without going through bank accounts, thereby achieving controllable anonymity. Unlike Bitcoin's complete anonymity, the central bank has the right to know the transaction data within the legal scope, and to trace the source of digital currency through big data analysis, while other commercial banks and merchants cannot obtain relevant information. This mechanism, while protecting data security and citizen privacy, also enables illegal activities such as money laundering to be effectively regulated.

In terms of transaction processing, DCEP uses a central ledger. The central bank's digital currency is technically neutral and does not presuppose a technical route. However, since the application scenario of DCEP is a high-frequency retail scenario, the ability to deal with high concurrency situations in digital currency transaction systems is relatively high. At present, the processing capacity of distributed ledgers is far from competent. The distributed ledger is used to assist in the registration of digital currency rights, and the transaction processing is still completed by the central ledger, which not only improves the security of data and systems, but also circumvents the limitation of processing speed.

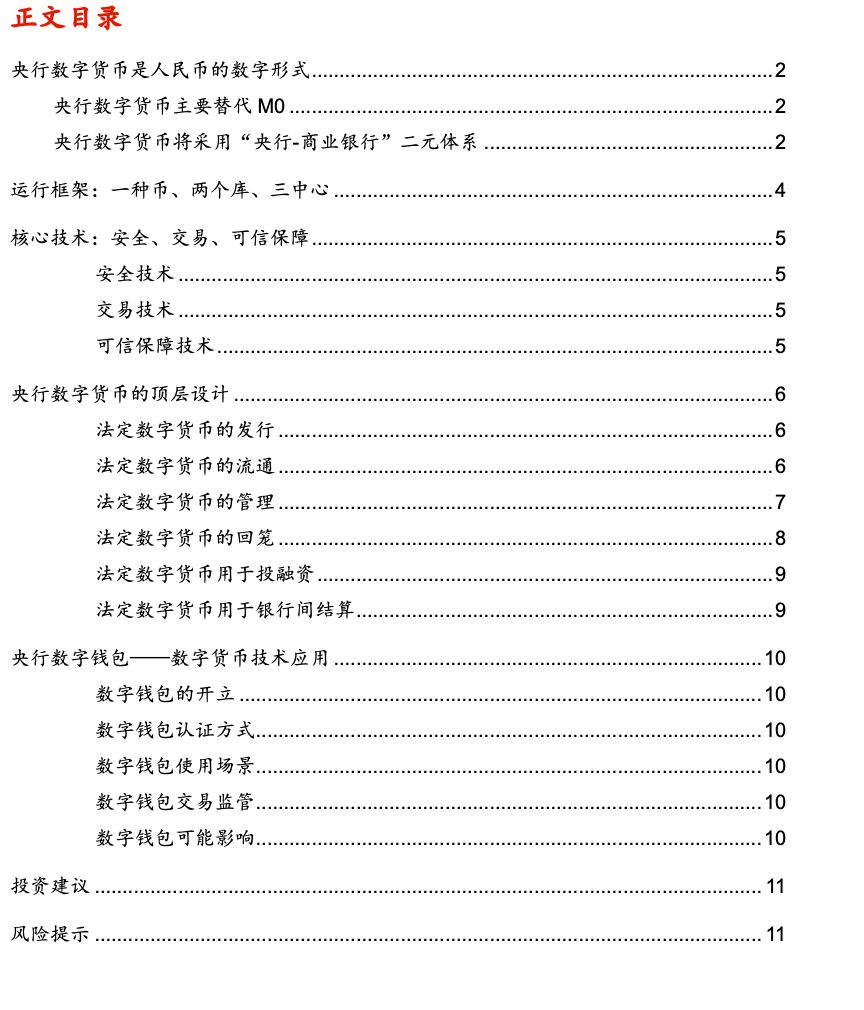

2. Operating framework: one coin, two libraries, three centers

The core of the central bank's digital currency operating framework is: one currency, two libraries and three centers.

Figure 3: Operational framework of the central bank's legal digital currency

Source: "People's Bank of China Exploration of Legal Digital Currency", Huatai Securities Research Institute

A currency: refers to the Chinese legal digital currency endorsed and issued by the central bank.

Two databases: a digital currency bank library and a digital currency issuing library. The issuance and circulation of digital currency by the central bank is based on a two-tier operating system of central bank-commercial bank-public. When issuing currency, the central bank issues digital currency to the digital currency bank vault of commercial banks. The commercial bank pays 100% reserve to the central bank as a digital currency issuing fund and enters the central bank's digital currency issuing bank.

The specific structures of the three centers are: certification center, registration center and big data analysis center.

1) Authentication center: responsible for centralized management of legal digital currency institutions and user identity information. It is a basic component of system security and plays an important role in controllable anonymity. Authentication can take the form of public key infrastructure (PKI) or identity-based cryptography (ibc).

2) Registration Center: Responsible for ownership registration and flow records, including central bank digital currency and corresponding user identity, legal digital currency generation and circulation, inventory check and extinction

3) Big data analysis center: Relying on big data, cloud computing and other technologies, it processes massive transaction data. Through analysis of payment behavior and analysis of supervision and control indicators, grasp the currency circulation process, ensure the security of digital currency transactions, and prevent illegal acts such as money laundering to provide data support for the implementation of macro policies.

The trusted service management module acts as an access point for the services of each party and is responsible for the issuance, management, authentication and authorization of digital currency applications. Users conduct digital currency transactions through mobile terminals. The digital currency client application is stored in the security module of the mobile terminal, and consumers and merchants can conduct online transactions with other mobile terminals through payment platforms, or offline transactions through NFC, etc.

3. Core technologies: security, transaction, and credible guarantee

The core technology of China's legal digital currency is divided into three categories: security technology, transaction technology and credible guarantee technology.

Exhibit 4: The core digital currency technology of the central bank

Source: "People's Bank of China Exploration of Legal Digital Currency", Huatai Securities Research Institute

Core Technology 1: Security Technology

1) Basic security technology: including encryption and decryption technology and security chip technology . The encryption and decryption technology is customized and designed by the national password management agency, and its core is to establish a complete encryption and decryption algorithm system. It is mainly used in digital currency generation, confidential transmission, and identity verification. The security chip technology is divided into terminal security module technology and smart card chip technology. The terminal security module is mainly used for secure storage and encryption and decryption operations, and provides basic security protection for digital currency transactions. Digital currency realizes transactions through the terminal security module mounted in the mobile terminal

2) Data security technology: including data security transmission technology and secure storage technology . Digital currency information is transmitted in ciphertext + MAC / ciphertext + HASH mode to ensure the confidentiality, security, and tamper resistance of data information. Data security storage technology stores digital currency information through encrypted storage, access control, and security monitoring to ensure the integrity, confidentiality, and controllability of data information

3) Transaction security technology: including anti-repetitive transaction technology, anonymity technology, identity authentication technology and anti-counterfeiting technology . Anti-repeating transaction technology ensures that digital currencies are not reused by adding digital signatures, serial numbers, time stamps, etc. to digital currency data strings (double spend problem). Anonymous technology realizes the controlled anonymity of transactions through blind signatures (including blind parameter signatures, weak blind signatures, strong blind signatures, etc.) and zero-knowledge proofs. The identity authentication technology verifies the identity of the customer through the authentication center to ensure that the identity of the trader is valid. Anti-counterfeiting technology ensures the authenticity of digital currency and transaction authenticity through encryption, decryption, digital signature, and identity authentication.

Core Technology 2: Transaction Technology

Online transaction technology and offline transaction technology provide two different technical solutions, online and offline, for each link of the transaction business such as device interaction, data transmission, and transaction processing, ensuring that digital currency transactions are not restricted by network conditions.

1) Online transaction technology: including online device interaction technology, online data transmission technology and online transaction processing, etc.

2) Offline transaction technology: through offline device interaction technology, offline data transmission technology and offline transaction processing, etc.

Core Technology 3: Trusted Guarantee Technology

Trusted service management technology is based on the Trusted Service Management Platform (TSM), which provides security chips and application lifecycle management functions for digital currency participants . Trusted service management technology provides various services for digital currency, including application registration, application download, security authentication, authentication management, security evaluation, trusted loading, etc., to ensure the security and credibility of digital currency security modules and application data.

4.Top-level design of central bank digital currency

The top-level design of the central bank's legal digital currency system mainly involves six links, including the issuance, circulation, management, withdrawal, investment and financing, and interbank settlement of legal digital currencies. The digital currency system consists of the central bank digital currency system, the commercial bank digital currency system, and the authentication system.

Figure 5: The composition of the digital currency system

Source: "China's Central Bank Digital Currency: Operational Framework and Technical Analysis", Huatai Securities Research Institute

Among them, the central bank digital currency system is used for the generation, issue and ownership registration of digital currencies. Commercial bank digital currency systems are used to perform banking functions on digital currencies. The authentication system is used to provide authentication to the interaction between the central bank digital currency system and the terminal device and the commercial bank digital currency system.

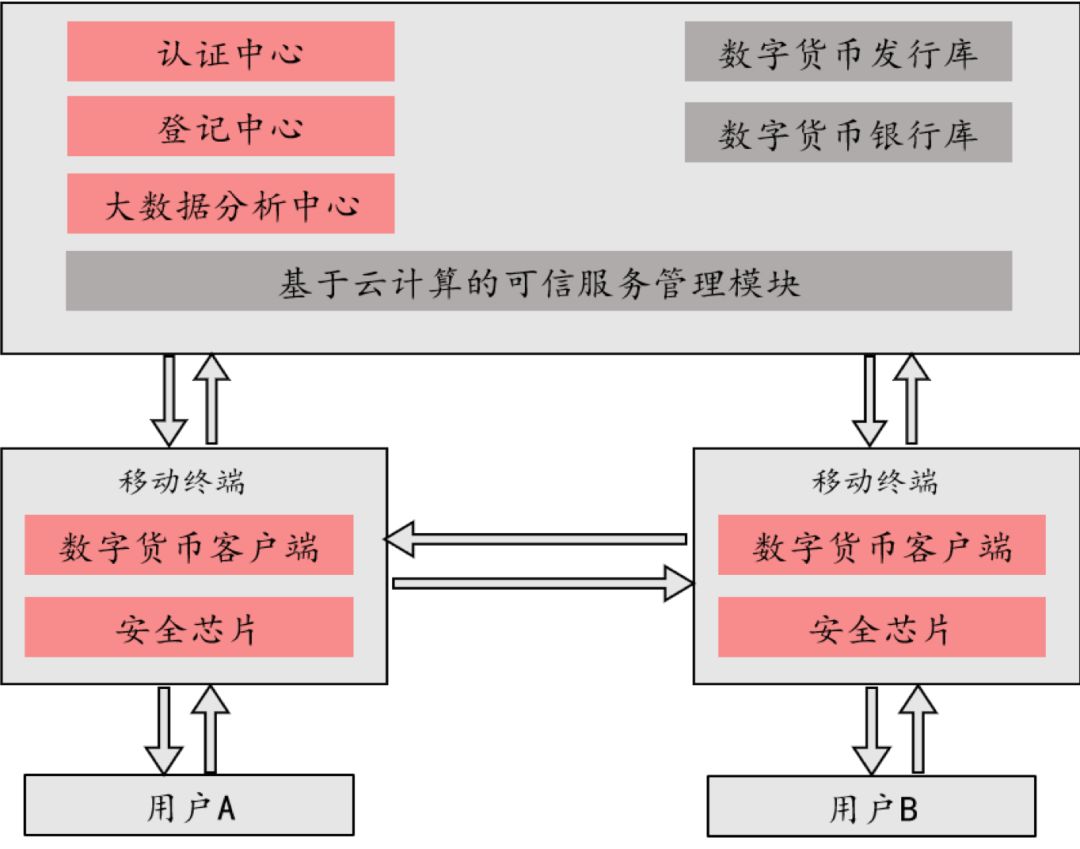

Issuance of fiat digital currencies

When issuing legal digital currency, the digital currency issuance system must first receive the digital currency issuance request sent by the applicant and conduct business verification. After the verification is passed, the issuance system sends a request to the Central Bank's Accounting Data Concentration System (ACS) to reduce the deposit reserve. After receiving the signal from the ACS that the debit successfully responded, the issuing system produced digital currency and sent it to the applicant.

Figure 6: Issuing process of fiat digital currency

Source: "China's Central Bank Digital Currency: Operational Framework and Technical Analysis", Huatai Securities Research Institute

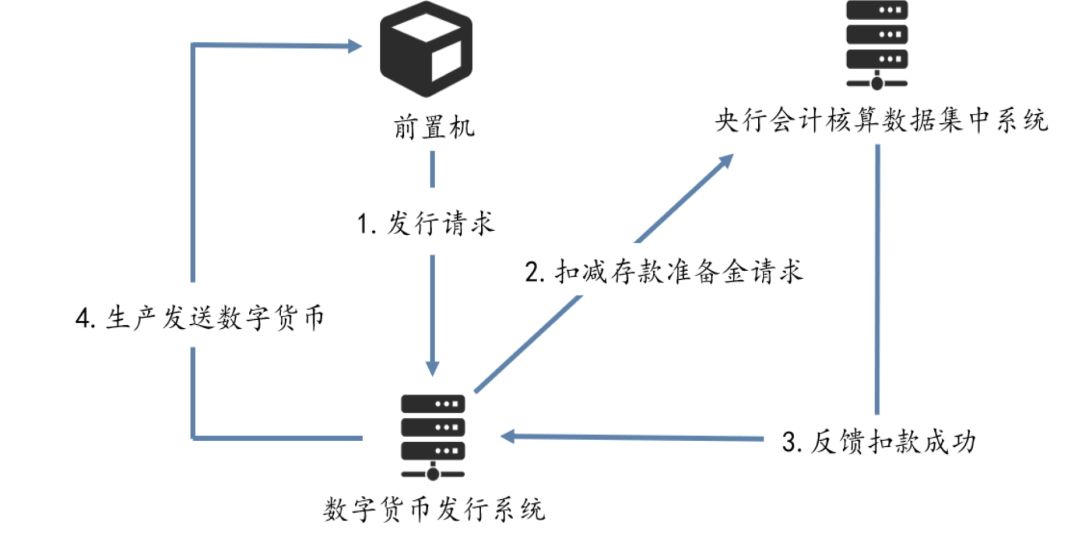

Circulation of fiat digital currency

When using fiat digital currency for transactions, the payment terminal selects digital fields from the digital currency safe deposit box to form a payment source digital currency string set according to the payment amount and a predefined matching strategy, and sends the string set to the management end. After the management end registers the digital currency string in the string set as invalid, it generates a payment to send to the digital currency string to the receiving end. The amount of the payment destination digital currency string is the payment amount, and the owner's identification is the receiving end.

Figure 7: Circulation process of fiat digital currency

Source: "China's Central Bank Digital Currency: Operational Framework and Technical Analysis", Huatai Securities Research Institute

Management of fiat digital currencies

The digital currency management system includes a digital currency tracking method system and a digital currency management system triggered based on certain conditions. The trigger conditions include economic status conditions, loan interest rate conditions, flow to subject conditions, and point-in-time information conditions.

1) Digital currency management method and system triggered based on economic conditions : It can adjust the return rate of funds accordingly, thereby avoiding liquidity traps and realizing countercyclical regulation of the economy. Implementation process: The digital currency system obtains economic information at the corresponding point in time when recovering the currency. When the economic information meets the preset conditions, the digital currency's return interest rate is adjusted and recovered according to the adjusted interest rate.

Figure 8: Digital currency management method and system triggered based on economic conditions

Source: "China's Central Bank Digital Currency: Operational Framework and Technical Analysis", Huatai Securities Research Institute

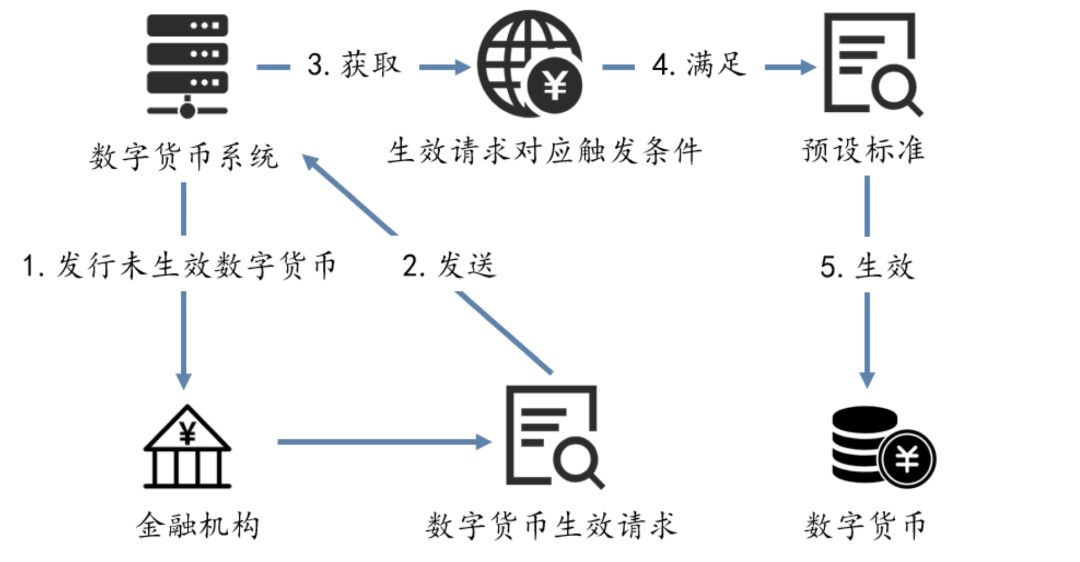

2) Digital currency management method triggered based on loan interest rate, flow to the subject, and point-in-time conditions : The digital currency management system controls the validity of digital currency through external trigger conditions, making digital currency investment more accurate and reducing the transmission delay of monetary policy To reduce currency idling. Implementation process: The digital currency system issues status information to financial institutions as ineffective digital currency. After receiving a digital currency validation request from a financial institution, it obtains information about the trigger conditions (loan interest rate / flow main body / point) of the validation request. . When the trigger condition meets a preset standard, the state information of the digital currency is set to the effective state.

Figure 9: Digital currency management measures triggered by loan interest rate, flow to the subject, and point-in-time conditions

Source: "China's Central Bank Digital Currency: Operational Framework and Technical Analysis", Huatai Securities Research Institute

3) Digital currency tracking method and system: while protecting the privacy of users, it can track the flow of funds of the fund payer across the subject within the scope of the issuer's management, and support customized tracking of currency flows. Implementation process: The digital currency system accepts the tracking request of the source currency owner, sets up tracking and saves the destination currency in the transaction currency generated by the transaction; after receiving the query request of the source currency owner, returns to it the tracking of the subsequent transaction process of the source currency. Chain.

Withdrawal of fiat digital currencies

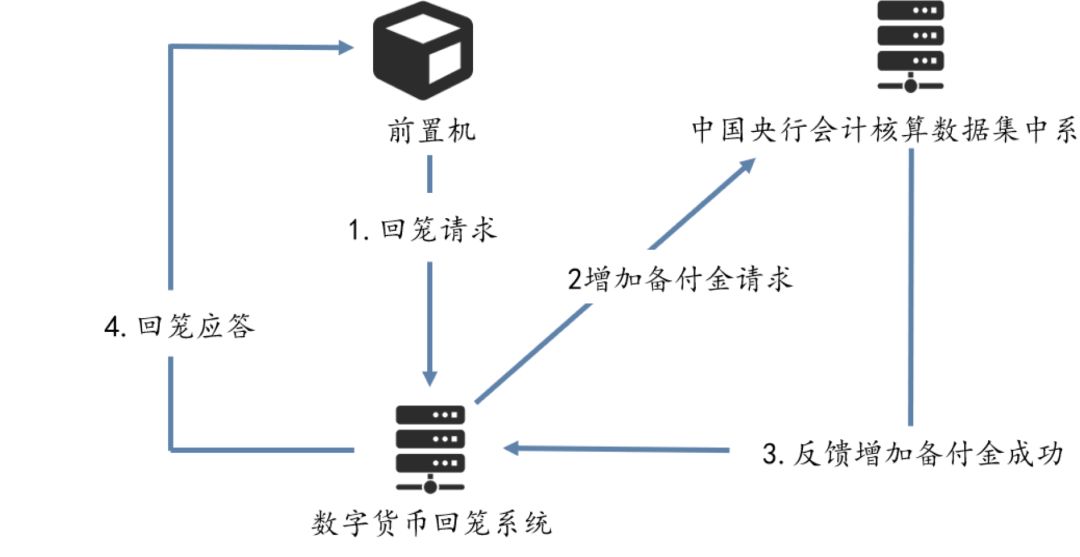

During the digital currency withdrawal process, the digital currency withdrawal system receives the digital currency withdrawal request sent by the applicant and conducts business verification . If the verification is passed, the return system sends a request to increase the reserve fund to the ACS system; after receiving a successful response from the ACS to increase the reserve reserve, it sends a digital currency return response to the applicant.

Figure 10: Withdrawal process of fiat digital currency

Source: "China's Central Bank Digital Currency: Operational Framework and Technical Analysis", Huatai Securities Research Institute

Fiat digital currency for investment and financing

The combination of digital currency system and smart contract technology can realize the transfer of funds from investors to fundraisers on the investment platform . Implementation process: First, the investor's wallet receives the smart contract issued by the investment platform, and after the investor confirms, adds the investment amount, the investor's digital signature and the investor's personal information to the contract. After the investment confirmation information is verified by the investment platform, the smart contract takes effect, and the investor's wallet pays the digital currency to the fundraiser through the digital currency system.

Fiat digital currency for interbank settlement

The inter-bank digital currency settlement system organically combines digital currency settlement with traditional inter-bank settlement methods.

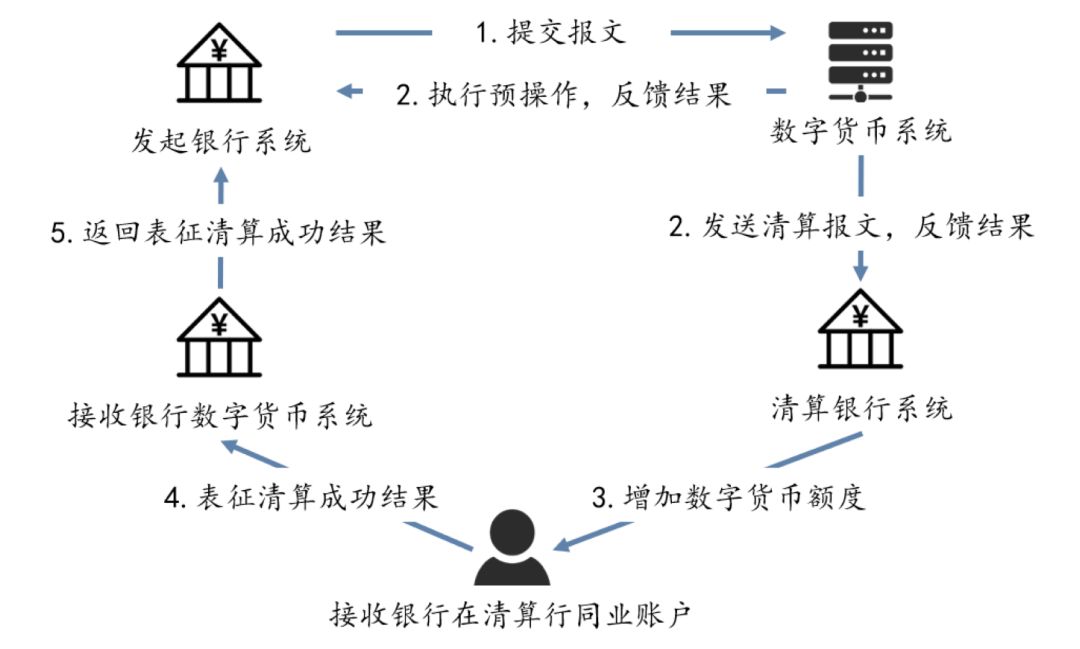

Implementation process: The initiating bank system sends a message to the digital currency system to pay the digital currency to the receiving bank. After receiving the message, the digital currency system performs pre-operations and feeds back the successful results of the operations to the originating bank and clearing bank. After the clearing bank system receives the clearing message sent by the digital currency system, it adds an amount equal to the amount of the received digital currency to the deposit balance of the clearing bank's interbank account, and sends the result indicating the successful settlement to the receiving bank's digital currency. system. The receiving bank's digital system returns the received results indicating successful clearing to the originating bank's system.

Exhibit 11: Inter-bank settlement process of fiat digital currency

Source: "China's Central Bank Digital Currency: Operational Framework and Technical Analysis", Huatai Securities Research Institute

5.Central Bank Digital Wallet-Digital Currency Technology Application

Digital wallet may become the carrier of central bank digital currency. The digital currency of the central bank can adopt a two-layer structure of a commercial hidden account system + digital currency wallet, and adopt two paths to establish a separate digital merchant management entrance or set up an independent digital wallet app in the existing bank and third-party payment system. One account manages both existing bank deposits and digital currencies.

Opening of digital wallets

Individuals and businesses open digital wallets through commercial banks and businesses . Similar to paper money, users and users do not need to bind the corresponding bank account for the mutual transfer, nor do they need the network. However, the recharge or withdrawal of digital wallets requires the corresponding bank account.

Digital wallet authentication method

Similar to online banking and third-party payment platforms, digital wallets also need to verify their identities for authorization, so digital wallet verification systems are required. Currently widely used authentication methods include specific generated identification codes (such as online banking U-Shield), biometric codes (such as fingerprint identification, facial structure light identification), and traditional passwords. The digital wallet verification system also needs the corresponding legal person identification code system and natural person identification code system. The legal person identification code may include business registration, administrative level information, and the natural person identification code may use more biometric codes such as fingerprint verification, facial recognition, etc.

Digital wallet usage scenarios

The digital currency of the central bank belongs to fiat currency and has unlimited legal compensation, so the receiver cannot reject the digital currency of the central bank. This means that as long as an electronic payment platform exists, you can use the central bank's digital currency for payment, instead of facing exclusive restrictions due to commercial competition like third-party payment platforms. Similar to electronic payment, digital currency transactions should involve operations such as quick payment, scan code payment, NFC payment, and digital wallet transfer. At the same time, the "dual offline technology" enables digital wallets to complete value transfer without the need for a network. The scope of application is wider, and small retail may become a high-frequency application scenario.

Digital wallet transaction supervision

The central bank's digital currency transactions implement controlled anonymity. In order to prevent the anonymity of digital currencies from being used for money laundering or terrorist financing, when big data identifies specific transaction characteristics, data mining technology can quickly perform identity comparison and lock accounts Ground real identity . At the same time, digital wallet transactions will set certain restrictions in accordance with current cash management regulations, and set transaction limits and balance limits according to different levels of wallets. For example, direct exchange for large amounts of cash may require advance reservations. This can reduce the risk of financial procyclical effects and reduce the crowding out effect of digital currencies on deposits.

Digital wallets may affect

Unlike bank deposits, digital currencies are bank off-balance sheet assets and do not affect the existing core business systems of banks. After the direct connection is broken, third-party payment platforms such as Alipay are essentially paid in commercial bank deposit currencies. After the introduction of DCEP, they will be replaced by digital RMB endorsed by the central bank. The main changes are reflected in the changes in payment instruments and the increase in payment functions. Channels and scenarios will not change significantly.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Sweep the haze of physical delivery futures debut, Bakkt cash delivery bitcoin contract hotly opened

- Intensive Reading | "2019 China Blockchain Industry Development Report": a comprehensive review of the current status and trends of the development of industry, university and research

- Perspective | DeFi's Pillar: Decentralized Liquidity

- Re-understanding Bitcoin: 8 answers to Satoshi Nakamoto's wisdom

- Small mining companies help themselves: use financial derivatives to hedge hash rate fluctuations

- People's Daily Observation: How Manufacturing Plants Blockchain

- Can the founders easily take half of the "decentralized scam" that raised 30 million?