Article overview of fintech infrastructure change trends and market panorama

Source: Chain News

Written by: Chris McCann, Managing Partner of Proof of Capital

Compilation: Perry Wang

Fintech startups target all core financial applications. These core financial applications include banking ($ 7 trillion), wealth management ($ 75 trillion), capital markets ($ 74 trillion), Borrowings ($ 8 trillion), real estate ($ 8 trillion), insurance ($ 5 trillion), payments ($ 2 trillion), and remittances ($ 800 billion).

- Viewpoint | Blockchain can solve three major pain points in the commodity industry

- Must master: these latest cryptographic advances will shape blockchain trends

- Perspective | Seeing the arrival of the era of intelligent privacy computing from the development of computing platforms

Although these financial activities have different scopes, they are all interconnected, and most of them are completed by traditional financial institutions, including JP Morgan Chase, Wells Fargo, HSBC, BNP Paribas, Mitsubishi UFJ Financial Group (MUFG) , Bank of America, Bank of China, Industrial and Commercial Bank of China, Citi, etc.

Many fintech startups are created by technology developers . For traditional banks, they belong to a very new customer base and they are changing the needs of the underlying financial infrastructure.

Before analysing in detail how the ecosystem of the infrastructure has evolved, I want to talk about the main trends that have led to this change.

Major structural trends in Fintech's vision

- Growing global customer base

- Embedded Fintech

- Financial institution split

- Developers become end customers

Growing global customer base

If known geographic barriers are overcome, financial services companies used to face a limited range of customers. When traditional banks started, they established offices in local, city, region, state, and even the whole country, and collaborated with international remittance banks to transfer funds across jurisdictions.

The original purpose of the bank was not to serve international customers. Under the existing system, sending international payments has huge sunk costs in terms of supervision and compliance. For international remittances among retail consumers, the average payment cost reaches 7% .

In contrast, digital commerce platforms need to deal with international customers from the first day of their creation. E.g:

- Apple – 1.4 billion active Apple device users on all continents.

- Airbnb -650,000 homeowners, 150 million tenants, 2 million orders per day, covering 191 countries.

- Shopify -covering 600,000 merchants in 175 countries, with a total transaction volume (GMV) of $ 15 billion in 2019.

- Uber -Covers 3 million drivers and 75 million passengers in 80 countries, with a GMV of $ 40 billion in 2019.

- Binance -covering 15 million users in 180 countries, the platform's transaction value reached 1 trillion US dollars in one and a half years of operation time, and the cumulative profit reached 1 billion US dollars.

Today's financial infrastructure platforms must be able to cope with customer groups in all jurisdictions, all value exchanges, all types of use cases (producers, distributors, consumers) from the first day of their inception.

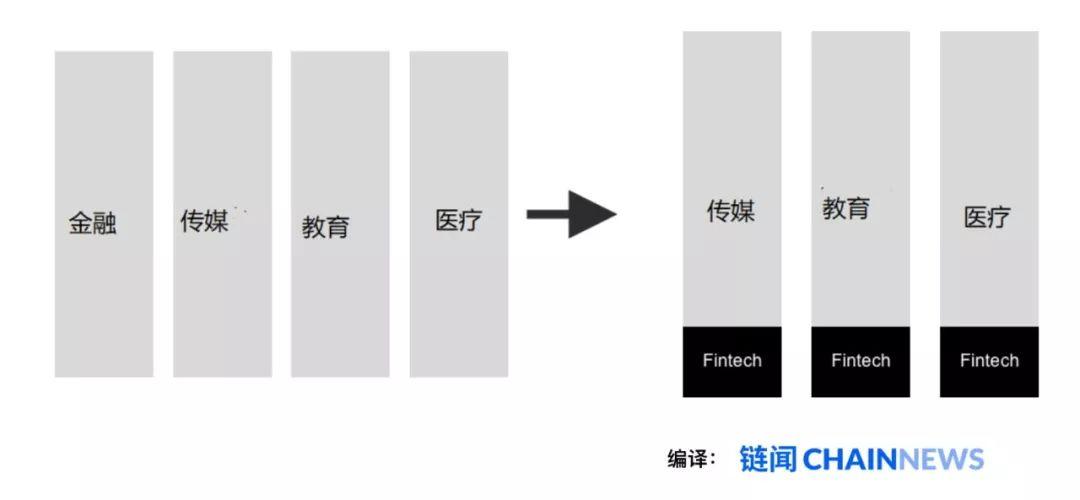

Embedded Fintech

The financial sector and fintech have long been seen as vertical industries serving specific use cases (banking, lending, transactions, etc.). However, what we are seeing today is the rise of " Embedded Fintech ".

Financial functions are no longer stand-alone applications, but are embedded in all consumer and business applications that people already use. E.g:

- Uber – Uber money feature is introduced to enable drivers to collect income in real time, and credit / debit cards are also issued to allow drivers to spend their balance.

- Grab -Created his own digital wallet that can be used to save and spend value (similar to WeChat Pay).

- Google – Checking accounts are now being offered through Citi and Stanford Federal Credit Unions.

- Facebook -is preparing to launch Libra , an ambitious initiative to develop digital currencies.

- WeChat (Tencent's)-1 billion users, and the total daily payment transactions of WeChat Pay reached 1 billion U.S. dollars.

Financial institution split

Financial companies used to be a large and comprehensive business, introducing a full range of financial products to all customers. For example, Wells Fargo provides all services to:

- Consumers — checking accounts, savings accounts, debit cards, credit cards, foreign exchange, remittances, and payments.

- SMEs -corporate checks and savings, debit and credit cards, corporate credit loans, loans, merchant services, credit card processing, and cashier systems.

- Business -Commercial checks, financing, real estate, employee benefits, institutional investment, investment banking, securities and wealth management.

by Tom Loverro: https://tomloverro.com/post/102797126721/banking-is-under-attack-heres-a-screenshot-of

by Tom Loverro: https://tomloverro.com/post/102797126721/banking-is-under-attack-heres-a-screenshot-of

As Fintech companies gain more and more momentum, they are mainly targeting narrow verticals and customer bases. The picture above shows how each fintech company is attacking a particular product segment provided by Wells Fargo.

Traditional financial companies have begun to feel the impact of large competitors and small fintech companies in various market segments and product areas.

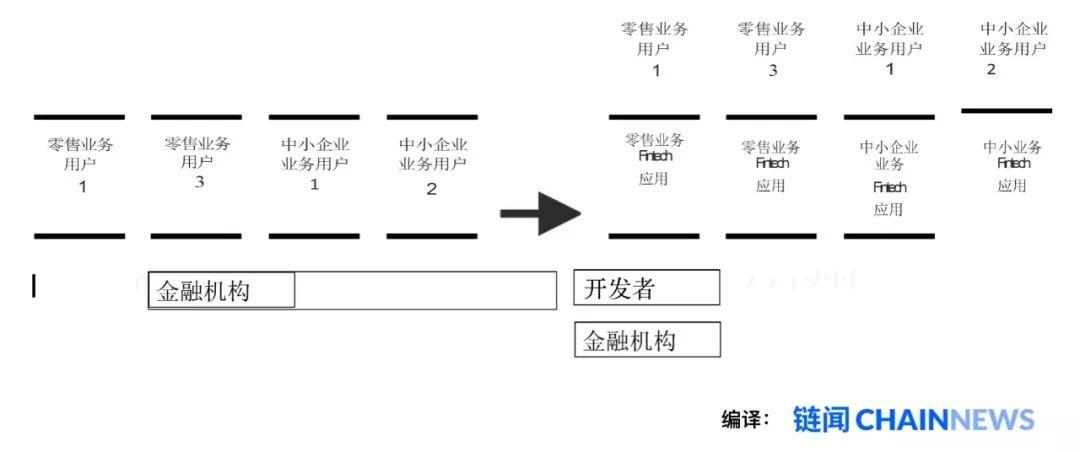

When developers become end customers

The establishment of financial institutions used to target customers (retail business) or business owners (SMEs) as customers. However, a new class of users has emerged, developers , who need access to the financial infrastructure used by these banks.

Developers not only want to access the data of financial institutions, that is, " open banking ", more importantly, they want to access the underlying functions provided by banks.

Before the advent of fintech platforms, if a developer wanted to create a new fintech company, it usually took more than two years to reach a partnership with a bank before starting operations. Now we see that it may only take a few hours for developers to launch new fintech applications using fintech platforms (such as SynapseFi, Sila, etc.). This greatly saves investment, and also makes the number of fintech applications in the market increase rapidly.

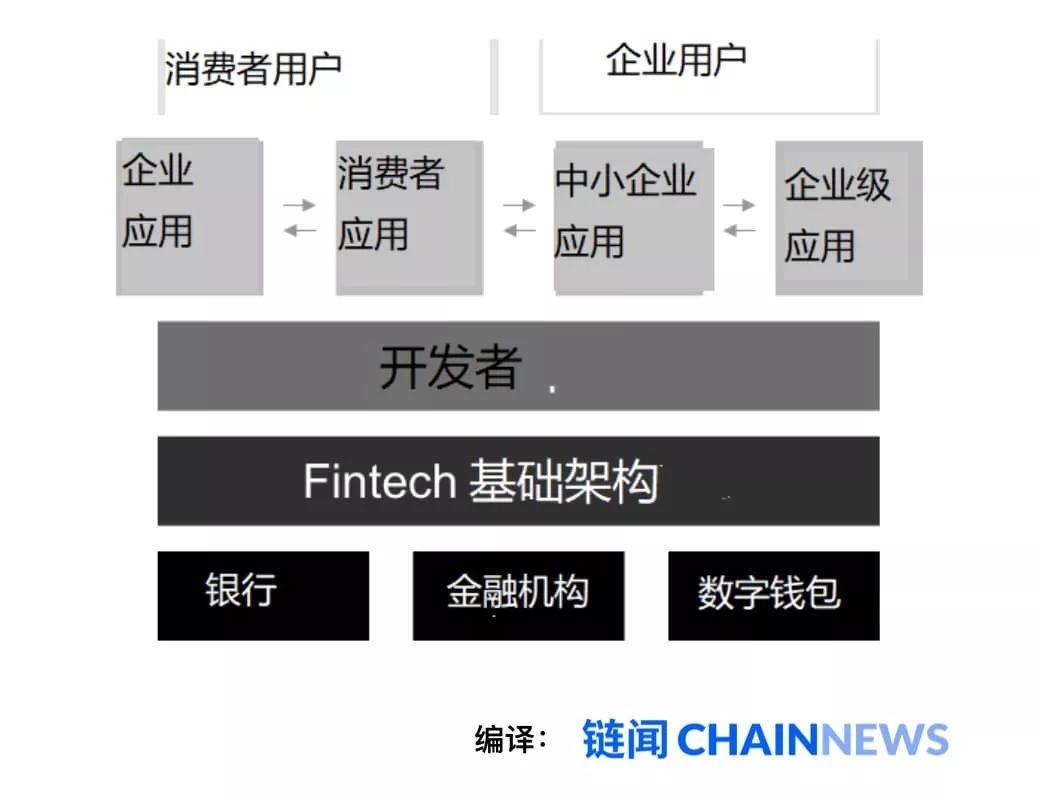

My prediction is that this trend will continue in the future, and financial infrastructure platforms will play a role in a range of financial networks, including banks, financial institutions, and an increasing number of digital wallets. These developer platforms will abstract the complex operations across multiple financial partners and allow various applications to embed fintech services in their products, including fintech and non-fintech applications.

Fintech infrastructure

All the above fintech trends and other changes are driving the demand for fintech platforms. The most obvious demand is from developers who are building fintech applications based on traditional and next-generation financial infrastructure.

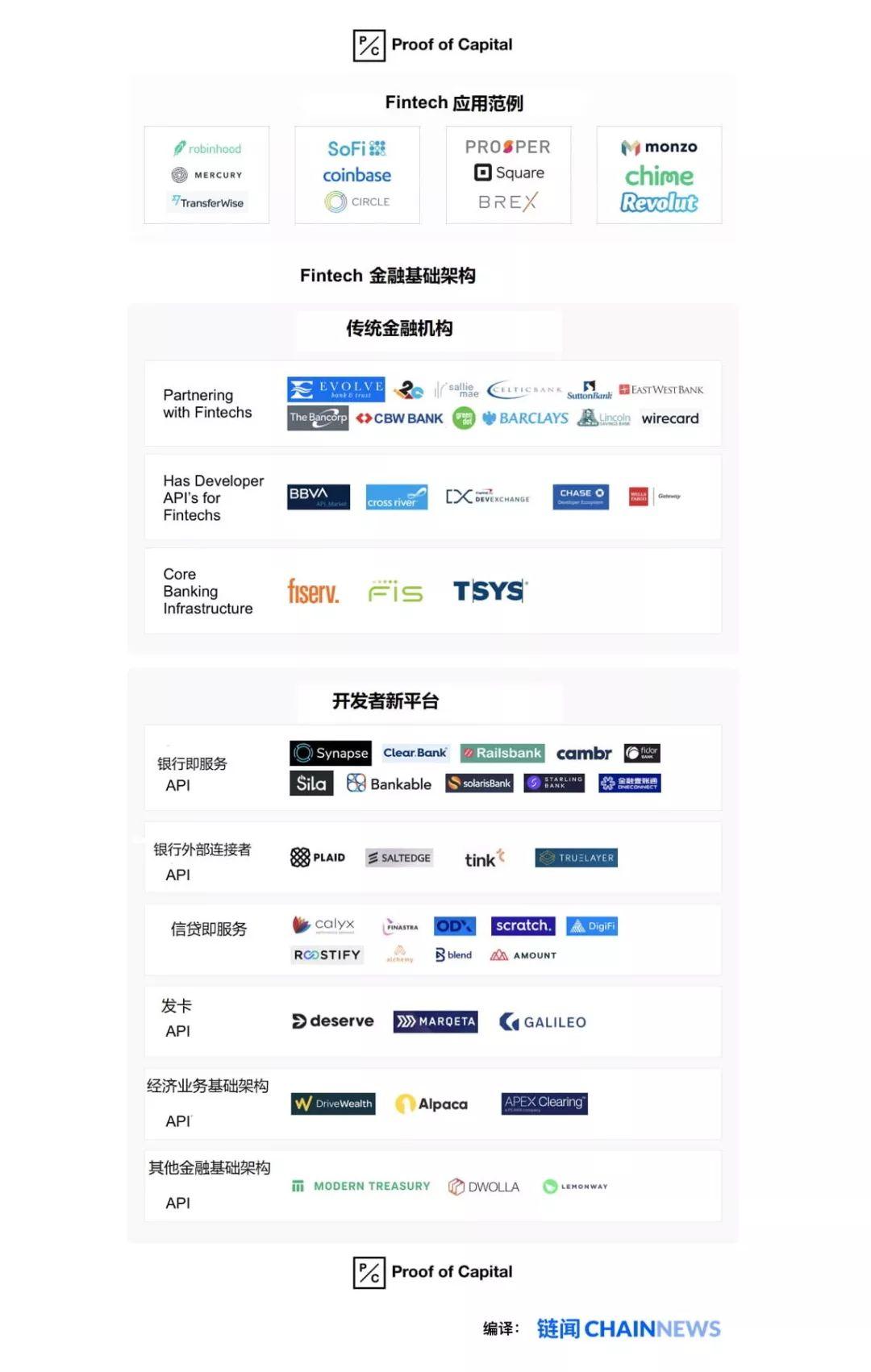

The following is a space map of the new fintech financial infrastructure:

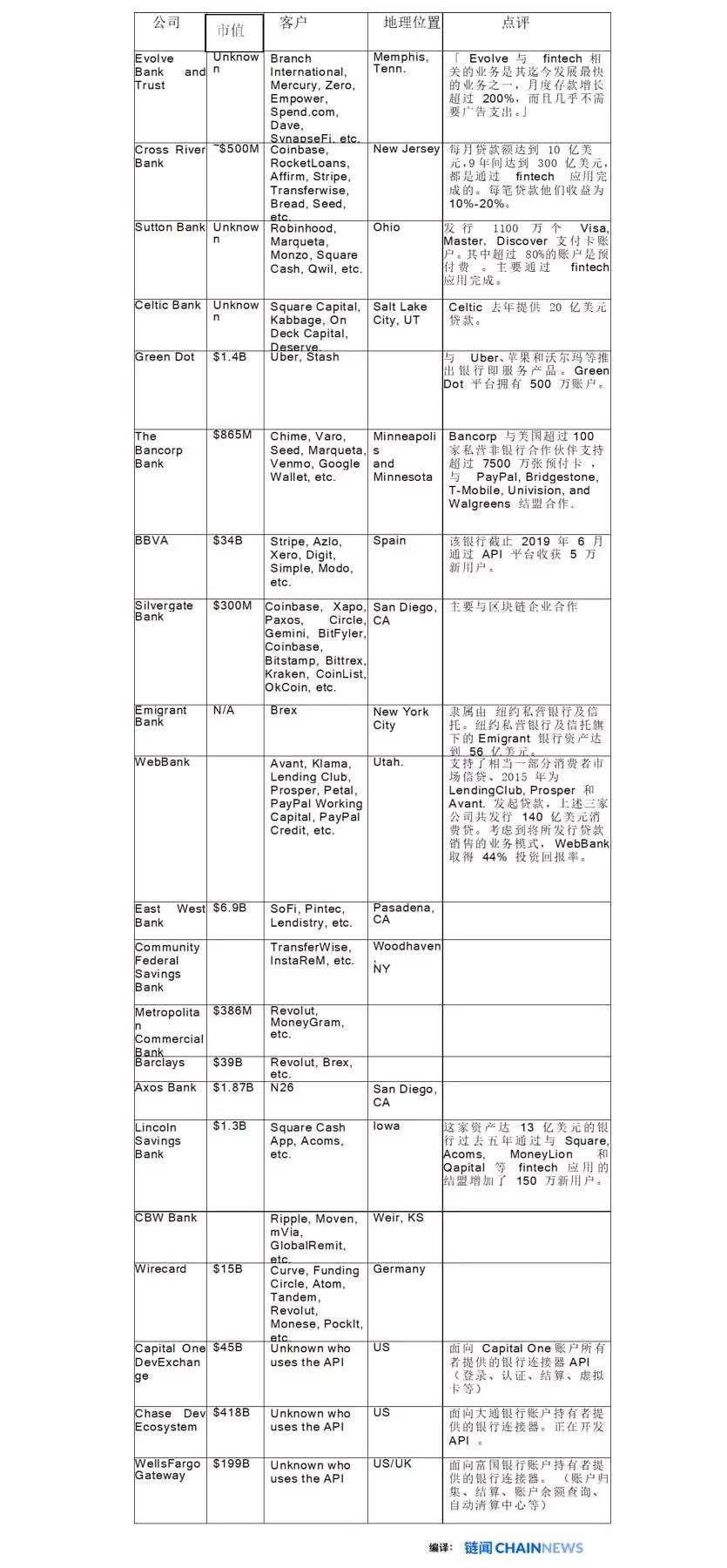

Traditional financial institution

This category includes all traditional banks that cooperate with FinTech companies, and their cooperation includes business level (white label banking), developer level (bank as a service), and existing core banking infrastructure providers (FIS, Fiserv, etc.) . Many of these pioneers were small community-oriented banks, with the exception of Bilbao Bank of Spain (BBVA), which developed its own platform through the acquisition of Simple .

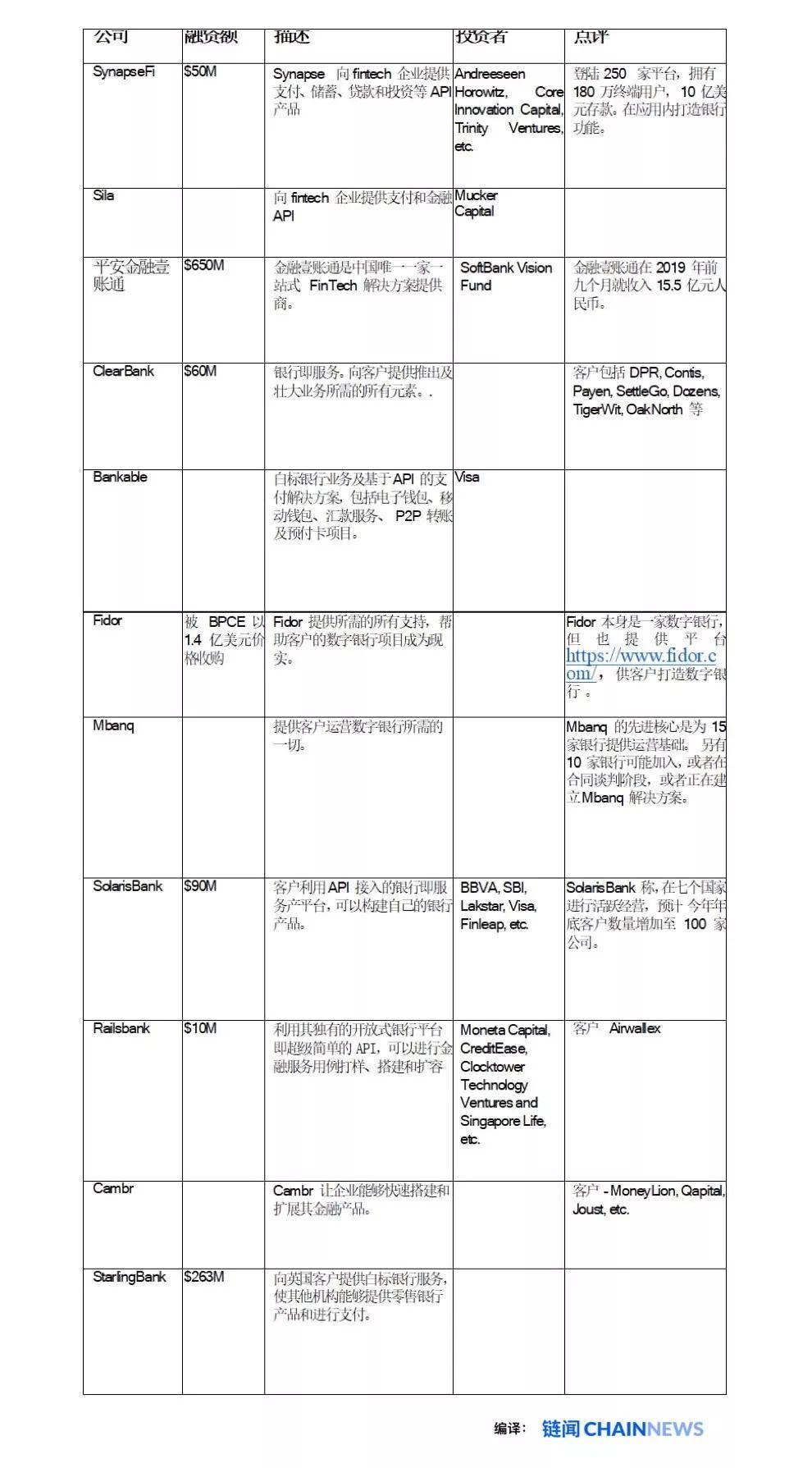

Banking-as-a-service platform

This category is mainly composed of other startups that try to provide developers with all the functions of a bank (deposits, savings, transfers, withdrawals) so that developers can build financial functions in their own applications.

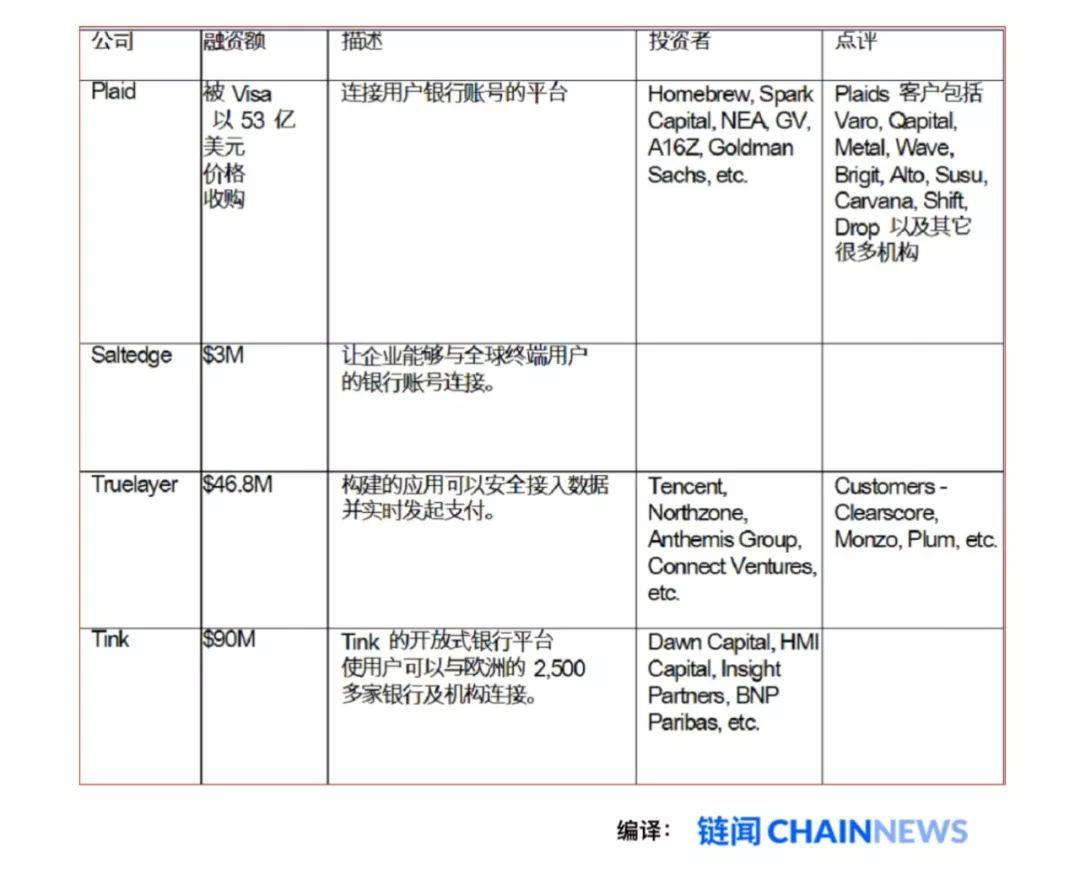

Bank Connector API

This category mainly includes platforms and services that allow users to link their bank accounts (Chase, Bank of America, Wells Fargo, Citigroup) through APIs, and developers can embed these APIs into the applications they develop.

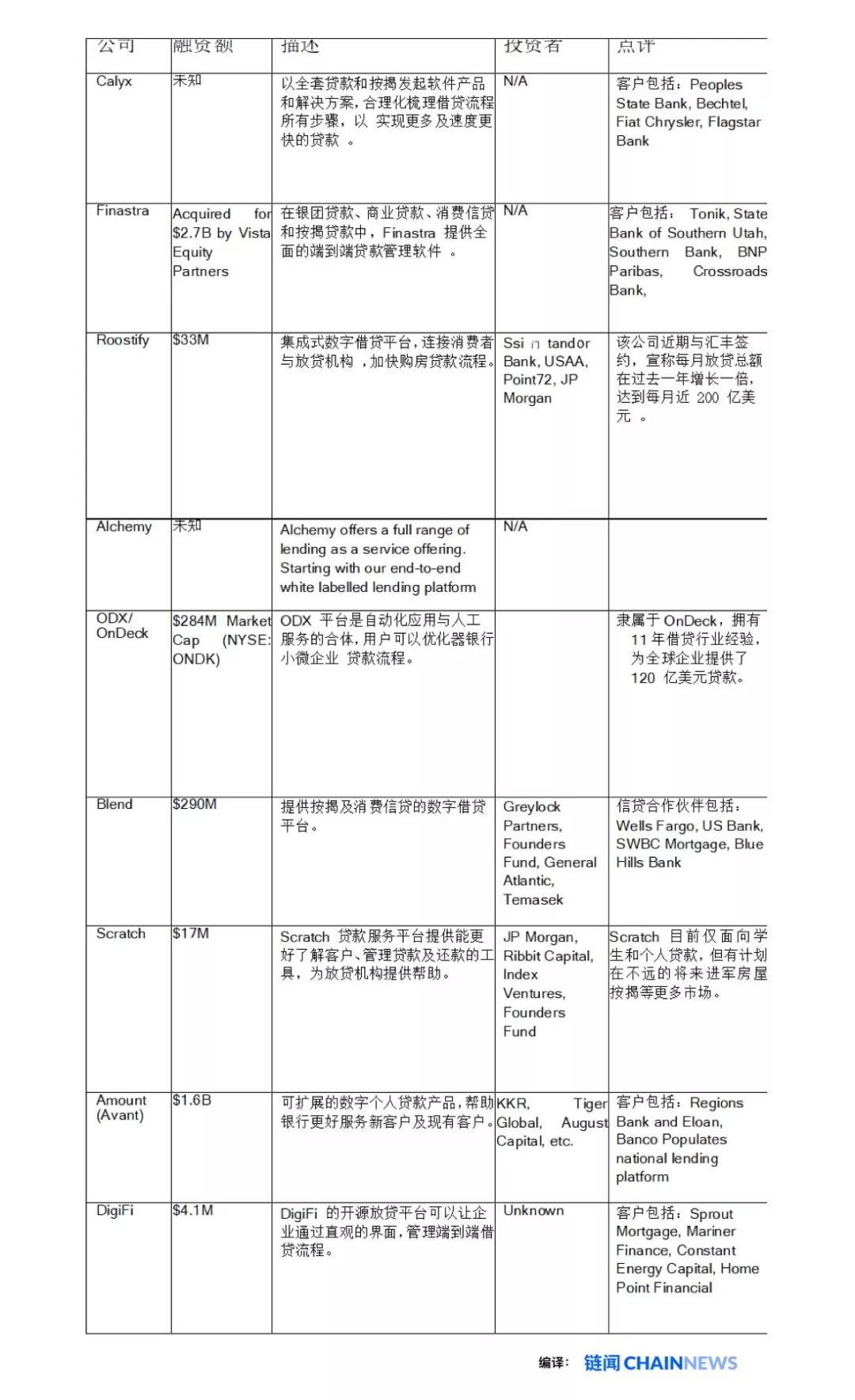

Lending as a service

This category includes platforms that provide end-to-end lending solutions that can be embedded in fintech applications or used by lenders and financial institutions. This includes some traditional players, as well as emerging startups that provide such services through APIs.

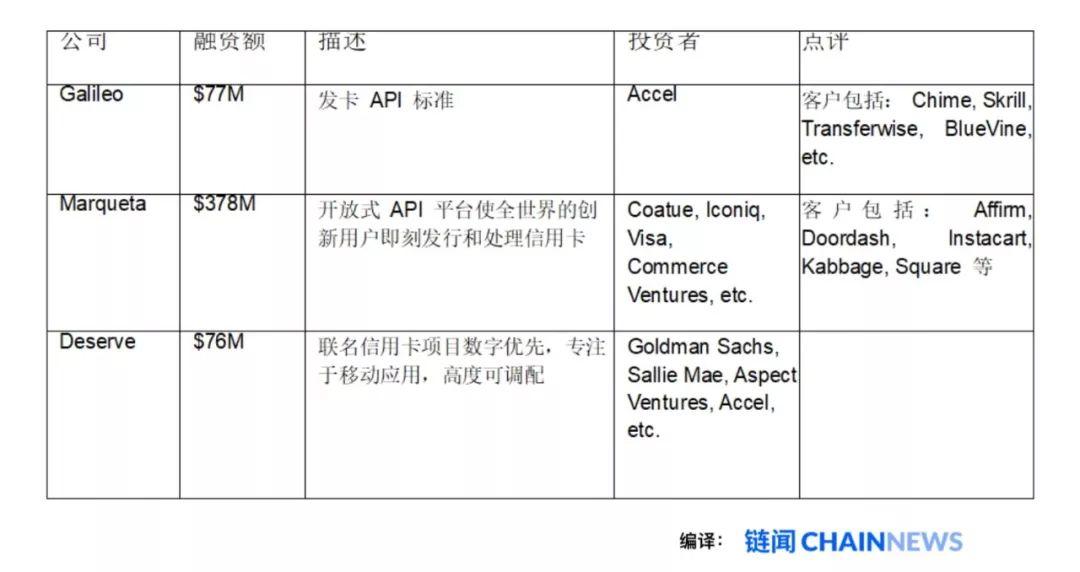

Issuing API for developers

This category mainly refers to platforms that allow developers to issue cards (credit cards, virtual cards, and prepaid cards) to end users in their applications.

Brokerage Business Infrastructure API

These APIs allow developers to provide stock trading and brokerage services in their fintech applications.

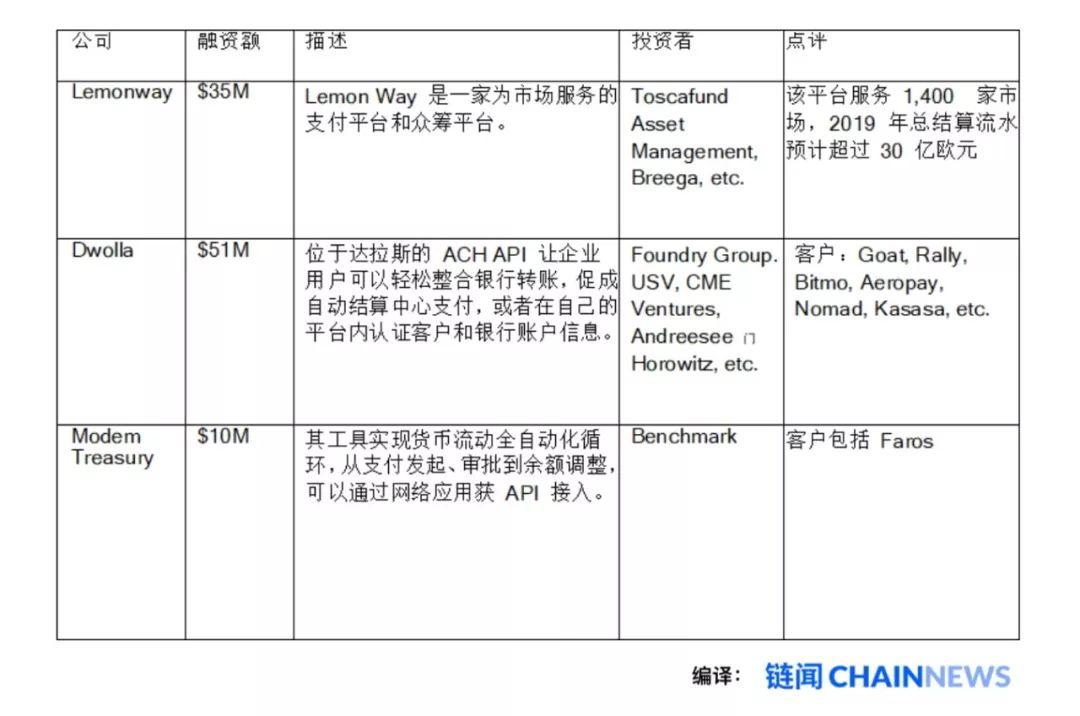

Other financial infrastructure APIs

Here are some other examples. These fintech infrastructure companies allow developers to build stock trading, trading markets, and other complex payment methods in their applications.

Bank vs. Developer

Many of the tools, APIs and infrastructures created above for financial applications were originally created for internal banking customers; however, with the rise of consumer and corporate fintech applications now, we need to treat external developers as Emerging new customers.

Plaid is a fintech infrastructure company that was recently acquired by credit card giant Visa for $ 5.3 billion . The latter said in its M & A report that there are more than 2,600 fintech developers on the Plaid platform. As more and more products embed financial functions in their applications, we will see that “ fintech developers ” will expand dramatically in all market segments and verticals.

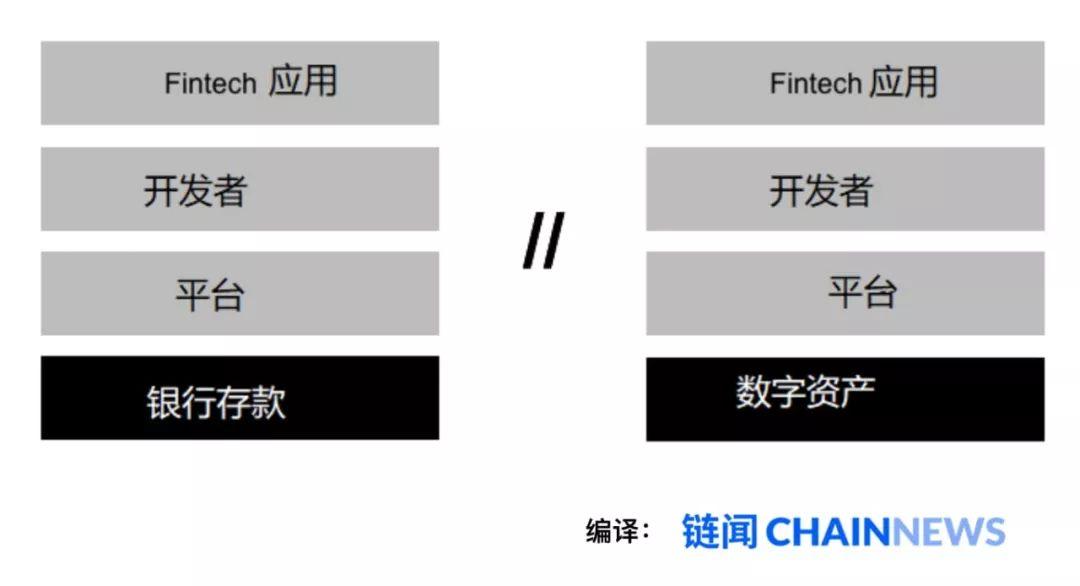

The future evolution of fintech infrastructure

Most people generally believe that fintech applications are built on top of existing banking systems.

However, as this infrastructure layer issue is resolved, a new banking runway currently in its infancy will emerge, most notably digital assets. Including Bitcoin and ETH, the most interesting ones are various types of stablecoins (USDT, USDC, etc.).

Given that digital assets are programmable by nature, many first-order problems have been resolved since their birth. Digital assets are stored in a common data layer (blockchain), have a shared interface (UXTO or ERC20 interface), and are built on interoperable protocols (assets can be stored in any digital wallet).

There is a big question here: is the first batch of digital asset platforms (Coinbase / Binance) to be the first to build a bridge between these gaps, or the traditional fintech application to move its digital stack down first, the answer is still unknown.

This cross-cutting area is very interesting and we have been watching closely.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Interpretation of SEC Commissioner Hester Peirce's "Token Safe Harbor Proposal" (with translation of the proposal)

- Crypto derivatives exchange FTX seeks $ 15 million in funding

- Graphic dismantling: Where did FCoin assets go? Is there a problem with the funding chain in 2018?

- Cryptocurrency Essence Series: The Rise and Development of the Mining Industry

- Forbes: Bitcoin's rebound this year is more sustainable than 2019

- MakerDao urgent vote to prevent governance attacks, this crisis may be related to the life and death of DeFi

- "The Secret History of Bitcoin": Who is the super-large Bitcoin mining pool with a computing power that approached 51%?