Can Bitcoin really become a safe haven under the financial crisis?

There is an old folk story about a factory worker suspected of stealing. One night, when the worker left the factory, the trolley was covered with a piece of cloth. The security guard picked up the cloth and checked it below, but found it was empty and let the workers pass. The next night, it was still like this. This situation continued until the end of the discovery that the worker had been stealing a cart.

Bewildered by the possibility that workers might carry away valuables, the security guard never considered the vehicles he might use to transport them. The trolley is so conspicuous that it will not be suspected.

Our own financial system also has its well-known trolley: the US dollar.

In each financial crisis, we conduct post-mortem analysis of the quotations and orders that were offered. We question the Fed. We fired the person who gave the green light to each other. We help the institutions get out of the woods. We introduce new legal and financial protection measures. Simply put, we are trying to prepare better for the next crash.

- What is EOS? What is the difference between Bitcoin and Ethereum?

- Zcash completes the first fork Ycash, what does this mean?

- Ethereum, Cosmos, Polkdot ecological inventory

But what if the actual problem lies in the characteristics of the dollar itself? This problem allowed Nakamoto to start researching Bitcoin – eventually Bitcoin came into being after the 2008 financial crisis.

Because we haven't seen how a new digital asset behaves in the global financial crisis, there are many claims about the fate of Bitcoin during the next crash. Of course, no one can know it clearly, but history allows us to paint a reasonable blueprint.

The fate of Bitcoin in the global financial crisis depends largely on the location of Bitcoin in the Exter pyramid and the time frame to consider.

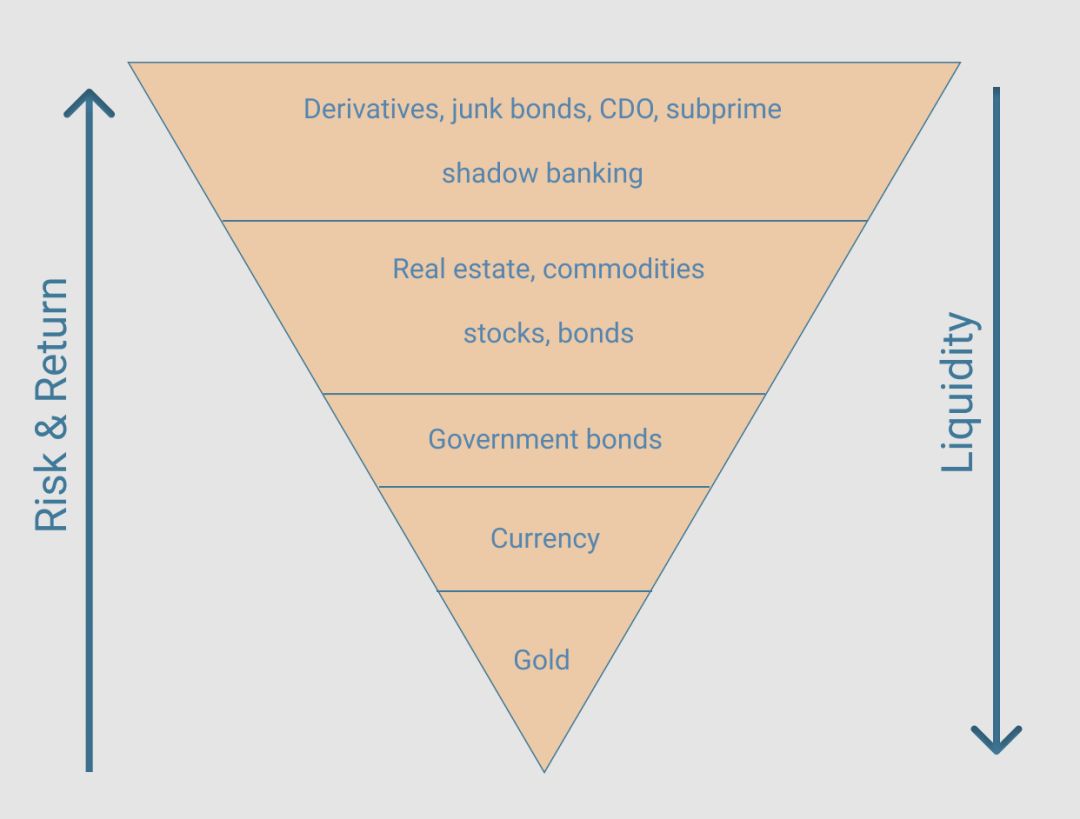

First, the importance of the pyramid base

As described in the Bitcoin Standard Monthly Bulletin, the Exter Pyramid was proposed by the late Vice-President of the Federal Reserve Bank of New York, John Exter, which provides a model for organizing financial assets based on risk and its corresponding liquidity.

The higher the return on an asset, the higher the risk associated with it. The greater the risk and return of an asset, the less liquid it may be. The bottom of the pyramid is very narrow, because the assets at the bottom are difficult to increase supply. At every level, the asset size increases because they become easier to produce, which increases both risk and liquidity.

Exter pyramid

The bottom of the pyramid is gold, it does not generate returns, but it is the safest asset, because this is not the responsibility of people. It also has the highest liquidity because it is a financial asset that has been accepted in most places in history because it is an asset whose price does not depend on anyone who fulfills its obligations.

History shows that no matter how many new currencies are created, once the situation becomes bad, people will once again use familiar, flowing, non-personal, gold without trust.

Looking up the Exter Pyramid, the risk (and return) of assets is increasing while the liquidity of assets is declining.

Above the gold is the dollar, which does not provide returns and is highly liquid, but the risk is higher than gold because its price depends on the Fed's approach. Going up is government bonds, which are less liquid than paper money, but have returns. Above the government bonds are commercial bank deposits, on which are various financial assets with increased risk and reduced liquidity, because the risks greatly impair the applicability as a medium of trading flows.

The Exter pyramid becomes wider as it reaches the top. Higher-risk assets are often used as collateral, so supply can grow faster than assets that require tangible support. This can be seen in the housing crisis of 2008, where false collateral obligations soon exceeded the value of the mortgages that supported them.

Although the pyramid is the most stable geometric structure, the inverted pyramid can only be stabilized when there is more gold at the bottom. When it becomes top-heavy, it collapses and collapses. In other words, as the debt vouchers surge, the creditworthiness of the borrower declines, and the possibility of defaults that result in a diminishing supply of money is increasing, leading to the collapse of the pyramid.

Second, the currency status of Bitcoin

An extreme example of the collapse of the Exter pyramid is reflected in Venezuela: inflationary monetary policy has led to the collapse of demand for monetary assets itself, which has led to a shift in demand for more liquid assets (such as dollars or gold) under the Exter pyramid, most Interestingly, the recent increase in demand for bitcoin.

This attempt to shift capital from “risk-in-progress” investments to “safer” investments is known as asset security transfer or liquidity transfer. People are unwilling to take risks and are more willing to keep their wealth and make it liquid.

Uncertainty in the market naturally leads to a safe transfer of assets because investors sell their risky assets in exchange for safe-haven assets like cash or gold.

The less extreme collapse of the Exter Pyramid was the financial crisis of 2008, when assets above the pyramid, including risky financial assets, all experienced liquidity collapses, and below the pyramids, such as the dollar, gold and government bonds, due to Investors see it as a safe haven and have risen in price.

Therefore, in terms of how its owner and its potential owners hold, the fate of Bitcoin in the financial crisis depends on its position in the Extre pyramid of the global economy.

If most Bitcoin holders are short-term speculative types, Bitcoin may be closer to the top of the Exter Pyramid and may suffer the same results as those of high-risk assets in 2008 , because short-term speculators of Bitcoin must liquidate them. Positions to hold more liquid, lower risk assets, such as the US dollar.

On the other hand, if the demand for Bitcoin is driven by its liquidity and usability in terms of international fast payments, then Bitcoin can be considered closer to the bottom of the pyramid. In this case, you would expect an increase in demand for Bitcoin during the financial crisis, as people choose to sell less liquid assets in exchange for Bitcoin.

Although this may not sound reasonable at first, remember that Bitcoin can be very useful in order to quickly transfer assets around the world, so it can attract demand for the asset in a crisis, even when it is short-term speculation. Exit this market.

In addition, Bitcoin can be understood as the golden status of the Exter pyramid in the cryptocurrency field. It is by far the most liquid digital currency. In the financial crisis, when people seek to liquidate risky positions from the cryptocurrency sector, Bitcoin is the most popular for those who want to exit the most risky market. The advantages of liquidity become their choice.

Only time and a full-fledged financial crisis can tell where bitcoin is in today's Exter pyramid, but in the long run, there are some important economic factors to keep in mind. Even if Bitcoin fell sharply during the financial crisis, it could continue to operate and perform its functions as usual, which would help prove its usability and value proposition as a neutral global settlement system.

Even as its price plummets, it will cause a large drop in demand as a short-term speculative asset, but its demand as a global liquidity tool will continue to exist. Over time, this feature tends to push the role of Bitcoin below the Exter pyramid.

More importantly, perhaps another unique value proposition of Bitcoin highlighted in The Bitcoin Standard: Bitcoin is the first absolutely scarce liquid asset. Even if the price increase of Bitcoin proves to be driven by short-term speculative demand, the supply of Bitcoin is still scarce, and the rise in demand and prices does not work at all.

This will distinguish it from all other assets above the pyramid, whose supply will be affected by demand. As the supply of these assets increases over time as demand increases, the difficulty adjustment of Bitcoin may make Bitcoin become more scarce over time, and naturally push it A more basic location in the Exter pyramid.

Third, the currency status of Bitcoin

For its first financial crisis, the judgment and practice of most Bitcoin holders will be difficult to guess, but the most important thing here is to understand: Bitcoin takes one more time and more financial crisis. A very different way distinguishes it from other assets in the Exter pyramid: its supply is fixed.

Although Bitcoin is in the early stages of its first crisis, the subjective opinions of various Bitcoin holders may determine the direction of change, but every time the recession is over, the fundamental economic characteristics of Bitcoin and its absolute scarcity are Make sure that the supply is minimal.

Because the stock-to-Flow ratio of Bitcoin continues to drop sharply, this feature has become more apparent over time, which has led to a smaller proportion of mining output that is gradually accounting for new supply, thus making bitcoin more Full currency advantage.

If the new financial crisis is approaching, Bitcoin will be distinguished from other assets by virtue of the fact that its supply may not increase too much. Former JP Morgan Chase Global Macro Leader Alex Gurevich explained this clearly in a blog post last year:

When Bitcoin first started trading, I barely realized it and didn't know its price. As a trader, I was very interested in its straightforward price increase in 2013, followed by a bear market in 2014.

It is worth noting that its decline has been supported; it has not continued to fall to the low point of the bear market. Instead, it stabilized and achieved a solid double-bottom in 2015 and began to soar. This trading model is consistent with precious metals, but is compressed to a shorter time frame. For example, … gold slowly stabilized its price after it soared in 1980.

So far, this trading model has only been shown in Bitcoin's own bubble, but we have not seen it in the context of the global financial crisis. It may not appear in the first crisis because supply growth rates are still not very low and the number of holders is still small, so they are very price sensitive.

Whenever money flows into an asset in the Exter Pyramid, a large amount of supply is generated. When people turn to the US dollar, the Fed may take an increase in supply. When people seek to store their homes as value, the more developers build, the more the house's supply increases, and ultimately the price. When people choose mortgage-backed securities, the securities themselves will proliferate rapidly, just like the houses that support them, which also causes prices to fall.

But as more and more money flows to Bitcoin, there will be no change in supply, so its performance is similar to that of precious metals, as Gurevich observed.

Fourth, consumer behavior after the crisis

In a study analyzing the major changes in purchasing behavior during the economic crisis, the performance of consumers' self-reliance and control was investigated:

“[After the financial crisis] consumers want to make changes and know that they can only rely on themselves. The recession is an opportunity to take a step back and think seriously. They will look for something “more important than self” from “positive pessimism”. "To the "active mindfulness".

Despite their anxiety, people are changing the status quo and better controlling their current lives and future. The main way they do this is through their consumption choices. Their most powerful means of control is "active mindfulness."

Does anyone wonder if consumer behavior will become more self-reliant and self-made? During the economic crisis, it is not possible to withdraw funds from banks as needed, and to clearly understand that the unchangeability of our financial system is contrary to the nature of its disruption, which will only lead to serious mistrust of financial institutions. And there is no clearer, smoother way to regain that control than having your own bitcoin and keys.

The shift to behavior that is more controlled, self-reliant, and out of the traditional post-recession is precisely the growth environment that Bitcoin needs to thrive. Coupled with the usual signs of a recession – including liquidity depletion and the interbank borrowing market, it is clear that after some financial crises, the perceived value of Bitcoin will increase over time.

Fifth, the new base of the pyramid

For its first crisis, Bitcoin may fall sharply, but no matter how much it falls, it may eventually stabilize at a certain price due to the smaller number of new ones. This is an important difference between Bitcoin and other assets (except gold).

The expected stability may increase the credibility of Bitcoin as a means of hedging and value storage. Considering that the Bitcoin network will continue to operate and will remain at a certain price, even if a new user begins to recognize its value proposition, it may only temporarily affect it.

This may not happen for the first or second economic crisis, but as time goes on, as the supply growth rate continues, and after several financial crises raise the awareness of Bitcoin as an alternative asset, Bit The currency may develop in a similar way towards the gold position in the Exter pyramid.

Its widespread worldwide sales, as well as its scarcity and volatility, will ultimately make people more interested in holding it as a long-term value store rather than as a short-term speculative bet.

According to the hypothesis, the bite-based Exter pyramid may be more stable than our traditional gold-based pyramid; except for the creation of productive assets, it has almost no growth, and with a small amount of reserves, re-collateralization and maturity mismatch (maturity mismatching) controls very few unsustainable expansions.

Regardless of the performance of Bitcoin in the next financial crisis, one thing is clear: it is time to take a closer look at our trolleys.

-END-

Translation: Chuan , a contributing author of the Blockchain Institute.

Disclaimer: This article is the author's independent point of view, does not represent the position of the blockchain study society, and does not constitute any investment advice or advice.

Source: https://www.tokendaily.co/blog/what-happens-to-bitcoin-in-financial-crisis

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- More than 1,000 Bitcoin ATMs operated by LibertyX in the United States

- Japan is leading the creation of an international cryptocurrency payment network similar to the banking network SWIFT

- Russian smelting giant Nornickel will launch digital trading platform by the end of 2019

- The coin chain completes the main network upgrade, and the new version of Galileo implements four major updates.

- Fold App integrates Lightning Network Protocol to support the use of Bitcoin for payment at merchants such as Whole Foods, Starbucks, etc.

- Australia's major supermarket chains are now accepting bitcoin payments

- India may ban all cryptocurrencies except the "digital rupee"