Comment: Upending the existing financial order, digital currencies such as Libra cannot do it

Source: First Financial

Author: Wang (The author is Secretary-General of China Society of Macroeconomics)

Blockchain, digital currency, and financial security are three topics that are closely related. Let me start with digital currency.

I. Digital Currency Issues: Why are there digital currencies?

When it comes to digital currency, we must say bitcoin. Bitcoin came out in January 2009. What is the background? It was the 2007 US subprime crisis. When did it catch fire? It was 2016, and the price of 1 bitcoin was still under one thousand dollars before 2016. Two years ago, it was still under one hundred dollars before 2014. The average daily trading volume is even smaller. It was below 100 million US dollars for a long time before 2016. It suddenly expanded to 4 billion U.S. dollars in 2016, 5 billion U.S. dollars in 2017, and has violently climbed to December 2019. $ 9 billion.

- ConsenSys report: Central bank digital currencies can bring huge efficiency and cost savings to the financial system

- Dong Feng: Blockchain warehouse receipts are expected to become the beginning of China's industrial Internet in the next two decades

- Mortgage-based distributed stablecoins: new ideas for inclusive finance, new trends in distributed finance

So what happened in 2016? It was the Bank of Japan and the European Central Bank that introduced negative interest rates at the beginning of June and June respectively. After the crisis in 2007, the QE (Quantitative Easing) policy introduced by major Western central banks for emergency purposes not only did not end, but continued to increase. Trend.

After the 2007 crisis, the Federal Reserve launched three consecutive rounds of QE. It announced that it would withdraw from QE in early 2018, but it turned back after September 2019. By the end of the year, it had newly purchased US $ 400 billion in debt, and the increase was larger than the previous three rounds of QE. The outside commented that it was the Federal Reserve's QE4, but the Federal Reserve did not recognize it. At the same time, US President Trump has continued to pressure the Fed to implement negative interest rates, saying that the Fed is his "biggest enemy" because the European and Japanese central banks have negative interest rates, and the government not only does not have to bear interest, it can also make money.

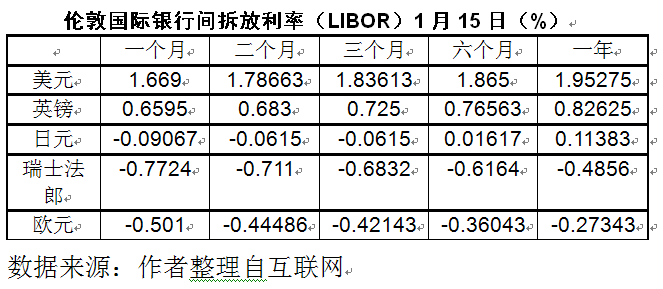

A large number of currencies and negative interest rates continue to depress the level of returns in developed country financial markets. Negative interest rate bonds just appeared in Europe in 2014. By March 2019, global negative interest rate bonds had exceeded $ 10 trillion, and by October last year, it had reached $ 17 trillion. The following table shows that the interest rates of the yen and the euro are in the negative zone, and the interest rates of other major countries are not far from "0".

In the context of economic and financial globalization, the monetary policies of all countries are mutually transmitted. The main body of world currency capital is in developed countries, and developed countries have entered negative interest rates one after another, and China cannot be immune from it. On July 4, 2019, the Bank of Shanghai's overnight lending rate (SHIBOR) was lower than "1%" for the first time, and entered the "0" range again on December 2 at 0.84%, while the discount rate on the national bank silver coupons during the same period It also fell below 1% and took the lead in entering the "0" era. Zhou Xiaochuan, former governor of the People ’s Bank of China, said that China should “try to avoid entering negative interest rates as quickly as possible”, which also means that China may inevitably have an era of negative interest rates.

Why is there such a phenomenon that negative interest rates are completely contrary to traditional economic theory? It is the impact of the new globalization, which makes the capital output rate of developed countries negative, so how much currency you invest will not enter the real economy, the return on investment of the real economy is negative, the price of funds is negative, and the interest rate is Negative, so the emergence of negative interest rates is not determined by the central bank's monetary policy, nor is it the commercial banks' preference for negative interest rates, but the objective economic development trend produced by the new globalization.

But the society needs to develop, and more and more pensioners are required to retire. However, the real economy cannot provide returns, so QE can only be implemented continuously, that is, financial bond issuing banks to buy, resulting in a growing proportion of fiscal expenditure from central bank notes. Larger, it has already accounted for 1/4 in Japan, and the United States and Europe are also 15%. This approach also has a good name, called MMT-modern currency theory. This is the only important theory that has developed in economics ten years after the 2007 crisis. It is the fiscalization of monetary policy. To put it another way, it is the monetization of fiscal policy, that is, as long as there is no inflation, the government can send as much currency as possible, and the government can use the central bank's money as the tax revenue. But everyone can see that the new crisis is coming again, and the way to deal with the new crisis is deeper negative interest rates and a larger QE.

Therefore, Bitcoin began to "fire" five years after its launch, and began to "fire" eight years after its launch, due to people's expectations that sovereign credit currencies will soon collapse in QE, negative interest rates, and the new crisis. . When Satoshi Nakamoto launched Bitcoin, he only emphasized that he was trying to create a decentralized and peer-to-peer currency. He did not say anything from the perspective of macro and even social politics, but Hayek, a representative of Western neoliberalism I wrote a book called "Denationalization of Currency", and there is a saying that the private digital currency is "to prevent us from being driven by continuous inflation to the government to completely control and direct, and ultimately the only way to save civilization is : Depriving the government of the power of the money supply ", I see that I have explained why there are digital currencies such as Bitcoin and Libra.

Digital currency and financial security

Whether the transition to the digital economy will generate new financial insecurity is a problem that must be faced. I think there are three aspects worthy of attention.

The first is whether private digital currencies will seriously disrupt the existing financial order?

Bitcoin is a currency that is publicly issued on the Internet. It has no issuing body and does not anchor any sovereign currency. It is a completely decentralized currency. If decentralized currencies such as Bitcoin and Ethereum can continue to expand the scale of use, it may be sooner or later that a chaos in the existing monetary and financial order will break out, because the government's most important means of macroeconomic regulation and control is monetary policy. Centralized currency is precisely to take away the most important macro-control tool in the hands of the government.

But at least from the current point of view, this worry does not seem necessary, because when Bitcoin and other cryptocurrencies have grown to the current millions of users and hundreds of billions of dollars in market value, they have already encountered technical bottlenecks and are increasingly unable to run. The total stock of major world currencies, including the M2 of the US, Japan, Europe, Britain, Switzerland, and medium-sized currencies, is at least 60 trillion US dollars. So I have reason to think that in the future, it is possible to replace sovereign credit currencies, and they will never be cryptocurrencies such as Bitcoin. That is, the fundamental challenge to the existing financial order will not come from cryptocurrencies. So Bitcoin has been around for a decade, but central banks haven't paid much attention to it.

There is also a folk digital currency like Libra, which anchors a package of sovereign currencies. Because of this relationship with sovereign currencies, its problem is not to replace sovereign currencies, but to share the currency issuance rights of central banks of various countries, thereby sharing countries. The central bank's coinage tax. This is a terrible thing for central banks and even governments of all countries, because it is inseparable from the right to issue currency whether it is to meet recurrent fiscal expenditures or to engage in a larger QE against the crisis. Therefore, the governors of the central banks of the 26 countries held a meeting in Basel, Switzerland last September, and collectively refused to land Libra in their country.

Private digital currencies such as Libra that anchor sovereign credit currencies are called "stable coins", which depend on the value of the sovereign currency. Therefore, if the credit of sovereign currencies is unstable during the new financial storm, these "stable coins" It is not stable. So from the perspective of subverting the existing financial order, I don't think Libra can do it.

So at least from the current point of view, private digital currencies that can subvert sovereign credit currencies have not yet appeared.

The second is the central bank's digital currency-can the CBDC end the financial risks generated by sovereign credit currencies?

At present, central banks in various countries are actively studying the issue of sovereign digital currencies, hoping to meet the challenges brought by private digital currencies. However, if, like Hayek said, the emergence of folk digital currencies is due to the proliferation of sovereign credit currencies, and the market needs a stable environment for bookkeeping, payment and stored value, in order to place the hope of high-quality currencies on folk digital currencies, Then the CBDC can't solve these problems either, because the sovereign credit currency and the sovereign digital currency have no difference in the source of the currency generation, the only difference is the use of digital cash instead of paper money. The collapse in the financial crisis, even if there is a CBDC, it will be a destiny with the sovereign credit currency.

In addition, the CBDC may also create new risks, because digital fiat currencies may cause deposits to flow from the commercial banking system to the central bank, which will have an effect similar to the increase in deposit rate, which will lead to monetary tightening. For countries such as China where digital payment has become widespread, it should have little impact, but for countries that have not universally adopted digital payment in Europe and the United States, the impact may be significant.

In addition, the launch of digital fiat currency will bring back the banknotes originally circulated outside the banking system into the banking system, which will greatly improve the transmission efficiency of monetary policy, but also improve the transmission efficiency of negative interest rates. What will happen to the combination of digital fiat currencies and negative interest rates? The effect is also a big unknown.

The third is the question of resistance to quantum cryptography.

Quantum computers are a new breakthrough in computing power. The most optimistic estimate is that they can enter the commercial stage after five years. In the current highly electronic financial system, the blockchain technology that has been promoted in China uses a large number of cryptographic technologies. For example, Internet banking, which has become very popular, must use E-TOKEN as the password to access personal online banking accounts. 256-bit hash password protection.

There are no passwords in the world that cannot be cracked. The security provided by passwords is always relative, so the definition of password security means that the cost of cracking is greater than the benefit. Before the emergence of quantum computing power, it is said that even a 256-bit hash password cannot be cracked even if it exhausts so much energy contained in the sun, so it is very safe. Bitcoin uses a 256-bit hash signature method to protect the blockchain. The information recorded in it cannot be tampered with. But it is said that a quantum computer can complete a computing task that can only be completed on a computer for 10,000 years, so all current encryption methods are like waste paper in front of quantum computing power. Therefore, if we do not have China's own quantum computing power, and if we develop a code that can be protected from quantum computing power, China's financial system will be insecure.

Blockchain and the digital revolution

In 1999, on the basis of the Internet TC / IP communication protocol, a "P2P" communication protocol appeared. This P2P is not a network loan, but a point-to-point communication protocol. Since then, the foundation of the blockchain has been created on the Internet. However, the general recognition of the blockchain started in the past two years. It was because of the bitcoin fire using blockchain technology that people became aware that there is still such a kind of behavior that can run automatically without any government organization. Currency and trading methods.

The decentralization of the blockchain is de-government and de-intermediation, which allows people who do not know on the Internet to establish trust relationships through smart contracts and other forms of consensus mechanisms, and prevents counterfeiting through distributed accounting and modern cryptographic technologies. And tamper with transaction information, and allow money and securities to run on the Internet. Blockchain has created too many miracles that completely violate the traditional market operation mode. It has opened a new door for people to transform the social and production relations in the era of the Internet and the digital economy. People will certainly be very excited about this.

But just when people first knew the blockchain, Bitcoin began to pour cold water on people's bright prospects for transforming production relations.

The first is that the transaction speed of Bitcoin is too slow. As mentioned earlier, it is only 7 times per second, which is far less than the speed of WeChat and Alipay hundreds of thousands of times per second. The speed of the second generation blockchain currency Ethereum is only 15 times. Libra has adopted a semi-blockchain approach. It is said that it can reach thousands of times per second, but if Facebook itself advertises to cover the payment needs of the world's 2.7 billion people, it is simply impossible.

So why is the transaction speed provided by the blockchain so slow? It is because to run money on the open Internet, a large number of cryptographic technologies must be used to protect it. Take Bitcoin, for example, the number of password bytes used in each block is more than the transaction information in it. The so-called "point-to-point" transactions are also carried out on the open Internet. For the safety of money, they must be encrypted. This is the so-called "public key and private key" technology. Such layer-by-layer encryption, security is safe, but transfer transactions Information must be long, and speed is sacrificed.

The transaction speed is too slow to use blockchain technology in large-scale and high-frequency transactions. This is the first cold water poured on the blockchain by Bitcoin practice.

The second problem arises from the distributed ledger. The trust mechanism of the distributed ledger is caused by the difficulty of tampering with records. This difficulty arises from the fact that transaction information must be recorded synchronously at each node. Therefore, it is not necessary to change a book to change the account, but to exceed 51%. The ledger must be changed before the blockchain will recognize this as true information. Therefore, the more users of the distributed ledger, the more difficult it is to tamper with the ledger, and the more trusted the information in the ledger.

But with the extension of time and the scale of transaction information, more and more transaction records must be stored. When Bitcoin first came out, the storage footprint was only 20 G. By the end of 2018, it had jumped to 200 G. By the end of 2019, it had jumped to 300 G. According to the current growth rate, it will exceed 10,000 in ten years. G.

This raises two questions. One is why should I keep the transaction information of others? The second is that if a large amount of stored information is used in application scenarios such as WeChat and Alipay, the mobile phone will not be used at all, because the relevant calculation proves that if it is a transaction scale such as WeChat and Alipay, with the current mobile phone's dozens of G of storage space, It's full in three days, and less than a month after using it on a PC.

What can fully reflect the "primitive" of these blockchains, such as decentralization and trust, is the public chain. The public chain is a freely accessible blockchain. Bitcoin and Ethereum are both public chains. "Consensus", I think this consensus is that the public chain has no basis for large-scale applications because of technical bottlenecks. A scale like Bitcoin, with 7 million daily active users, a daily transaction size of $ 9 billion, and a market value of $ 300 billion, has already reached the ceiling. Therefore, it is not possible to use blockchain technology for payment and securities transactions in large economies such as China, the United States, Japan, and Europe.

Blockchain is one of the application technologies produced in the era of digital revolution. If the digital revolution is new productivity, it will inevitably bring a new production relationship corresponding to it. This new production relationship will inevitably have a devastating effect on the original production relationship. And will stay alive for a long time. The commercial bank deposit and loan system and double-entry bookkeeping method that followed the Industrial Revolution can continue for 300 years to this day, which is the embodiment of the vitality of new production relations.

However, bitcoin based on blockchain has been struggling with "old-fashioned dragon clock" ten years after its birth, and it is difficult to continue to expand when there are only a few million users. It can only be explained that blockchain technology only reflects some of the advanced in the digital revolution era. By nature, the full picture of the digital revolution has not been shown. But without the prospect of large-scale application, it is impossible to have a qualitative and revolutionary impact on the transformation of production relations.

By the way, the digital revolution, including blockchain, is a multidisciplinary integration of economics, computer science, cryptography, and law, which is completely different from the traditional way of economics development. Digital technology is used to express the economy. Social science thoughts such as science and law, so if an economist or economic manager does not know how to use digital technology to express economic thoughts and the particularities and technical limitations of economic and social management methods, he will only use those generated in the blockchain The ideal scenario, such as the principles of trust, self-organization, non-tampering, and forgery, and the infinite enlargement of the economic formula, will lead to serious misunderstandings.

For example, the most cutting-edge technologies in the field of blockchain in 2019 are "cross-chain" and "sharding" technologies. The former is to place cryptocurrency transactions outside the chain in a centralized manner, and the latter is to block the entire block. The chain community is divided into countless small areas to run, the purpose is to bypass the bottleneck of transaction speed, but cross-chain technology has returned to a centralized approach, and fragmentation has destroyed the unified consensus mechanism, and various small areas have appeared. The problem of how to generate consensus in a large area. However, in many domestic economists' articles and speeches, they are cheering that the speed bottleneck of the blockchain has been broken, and they do not understand how this breakthrough has failed in the vision of the beautiful production relations that were originally highly expected.

Finally, I would like to say that the prospect of the complete transformation of the production relationship by the digital revolution is not only existing, but also increasingly clear. This is the prospect brought by AI.

The artificial intelligence method generated in the digital age has brought the consensus mechanism and smart contracts into the relationship between people, that is, using machine management to replace traditional human-to-human management, and using machine intermediaries to replace traditional human intermediaries. Status has gradually changed from the traditional trust in people to the trust in machines. Machine trust is a new way of trust. People have selfishness but machines do not. People can forge and tamper but machines do not. Once people's consensus is turned into machine language, it is used to manage human production and trading activities. Previously pure Qualitative changes will occur in the production relationship composed of people.

Why does the distributed ledger construct a trust mechanism? It is because more than 51% of people will not allow counterfeiting, that is, the human subject's consensus is to reject counterfeiting, and the so-called "Byzantine fault tolerance mechanism" is to allow machine intelligence to ensure that even if 49% of people want to counterfeit, This fake cannot be created, and the consensus mechanism can continue to operate. Of course, the consensus mechanism can also be modified, and it can only be changed with the consent of 51% of people. Therefore, the essence of the consensus mechanism is "democratic centralism" implemented by machines.

AI-based consensus mechanisms and smart contracts are not limited to running on distributed networks, and not only blockchain technology can use AI. And for the Internet, centralized and decentralized networks are not the distinction between advanced and backward, but depend on what problems you need to solve with network technology, and whether network technology can solve these problems. When the Internet first came out in the 1980s, because PCs were not fast enough to run large programs, people who wanted to listen to music and watch videos online could only log in to high-performance servers on large websites, but now mobile phones The speed has already caught up with the minicomputers of the 80s, the speed of the PC is faster, and large programs can be run at each node, so the Internet has a technological foundation for distributed development, and the blockchain is here.

However, if the blockchain also has a technical ceiling, such as when Bitcoin has reached 7 million users and a market value of 300 billion U.S. dollars, it will not run on the Internet. If you want to move larger-scale value transactions to the Internet, , You have to go back to the centralized way. But it is not humans that manage transactions, but AI, machine intelligence, and letting machines perform human consensus, which will open up a new world of human production relations. This new relationship is not the traditional human-to-human relationship, but the human-machine-human relationship.

Of course, the centralized approach will also face the problem that the consensus mechanism is tampered with by the centralized network administrator, which involves the question of how to supervise and how to use password technology for protection.

Also, it is not that there is no place for blockchain, and there is a very broad prospect for promoting the use of "alliance chain" among enterprises. In fact, the blockchain that our country currently encourages is the focus of alliance chain.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- What is Freecash (FCH)?

- Super Ledger Executive Director: Supply chain management and trade finance are two major directions for blockchain landing

- Blockchain competition: What are the differences between China and the United States?

- Wall Street predators lose coins, crypto world "lost shares"

- Deconstructing the DeFi ecosystem, and multiple ways for the oracle to optimize the DeFi ecosystem

- DigixDAO dissolution proposal has been passed, will tens of thousands of Ethereum flow into the market?

- Which lending platform is better? We analyzed 8 DeFi platforms for you