Depth | Panorama of Global Digital Currency Regulatory License

Writing | Wang Mengting, Zhao Sheng

Editor | Yu Baicheng

Guide

- DeFi Review: Beyond the critical DeFi network effect

- Netizens broke the news: Reddit is suspected of developing the reward function of blockchain

- Research | Blockchain technology is expected to restructure the international payment model

In order to better grasp the policies of the digital currency industry and predict the future development trends, this article starts with the national regulatory measures for the digital currency industry, sorts out the development details of global digital currency regulatory licenses, and summarizes the digital currency regulatory situation.

1. Status of global digital currency regulation

01 Digital Currency Development Trend

In recent years, with the increasing maturity of blockchain technology and the rapid development of digital currencies, the market size of decentralized encrypted digital currencies is increasing. According to the latest data from CoinMarketCap.com, as of March 31, 2020, there were 319 digital currency exchanges in the world, and 5,290 digital currencies have been issued, with a total market value of up to 181.4 billion US dollars. The top three in market value are Bitcoin and Ether respectively. With XRP, the market value of Bitcoin exceeds 114.8 billion USD.

While the market scale is gradually expanding, the influence of digital currencies is becoming wider and wider. More and more users and institutions are beginning to accept digital currency. The application scenarios of digital currency have already involved many fields of daily life such as shopping, transportation, travel, and travel. In addition, many foreign commercial organizations have successively launched digital currency issuance plans, and many countries such as Canada, China, Sweden, and the United Kingdom are also actively promoting the introduction of legal digital currencies.

Digital currency is becoming an indispensable and important factor in the modern economy with an unstoppable trend.

According to the credit level of the issuer, we may simply divide the current digital currency into three categories, namely, decentralized encrypted digital currency, institutional digital currency and legal digital currency. The digital currency discussed in this article, unless otherwise specified, mainly refers to encrypted digital currency.

Digital currencies are having an impact on the global financial system, creating more possibilities for economic development. However, digital currencies, especially decentralized cryptocurrencies, still have many problems.

1. Network security defense is difficult, and it is easy to cause security risks . Digital currency is based on blockchain technology. In theory, blockchain technology can bring extremely high security to digital currency, but almost all related operations of digital currency need to be based on the Internet. The inherent security problems of the Internet such as hacker attacks , Potential threats such as virus intrusion will be reflected in the encrypted digital currency market. Especially as an intersection between project parties and users, the exchanges connecting the primary and secondary markets of digital currency are often subject to security incidents such as hacker attacks, platform downtime, and user data loss. The most famous exchange theft in history was in March 2014. Japan ’s largest bitcoin trading platform, Mt.Gox, was hacked and lost about $ 365 million worth of bitcoin.

2. Digital currency has anonymity characteristics, which easily lead to illegal activities such as money laundering and fraud . Unlike fiat currencies, digital currency issuance transactions do not need to go through financial institutions, so financial institutions cannot verify the information of transaction users. The traditional financial supervision system is not fully applicable to digital currencies, and criminals will use supervision loopholes to conduct money laundering and other illegal acts. The early development and growth of Bitcoin was inseparable from illegal transactions in the dark web such as the Silk Road.

3. The price fluctuates sharply, the market speculation psychology is serious, and investors' rights and interests are difficult to protect . Since mainstream digital currencies such as Bitcoin are mostly based on open source algorithms, and there is no clear issuing and operating body, no one or institution can control its issuing transactions. As an asset, digital currency lacks the credit guarantee of the state, the currency value fluctuates greatly, and consumers are prone to speculation. Faced with the open digital currency market, cross-border investment is inevitable. At this time, due to the regulatory gap between countries, the rights and interests of investors cannot be guaranteed, and illegal fund raising may occur, forming a high-risk cross-border investment market.

The emergence of digital currency is a challenge to traditional currency finance. How to balance digital security and privacy protection, how to effectively supervise digital currency, and protect the rights and interests of various parties are all issues that governments and regulatory authorities of all countries need to think about and solve.

International financial institutions have always kept a close eye on digital currencies. The Bank for International Settlements has issued guidance and suggestions on the payment function of digital currency and whether the digital currency has monetary attributes. In November 2015, the Bank for International Settlements released the "DigitalCurrencies" report detailing the impact of digital currency as a retail payment method. In March 2018, the Bank for International Settlements released the "Central Bank Digital Currency for Payment, Monetary Policy and Financial Stability The report of "The Impact" analyzes the issuance of digital currency by the Central Bank. In June 2017, the International Monetary Fund (IMF) released a report "Fintech and Financial Services: Initial Considerations" on the development of the fintech industry, focusing on how to effectively regulate distributed ledger technology (DLT) and its foundation. Digital currency made recommendations. In 2018, the Organization for Economic Cooperation and Development (OECD) and the G20 G20 jointly released an interim report, "Tax Challenges Brought by Digitalization", which proposed the supervision of digital asset transaction information formed by cryptocurrencies and blockchain technology.

In addition to international financial organizations, national regulatory authorities are also paying attention to and actively studying digital currency regulation. As different countries have different financial environments, countries have different attitudes towards digital currency supervision. Some countries, such as the United States and Japan, hold a supportive attitude and actively deploy regulatory measures in the digital currency industry. However, some countries, such as India, currently prohibit digital currency related business within the territory.

The following is the regulatory situation in some countries :

The United States : Different states have different attitudes towards digital currencies. New York State has strict control over digital currency exchanges, and currently only a small number of exchanges have obtained authorizations; Washington State enacted Act 5031 in April 2017, which requires all currency exchanges in Washington State, including virtual currency operators, to You must apply for a license to operate. Currently, many exchanges operating in Washington State have obtained the relevant licenses. Other states are also actively taking measures under the regulations of the US Securities Regulatory Commission to implement license management of digital currency transactions.

Japan : Japan is the first country to incorporate digital currency transactions into the legal system. In 2017, Japan began to implement the "Funding Settlement Act", recognizing the legality of digital currency as a means of payment. After that, the Japan Financial Services Agency (FSA) promulgated the "Payment Service Act" to implement comprehensive supervision of digital currency exchanges. All exchanges operating in Japan must obtain license authorization from the Ministry of Finance and FSA.

Singapore : Under the guidance of the Singapore government ’s principle of “not seeking zero risk and stifling technological innovation”, Singapore actively develops blockchain technology and actively promotes the development of digital currency. One of the countries. Due to Singapore's positive and good institutional environment, many exchanges have chosen to conduct business in Singapore. For example, WBF EXCHANGE has worked closely with the Singapore government.

In March 2020, the Monetary Authority of Singapore (MAS) officially announced the list of exempt enterprises for payment service business licenses. The entities on the list have obtained licenses and operating rights for specific payment services or digital currency related payment services during the exemption period. Singapore entities including Alibaba, Alipay, Amazon and other large institutions are on the list.

Regarding the exempt licenses for digital currency-related payment services, including Binance, OKCoin, BitStamp, Binxin, Coinbase, CoinCola, TenX, Upbit, ZB and other nearly 200 companies can legally operate in an exempted state before the license is officially issued.

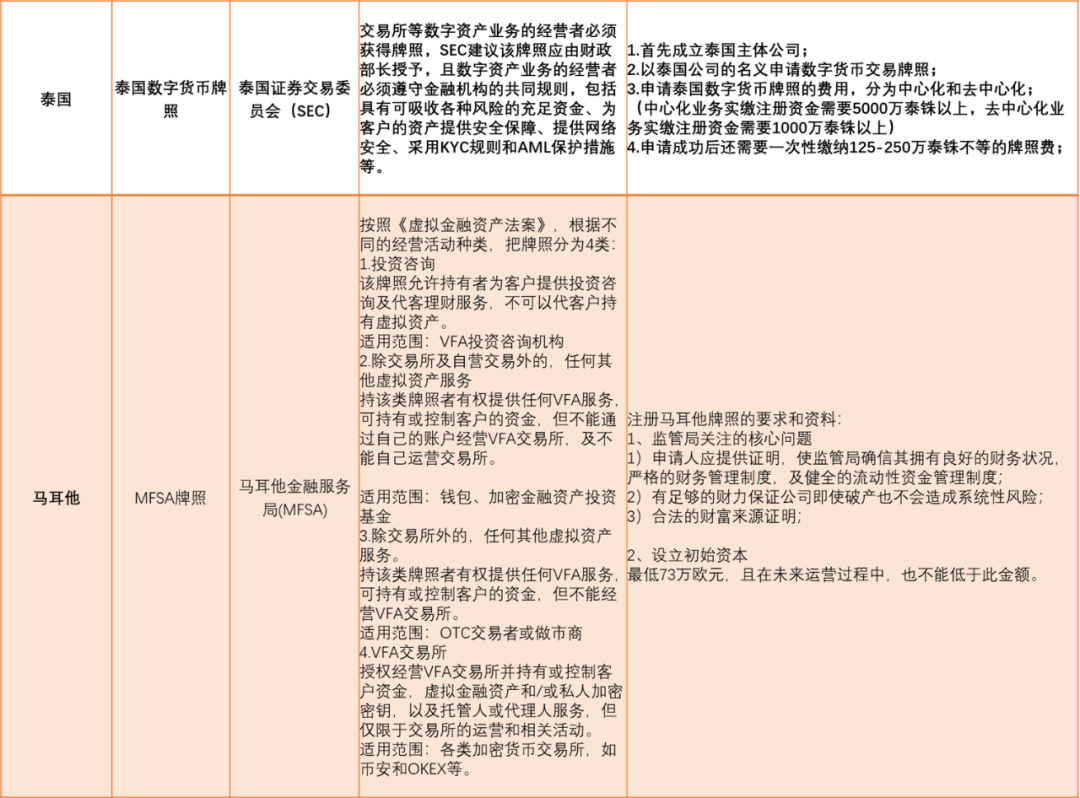

Thailand : In order to better regulate the digital currency industry, in June 2018, Thailand promulgated the "Digital Assets Law", announcing the issuance of licenses for compliant cryptocurrency exchanges and beginning to implement license management.

Australia : Due to increasing financial crimes, in October 2017, Australia passed the "Financial Bill 2017 Amendment (2017 Measures 6)", and at the end of 2017, the "Anti-Money Laundering and Anti-Terrorism Financing Act 2017 Amendment" was formally It is clear that digital currency is not a monetary asset, but an electronic manifestation of value.

Institutions that provide digital currency trading services must submit an application to the Australian Transaction Reporting and Analysis Center (AUSTRAC) to obtain corresponding regulatory licenses and entry permits. Exchanges should conduct anti-money laundering and anti-terrorism financing assessments of their businesses in accordance with the system standards under the anti-money laundering / CTF framework. Those who violate the rules will be sentenced to two years in prison or a fine of 500 pounds. Those in serious cases will be sentenced to seven years in prison or a fine of 2000 pounds.

Russia : At the end of December 2017, the Russian Central Bank drafted a proposal for a new multinational cryptocurrency. The proposal hopes to join the BRICS and the Eurasian Economic Union (EEU) to create a new multinational cryptocurrency that can be legally circulated among member countries.

Germany : Germany was the first country to recognize Bitcoin. In August 2013, the German government officially recognized Bitcoin as a legal currency. Cryptocurrency owners can use Bitcoin to pay taxes or for other purposes. The German Federal Financial Supervisory Authority (Bafin) stated that the regulation of encrypted digital currencies should comply with the requirements of the current financial regulations. Enterprises that issue digital tokens must comply with the provisions of the Banking Law, Capital Investment Law, Insurance Supervision Law, and Payment Services Supervision Law.

Canada : Canada has always been friendly to mainstream digital currencies such as Bitcoin and Ethereum. A local Canadian company specializing in cryptocurrency investment has obtained its first Bitcoin fund license. However, regarding the crime of digital currency, the Canadian federal government proposed in 2018 to take measures against shadow payments made by terrorists and money launderers using virtual currency and prepaid credit cards.

Philippines : The Central Bank of the Philippines (BSP) has been deploying digital currency exchanges to be regulated since February 2017, hoping to regulate this emerging market and promote its orderly development. In 2019, the central bank issued the first batch of exchange permits in this area.

Nestor Espenilla Jr, governor of the country ’s central bank, said, “The base of cryptocurrency exchanges is small but growing rapidly – that ’s why we decided to let them register and the central bank is actively incorporating the exchange into the central bank ’s regulatory framework. "

Malta : As the smallest EU member state, Malta is one of the regions with the most friendly attitude towards digital currencies. Malta has repeatedly expressed its welcome to the entry of digital currency exchanges. At the same time, Malta has actively formulated sound rules and regulations for the industry.

In April 2018, the Malta Cabinet approved the submission of three bills, one of which is the Virtual Financial Assets Act, which provides a regulatory framework for cryptocurrencies. The other two bills are the Malta Digital Innovation Authority Bill and the Technology Arrangements and Services Bill.

According to the regulatory measures of some of the above countries, it is not difficult to find that when many countries conduct digital currency supervision, most of them choose to use licenses to supervise digital currency related industries. The digital currency supervision license is a prerequisite for the relevant enterprise institutions in the digital currency industry chain to enter the market. Only by obtaining a regulatory license can an institution be able to conduct digital currency-related businesses and services in compliance with local regulations, such as setting up digital currency exchanges, trading, and issuing digital currency financial derivatives .

Various countries have different requirements for license applications, and some countries and regions even require securities, bank, and fund-related licenses to be applied for at the same time. However, it is clear that with the in-depth understanding and exploration of the blockchain and digital currency markets in various countries, the relevant legal system of digital currency is gradually improving and moving towards compliance.

2. List of major global digital currency regulatory licenses

With the advancement of technology, money laundering and fraud crimes are becoming increasingly difficult to monitor and blame in time. Emerging payment tools and business models are increasingly blurring the regulatory boundaries of existing bills. The lack of a global response mechanism has exacerbated this situation. Therefore, as a gray area of supervision, regulators cannot always allow encrypted digital currency to be free from the regulatory system, especially in the context of the increasing size and influence of the encrypted digital currency market today.

Secondly, the regulatory agencies are willing to issue licenses to digital currency related institutions, which also reflects that the regulatory authorities are gradually recognizing and accepting digital currencies. Digital currency regulatory licenses can raise the threshold of the digital currency industry and increase industry value and social recognition.

Although the relevant laws and regulations in different countries are different, the supervision of digital currency related businesses by issuing digital currency regulatory licenses can protect the rights of investors to a certain extent and maintain the order of the financial market. Having a digital currency license is equivalent to having a business operation license. On the one hand, the regulatory license can supervise the organization's compliance with the digital currency-related business and avoid risks. On the other hand, it can enhance the image and credibility of the exchange and increase investor confidence. Accelerate the development of platform business and provide investors with more diversified services.

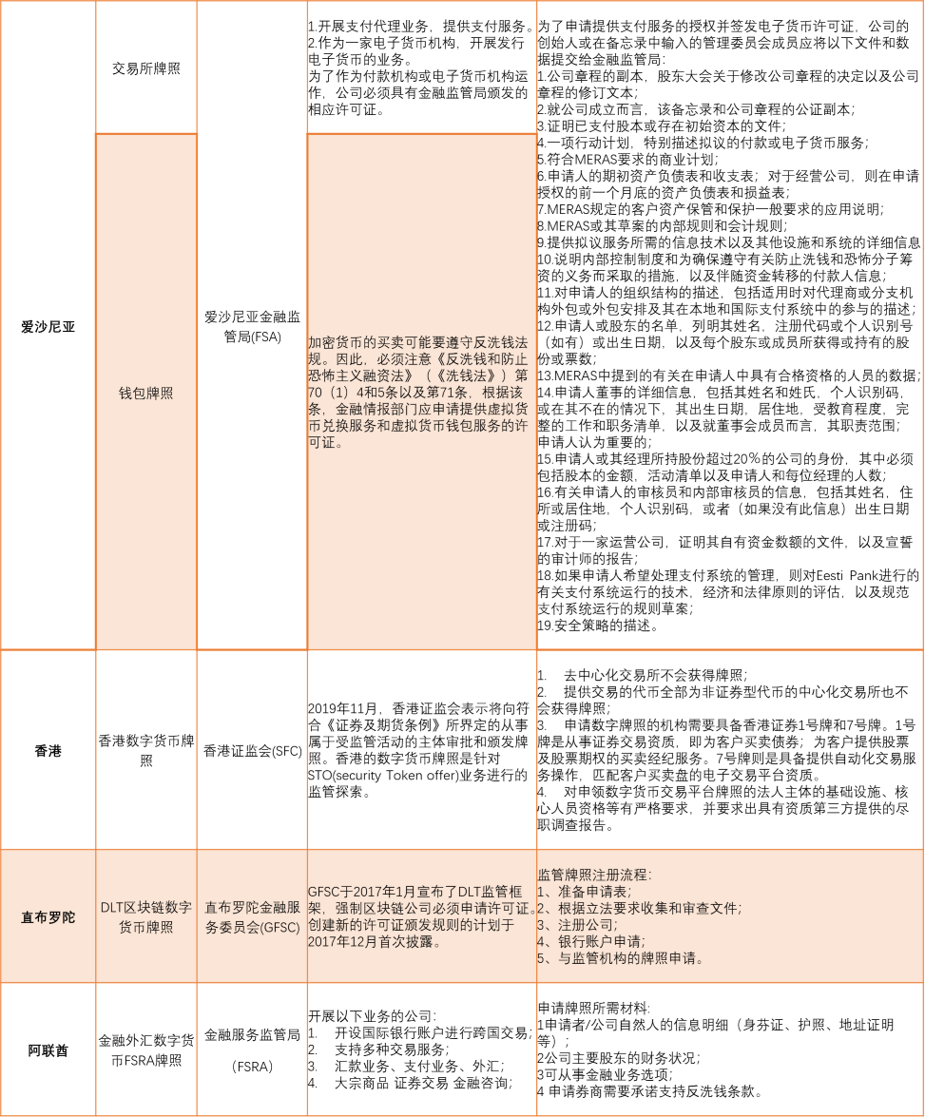

According to incomplete statistics of Zero One Think Tank, the current major global digital currency related regulatory licenses are as follows:

In general, most of the digital currency licenses in various countries are issued to registered enterprises in the host country. The main regulatory bodies are companies that provide digital currency transactions and digital wallet services. The main regulatory purposes are anti-money laundering and anti-terrorist organization financing.

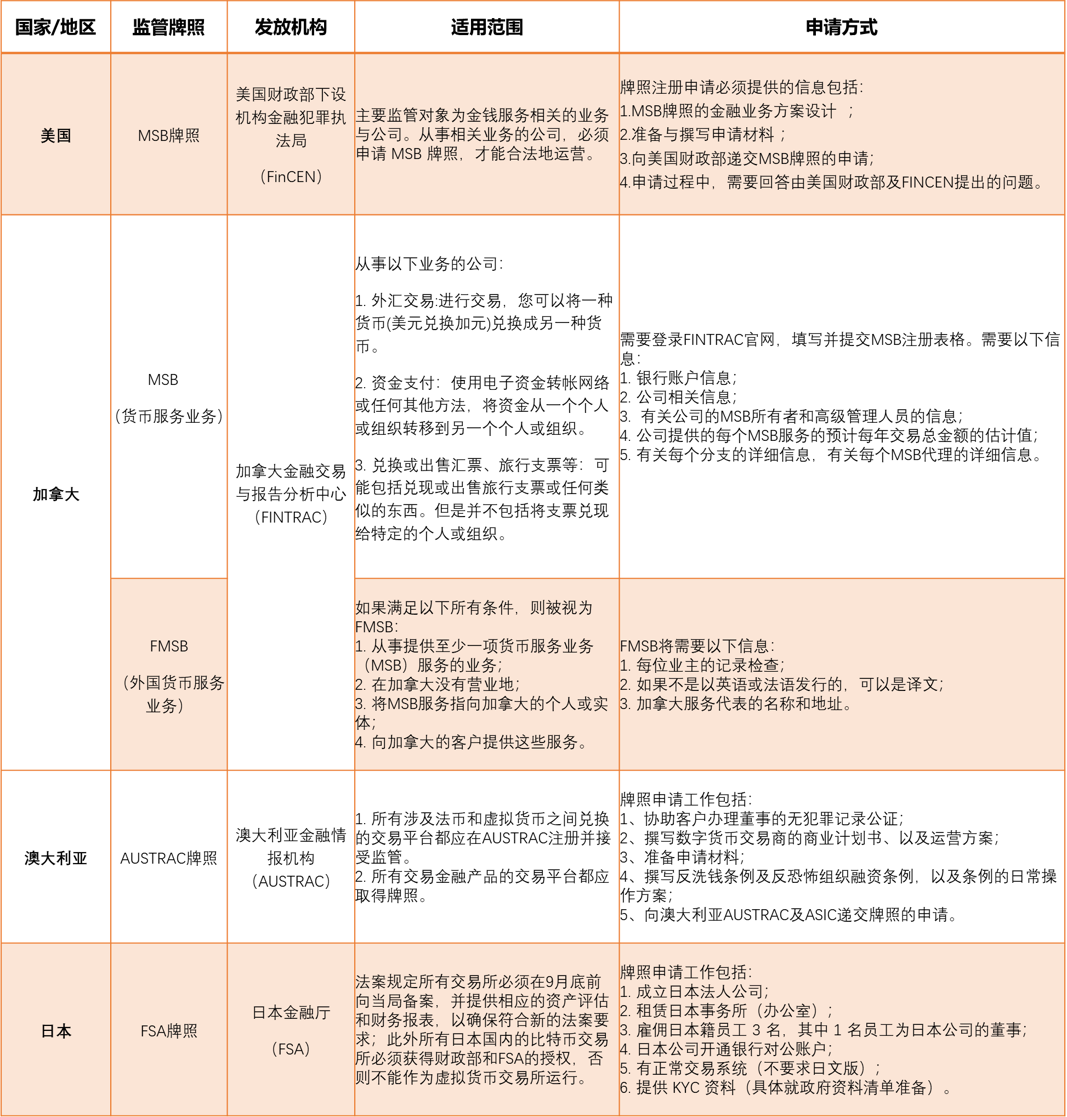

1. US MSB license

The US MSB license is supervised and issued by the Financial Crimes Enforcement Agency (hereinafter referred to as FinCEN) under the agency of the US Treasury, and is a registration and licensing system. Its main supervision objects are engaged in business and companies related to money services, including international remittances, foreign exchange, currency transactions (including digital currencies), and provision of prepaid items.

The registrant of the MSB needs to be registered as an entity of the money service business (MSB) in accordance with the provisions of the Bank Secrecy Act (BSA) of 31 CFR 1022.380 (a)-(f), which is managed by FinCEN.

All MSB registrations must be completed electronically through the BSA electronic filing system. The information submitted by the organization when registering the MSB should include:

1. The legal name of the registrant;

2. The name of the registrant's "business" (if applicable);

3. The address of the registrant;

4. MSB activities undertaken by registrants;

5. Explain that the registrant is engaged in MSB activities;

6. Number of branches;

7. The date of signing the registration form;

8. The date the registration form was received.

With few exceptions, every money service company (MSB) must be registered with the Ministry of Finance. If the person who participates in the MSB because he is an agent of another MSB, there is no need to register. The money service business registration form (FinCEN Form 107) must be completed and signed by the owner or controller, and submitted within 6 months after the establishment of the MSB. The registration must be renewed every two years, and under limited circumstances must be re-registered. FinCEN will impose fines, civil penalties and criminal penalties for violations.

Companies conducting business must comply with federal regulations to register as MSB, and the states that also comply with remittance activities must also comply with state regulations. Currently, 53 states and regions have licensing requirements. The cost of their fees mainly includes guarantee fees, application fees, and permit Fees, investigation fees and other expenses.

Application conditions:

1. More than one company director and shareholders (natural or legal persons without international restrictions), valid identification documents (identity card or passport).

2. There is no restriction on the company name, as long as there is no duplicate name in the search.

3. Different states have different registered capital, generally USD 50,000, no capital verification and no need for investment. When registering a company, it is necessary to state the amount of shares issued when the company was established. Usually, the company initially issues 3,000 to 50,000 shares.

4. The percentage of shares held by each shareholder applying for registration of a US company.

5. It is required to have a local registered address.

The US MSB is currently the most cost-effective license, Huobi, Binance, and Nui Tuan all have this license to operate, and the application speed is faster and the popularity is higher.

2. Canadian Regulatory License

The Canadian digital currency regulatory license is reviewed and issued by the Canadian Financial Transaction and Report Analysis Center (FINTRAC). The license is divided into MSB and FMSB. According to relevant regulations, engaging in money service related business (MSB) needs to register with FINTRAC and obtain a compliance license. As of June 1, 2020, foreign currency service companies (FMSB) must be registered with FINTRAC.

Canadian MSB can provide the following services to the public:

1. Foreign exchange transactions: For transactions, one currency (US dollars to Canadian dollars) can be exchanged for another currency;

2. Fund payment: Use the electronic fund transfer network or any other method to transfer funds from one individual or organization to another.

3. Exchange or sale of money orders, traveler's checks or anything similar: this may also include cashing out or selling traveler's checks or anything similar. This does not include cashing checks to specific individuals or organizations.

MSB application requirements:

1. There must be a company incorporated in Canada;

2. Have proper business structure, good internal monitoring system, and company personnel have certain qualifications and experience in the digital currency industry;

3. There are compliant anti-money laundering reports that meet the requirements;

4. Comply with Canadian laws and business rules.

If all the following conditions are met, it is considered FMSB:

1. Engaged in providing at least one money service business (MSB) service;

2. There is no place of business in Canada;

3. Point MSB services to individuals or entities in Canada;

4. Provide relevant services to Canadian customers;

If it belongs to FMSB, as of June 1, 2020, the company needs to fulfill the following obligations:

1. Register business with FINTRAC;

2. Report certain financial transactions to FINTRAC;

3. Keep certain transaction records;

4. Identify customers;

5. Develop a compliance plan.

At the same time, the FMSB must verify the identity of its customers for certain activities and transactions in accordance with the prescribed criminal proceeds (money laundering) and terrorist financing regulations (PCMLTFR). Starting June 1, 2020, the company needs to verify the identity of its customers in order to submit a suspicious transaction report (STR) to FINTRAC. Before submitting an STR, reasonable measures must be taken to identify individuals who conduct or attempt to conduct suspicious transactions.

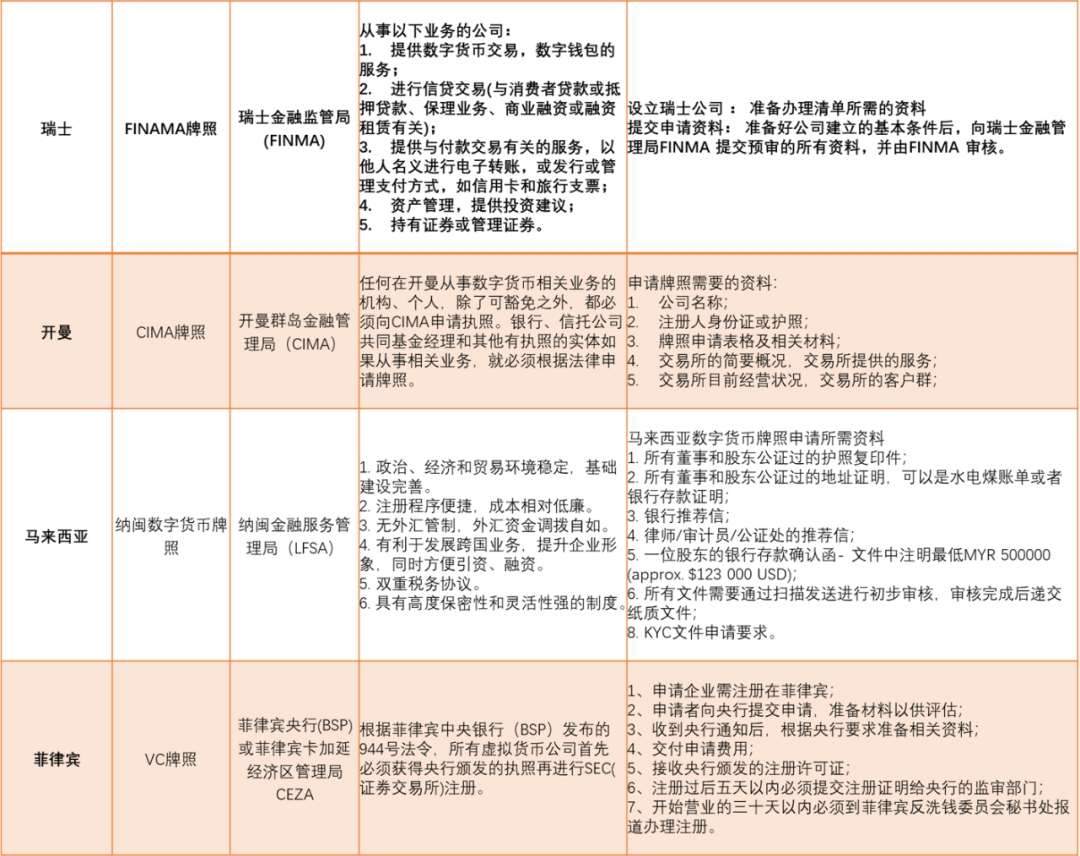

3. Swiss FINAMA license

The Swiss FINAMA license is issued by the Swiss Financial Supervisory Authority (FINMA), and the Swiss government has always been open to digital currencies. The regulation of digital currency is mainly to prohibit money laundering, so the digital currency used in the transfer industry is subject to key supervision.

According to the relevant regulations, the company applying for a digital currency license must be a Swiss company. Therefore, the first step in applying for a license is to establish a company in Switzerland. In addition, it also needs to meet:

1. The company must have two Swiss resident directors;

2. The company's registration category is SA / AG / PLC [1];

3. A deposit of 100,000 francs, of which 50,000 Swiss francs will be frozen when the company is registered, and will be unfrozen after the company registration is completed. The company needs to keep a minimum deposit of 100,000 Swiss francs in the account;

4. The relevant information of the registrant needs to be submitted.

According to regulations, after setting up a company, you need to open a Swiss public account, lease a Swiss office, and hire Swiss employees, and then you can submit relevant information for a license application. The total application duration is about 7-10 months.

After obtaining the license, the business scope that Swiss digital currency company can operate includes:

1. The company can provide digital currency transactions, digital currency libraries, and digital wallet services; secondly, it can provide the following other services:

2. Conduct credit transactions (related to consumer loans or mortgages, factoring business, commercial financing or financial leasing);

3. Provide services related to payment transactions, make electronic transfers in the name of others, or issue or manage payment methods, such as credit cards and traveler's checks;

4. Trade in the customer's own name, or trade in currencies, currency market instruments, foreign exchange, precious metals, commodities, securities (stocks, stocks, value rights) and their derivatives;

5. Asset management;

6. Holding securities or managing securities;

7. Provide investment advice.

FINMA issued its first regulatory license in October 2017 for a bitcoin company Moving Media. The company is a direct secondary financial intermediary (DSFI) registered in Switzerland. Obtaining a compliance license means that the company strictly complies with AML and KYC regulations.

3. Suggestions and Challenges of China's Digital Currency Regulation

The diversified supervision of various countries is promoting the gradual compliance of the digital currency industry, and the digital currency industry has gradually developed into one of the important factors of the economy in the new era. At present, China's digital currency is constantly developing. China began to study digital currency as early as 2014. By 2019, China's central bank legal digital currency has basically matured in technology and operational framework. Entering 2020, despite the double impact of the epidemic and the economic downturn, the central bank's digital currency is expected to accelerate its landing and provide new vitality to China's financial market. But it is undeniable that the overall industry of digital currency-related industries is still in the early stages of development, and at the same time, China's supervision in related fields also has a certain lag compared with international advanced practices.

The traditional currency supervision ideas and methods have been unable to meet the development needs of encrypted digital currencies. The supervision of digital currencies in various countries may be able to bring some enlightenment. Regulators can seek technological and methodological innovations. In the context of digital currencies becoming a megatrend, China may need to seek a new balance between regulatory compliance and technological innovation, to a certain extent and to a certain extent to allow relevant digital currencies Innovation and breakthrough.

Among them, the supervision sandbox method of the British Financial Conduct Authority (FCA) in 2015 is worth learning. The regulatory sandbox can provide a buffer for the development of the national digital currency. The regulatory sandbox can be regarded as a "test field". When the regulatory system is not clear, it provides a relatively controllable environment for some institutions that conduct digital currency business Conduct pilot operations. At the same time, it accepts the supervision of the supervision department and the detection of related subjects to ensure that the risks are controlled within a certain range and will not cause harm.

In fact, China has already piloted the sandbox method of supervision. The blockchain financial plan officially launched in China in 2017 is the first domestic sandbox plan to be launched by the government as the leader. Hong Kong, China currently implements a regulatory sandbox, and has launched digital currency related licenses. It is believed that after comprehensive considerations in various aspects, China will also launch a set of digital currency regulatory policies that meet China's national conditions.

[1] AG and SA are "share companies". The name of the company including AG is mainly Germany and Switzerland, and SA mainly appears in France, Switzerland, Belgium, Luxembourg, Italy, Spain, Portugal, Panama, Argentina, Mexico and Chile; PLC is Public Limited Company, which means public offering company , Can be understood as a listed company.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- 930 days, witness the blockchain speed of Xiong'an New District

- The Secret History of Bitcoin: Bitcoin and Space Travel

- MOV announces the first list of federal nodes, from open applications to open ecosystem

- Analyst: Bitcoin is picking up steadily and may hit a record high in the coming months

- Bitcoin Technology Weekly 丨 Lightning Network usher in a major update, the 0.168 BTC channel limit will disappear

- QKL123 market analysis | BCH computing power switch, BTC computing power soars, what will happen to BSV tomorrow? (0409)

- Depth | How to invest in blockchain infrastructure in a macro cycle?