Detailed explanation of the new blue ocean of crypto asset derivatives: options trading

Source: blockVC

Editor's Note: The original title was "The New Blue Ocean of Crypto Asset Derivatives, Detailed Explanation of Options Trading"

Foreword

At the end of 2017, two US exchange giants, CME and CBOE of Chicago Board of Trade, successively launched Cash Settled Bitcoin futures. For the first time, traditional financial markets have publicly traded digital currency derivatives.

However, in the past two years, the performance of the digital currency market has not continued the previous feverish bull market, and the futures products launched by the two exchanges have not received the favor of the market. CBOE has stopped the new Bitcoin contract The listing actually closed the Bitcoin futures trading market. But with the addition of new players Bakkt in 2019 and the launch of Bitcoin options, the market has renewed interest in Bitcoin derivatives.

- Central bank digital currency industry chain carding: more than 20 companies participated, most of them have been listed

- Hackers demand bitcoin ransom in Johannesburg. When is Bitcoin Ransom?

- Introduction to Blockchain | Centralized exchanges continue to thunder, what are the advantages of DEX?

This article, as the first of a series of research reports on digital currency derivatives, will start with Bakkt's newly launched Bitcoin options products, and will use several articles in the future to systematically conduct financial products in the digital currency derivatives market description.

Options Product Introduction

What are options?

Option is a kind of financial derivative (Derivative), which represents the right to choose and trade the selected subject matter. The subject matter can be stocks, commodities, foreign exchange, interest rates and other underlying assets.

When the option buyer pays premium, he has the right to buy or sell a certain amount of the subject matter at the strike price to the option seller at a specific time or at a specific time. This right is called Options.

If this right is to buy the subject matter, it is called Call Option, referred to as call option; if this power is to sell the subject matter, it is called Put Option, referred to as call option. Like futures contracts, option contracts also have expiration dates. If the buyer can only choose to exercise the right on the expiration date, the option is called a European option; if the buyer has any day on or before the expiration date The option that can be exercised is called the American Option.

Whether it is a call option or a put option, their buyers pay a certain amount of premium at one time to obtain the right to buy and sell at a fixed price. The biggest difference with futures contracts is that option buyers do not bear Obligations only enjoy rights, while option sellers have obligations but no rights. When you become short or long in a futures contract, you also bear the rights and obligations, that is, you can complete the delivery with the opening price, but you must also complete the delivery with the opening price, so the correlation between the futures contract and the spot price curve It is very high, almost 1, the withdrawal of the spread is a time cost of financing. However, the option buyer does not bear the obligation, that is, when the price moves in the opposite direction to the expected, the buyer can choose not to execute the contract and only lose the option fee spent on the purchase of the option, and all the gain of the option seller is the premium of the sold option , The buyer needs to perform the contract obligations unconditionally when exercising the right.

History of options

The prototype of modern options appeared in the tulip bubble period of the Netherlands in the 17th century.

Due to the limited supply of tulip bulbs, pure spot trading has been unable to meet the frantic speculative demand, so options with high leverage characteristics were born at this time, magnifying the efficiency of capital utilization in the market, and deriving many transactions that could not have occurred. At the peak of the tulip bubble, the tulip market in the Netherlands has grown to the point where there is no physical transaction, because the growth rate of tulip bulbs cannot keep up with market demand. At this point, a fully cash-settled contract appears, and the buyer and seller only settle the difference between the spot price and the contract's performance price at maturity. When the tulip bubble ended, the price plummeted, put buyers demanded performance and settled the profits of the tulip bulb. However, the put seller's funds were limited and could not be fulfilled. In fact, it was technically bankrupt. The market collapsed.

Options contracts in modern financial markets originated in the over-the-counter options market created by Russell Sage in Chicago in 1872, but did not become active until the Chicago Board of Trade (CBOT) launched overnight options products. In 1932, the "wheat plunge" in CBOT led to the United States banning all commodity-related on- and off-exchange options in the Commodity Exchange Act of 1936, and the pace of options development slowed down again.

In 1973, under the organization of the Chicago Board of Trade (CBOT), the Chicago Board of Trade (CBOE) was established. This marks the formal development of options trading into a unified, standardized and standardized all-round development stage. In order to avoid repeating the tulip bubble, the Chicago Board Options Exchange added an independent third-party clearing and settlement agency Options Clearing Corporation (OCC), which greatly reduces the performance risk of option buyers.

Driven by the US option market, countries around the world have begun to prepare their own option trading markets, and introduced option trading into agricultural products and energy futures, which has greatly promoted the development of commodity options. As the United States, the United Kingdom, Japan, Canada, Singapore, the Netherlands, Germany, Australia, and Hong Kong, China have successively established options trading markets, options trading has also expanded from a single stock to a variety of commodities, financial securities, foreign exchange and gold Nearly 100 varieties including silver.

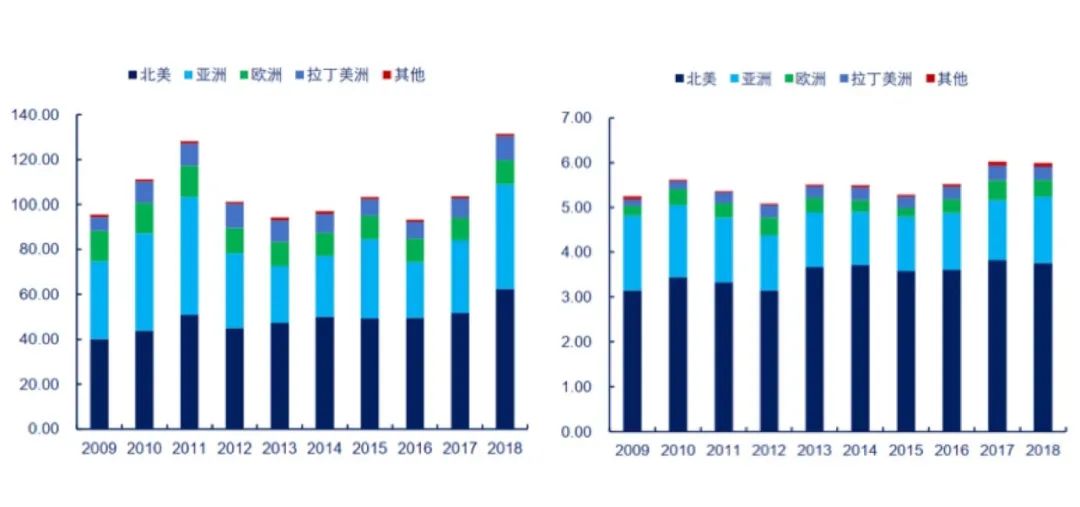

Global options volume (left) and positions (right) (100 million contracts) by region Source: FIA, CITIC Futures

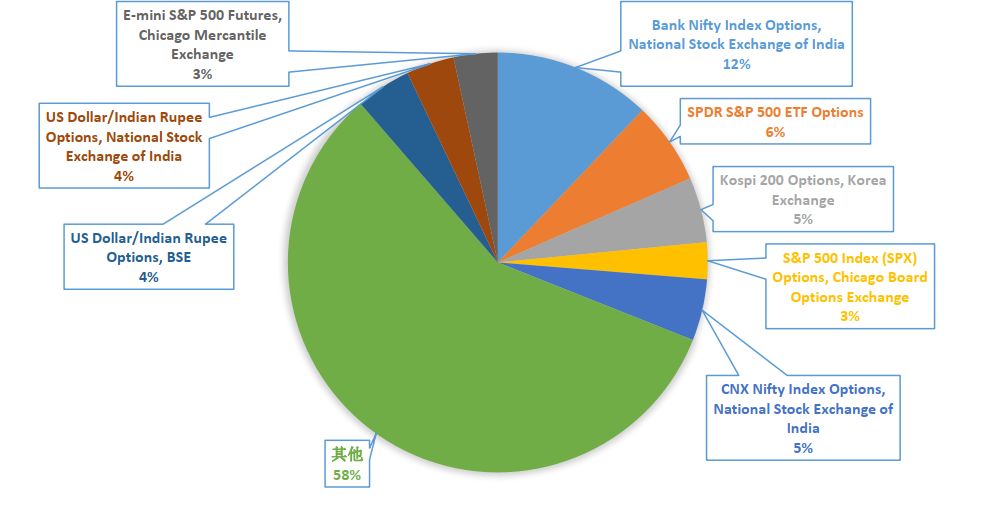

From the perspective of the proportion of trading volume of the major options in the world, the head effect of the distribution of options volume is more obvious. The trading volume of the top four options in 2018 has already accounted for 28% of the total trading volume of global options. Among them, the largest single option trading volume in the world is the Bank Nifty index option from India's NSE, with a trading volume of 1.587 billion, accounting for 12%. The second is CME's E-Mini S & P 500 futures options, with 835 million contracts accounting for 6%.

Proportion of global major options trading volume (100 million pieces) Source: FIA, CITIC Futures

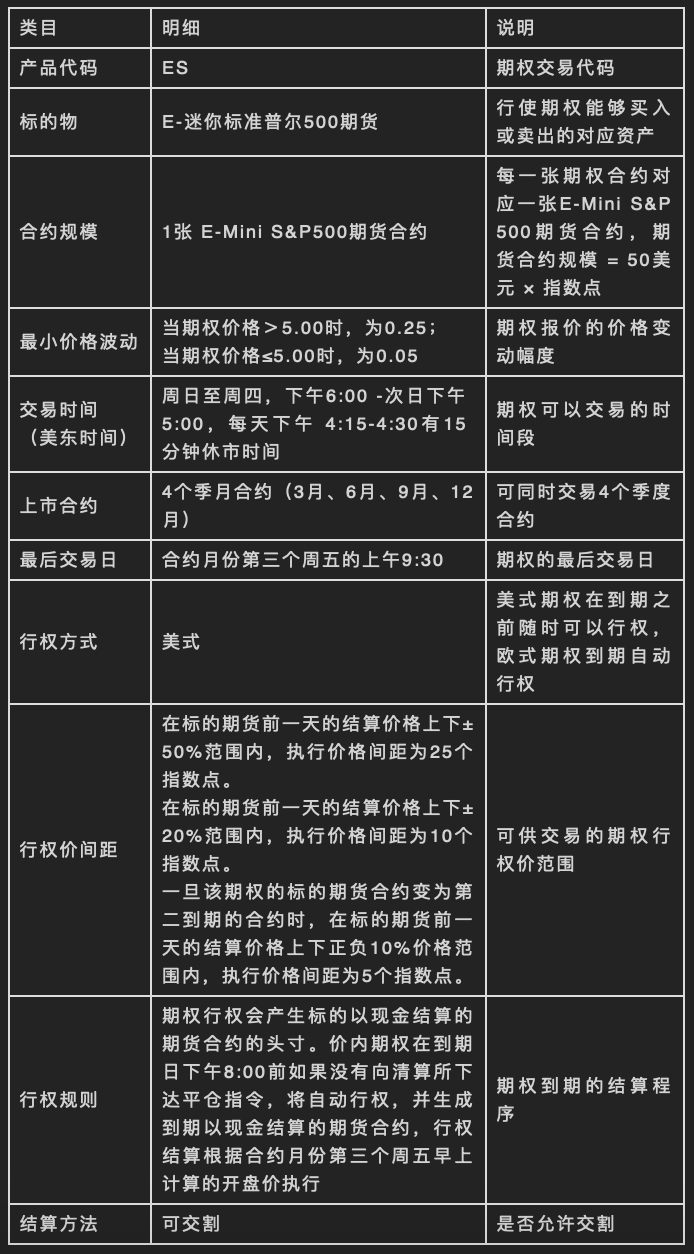

Elements of an option contract

Like futures contracts, option contracts traded on the exchange have clear contract specifications. The following takes the Chicago Mercantile Exchange CME's fist trading product E-Mini S & P 500 futures options as an example to explain the standard option contract elements.

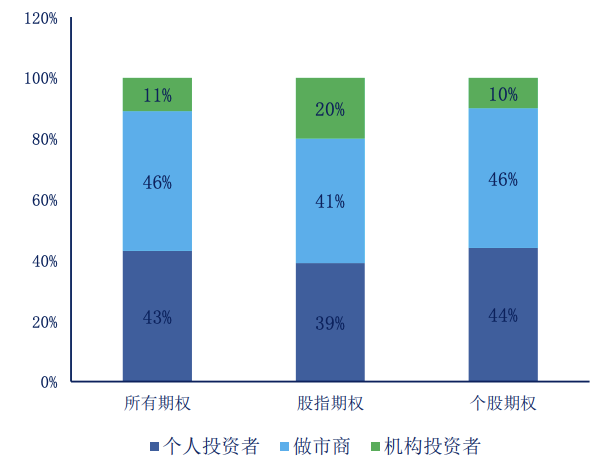

Participant structure of the options market

The options market is an institution-led market . Taking the US options market as an example, the main participants are: exchanges, options clearing companies (OCCs), options market makers, e-commerce companies, institutional investors, individual investors, and market regulators. Institutional investors (including market makers) are dominant, accounting for about 57% of the market, and individual investors account for 43%. Among them, the largest trading volume is market makers, accounting for 46%. Market makers provide good liquidity for the entire market. In terms of classification, there are relatively more institutional investors in the stock index options market, accounting for 20%; while in the individual stock options market, the proportion of human investors has increased, accounting for 44%.

Investor structure in the US options market Source: OCC, CITIC Futures

Digital currency options

The digital currency options market is currently at a very early stage. There are mainly two types of digital currency options trading venues on the market. One is the native digital currency options exchange, such as Deribit and OKEx; the other is based on traditional fiat currency exchanges Bit trading products such as Bakkt and CME. In addition to over-the-counter trading, there are many institutions and traders who will participate in digital currency options trading as counterparties to over-the-counter trading.

Native digital currency options

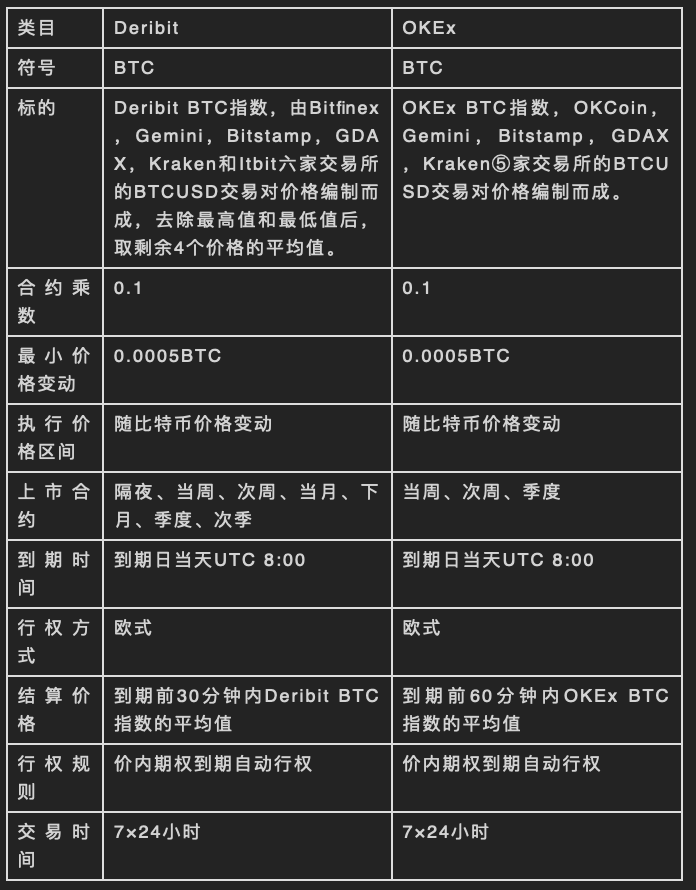

The earliest exchange to launch digital currency options was Deribit. This Dutch-based derivatives exchange was created by professional investment bank traders in 2016. It was not until four years later in 2020 that OKEx, the leading player in digital currency derivatives, launched. With reference to competitors' options trading products, it has become the two largest digital currency options exchanges in the market.

Deribit and OKEx options trading volume and position data source: Skew

Contract rules

For the first time, Deribit provided a standard option product for settlement through Bitcoin and the corresponding risk control rules. As the trading venues of digital currency options were completely blank at the time, it gained a certain popularity in the bull market in 2017 and has a good reputation. Trading volume performance. OKEx's recently launched bitcoin options products, except for slight differences in details, basically follow the Deribit option product rules.

Data source: OKEx official website, Deribit official website

Data source: OKEx official website, Deribit official website

Although Deribit options are settled through BTC, they are not the same as the currency-based reverse contract formation mechanism familiar to everyone in the market. The core difference is that the face value of the reverse futures contract is denominated in US dollars, while the face value of the option contract is bitcoin denominated, that is, Deribit's option contract actually has a similar contract mechanism with the current forward futures contracts that are popular in the market . Deribit's option contract quotes use BTC as the price unit, and the face value is also BTC as the price unit. In fact, the meaning of the price is the percentage of premium (premium) to the face value. It is intuitive to understand how much 1BTC is paid. To obtain the right to buy or sell 1BTC at a fixed strike price at a certain time in the future, this quotation method actually matches the direct calculation result of the Black-Scholes model, which is the theoretical pricing model of options. But compared to the traditional financial market options that are settled directly in fiat currency quotes, a new risk is actually introduced here, that is, the risk of price changes of the premium and margin relative to the fiat currency price.

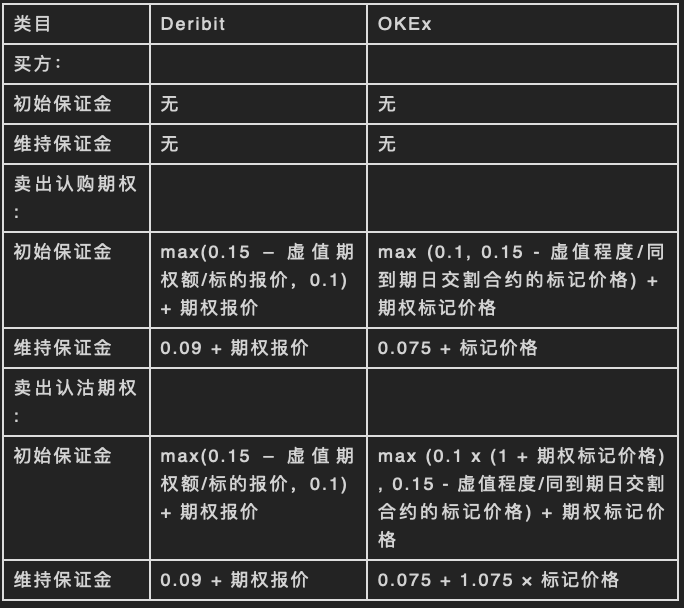

Risk control mechanism

The risk control mechanism of options is quite different from the risk control mechanism of options, and there are different risk control rules for buyers and sellers. The buyer of the option is the right party and does not bear any obligations, so the buyer of the option does not need a deposit, and all risks have been transferred at one time by purchasing the option when the option is purchased; the seller of the option is an obligor and needs to hold sufficient margin It has been ensured that sufficient funds are available to pay the buyer's exercise spread when the option is settled.

Source: OKEx official website, Deribit official website

Transaction rate

The calculation of the option's transaction fee rate is based on the percentage of the nominal value of the underlying value of the option contract, and the proportion of the premium to the nominal value is usually small, so the commission: the proportion of the premium is often large.

Deribit's open retail account rate is uniformly 0.04% and does not exceed 12.5% of the premium.

OKEx's option fee rate is similar to other derivatives on the platform and supports tiered fee.

Source: OKEx official website

Fiat digital currency options

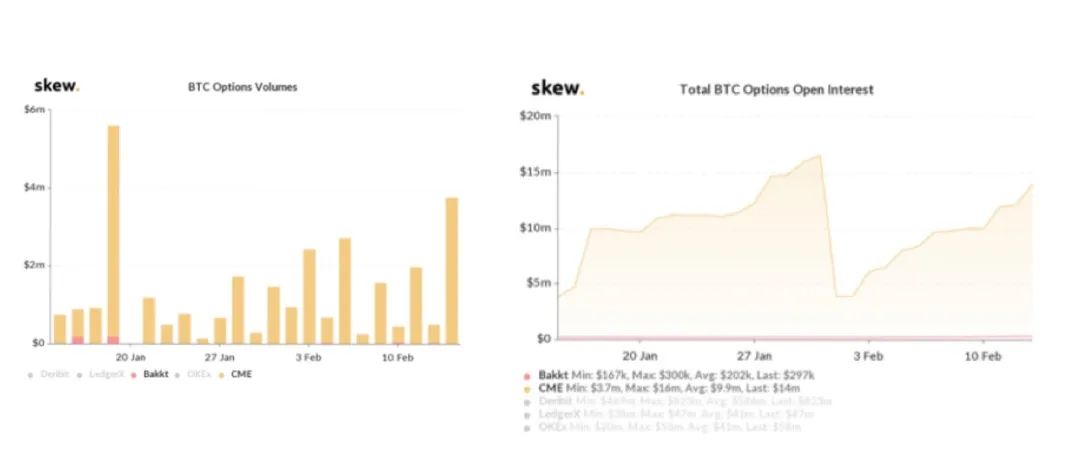

Intercontinental Exchange ICE as the major shareholder of the digital currency exchange Bakkt is the world's first fiat currency exchange to launch publicly traded Bitcoin options products, followed by CME also released its options trading products, although CME's option products were released later, However, from the perspective of volume and open interest, both are far ahead of competitors Bakkt.

CME and Bakkt options trading volume and position data source: Skew

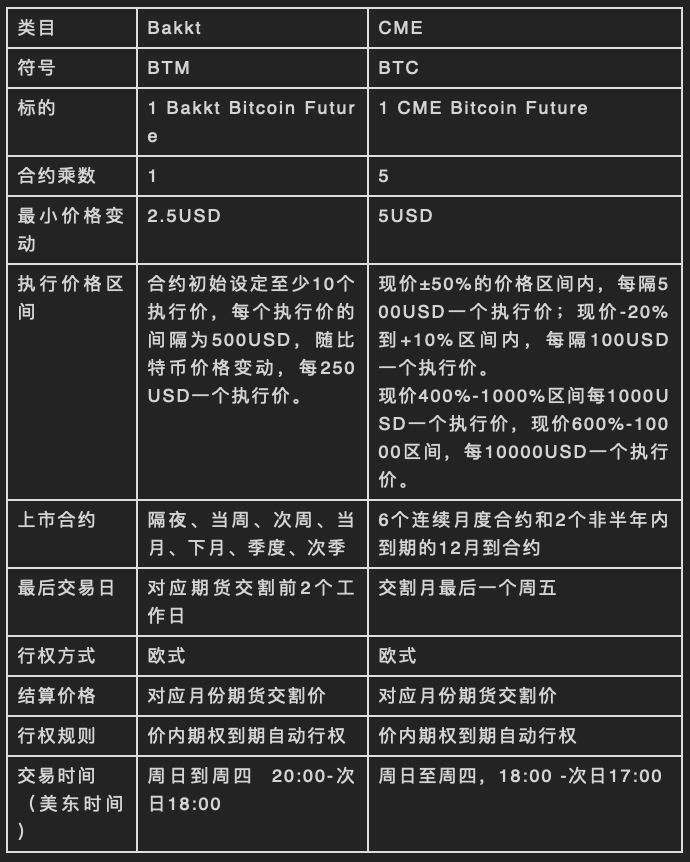

Contract rules

Both Bakkt and CME release USD-denominated Bitcoin option products with contract rules similar to traditional commodity futures products.

Data source: ICE official website, CME official website

Risk control rules & transaction rates

Both Bakkt and CME belong to the US open financial market exchanges. Clearing and risk control are completed through third-party clearing houses. Brokers usually require a portion of additional margin in addition to the margin required by the exchange and clearing house. Each broker has Different risk control rules and margin requirements vary.

Similarly, in the traditional financial market, the exchange does not levy commissions, usually only a part of the clearing fees and collection of some government taxes and fees. The main income comes from the charge for market data. If you need to obtain real-time CME and Bakkt option prices Data, you need to pay a real-time quote.

Options trading strategy

Option pricing

The premise of options trading is to understand why an option is traded at a certain price in the market. Generally, the main liquidity of the options market comes from market makers, not direct counterparties. The market maker will simultaneously make bid and offer quotes near a certain theoretical price. The core of option pricing is to find all market factors that affect the price and then perform modeling calculations.

At present, the most influential option pricing model in the industry is the Black-Scholes model (referred to as the BS model) proposed by Black and Scholes. They summarized several factors that affect the option price and constructed a stochastic differential equation to calculate the theoretical option price. The following is a simple example using the BS model of European option theoretical value calculation.

BS model for theoretical value calculation of European call options

BS Model for Theoretical Value Calculation of European Put Options

Refers to the probability distribution function in a standard normal distribution

Refers to the probability distribution function in a standard normal distribution

Is the remaining expiration time of the option from the exercise date

Is the remaining expiration time of the option from the exercise date

Is the spot price of the option object

Is the spot price of the option object

Is the strike price of the option

Is the strike price of the option

Is a risk-free lending rate for cash lending

Is a risk-free lending rate for cash lending

Is the annualized volatility of the underlying price of the option

Is the annualized volatility of the underlying price of the option

3) the remaining expiration time of the option;

By predicting the trend of the factors that affect the option price, different options trading strategies can be formed.

Buyer strategy

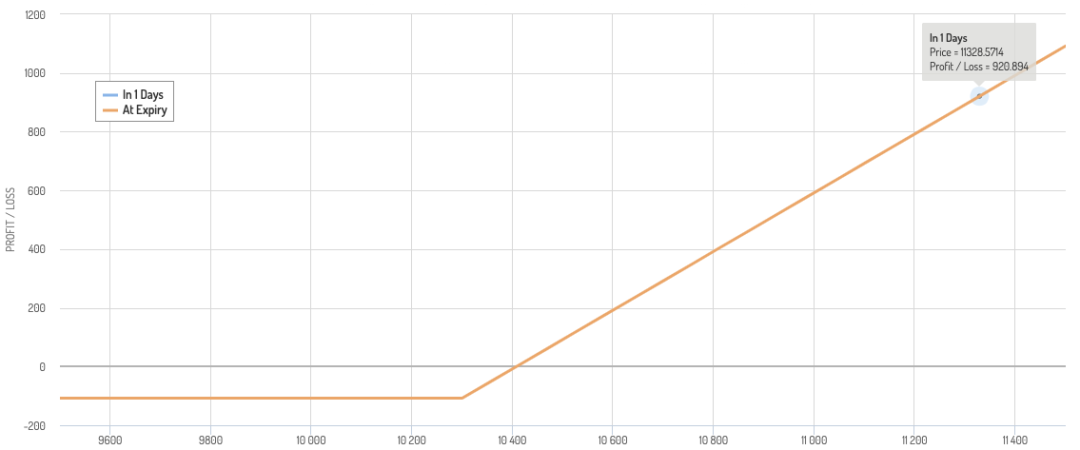

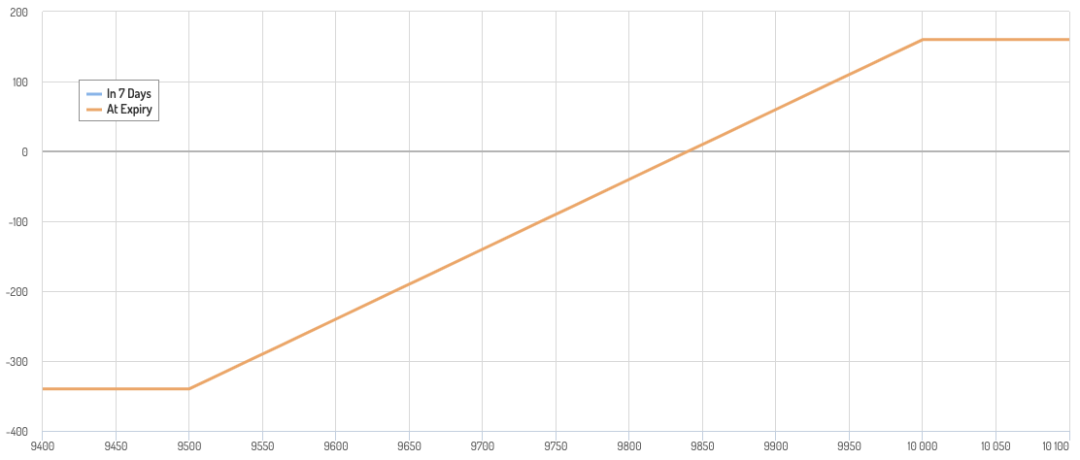

As a simple buyer of options, the main strategy is to prejudge the direction of the price fluctuations of the underlying object, so as to obtain the return of the difference between the current price and the exercise price. When the remaining expiration time of the option is short, the option The royalty is very low. The nominal value of the leverage may be as many as tens or even hundreds of times. When the market fluctuates violently, it is easy to generate multiples in a short period of time. The following figure is an example

Data source: OptionCreator

This is a Bitcoin European call option maturity return chart with a remaining expiration time of 1 day. The current price and the exercise price are both 10300. The volatility σ = 50%. The theoretical option premium is approximately 107 ≈ 0.0104 BTC. When the price expires one day later, the price of Bitcoin will increase by 10%, the value of the option will reach 921≈0.0818BTC, the standard currency return will be about 750%, and the BTC standard return will be about 690%. The high leverage of the option can greatly enlarge the short-term trading income. At the same time, the premium of short-term options is very low, and even if the extreme market exceeds expectations, only a limited amount of principal will be lost.

The disadvantage of option buyers is that when the expiry date is getting closer, the option will lose time value, so buying and holding the option for a long time is not a good strategy. It is like going to a casino to continue to gamble money. Lose light. Not everyone can gain dozens of times through the CDS (credit swap swap, an option-like insurance) like the protagonist in the big short.

Seller strategy

The seller of the option bears all the risks of the price change of the subject matter, and the gain is the limited premium paid by the option buyer. This behavior is similar to the insurance company in the real world, which collects limited premiums and pays high damages. Therefore, under normal circumstances, the option seller's strategy is mainly an option market maker and selling long-term put options.

Option market maker

Option market makers make market-making transactions by providing bilateral quotes for multiple option contracts. The main sources of income come from the spread of market-making, the liquidity rebate of the exchange , and the time value of options sold .

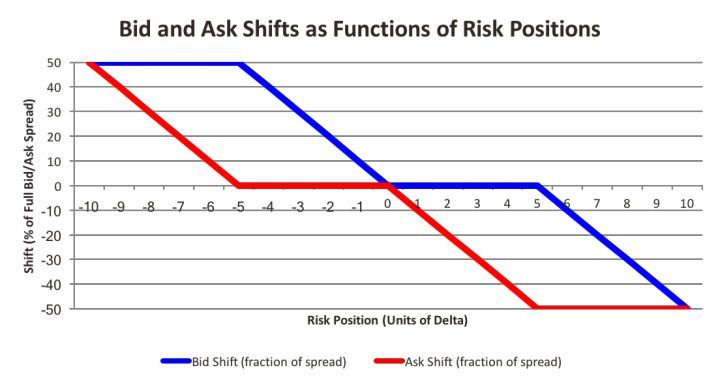

The current market maker strategies are mainly divided into inventory models and information models. The mainstream strategy is to predict the extremely short-term market trend through the analysis of the market microstructure, and then calculate the optimal bidding strategy based on the current market maker's position risk and the constraints of market making obligations.

Adjustment of inventory model to bid and offer prices

The inventory model was proposed by Demsetz in "Transaction Costs" in 1968. This is the earliest theoretical model for market makers. Demsetz believes that the bid-ask spread is actually the compensation provided by the organized market for the immediacy of the transaction. In actual market making abroad, the market maker will also determine the optimal form of quotation according to the inventory size of the market making variety.

The information model was proposed by Bagehot in 1971. He believes that the cost of information, that is, the cost of information asymmetry, is the cost that unknown traders pay to informed traders and is the main reason for the spread. At present, the mainstream strategies of major market makers are to predict the short-term trend of the market by studying the market microstructure, especially the order book and volatility.

Traditional information theory believes that informed traders often trade through market orders, so the order book formed by limit orders does not have additional information. With the disclosure of transaction information and electronic transactions promoted by major transactions, more and more investors use limit orders. At the same time, large passive investment managers, including ETFs, also use order books to estimate impact costs. Therefore, the market generally believes that the microstructure of the order book can predict short-term price movements.

Most of the long-term stable and profitable market maker systems are multi-strategy, or dynamically adjust the parameters of the strategy according to the characteristics of the market.

Sell put option

Compared to selling call options Call, the risk of selling Put options Put is relatively small, because the price of the underlying can only fall to 0 at most, so selling Put is actually a trading activity with limited income and limited loss. But in reality due to the existence of inflation, the value of the physical object tends to increase over time, that is, the farther away in the future, the lower the possibility of the same thing being lower than the current price, so sell Put options with strike price and current price that are close to each other will not be exercised in the future, which has also become a probability-dominated transaction.

The most well-known example of selling Put is the stock god Buffett. He once sold a large number of Puts in the S & P500 index ETF that expired a few years after the 2008 global financial crisis. With the US stock market 10 years after the bull market, he used to trade Put options bought by his opponent turned into scrap paper, and he earned hundreds of millions of dollars in premiums.

Similarly in the digital currency market, due to Bitcoin's halving deflation every four years and long-term high price fluctuations, selling Bitcoin's long-term Put will be a huge win.

Combination strategy

In the actual option trading market, most of the transactions exist in the form of option portfolios. According to the current bull market in the digital currency market, there are many options that can obtain stable Alpha.

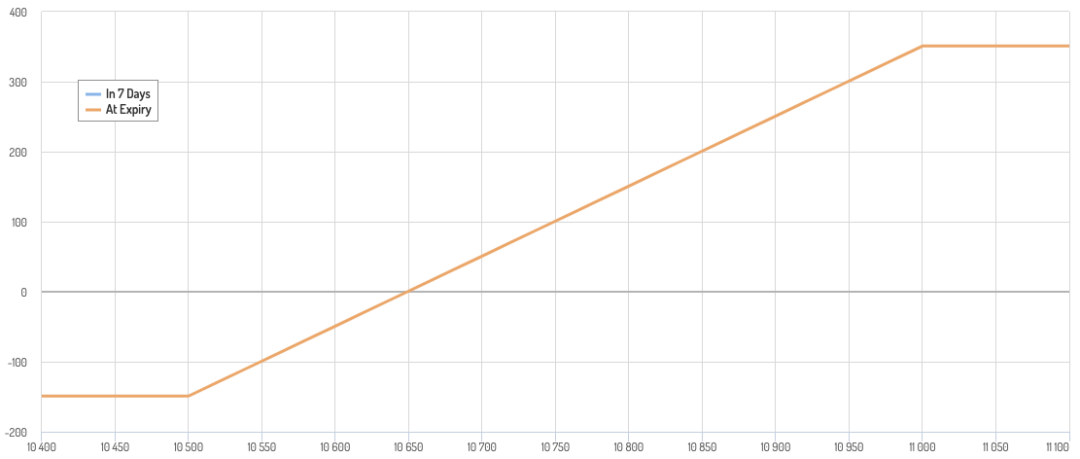

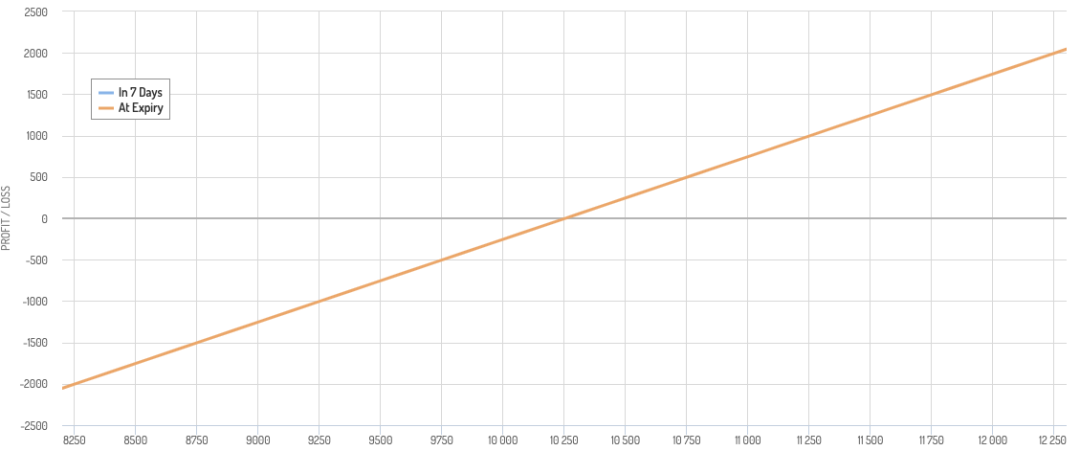

Bull Spread

The bull spread spread is an option combination constructed by buying a call option Call with a strike price closer to the current price, and then selling a call option Call with a farther strike price.

Assume that the price of the underlying Bitcoin is 10250, the volatility is 70%, the interest rate is 2%, and the remaining time is 7 days. The call with the exercise price of 10500 and the call with the exercise price of 11,000 are sold.

Buy 10500Call @ 290, Sell 11000Call @ 141

If the Bitcoin price is ≤10500 after 7 days, you will lose the option fee of 290-141 = 149; if the Bitcoin price is ≥11000 after 7 days, you will get a profit of 11000-10500-141 = 359; Get gain / loss for Bitcoin price -10500-141.

Compared to simply buying call options, the bull spread combination reduces the cost by about 50%, and also limits the income to a certain range, which is suitable for short-term trend trading in a bull market.

Bear Spread

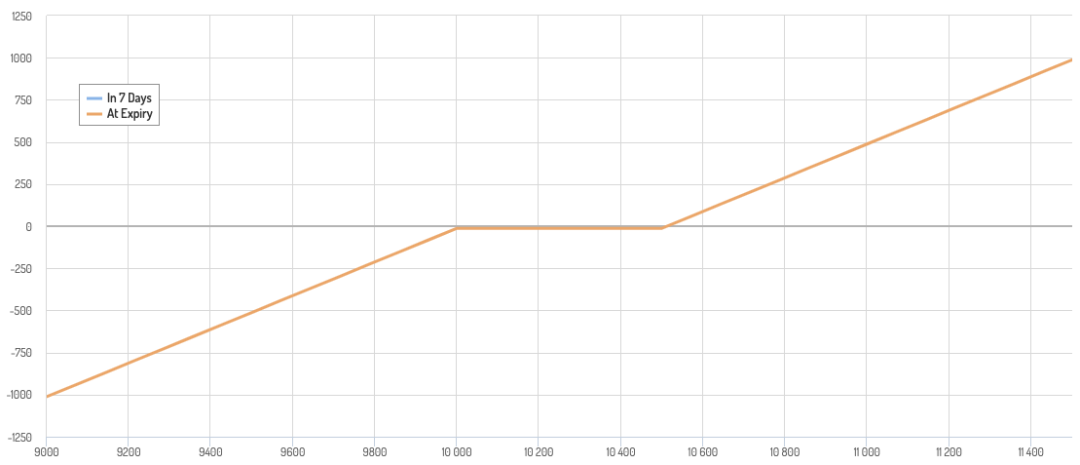

Corresponding to the bull market spread is the bear market spread. Selling the bear market spread arbitrage combination is by selling a put option with a strike price closer to the current price, and then buying a put option with a farther strike price. To build an option portfolio.

Assume that the price of the underlying Bitcoin is 10250, the volatility is 70%, the interest rate is 2%, the remaining time is 7 days, the selling option price is 10000Put, and the selling option price is 9500Put. The combined yield to maturity curve is as follows:

Buy 9500Call @ 117, Sell 10000Call @ 277

If the Bitcoin price is ≥10000 after 7 days, the gain will be 277-117 = 160; if the Bitcoin price is ≤9500 after 7 days, the loss will be 10000-9500 + 160 = 340; if after 7 days, 9500 <Bitcoin price <10000, you will get a gain / The loss is 10,000-Bitcoin price +141.

Because the bull market price trend is upward, the possibility of selling the bear market spread is lower, and the bear market's decline is more plunging. Compared to simply selling Put, the possible loss of the bear market spread is relatively limited.

Synthetic futures

The buyer of the option is the right party and the seller is the obligor. If the two options with the opposite rights and obligations are combined at the same time, it can be formed into a futures contract with the same expiration time.

Assume that the price of the underlying Bitcoin is 10250, the volatility is 70%, the interest rate is 2%, the remaining time is 7 days, the selling option price is 10250Put, and the buying option price is 10250Call.

Buy 10250Call @ 398, Sell 10250Put @ 394

By buying and selling a combination of Call and Put with the same strike price, respectively, it is possible to construct a maturity return curve chart that is the same as the longs of the futures. A slight modification of the option portfolio can more effectively reduce the risk of the combination. Under the same conditions, the selling option price is 10250Put and the buying option price is 10250Call.

After the adjusted income curve is between 10000-10500, the return will be kept as the difference between the option fee 290-277 = 13. Only when the Bitcoin price is less than 10000, exercise loss will occur . Synthetic contracts with spreads are suitable for fear of going up short Of traders make up for the dead sheep, and when the market has sufficient upward momentum, it can still generate enough good returns.

to sum up

Compared with option products in traditional financial markets, digital currency options are currently limited to the Bitcoin category, but the market foundation and participating institutions have been basically constructed. The standard option products provided by native digital currency exchanges are still the main trading targets in the current market, which is consistent with the status quo of the futures market. Compared with the efforts of traditional financial institutions under the compliance framework, the innovation of native digital currency exchanges is more efficient and Bold, built enough lead. As the jewel of the traditional financial market, the trading volume of options products in the digital currency market is not yet praised, and there is still a lot of room for expectation in the future. It will bring more financial innovation through various types of retail structured products.

References:

[1] Black–Scholes model

[2] Brief Introduction to Options Market Maker Strategy

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- SEC rejects Wilshire Phoenixd's Bitcoin ETF application

- Economics of halving: what will happen to the price of Bitcoin?

- Three drafters talk about the first financial blockchain specification: the central bank recognizes the blockchain, and the industry no longer grows savagely

- Libra welcomes new members, has this company been almost acquired by Coinbase for $ 150 million?

- Bitcoin once fell below $ 8,600, and BitMEX's bitcoin settlement exceeded $ 150 million

- Blockchain applications enter the fast lane: 4 "Blockchain +" scenarios have begun to fight the epidemic

- Viewpoint | Professor of Beijing Jiaotong University: Blockchain talent reserve is extremely insufficient