"Gray" carnival digital currency management: profiteering, trading, lack of supervision…

P2P online lending and digital currency seem to be two parallel orbits, but there is an intersection. This intersection is digital currency management.

Since the second half of 2018 , people who have been rushing in the P2P online lending and digital currency markets have found that their days are not good.

P2P is frequently thundering, supervision is rampant, and the industry is mourning; digital currency has been in the cold for a long time, and mainstream currencies have not been spared, and the market is so cold.

- Daily Twitter Pickup: Coinbase releases Visa debit card; Youtube currency circle red talks about mining "ban"

- Babbitt Exclusive | US Congress Hearing Record: Does Goldman Sachs really want to do cryptocurrency transactions? Why is JP Morgan Chase?

- Getting started with blockchain | Read the hash function in a text

However, the digital currency management at the intersection is accumulating strength and growing against the trend.

1, true trend or fake demand

Zhu Qing, a true 90-year- old, was the youngest technical director of the ice technology technology company.

In 2018 , she jumped out of the comfort zone and chose to use the digital currency lending platform as a starting point for entrepreneurship. She founded the Vena ( Loss Agreement) project, enabling users to conduct P2P (peer-to-peer) digital asset collateral on Vena 's DApp , providing digital assets. Financial management, lending and other services.

In her view, the financial assets of digital assets based on blockchain are very strong, and the financial services corresponding to the legal currency can be mapped. This is especially true for lending and wealth management.

Like Zhu Qing, from the online lending industry to the blockchain, there are not many people who are transforming into digital currency lending and wealth management.

But what drives them to take this step? Is digital currency management a “true trend” or a “false demand”?

The industry generally believes that the digital currency market is large, and the derivative financial market will be bigger or even larger. According to CoinMarketCap data, as of April 9 , the total market value of the digital currency market is about 1.2 trillion yuan. From this perspective, the digital currency wealth management market is also a huge blue ocean market of trillions.

But how many people are currently in the digital currency market? It is difficult to count. In 2018 , insiders claimed that there were more than 30 million users in the entire digital currency market, and it is clearly not so much today. At the closing session of the “Block Chain Winter Apocalypse” held by Zero Finance and Binary some time ago, a media person said that the current number of users in the Australian digital currency market is about 400,000. In China, it may be magnified ten times, around three or four million users. Such a group is still too small compared to the 145 million registered users of A shares in 2018 .

Although the digital currency market is currently a small-scale stock market, it is not difficult to see some incremental trends: many mainstream entities are already actively deploying blockchain and digital currency, like today's most influential JP Morgan Chase, Facebook. Starbucks and so on.

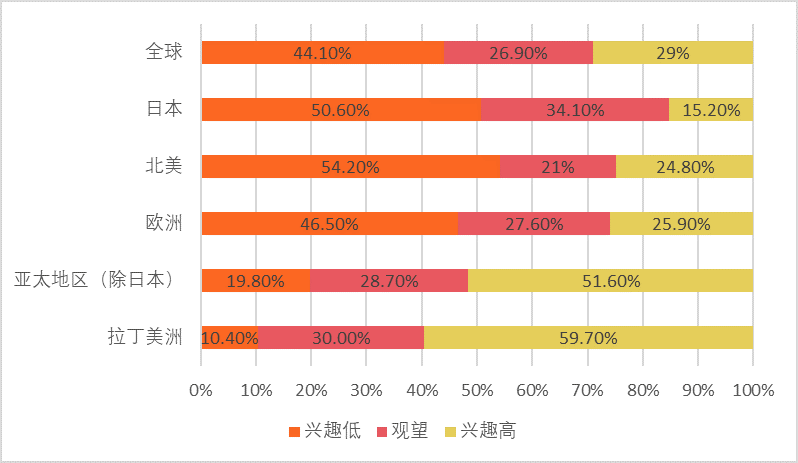

In addition, the 2018 Global Wealth Report released by Capgemini shows that although digital currency is not currently a major part of the high net worth population portfolio, as an investment tool and value store, people from all walks of life are increasingly interested. Globally, approximately 29% of high net worth individuals are more interested in digital currencies, and in Latin America and Asia Pacific, this proportion is more than half.

Figure: Global high net worth people's attitude towards digital currency

Source: Capgemini's 2018 Global Wealth Report

All of the above are only predictions on the scale, but the key is whether users really have digital money management needs? He has many years of experience in traditional financial markets. Li Zhe, who is now a partner of FutureMoney , believes that the digital currency market should definitely exist in the wealth management market. As long as the user accepts and agrees with the "currency-based" thinking of digital currency, there will be a need for financial management .

The bear market since 2018 has caused the market to be deserted for a while, but it has forced a large number of speculators to go out. Many users who are still in the circle today have bitcoin or blockchain beliefs, especially bitcoin mine owners. They hold a lot of digital currency in their hands, and most of them don't want to operate in short-term and choose to keep their coins.

For these people, financial needs will exist more or less: not losing digital currency, but also earning additional income to meet cash needs, why not?

2. Three ways to play digital currency management

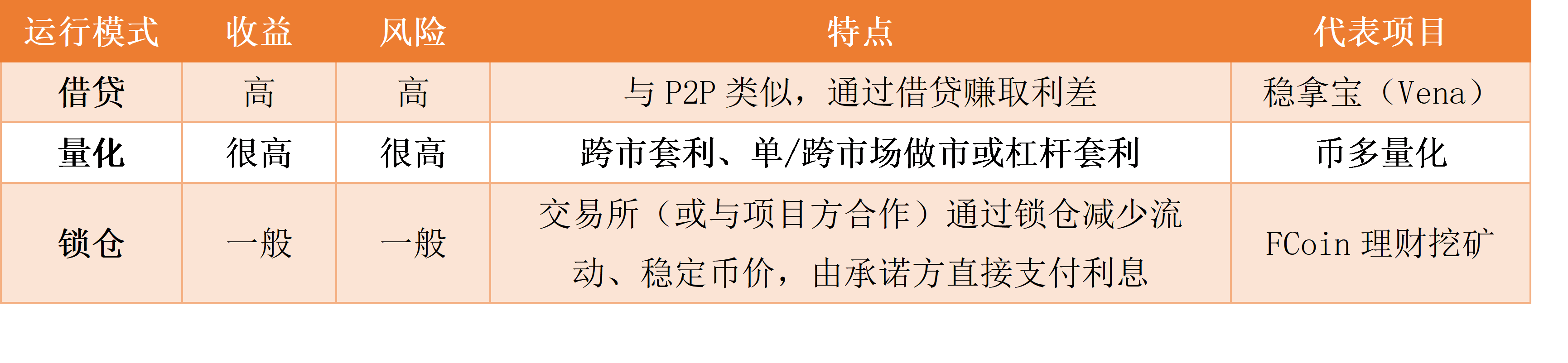

At present, the more popular modes of operation of the digital currency management market can be roughly divided into the following three categories:

( 1 ) Borrowing

The lending model of the digital currency financing market is similar to the P2P online lending. The difference is that the borrowing target is changed from the legal currency to the digital currency. The current common borrowings are: currency borrowing and legal currency borrowing.

Among them, French currency borrowing refers to borrowing between digital currency and legal currency; and currency borrowing can be divided into borrowing between digital currency, borrowing between digital currency and stable currency.

"We are not doing credit business for digital assets. The industry does not have enough data to allow users to make unsecured credit loans. It is generally a pledge loan business," Zhu Qing said in an interview.

In general, depending on the collateral, there will be a large fee gap:

If the pledge is legal currency, the value is relatively stable, the risk is small, and the handling fee is relatively low, about 17% , that is, the digital currency that the user can borrow is about 83% of the value of the pledge currency;

If the pledge is a digital currency, the value fluctuates greatly and the risk is relatively increased. Generally, the digital currency with 2-3 times the value of the required funds is required, and the indicators such as the warning line and the clear warehouse line are also set for risk control.

Since digital currency lending is currently the same as early online lending, there is a lack of supervision, and many interest on lending and financing has already crossed the 36% legal red line. However, due to the advantages of fast transactions and streamlined processes, digital currency lending is still booming in the last two years .

Digital currency lending has emerged in the bull market. At that time, investors were blindly optimistic. They wanted to continue to increase their weight and suffered from limited "ammunition", which led to the creation of digital currency lending services.

In the bear market, investors are not willing to cash in digital currency, but also need cash flow or new investment layout, which further promotes the boom of digital currency lending. It is understood that between March 2018 and January 2019 , the digital currency lending platform Genesis Global Trading will issue a total of $ 700 million in digital asset loans.

( 2 ) Quantification

Quantitative trading refers to the use of advanced mathematical models to replace human subjective judgments, using computer technology to screen a large number of "high probability" events that can bring excess returns from large historical data to formulate strategies to reduce investor sentiment fluctuations. The impact of avoiding irrational decisions made in the face of extreme fanaticism or extreme pessimism.

Generally, it can be divided into two types: risk-free arbitrage and trend arbitrage.

In the digital currency market, the simplest and most direct quantification is to use the spread between different exchanges to carry out brick arbitrage; or cooperate with exchanges and project parties to make market arbitrage in a single market / cross-market. These can all be classified as risk-free arbitrage.

However, due to the increasing quantitative competition, the operational space of risk-free arbitrage is getting smaller and smaller, and usually requires high-frequency operation to obtain relatively considerable benefits.

The trend of better-yielding arbitrage is currently very difficult for the digital currency market.

“Sometimes you will find that the more models you use, the more accurate the conclusions are,” said a digital currency quantitative investment practitioner. This is mainly because the digital money market is still in the early stages of development, has not experienced multiple economic cycles, and historical data is not enough. It is difficult to establish a fully effective quantitative model. In addition, the dealers in this market have too many trading factors, and the established quantitative model is perfect, which is not the direct result of the dealer's trading. This is why many quantitative teams work with exchanges and project parties.

Even though the quantitative investment in the digital money market is still immature, it can often bring high returns to users.

“Our quantitative team can achieve 50%-200% annualization. Only users need to open an account at BitMex , and then hand over the account to us for operation, the profit is five or five points.” A certain quantitative team in China is responsible for Zero Finance. Binary said, "In doing so, the coin is still in the hands of the user, and the user is more at ease. We are only helping the user to trade."

At the same time, the person in charge also said that in the process of quantitative trading, the commitment to guarantee the principal, a loss of 30% will be returned to the user.

For such high returns, analyst Diane said, "If someone says that I can give me 12% of the points, I might think he is a liar. Now the quantitative team in the digital money market is generally lacking in experience and has not gone through the market. Recognition is very risky."

Although every quantitative team is currently trying to promote its own profitability, in fact, more quantitative teams are quietly dying. In the digital currency market, the era when simple strategies can make a lot of profits has passed, and now the competition is becoming more intense and the difficulty is getting bigger.

Quantifying transactions is destined to be a small group of people earning a lot of money, and more leeks are cut without temper . Even as the protagonist in this game – the quantitative team in the digital currency market, in addition to having enough experience and rich arbitrage strategy, there must be strong capital strength to participate in the rule making, otherwise it may become a banker's leek. .

( 3 ) Locking the warehouse

Locking is a common and unique way of playing in the digital currency management market. It is usually initiated by the project party or the exchange.

The project party or the exchange initiated the lock-in program, mainly to reduce the market liquidity of the digital currency, stabilize the price, and avoid the price plunging .

For example, FCoin's recently launched financial mining is a lock-and-lock model. As long as you hold and lock 10,000 FT, you can enjoy financial mining, and the FCoin exchange will return 2 million FTs per user according to the proportion of each lock.

Photo: FCoin wealth management mining rules

Source : FCoin official website

Locking is somewhat similar to regular financial management. The platform requires that the digital currency be locked. In addition to simply stabilizing the price, it is also possible to absorb user funds and mine the POS-based currency to obtain revenue.

In addition to these centralized financial management methods, decentralized financial services with more blockchain characteristics are gradually being derived. For example, the decentralized lending platform Compund or Dharma is currently online.

3. Four types of subjects in digital currency management

The service providers in the digital money management market can be basically divided into four categories: exchanges, wallets, quantitative teams and specialized financial platforms.

Exchanges and wallets have certain advantages in carrying out wealth management business by virtue of their traffic advantages. "The exchange and the wallet itself are traffic portals. In the future, the goal is to make products such as Alipay. The quantitative team and the wealth management platform are dedicated to financial management, and generally cooperate with exchanges and wallets as their product providers." Zhe said.

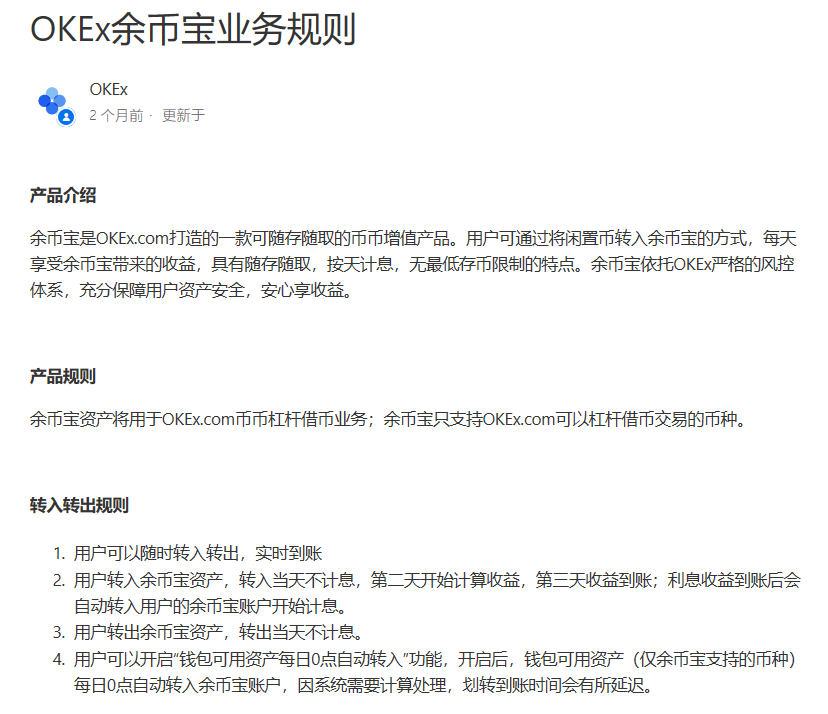

The exchanges use more of the lock-in rebate and lending models. For example, OKP Exchange's OK PiggyBank product is used to earn the proceeds by using the assets deposited by the user for the currency leveraged lending business of the exchange.

Figure: Description of the business rules of the remaining coins

Figure: Revenue from surplus coins

Source: OKEx official website

In addition to FCoin , many exchanges, including OTCBTC , have introduced similar lock-and-lock financing.

Figure: Introduction to the OTCBTC Locking Program

Source: OTCBTC official website

In terms of wallet financing, Cobo is known for earning revenue through user investment mining, with the highest annualized income of 85%.

Photo: Cobo Financial Services

Source: Cobo official website

Quantitative teams and financial platforms do not have the traffic advantages of exchanges, but with their professionalism, they have become an indispensable part of the digital currency management market. Behind many exchanges and wallets, there are more or less quantitative teams and financial platforms.

Take Wen Na Bao as an example. Steady is a wealth management product launched by the digital currency lending platform Vena . It supports the exchange between USDT and the wave field and lending and financing. The risk is relatively low, and the annualized rate of return generally exceeds 10% .

Figure: Wen Nao Bao wealth management products (partial)

Source: Steady App

4 , online loans to the left, digital currency to the right

Digital currency management and P2P online lending are somewhat similar.

In 2005 , Zopa , the world's first P2P online lending platform, was established.

In 2007 , P2P crossed the sea and entered China, but it was not until 2010 that the first real online loan platform appeared.

Subsequently, online loans entered the fast lane of development. In 2013 , it was regarded as the first year of online loans, and the industry began to grow wildly.

At that time, the online loan market presented a “prosperous” scene due to risk mismatch and lag in supervision. The annualized rate of return of products often exceeds the 36% legal red line, even if it exceeds 100% , it is not unusual.

The golden age of online lending is still in sight, and now the digital currency financing market is ready to go. Many digital currency wealth management products have advertised themselves as the balance of the digital currency market and P2P . Such products as “Yu Bao Bao” and “Sheng Na Bao” are numerous, and digital currency lending has sprung up under the stimulation of high returns.

Some industry analysts believe that the digital currency management market in 2019 is like P2P online loans in 2013 .

Chen Yunfeng, a senior partner of Zhong Lun Wende Law Firm, also said that the current digital currency management market can indeed be benchmarked against the 2013 first year of online lending: supervision has not yet been introduced, the market is relatively irregular, and publicity Higher yields and higher potential risks in the industry.

However, the P2P online lending industry has already passed the stage of barbaric growth. After experiencing frequent violent thunder last year, it has now ushered in the rectification of supervision. In 2018 , it was also called the first year of P2P filing.

According to Zero Financial Statistics, as of the end of the first quarter of 2019 , there were 1,027 normal operating platforms for the P2P online lending industry nationwide, down 52.5% year-on-year. There were 53 problematic platforms in the first quarter, a significant decrease of 77.1% from the fourth quarter of 2018 , which is only one-tenth of the number of problematic platforms in the third quarter of 2018 . Since October 2018 , no new platforms have been launched.

Under the continuous high pressure of supervision, the P2P online lending industry is experiencing a period of painstaking struggle, which is inconsistent with the barbaric development of the digital currency wealth management market.

5 , a "grey" carnival

Digital money management, the road ahead is long.

Getting customers is the first problem. There is a certain threshold for entry in the digital currency market. At the same time, due to the current stage of stock market, it is difficult for large-scale new users to enter in a short period of time. All platforms are competing for limited market share, resulting in the largest number of customers in the digital money management market. problem.

Second, it is wind control . Most of the current digital currency management risk control is based on the traditional capital market, and can not be well adapted to the digital currency market.

It also involves a "currency standard" issue. Different from the traditional financial services of the market, the target of digital currency management is inherently unstable, so the income comes not only from financial transactions, but also from the price fluctuations of the digital currency itself. If the rise and fall of the digital currency market is higher than the digital currency wealth management market, for investors who have not formed the "currency-based" thinking, wealth will not shrink but will shrink, although the number of digital currencies will become more . This also limits the development of the digital currency wealth management market to a certain extent.

The last and most important issue is the regulatory issue.

At present, many digital currency lending platforms will adopt an “export-to-domestic” model in order to evade possible supervision, that is, the server is set up overseas, but the service is aimed at domestic investors.

In this regard, lawyer Zhang Xiaofeng, a partner of Beijing Wanshang Tianqin Law Firm, said in an interview that “institutions involved in lending and wealth management need to have corresponding qualifications and conditions in accordance with domestic laws. For example, enterprises need to have certain registered capital, enterprises. The shares held by legal persons or other social organizations shall not exceed 10% of the total registered capital of the microfinance company, and shall be registered with the financial supervision department or obtained the corresponding license in accordance with the regulations. At present, the digital currency management platform itself has no legality. Words are completely outside the scope of domestic regulation."

In the legal context of our country, only things that are prescribed by law as "things" can be pledged. For digital money lending and financial management, Xiao Wei, director of the Bank of China Law Research Association, believes that “ whether the digital currency pledge loan is legal depends on the 'currency ' and cannot be generalized. If the borrower holds bitcoin, ie 'specific virtual goods', Mortgage for financing purposes, the law can be tolerated; but our law does not recognize other native tokens as legitimate virtual assets. "

Another problem with the lack of supervision is that the nature of the financial platform is unclear . For the digital currency lending platform, their role should be the intermediary. But nowadays, due to the lack of regulatory mechanisms, some platforms may hold a large number of digital assets sold by users. This creates a pool of funds in disguise, and it is entirely possible for the platform to use it to quantify investments or invest in other high-risk wealth management products. This problem also exists in the lock mode.

Such risks may cause P2P thunder to repeat itself in the digital currency world. The so-called violent thunder of P2P is because the platform that should only be engaged in the information intermediary business is disguised and stored, and the funds escrowed by the user are misappropriated, causing damage to the users and eventually causing chain violent thunder.

At the same time, however, digital currency management can indeed evade supervision to a certain extent . The reason is that the classification and definition of digital currency by law is not yet clear. At present, the interest income of many digital currency lending platforms is settled through digital currency. Although the annual interest rate can be calculated to exceed the 36% legal red line of the regulatory regulations, digital currency is not regarded as currency or asset in China. . According to Article 9 of the Supreme People's Court's Provisions on Several Issues Concerning the Application of Laws in the Trial of Private Lending Cases, borrowing through digital currency is not within the prescribed range, and the interest thus calculated cannot be counted as interest. In this way, some digital currency lending platforms have bypassed regulatory requirements.

If the digital money management market really needs to develop, it cannot be left out of the regulatory system . "Compared with the online loan market, the development path of the digital currency wealth management market still needs to be observed, but it must be affirmed that blind and disorderly development is not conducive to the digital currency and digital asset industry. The digital currency wealth management market urgently needs regulatory intervention to establish and improve. The digital currency management access system and business practices protect investors' interests and maintain financial stability and national security." Chen Yunfeng said this to Zero Finance. Binary said.

Today's digital currency management market seems to be on the old road where P2P online loans have gone.

There is no contraindication before the regulation has come. Digital currency management will continue this "grey" carnival.

(Author: Mr.J pipeline: Sun Shuang Source: Zero One Finance · Binary)

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Stabilizing currency management: The next block in the blockchain?

- Explain the 12 blockchain demonstration projects selected by the Korean government

- US SEC Chairman: Using existing laws to deal with cryptocurrency entity non-compliance

- Money and payments in the digital age: IMF presidential bureau, Circle "heads-up" JPMorgan Chase and regulators

- Can the bitcoin belief that has collapsed be rebuilt now?

- QKL123 Research Report | Ruibo, the leading currency for cross-border payment, can the market stand in the top three?

- April 11 market analysis: BTC innovation is high, EOS is about to touch the annual line