Nine highlights of the DeFi world in 2020: the rise of the DeFi dark horse, but potential risks deserve attention

Written by LeftOfCenter

Source: Chain News

Editor's note: The original title was "Nine Highlights of the DeFi World 2020"

No matter what harm you have just done in the cryptocurrency world in 2019, we sincerely hope that the coming 2020 will rekindle your hopes. Yes, for the blockchain industry, 2019 is a year of ups and downs, and the fall is much more than the year of rise. In this year, the currency price was not beautiful, but it is undeniable that we felt that "Open Finance DeFi Undercurrents surging in the realm.

- One article reads DeFi's fifth Uniswap: the unique existence of the crypto world

- Vitalik Buterin's latest brain hole: a scalable data blockchain model without committees

- Behind Bitcoin's soaring: how to help India achieve $ 5 trillion economic scale?

We believe that DeFi has emerged and will unlock great potential. In order to allow readers to better understand the development trend of the DeFi field, Lianwente presents nine highlights that occur in the field of "open finance". I hope to provide a window for everyone to gain a glimpse of the current situation in the DeFi world. .

As an aspect, our observations and conclusions are certainly not perfect. Welcome everyone to comment.

Look at one

Can the DeFi asset explosion continue?

The assets deposited in the DeFi system in 2019 continue to grow, which has become an important indicator that excites the crypto world, especially the Ethereum ecosystem.

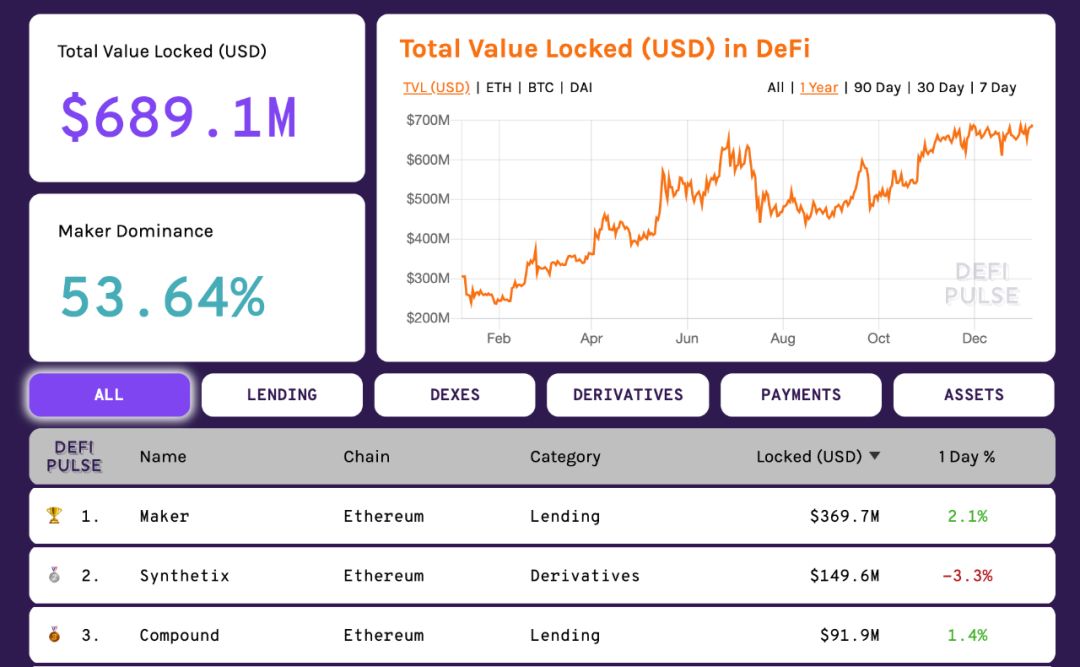

defipulse.com statistics, as of January 6, 2020

According to data from DeFiPulse (defipulse.com), the size of locked-up funds in the DeFi system has increased from around $ 290 million to $ 690 million since the beginning of 2019. Among them, Maker locked up about 370 million US dollars, accounting for 53.64%, ranking first. The newly emerging Synthetix, locked up about 150 million US dollars, ranked second. Lending platform Compound, locked up $ 92 million, ranked third.

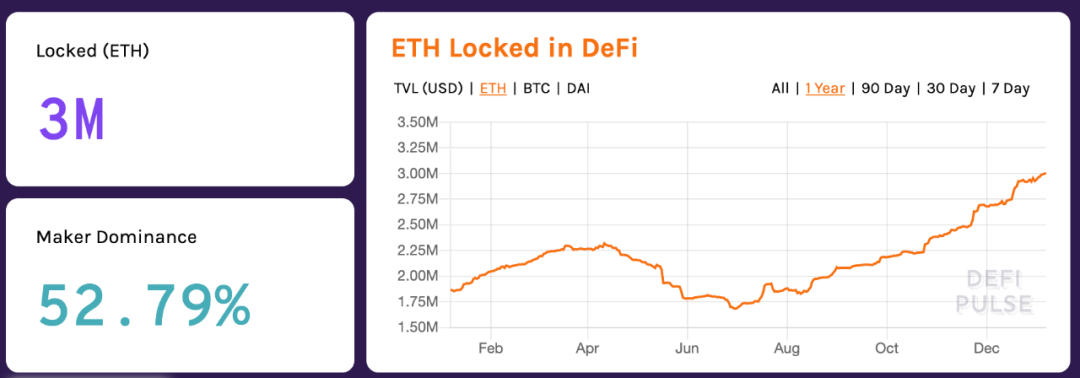

defipulse.com statistics, as of January 6, 2020

Of course, the most active cryptocurrency asset in the entire DeFi ecosystem is Ethereum. By the beginning of 2020, there were more than 3 million ETH locked in the DeFi ecosystem, a record high. The amount of ETH locked in the DeFi ecosystem is already close to 3% of the total amount of circulating ETH.

The number and value of assets locked in the DeFi system are currently the simplest and direct indicators for measuring this type of application. This indicator has shortcomings, but the direction is very clear. Judging from the development trend of the past year, this indicator is all good. However, whether this trend can continue in 2020 and achieve explosive growth deserves close attention.

Aspect two

DeFi dark horse rises, but potential risks deserve attention

MakerDAO is currently the "king" in the DeFi world. As mentioned above, the value of the assets locked by the Maker agreement is about US $ 370 million, accounting for half of the entire DeFi ecosystem. Maker officially launched the multi-asset mortgage Dai function MCD at the end of 2019, adding more collateral categories. Although its launch time was much longer than originally expected in the first quarter of 2019, it still cannot erase this. This is the DeFi world in 2019. The most anticipated important product upgrades of the year.

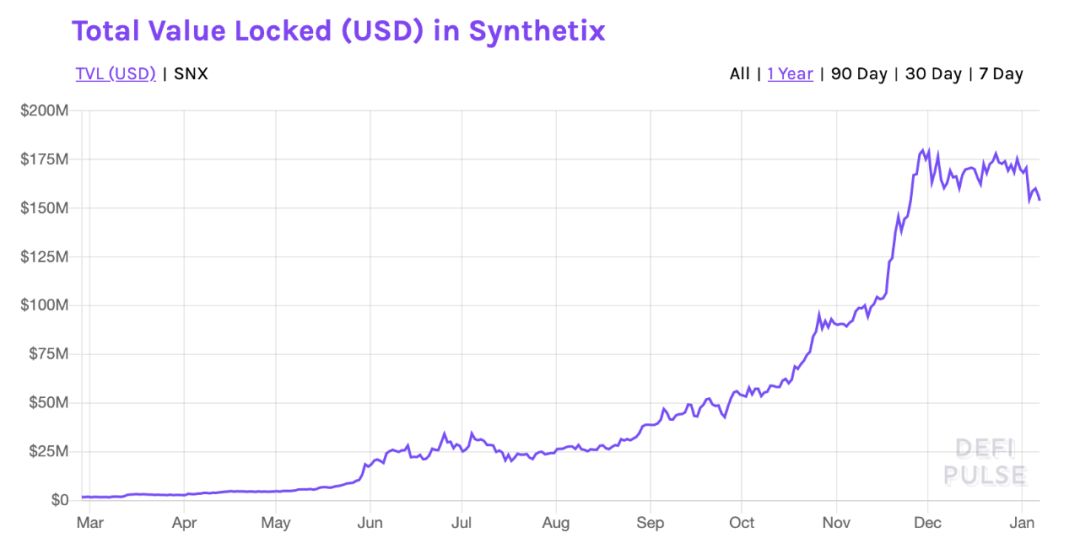

In addition to the dazzling MakerDAO, Synthetix, another synthetic asset issuance platform, is undoubtedly one of the fastest-growing projects in the 2019 DeFi project. The price of its issued token SNX has increased by more than 30 times in 2019, and its market value has hit the overall ranking. About 30 people. The value of locked assets on the Synthetix platform even rushed to the second position of DeFi, second only to MakerDao.

Synthetix is a decentralized synthetic asset distribution agreement built on Ethereum. Users can mortgage Synthetix's ERC20 token SNX to generate synthetic assets through mintr (a DApp on Synthetix). This synthetic asset can be a stablecoin, or Long / short assets and commodities corresponding to a certain kind of token, and can carry out arbitrage through Exchange.synthetix.

In this mechanism, the SNX mortgagor is the counterparty to all synthetic asset exchanges, and the mortgagor needs to bear the entire debt risk in the system.

Synthetix's rapid growth is remarkable, and its potential risks cannot be ignored. These potential risks include the risk of the oracle machine, the poor liquidity of the token, and the risk of unlocking the market due to the current excessive increase.

Cao Yin, an early user in the DeFi field and managing director of the Digital Renaissance Foundation, wrote that "In essence, the SNX project is a copy of the A-share routine. The focus is on attracting market capital to follow suit through performance-driven pull, and then freezing liquidity through lock-up or burning mechanisms, thereby forming the effect of continued net inflow of funds to set prices. " He believes that this is a very dangerous game. When the price is too high, as long as someone starts to sell it, it will immediately cause a catastrophic bankruptcy, which will cause a death spiral. Increase.

The value of Synthetix's hedging assets has increased rapidly in the past year and has entered a stagnation period

At present, the project of Synthetix has transitioned from a period of rapid growth to a period of stagnation, and the value of SNX's hedging assets has also declined.

Aspect Three

Maker mode out of Ethereum

At present, Ethereum is still the home of DeFi. However, other public chain projects have also begun to cultivate their own DeFi ecosystem. The particularly prominent trend is that the Maker model has begun to get out of Ethereum.

The success of MakerDAO and its mortgage debt warehouse model has verified the feasibility of this new model of digital currency mortgage lending in practice. The potential of this model in open finance has caused other project parties to follow suit.

For example, Kava, the first DeFi project on the cross-chain project Cosmos, has just recently released the mainnet. Similar to Maker, Kava is also an automated mortgage lending platform. It also issues two tokens: the stablecoin USDX (similar to Dai) and the equity governance token KAVA (similar to MKR). Users can mortgage BTC, XRP, ATOM, and BNB tokens in multi-mortgage debt positions CDP to generate stable currency USDX, USDX and USD 1: 1 anchor; in addition to USDX, another equity and management type is issued in the system Token KAVA. Kava, which has just started, has done well and has been online for less than a week on the main network. The size of validator nodes' pledged assets has reached $ 80 million.

Another similar project is the mortgage stablecoin Checker secretly developed by Arthur Breitman, co-founder and CTO of the public chain project Tezos. At present, the specific details of the project are unknown, but from the published information, the project is similar to the MakerDAO model, and the stable coin Checker is also generated by locking the XTZ token mortgage. The difference is that there is an additional Tezos baking reward for locking XTZ tokens. In other words, locking XTZ tokens will yield higher returns than simply baking.

In the Bitcoin ecosystem, the Maker pattern has also recently appeared. Money on Chain, a startup that is transforming into a non-profit trust, has launched a DeFi platform based on the Bitcoin sidechain Rootstock (RSK). In most Bitcoin DeFi use case scenarios, either Bitcoin is wrapped into an Ethereum-formatted token, or a centralized service is provided to mortgage Bitcoin to obtain a DAI loan, and Money on Chain uses a An open source protocol inspired by Bitcoin to build solutions.

Money on Chain claims to be an evolving ecosystem that can build lending products based on it. Like MakerDAO, there is not only one kind of token in the Money on Chain ecosystem, but there are 3 kinds of tokens, which are:

- Mortgage Bitcoin generated Dollar on Chain (DoC), which corresponds to the stable currency Dai in MakerDAO;

- BitPRO (BPRO), which is charged by users of the system and represents the cost of bitcoin, is called "passive income";

- The Money on Chain token (MoC), which can be used for community voting governance, corresponds to the MKR of the Maker Foundation.

Money on Chain will issue a variety of stablecoins linked to the fiat currencies of many Latin American countries in the future in order to reduce the risk of volatility and be more acceptable to businesses. However, the challenge for the project is compliance, so it is currently focused on the Latin American market.

Aspect 4

How to introduce real assets and off-chain assets into the DeFi system?

In the field of DeFi, there has been a lack of new quality assets.

In 2019, more asset classes, including physical assets or off-chain assets, will begin to enter the DeFi system. This includes not only the newly launched Maker multi-asset mortgage Dai (MCD) system, but also the Maker Foundation in conjunction with the German supply chain financial district. The blockchain platform Centrifuge has launched a series of pilot experiments in areas such as logistics, real estate, and streaming music supply chain industries (such as Spotify), which have "long repayment cycles and large funding gaps in each stage of operation". ( Please refer to the article "How to make DeFi out of the small circle game? Maybe look at its application in the real industry" for a more detailed case)

In addition, RealT, the real estate investment platform, launched the first real estate token fund pool on Uniswap and is also working to introduce real assets into the DeFi system. The property is currently sold out and holders of its tokens have started to charge rent based on their share.

Look at five

DeFi tokenized derivative gameplay is constantly renewed

Another interesting project in the DeFi system is Compound. Compound has added cToken (including cDai, cETH, etc.) tokens in the v2 version. It represents the principal plus interest after the user deposits funds (such as Dai). As an ERC20 token, cToken can be traded and transferred. . The increase in cToken opens a whole new world for practicality and liquidity, allowing all assets locked in Compound in the past to flow throughout the ecosystem.

DeFi's interoperability and composability make it possible for RC20 format cToken to be integrated by other protocols. For example, Uniswap provides the Dai and cDai transaction pools, which means that injecting cDai into the Uniswap liquidity pool allows users to earn Compound interest while earning fees in Uniswap-related transaction pools.

Based on this, another DeFi project, decentral, issued rDAI to further pledge the profits generated by cDAI to generate another token. It hopes to tokenize the ownership of the interest generated by paging cDAI, which is essentially a token principal and interest ownership. The practice of separation.

Aspect six

DeFi Insurance Services

Insurance services and products are emerging in the DeFi space and have become important branch areas.

Different from insurance business such as accident insurance and life insurance in our traditional perception, the DeFi insurance agreement is essentially a smart contract-based insurance, which mainly provides risk protection for several types of accidents that often occur in the currency circle. Including the theft of private keys, attacks on exchanges, stolen wallets, manipulation of loopholes in smart contracts, etc., designed to provide investors with hedging risk insurance services. Related products include Etherisc, CDx, Nexus Mutual, Opyn (oTokens) , VouchForMe, and KeeperDAO.

The Orange Book of Blockchain Media once gave a good introduction and summary of these core projects in the article " Guardian of DeFi: A New Circuit of Insurance ".

- Nexus Mutual: It adopts a risk-sharing model. It has a risk-sharing pool governed by NXM token holders, and the community decides which claims are valid. Nexus Mutual is essentially smart contract-driven insurance, which means that DeFi users can use this solution to buy insurance for funds borrowed from Compound or Dharma, and digital currency stored by Uniswap, to hedge risks.

- Etherisc: It is a universal decentralized insurance application platform. By providing developers with a common insurance infrastructure, product templates, and insurance license-as-a-service, anyone can create their own Insurance products ranging from flight delay insurance, hurricane insurance to crypto wallets and loan mortgage insurance.

- Opyn (oTokens): oTokens is currently only a proposal. The team behind it hopes to propose a more comprehensive protocol to replace dYdX. In essence, users can protect their assets by purchasing put options on the Convexity Protocol. The user mortgages Ethereum ETH to mint an ETH oToken. This oToken represents a put option on Ethereum. Others can buy this option to obtain insurance against a ETH plunge. Users who mint oToken are equivalent to collateralizing ETH to sell options to obtain additional income, and holding ETH can also make money.

- VouchForMe: aims to reduce the cost of insurance by collecting endorsers and guarantors of users in social networks and social relationships to provide endorsements that meet requirements. When guaranteeing, you need to sign a financial commitment letter linked to the insurance claim. The more people you guarantee, the lower the premium. If there is a claim, the guarantor will bear a certain proportion.

- CDx: is a credit default swap agreement. Credit default swap (CDS) is a financial product designed to protect users from the risk of default by another party. Buyers make continuous payments during the insurance period to make payments and receive compensation if they default.

- SWAP RATE: It is a DeFi-based interest rate swap (Interest Rate Swap, IRS), which means that when you are on various decentralized platforms, you will face uncertain interest rates. Now, as long as you use SWAP RATE With smart contracts, you can obtain a fixed interest rate for borrowing. When the expected interest rate does not reach, the platform will make up the difference for you through the contract. Of course, if the income has exceeded the agreed interest rate, the natural contract will also make you redundant. The proceeds are given to the platform.

In addition to the above projects, recently distributed system development company Talo and digital asset management platform Amber Group jointly launched a project called "KeeperDAO". KeeperDAO, which is positioned as a “ liquidity underwriter on the DeFi chain, '' is essentially a cross-agreement insurance fund that minimizes trust. It encourages token holders to participate in liquidity provision and liquidation through economic incentive strategies. KeeperDAO encourages token holders to participate in the liquidity fund pool through economic incentive strategies to coordinate clearing and rebalancing in application areas such as margin trading, loans, and exchanges, allowing users to concentrate funds in Ethereum smart contracts, Gaining common benefits through on-chain arbitrage and liquidation opportunities not only allows all participants to obtain passive income through game play, but also ensures the liquidity and orderliness of decentralized financial applications.

Aspect Seven

How to solve the liquidity problem?

Compared with the traditional market, the overall market value of the crypto market is inherently small, and at the same time it faces the problem of insufficient liquidity, especially in the field of DeFi, which is originally small. In 2019, the project parties use all their best to release liquidity.

In order to release liquidity, a common trend is that DeFi and the centralized world work together to win-win, embrace each other, and explore a new hybrid model that combines the strengths of DeFi and CeFi.

Among them, the new version of the decentralized exchange DDEX's margin business began to support the centralized stablecoin USDT in addition to DAI. USDT is currently the largest stablecoin by market capitalization and one of the most liquid cryptocurrency assets. The increased support for USDT in the DDEX margin business will undoubtedly increase the liquidity of the loan pool on the platform.

In addition, MakerDAO has recently launched a multi-asset mortgage Dai (MCD) system, which has newly introduced assets other than ETH, and currently supports the most liquid attention token BAT. Whether centralized mortgage assets (such as tokenized bonds) and stablecoins (such as USDC or USDT) should be introduced has been the focus of debate in the MakerDAO community, but MakerDAO CEO Rune Christensen's point of view is very clear. He believes that the introduction of centralized assets can Increase the liquidity of Dai and the decentralized financial ecosystem, expand the cryptocurrency to as many people as possible, and expand the overall market value of crypto DeFi.

Not only do decentralized exchanges embrace centralized assets, centralized exchanges have also begun to move closer to decentralized stablecoins. OKEx, a centralized exchange, lists multiple decentralized stablecoin Dai trading pairs, and integrates Dai's deposit interest rate (DSR). As the world's first DSR (Dai deposit interest rate) trading platform, users can enjoy DSR years at OKEx. Revenue). According to MakerDAO CEO Rune Christensen, this provides a simple entry point for DeFi access for new users.

In terms of providing liquidity, the opportunity for DEX also deserves attention. A major obstacle to the development of the DeFi platform is the lack of liquidity, so bridging the liquidity from outside the platform for the DeFi platform is essential.

A liquidity aggregator like DEX.AG satisfies such a requirement. DEX.AG provides traders users with the best prices from 11 different decentralized exchanges. A typical use case of DEX.AG is that after the integration of the Synthetix native exchange in the near future, users of both platforms will have additional Benefit from the liquidity of the company, and at the same time, SNX holders can also charge more transaction fees.

In addition, after upgrading the v3 version of the decentralized exchange protocol 0x, a new liquidity bridging contract was launched, allowing 0x to aggregate network liquidity from 0x and other decentralized exchanges, including Oasis of Kyber Network, Uniswap, and MakerDAO. , So as to cross the major DEX platforms and provide the best prices for both popular and long-tail trading pairs. In addition, 0x also redesigned a new token economic model and encouraged economic liquidity providers to be consistent with the interests of the entire ecosystem through an economic incentive strategy, thereby incentivizing liquidity providers to provide maximum liquidity.

In 2019, there is another trend in creating liquidity, which is to create debt for the locked-up assets in the Staking business and maximize liquidity.

For example, in the Stake DAO service launched by Staking service provider Stake Capital, in order to release the liquidity of mortgage assets, a derivative of liquid assets (LToken) based on mortgage assets was invented. This token was generated at a ratio of 1: 1. Can be traded on the secondary market.

A similar model is Acala Network. This is a DeFi project initiated by a Chinese team.The solution will support the mortgage of Staking assets in the Polkadot network to generate stable coins, thereby maintaining the holder's continued access to mortgage income, while simultaneously releasing the liquidity of the mortgage assets and participating in it. Financial services such as centralized lending, leveraged transactions, and crowdfunding of quality projects. This means that DeFi can be applied to staking that lacks liquidity, which can create debt for locked-up assets and maximize liquidity.

Aspect Eight

Structural limitations of decentralized lending

In the field of decentralized lending, MakerDAO continues to hold an absolute leadership position in 2019. In 2019, MakerDAO upgrades from single collateral (Sai) to multi-asset collateral (MCD). In addition, it also introduces the much-anticipated Dai Deposit Rate (DSR), which is annualized at 4%, which is equivalent to the USD With a current account, users can deposit and withdraw without any counterparty risk. DSR is essentially a smart contract that can be integrated into any exchange. Its introduction is of great significance and it will become the benchmark interest of the DeFi ecosystem.

In the long run, if the development is smooth, DSR may become unsecured savings interest rate, which is equivalent to the impact of central bank reserve interest on commercial bank interest.

In addition, both Compound and Fulcrum have created funding pools that allow users to borrow and lend crypto assets, including Dai, USDC (Coinbase's stablecoin), and ETH.

Dharma, originally a competitor of Compound, underwent a major revision in 2019. The new version of Dharma is developed based on the Compound protocol. The "Computer Liquidity Pool" realizes "instant matching" to provide lenders with the best interest rate instantly, thereby solving the problem of delays previously complained by users. This means that the two parties have changed from a competitive relationship to a symbiotic relationship. It is also determined by the openness and combinability of DeFi open finance.

In the traditional lending market, barriers to entry are high. Generally, there are a few large companies that compete for efficient distribution of capital after obtaining capital. There is little competition and the company is highly structured.

Compared with the traditional lending market, the advantage of decentralized lending is that it can be accessed without permission. Massive sources of capital can directly compete for capital allocation. Not only that, DeFi's compatibility and composability also means that it must face competition from funds from other lending agreements. DeFi, a license-free lending model, will attract more market participants, and this situation has already emerged.

However, decentralized finance is also accompanied by structural limitations. A big advantage of traditional lending companies is that because they have a firm grasp of lender information and can rely on legal systems to force borrowers to fulfill their repayment obligations, they can borrow without the need for a mortgage or partial mortgage.

Decentralized finance requires excess pledges, which means low capital utilization. To solve this structural inefficiency problem in the DeFi field, we must solve the problem of decentralized identity, that is, how to ensure that the decentralized identity does not violate user privacy while ensuring that the decentralized identity takes effect. There are still contradictions in solving this problem.

Aspect 9

How to reduce the decentralized mortgage rate?

"Low mortgage rate" will be the future of DeFi. So how to reduce the loan mortgage rate in the DeFi ecosystem and improve the utilization rate of funds?

One solution is to build a credit market DAO, share loan risks by forming alliances, and share profits from interest rates. DeFi loaned new player Maple, which is trying to: As staking generates fixed interest to guarantee a portion of the income, the mortgage rate can be reduced by staking a fixed future known income.

Another credit union called "Union" uses the design of "credit cooperatives". In this mechanism, members who join the DAO organization can use Staking DAI or similar interest-generating crypto assets to calculate the corresponding value based on the joint curve. Shares, Staking assets will be sent to other currency markets to earn interest, and these interest will be pooled into a loan pool, where the funds can be lent to DAO members without collateral or partial collateral.

Another solution is to use zero-knowledge proofs (ZKPs). This solution can resolve Sybil attacks generated by partial mortgages without displaying public ID data. You can get a credit score without revealing any privacy. There are currently two options. One is to integrate data from various platforms in Web 2.0, such as granting credit to social platforms such as Airbnb or Uber, and integrating income-related data, but this method is "semi-centralized." Another approach is to extract data from traditional finance, but this approach significantly slows down the process and implements censorship.

Not only that, adding high-quality and less volatile assets can effectively reduce the mortgage rate. For example, in the case of Uniswap supporting real estate as collateral and the "real assets entering the DeFi system" mentioned in the above article, the Maker Foundation united the German supply chain The financial blockchain platform Centrifuge has launched a series of pilot experiments in areas such as logistics, real estate, and streaming music supply chain industries that have "long repayment cycles and large funding gaps in each stage of operation", all of which have increased physical asset access. DeFi system, which will effectively reduce the mortgage rate.

In addition, there is another way is to combine a decentralized identity system solution and a staking mechanism, allowing users to staking their personal reputation to reduce the loan interest rate. The more reputation they invest, the lower the mortgage rate. This scheme can incentivize top borrowers to always pay on time. paragraph.

If all of these are verified in 2020, large-scale development can be achieved, which is the key element to truly take off in the DeFi field.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Iran's Bitcoin price soars? The real situation may be just the opposite

- South Korean government agency proposes "South Korea's Nasdaq" to launch BTC trading? By no means unfounded!

- PoW will be replaced? PoC may start a new era of mining

- The Blockchain 50 Index rose by more than 5%. Can you understand what the sample companies are doing?

- Third World War Phantom strikes, digital gold BTC may usher in a super bull market

- Global blockchain ebb in 2019, China's "dominance" strengthens

- Industry still wait-and-see on SEC's proposal to expand "qualified investor" scope