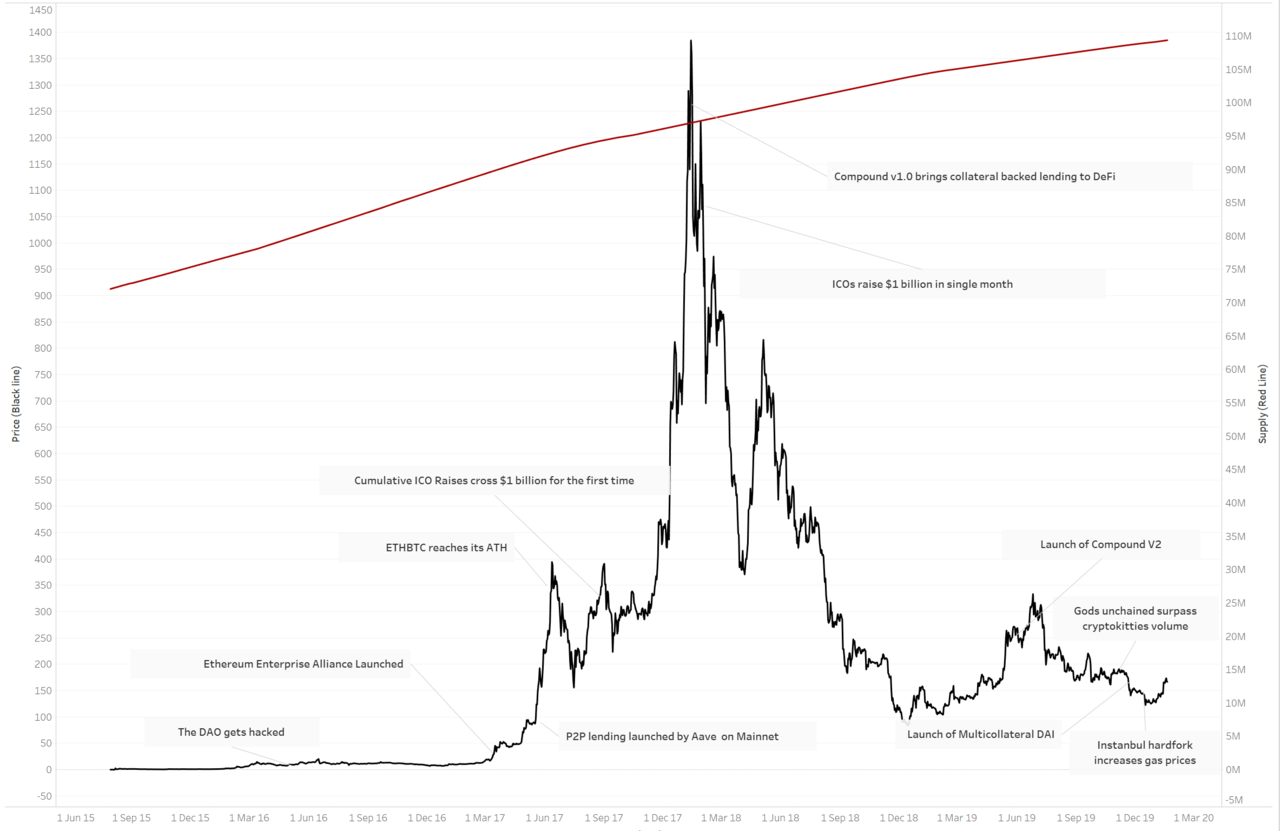

Viewpoint | Historical data inventory, see the evolution of Ethereum

The goal of Ethereum is to be a world computer. A lot happened along the way: being a cat dealer, being attacked at a fork, being a fighter against the dictatorship, and creating a new financial architecture. There are many sayings about Ethereum, some say it is currency, some say it is a failed product, some say it is a tamperable ledger, and so on. These evaluations are not very relevant. Ethereum is like a knife that can be used as both a tool and a weapon, depending on who the user is. Therefore, I started to explore the development of Ethereum by myself. I'm interested in this largely because I wrote an article on decentralized finance in May 2019. I found that almost all decentralized financial applications are built on Ethereum. This article is the result of my attempt to sort out all the data related to Ethereum.

-Photo source: https://twitter.com/joel_john95/status/1219543404117250049-

In this article, I have avoided comparing Ethereum to Bitcoin directly. Just as the financial system can emerge with various commodities, currencies and financial instruments, I believe that the digital asset ecosystem can also perform different experiments. If we believe in decentralization, one of the mechanisms that can achieve decentralization is to save multiple ledger backups, because a single ledger is more vulnerable to the impact of the Black Swan incident. In a world dominated by "ledgers," there is no room for such experiments. But for exactly the same reason, I support multiple ledgers, as long as these ledgers can play their role, and it is not wrong. I hope to reflect the development of Ethereum through this article, instead of demeaning Bitcoin or Ethereum.

- Weekly development of industrial blockchain 丨 Blockchain policies are frequently promulgated, and many points of government application blossom

- Viewpoint | Blockchain-based fintech is a weapon for epidemic prevention

- DeFi week selection 丨 bZx should be stolen? How should DeFi be taxed

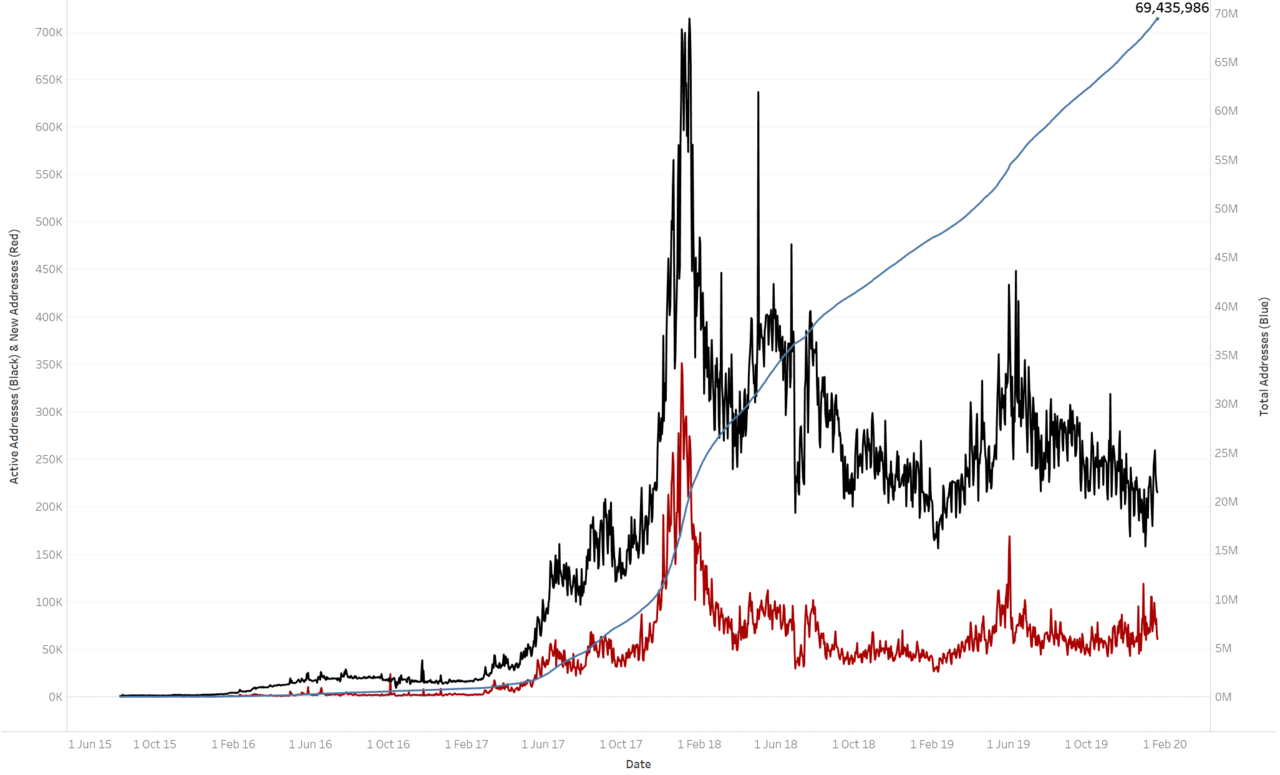

Growth in number of addresses and activity

-Number of active addresses in Ethereum (red lines indicate new addresses, black lines indicate active addresses, blue lines indicate the total number of active addresses)-

There are 69 million addresses on Ethereum, and only about 250,000 addresses are active every day. Among them, 50,000 are actually new addresses. Since the cost of creating a new wallet or transferring assets on Ethereum is lower than most networks, the data itself is not eye-catching. What makes me interesting is that the number of active addresses and new wallets is much higher than at the time of the ICO boom in 2017. A key factor may be the switch from USDT to the ERC-20 standard, and the emergence of many coin mixers on Ethereum (mixers, which serve as a transit point for multi-person transfers to obfuscate the flow of funds and protect user privacy). In 2019, approximately 226,000 different wallet addresses have interacted with decentralized financial applications. These users are most likely super users and will often use wallets. Although the field of decentralized finance is very attractive, it may be non-homogeneous tokens (NFT) and digital gambling that will support wallet activities on Ethereum in the future. Games such as Axie Infinity and Gods Unchained are driving a new generation of users to use the Ethereum network unconsciously. It's like a gradual transition from Internet chat rooms (IRC) to WhatsApp. The former is functional, while the latter has become mainstream. As the complexity of ledger interactions continues to decrease, more active addresses may emerge in the future.

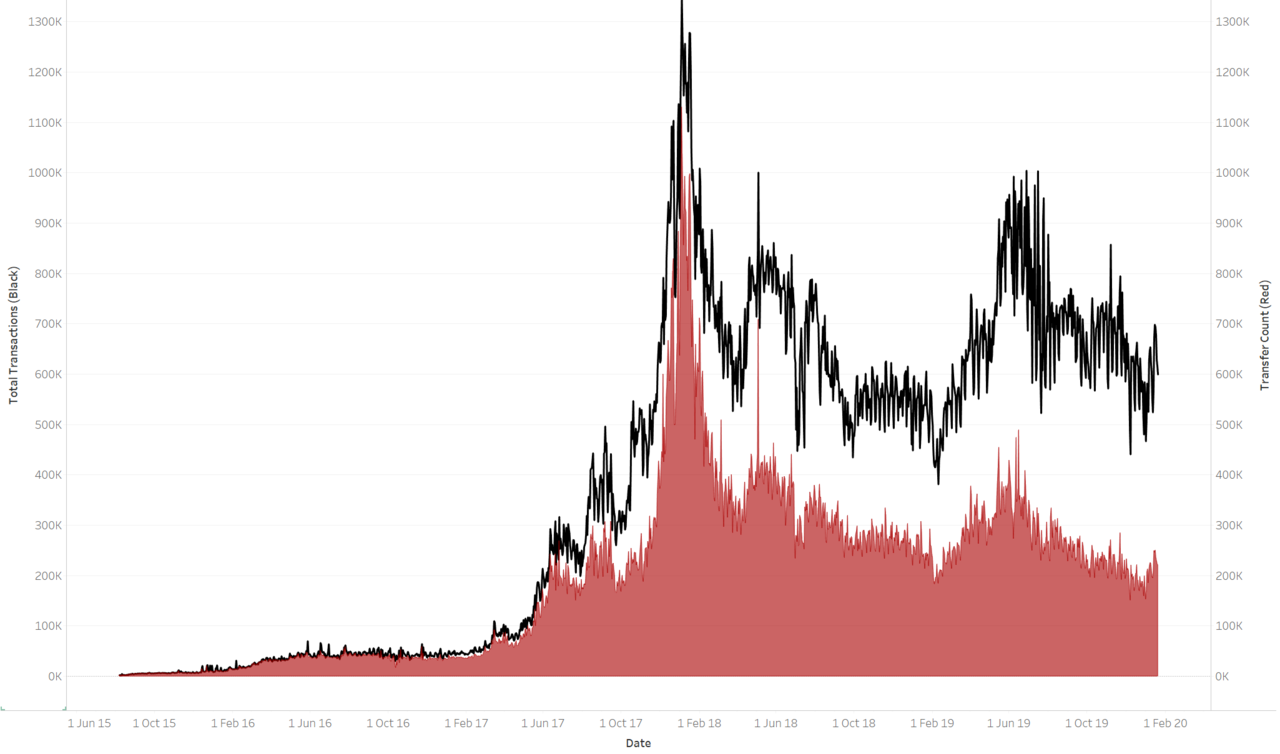

So far, Ethereum has processed 900 million transactions

-(Red indicates the number of transfers, black line indicates the number of transactions)-

If the number of active wallets and the number of new wallets are taken as an indicator of the number of people interacting with Ethereum, then the number of transactions is an indicator of their frequency of transactions. We can see the striking similarities between the previous two pictures. Compared with the hot year of the ICO, the number of transactions and transfers has not fallen significantly. This is largely due to the growing maturity of decentralized finance and liquidity pools. If the total number of addresses on Ethereum drops, it may be inferred from this that the remaining users are superusers and often initiate many transactions. However, neither indicator has declined, which indicates that

(I) Since 2017, new users have made up for the number of lost users

(Ii) The transaction frequency of new users is the same as that of investors in previous ICOs

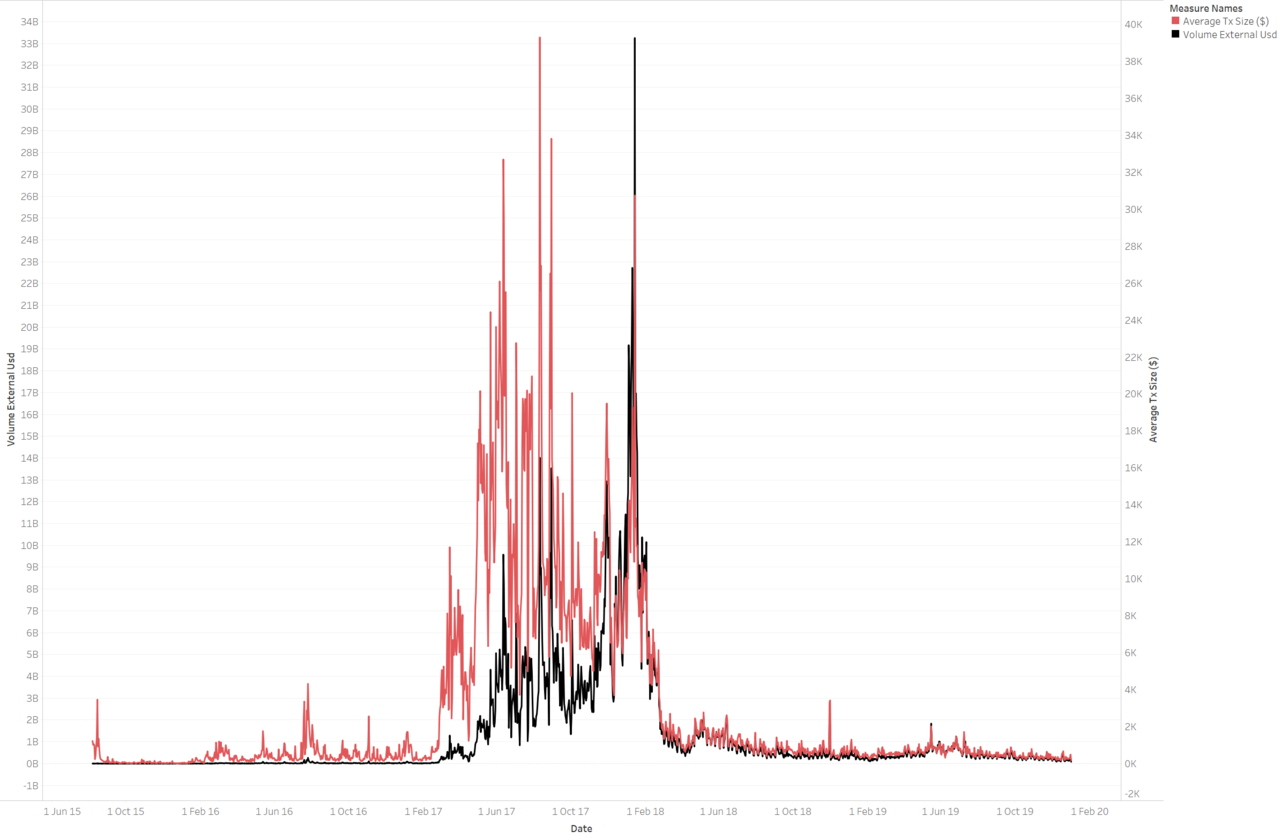

What really changed is the next indicator-the average transaction size on Ethereum.

Total transaction size reaches $ 2.1 trillion

-(The red line is the average daily transaction size, and the black line is the total daily transaction volume, all measured in USD)-

The average transaction size peaked on August 11, 2017, with nearly $ 40,000. The total transaction volume on the Ethereum blockchain reached its peak on January 14, 2018, which was $ 33 billion. These two data can be linked to the popular use of Ethereum at the time. The ICO boom first appeared in August 2017 and attracted more than $ 1 billion in funding by the end of September. On the other hand, since Bitcoin experienced a price adjustment in December 2017, the altcoin boom reached its peak in January 2018. However, the future still needs to look forward and not indulge in the past. The number of active addresses and transactions shows the number and frequency of transactions on the Ethereum ledger, and the average transaction size reflects the amount of funds transferred. As of the date of writing, the average transaction size was around $ 138. Based on these indicators, we can clearly see the popularity of digital assets.

simply put:

- The number of transactions has increased 6 times since February 2017

- The number of active addresses has increased approximately 10 times since February 2017

- Total on-chain transactions have increased approximately 12 times (from $ 11 million to $ 128 million)

- However, the average transaction size has been reduced by about 99.5%.

As non-homogeneous tokens mature, the average transaction size is likely to decline further. Generally speaking, Ethereum users do not need to transfer large amounts of Ethereum. If the number of small traders increases, it means that Ethereum is more attractive to users. In addition, this can be measured by the amount of ether in the top-ranked accounts.

The largest top 100 wallets hold about 30% of Ethereum

-(The red line is the number of coins held in the top 100 wallets of the exchange, the black line is the number of coins held in the top 100 wallets outside the exchange)-

Once we consider the proportion of Ethereum in the top 100 addresses, it will be more obvious to see the popularization trend of Ethereum. Including the wallet of the exchange, the number of Ethereum in the top 100 addresses accounts for 1/3 of the entire network, which is about 32%. For such a project supporting "decentralized finance", this number looks a bit scary, but it is gradually decreasing. According to Glassnode, by comparison, about 11% of Bitcoin's circulation is held by exchanges, and 8% of Ethereum's circulation is held by exchanges. Since November 2018, large Ethereum currency holders seem to be tuning coins. There are several explanations for this:

- Investors who were diversified during the peak of the coin price in 2018 are currently buying Ethereum. Now they can use the lower price to buy the ether sold in the year.

- The price of Ethereum has fallen sharply since its historical highest price, and some investors no longer sell Ethereum, so the proportion has stagnated and there has been no significant decline.

- As more and more retail customers buy Ether, the cost of holding a certain percentage of Ether increases. It is increasingly difficult to form new large households on the Ethereum network.

Another reason these big players no longer sell more Ethereum is that they can borrow in US dollars (decentralized finance) without going through traditional financial infrastructure. This is obvious if we analyze the decentralized finance through the power law. Generally speaking, 3 to 5 large households will own 60% to 80% of the total assets in a product. (For more details, please refer to my article on InstaDApp.) Another reason is that Ethereum has retained a large group of currency holders because they are very optimistic about the prospects of the Ethereum network. I think this is a sign of support.

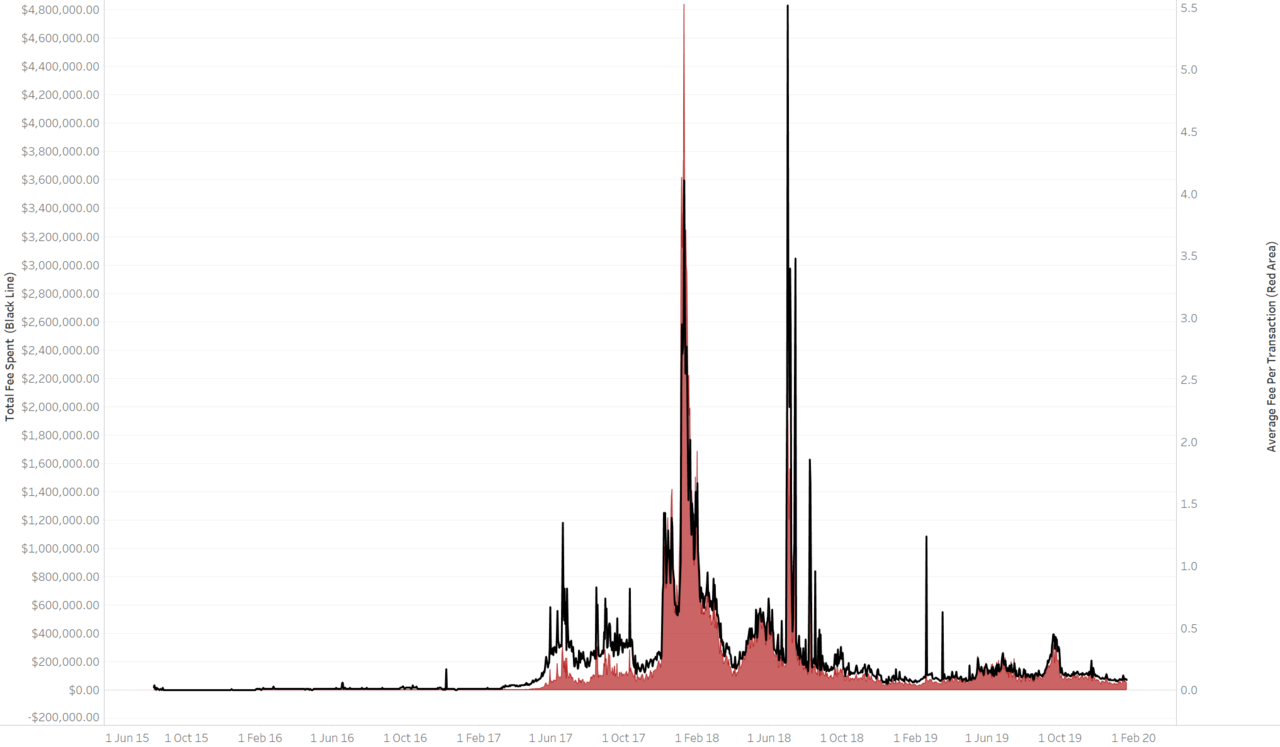

Ethereum transaction fees have reached around $ 242 million

-(The black line is the total fee, the red line is the average fee scale based on the number of transactions)-

The transaction costs of the Ethereum network amounted to $ 242 million. Interestingly, the historical peak of transaction fees was not during the ICO boom in 2017, but in 2018, when the total transaction fees at that time were $ 160 million. In comparison, the transaction fee in 2019 was only $ 34 million, which is similar to 2017. In February 2018, the cost of each transaction skyrocketed to $ 5.5, and today it has dropped to $ 0.1. Although the current transaction cost is very low, compared to the February 2017 period, the 0.03 USD before the surge in the price of Ethereum has more than doubled. As transaction fees fluctuate, this can adversely affect products built on Ethereum. Developers must consider the transaction costs incurred by small transactions. Decentralized computing and storage services usually need to deal with the risk that the cost of gas is too high, otherwise customers will not be attracted. Some projects are working to resolve this issue. For example, with Gasless by Mosendo , users do not need to hold Ether to pay for gas fees, and they can transfer DAI.

Similarly, there will soon be a batch of API-level projects, which will directly charge the enterprise while conducting transactions on behalf of end users who do not hold Ether. Nuo Network has now launched a similar earlier version. In the long run, if the price of Ethereum rises sharply, more complex derivatives and futures will emerge, and transaction fees can be hedged on a large scale, just like the traditional financial world today.

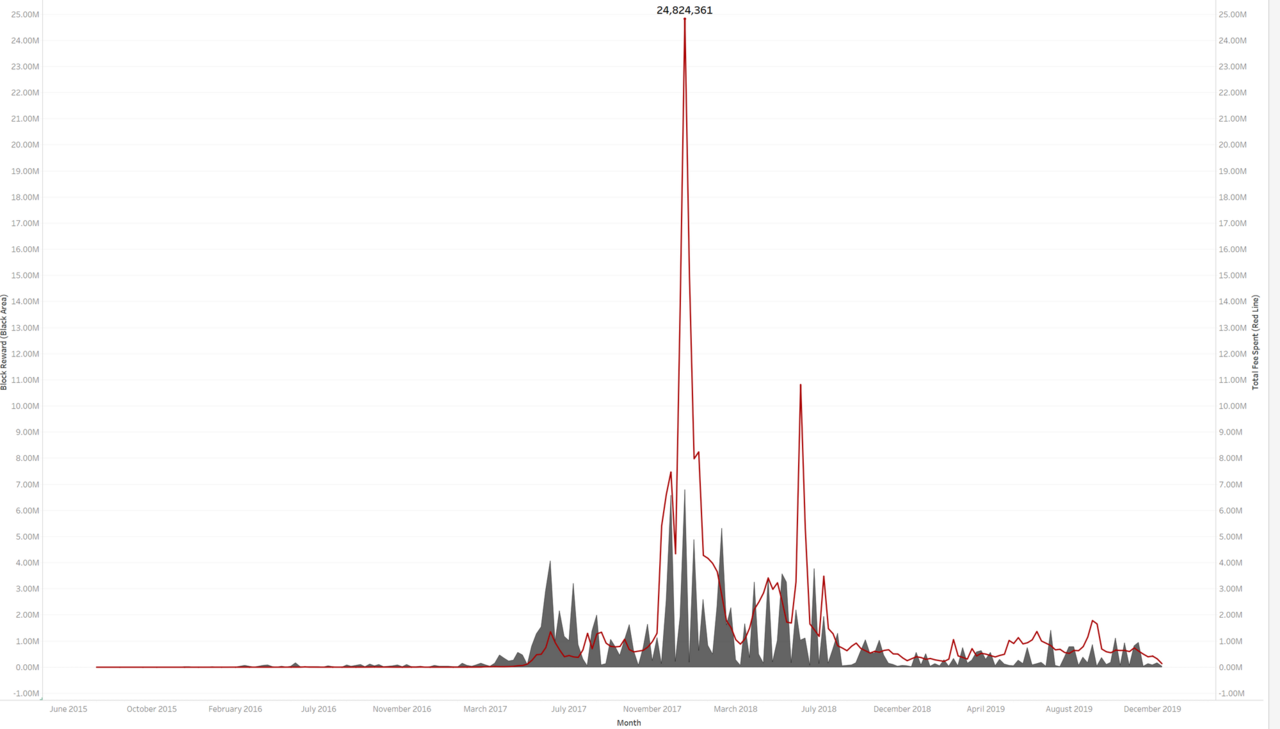

-(The black part is the scale of the block reward, the red line is the scale of the fee)-

Once you compare the block reward with the accumulated amount of transaction fees, you will find an interesting feature of Ethereum. Over the past 5 years, the total block rewards have reached $ 150 million. It can be said that, so far, Ethereum has paid about 300 million US dollars to miners, but in front of Bitcoin, it is a small witch. So far, Bitcoin has paid 16 billion U.S. dollars to miners. Judging from the transaction volume we see in the derivatives market, it can be said with certainty that given the cost mechanism of the two, people will prefer to mine Bitcoin over Ethereum. I also find a common explanation that Bitcoin miners also consider mining Ethereum as a sideline. Due to bullish expectations, miners usually hold net long positions. I find that the balance of the miners fluctuates with the fluctuation of the currency price, which confirms this even more.

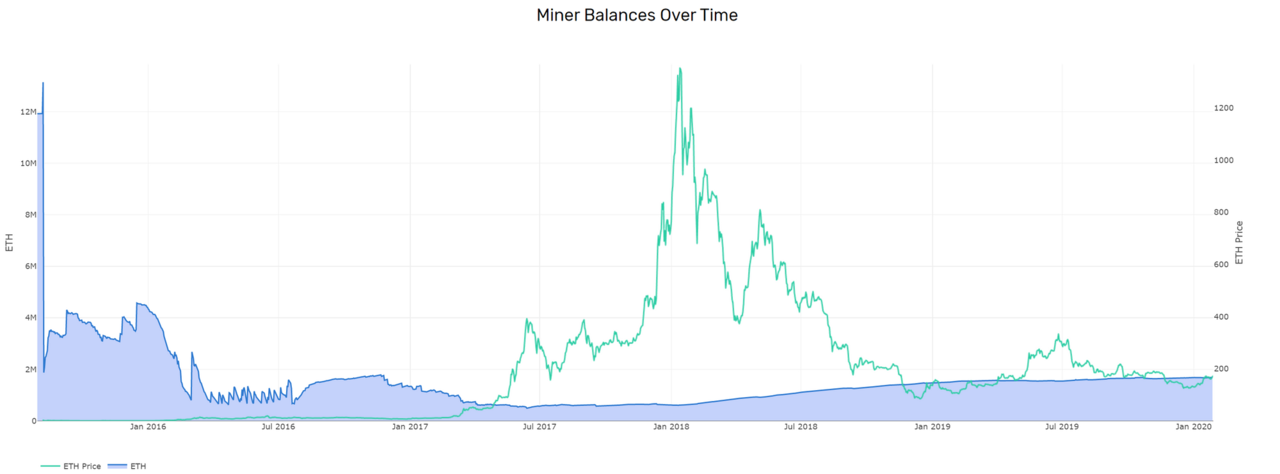

-Source: San Graphs (blue line is the price of ETH, dark blue is the number of coins held by the miner's address)-

In the past few years, a number of factors may have affected the behavior of miners. My understanding is that between January 2016 and January 2017, given the low transaction price of Ethereum, Ethereum seems to be just a popular ticketing project in the geek community. The first plunge in the price of Ethereum at the end of 2016 was after the "The DAO" incident, when Ethereum was in a recovery period. In March 2017, the Ethereum Enterprise Alliance was established, the currency price rose to US $ 40, and then there was another round of decline. With the soaring Ethereum price, block rewards and transaction fees can ensure the stable operation of Ethereum, and the balance of miners has reached a low point. Over the past year and a half, miner balances seem to have been increasing. In the past 18 months, the amount of ether held by miners has soared from 600,000 to 1.6 million. This group is the real coin hoarding party. However, to study the behavior of non-currency holders, we need to understand the situation of the exchange.

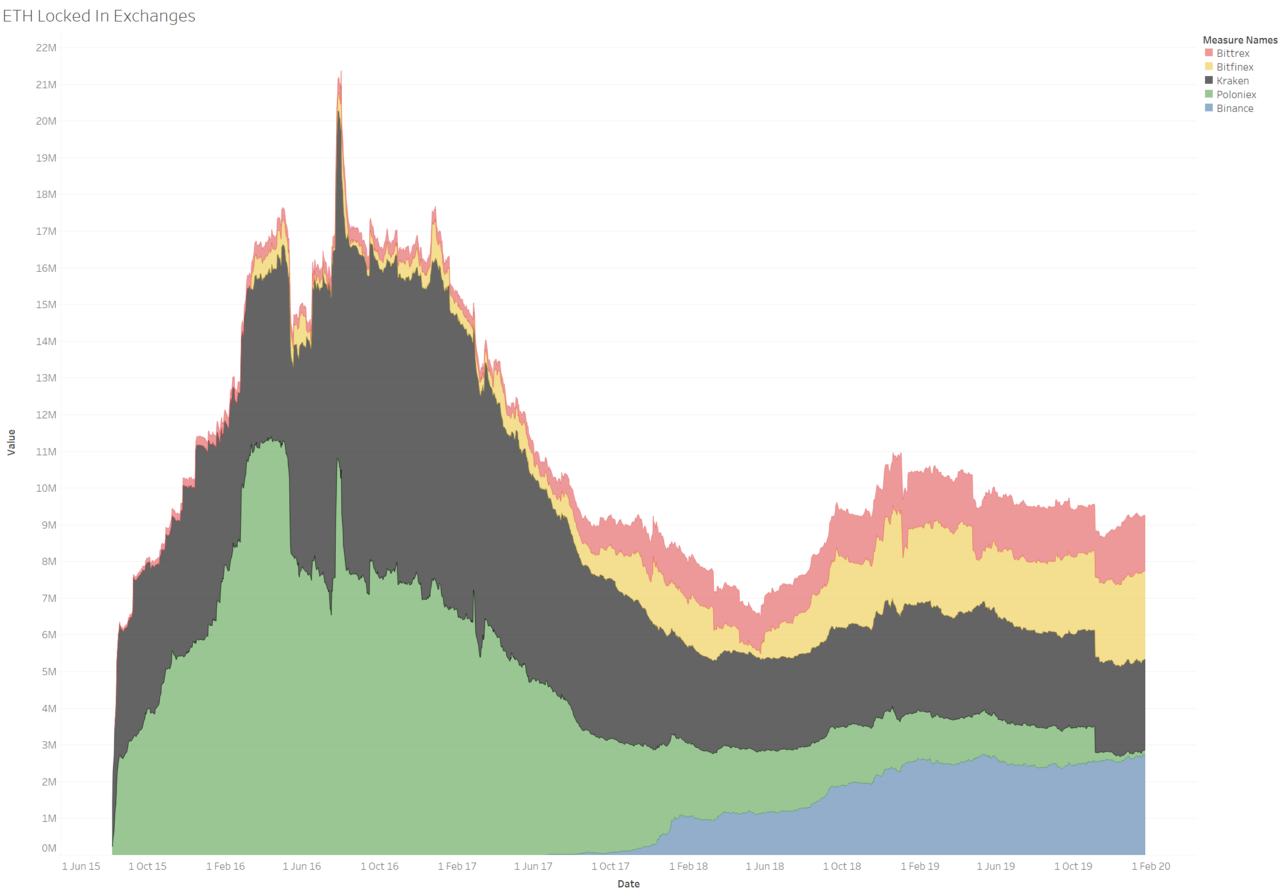

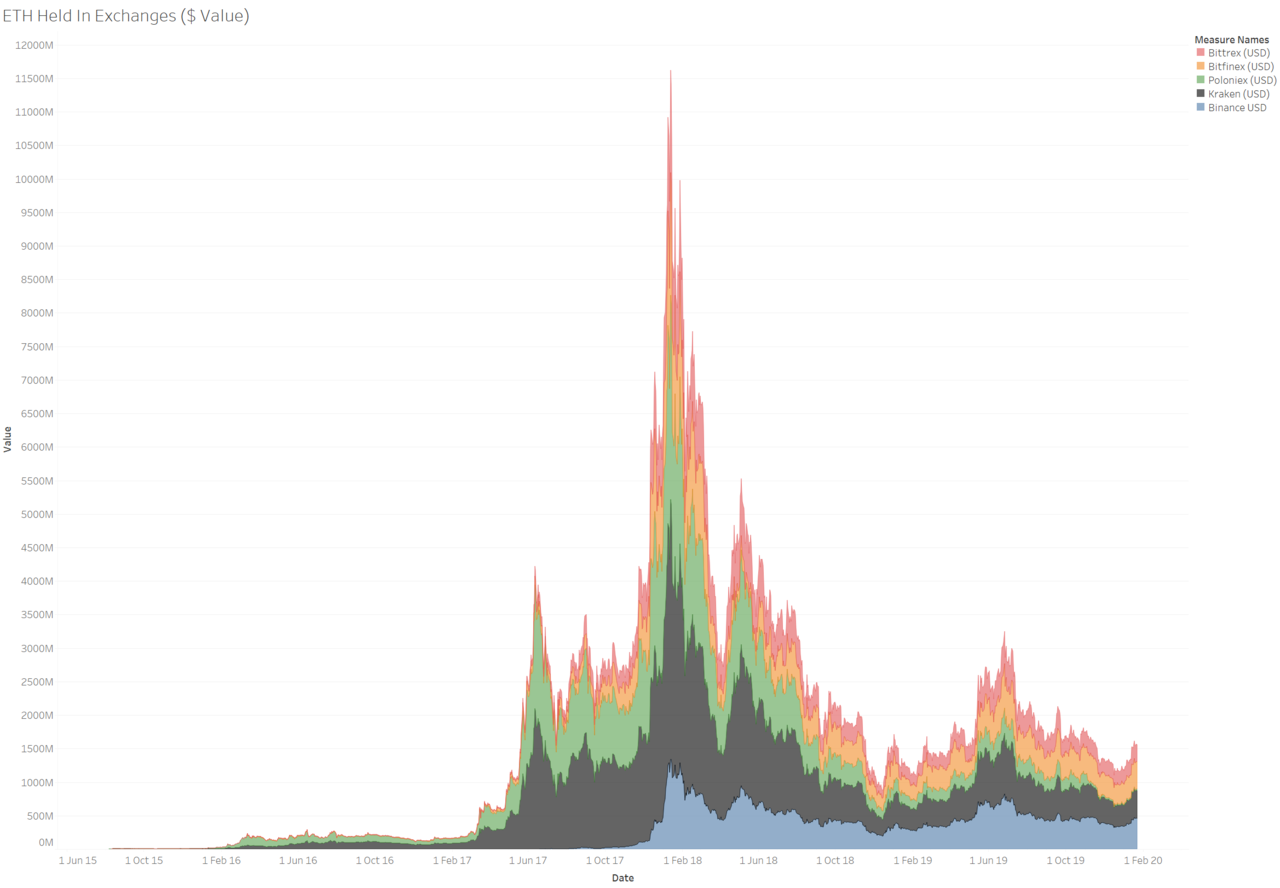

During the bull market, the exchange held ether worth $ 11.5 billion

-(Number of ETH held by each exchange)-

-(Value of ETH held by each exchange, denominated in US dollars)-

The reason why Ethereum can achieve such a scale and achievement is that a robust exchange ecosystem may be a key factor. Unlike today's listing of new coins, Ethereum's threshold for listing on Kraken and Poloniex, then the largest exchanges, was very low. But then again, if it were not for Ethereum that lowered the threshold for asset issuance and built a community around new assets, we would not see nearly 1,600 digital assets emerging in the market today. I dare not imagine what the token ecosystem would look like without Ethereum. After putting these charts together, I noticed a key piece of data, that is, the amount of Ethereum in circulation on the exchange is lower than that of Bitcoin. According to glassnode data, the supply of bitcoin is 18 million, and the number of bitcoins held by the exchange is about 2.1 million (accounting for about 11.6%). In contrast, the supply of Ethereum is 109 million, and the number of Ethereum held by the exchange is about 9 million (8.25%), which is slightly lower than Bitcoin. This is largely due to the relatively fast speed and low cost of Ethereum transactions. Because of the fast transaction speed of Ethereum, it is easier for people to transfer assets and profit from it when the currency price fluctuates sharply.

Note: The amount of Ethereum actually held by the exchange may be a few percentage points higher, because my data source does not include the balance of Coinbase.

After studying these data, I came to two other conclusions

- Since 2016, the amount of ether held by exchanges has been reduced by 50%. This may indicate that fewer and fewer people see Ether as a speculative asset.

- Currently, the total value of Ethereum held by the exchange is $ 1.5 billion. In contrast, as of the time of this writing, the value locked in decentralized financial smart contracts is half of the exchange, at $ 875 million. After the Ethereum locked in decentralized finance exceeds the exchange, a big reversal will occur.

What follows is the last indicator reflecting the current state of the Ethereum ecosystem-the ICO balance. But this indicator makes me a little worried.

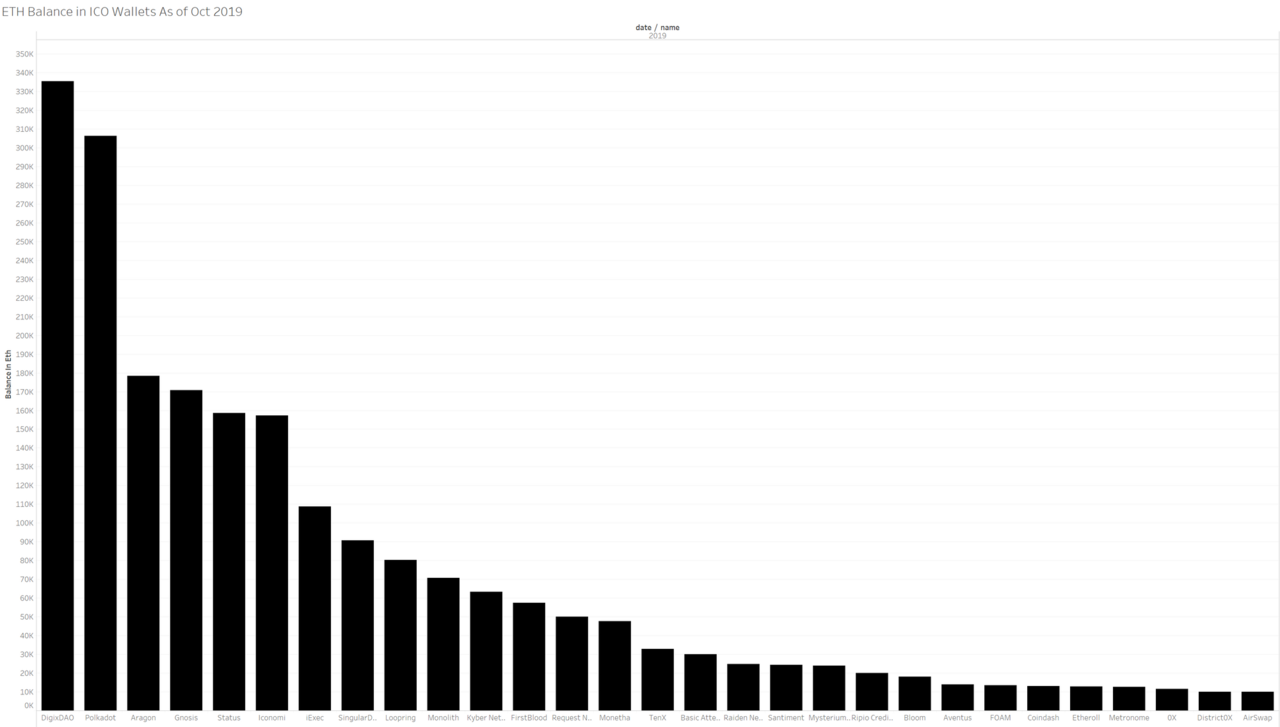

Major ICO project funds rush

-The largest ICO wallet as of October 2019-

During the ICO boom, major projects raised around $ 8 to 16 billion (the data sources vary, and the specific amounts vary). At present, the value of Ethereum held by major ICO projects is about 500 million US dollars. In the past two years, various project parties have been burning money, and it seems that there is nothing left. Take EOS as an example. Although EOS raised $ 4 billion and spent $ 30 million to acquire http://voice.com , it still failed to build its own social media platform on the chain (maybe it wants to build on bitshares One, haha [spread your hands]). If the network does not generate fees or the platform does not generate revenue, the project party can only raise risk funds or fail. At the end of 2019, we have seen many projects fail. By 2020, if these altcoins disappear, ICO projects are completely yellow, and assets will shrink sharply, these projects will have big troubles. There are two main reasons

- For the past two years, the project party has been burning money, but no progress has been made.

- The indicators of these ICO projects will become worse and worse, and there will be no sudden growth like MakerDAO, and later financing does not look optimistic.

Poor project prospects, lack of investment, low market adaptability of products (for example, Bancor and Uniswap), and the fact that funds are about to run out, are things worth reflecting on for the entire industry and community. This is not necessarily a bad thing. Funding rushes often turn entrepreneurs into survival models and focus on key performance indicators rather than just burning money. It may also motivate entrepreneurs to conduct experiments that have never been done before and develop entirely new business models. In the next few years, we will see a large number of projects fail.

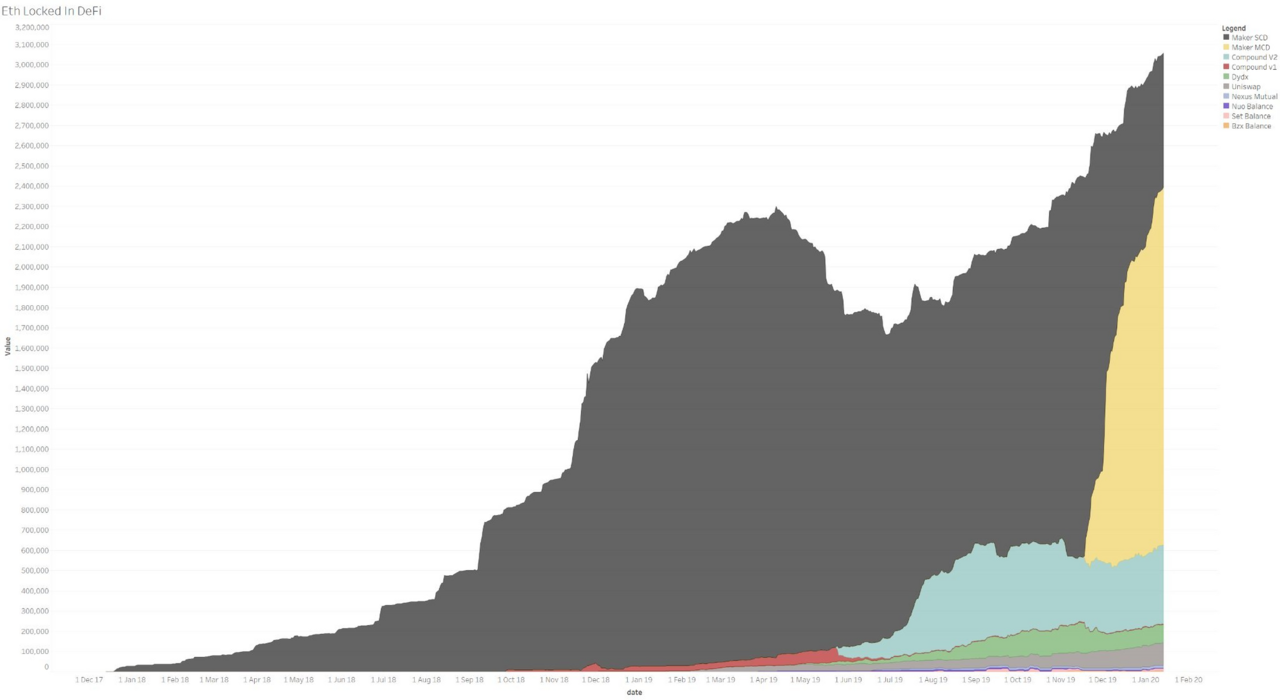

Since March 2018, decentralized finance has grown by 30 times, and Maker has made great contributions

-(Number of ETH locked in each DeFi project)-

Since 2017, decentralized finance has grown 30 times, largely due to Maker's credit. A key reason is that because the price of tokens is too volatile, stable assets are needed as a hedge. Since the emergence of Tether, stablecoins have become popular. In addition, as the price of Ether hits a new low (ie, $ 80), projects like MakerDAO allow Ethereum big whales to leverage the Ethereum they hold through Maker. In any case, since 2018, the decentralized financial sector has seen considerable growth. Interestingly, the locked Ethereum in decentralized finance shows a clear power law. In the field of decentralized finance, locked Ethereum is mainly used to generate SAI and DAI, and Compound is ranked third. Trading tools such as Uniswap and DyDx also aggregate some Ether, but not so much. It seems that the market has already decided on its own preferred currency issuance agreements. Projects such as Synthetix are experimenting with new models that use Ethereum and SNX tokens to issue assets. Synthetix is currently growing. It can also be seen from the figure that the industry does need new business models. Ethereum and transaction fees locked in the project alone may not be enough to support a for-profit enterprise. Hope we can see more new projects in 2020.

The power of Ethereum comes from its users

-Github activities for several mainstream projects (the top line is Ethereum, the purple next is Bitcoin, the second is EOS, and the blue line below is Maker)-Source: Santiment-

Finally, what makes Ethereum unique is its users. The more users Ethereum attracts, the richer its network becomes. When people think of Ethereum and its community, there are usually controversial events (such as ICO, "The DAO" fork, etc.) that seem unacceptable to them. However, they often overlook that these events occur precisely because the Ethereum network can attract all kinds of people. Most of them are developers. Compared to other networks (and their github activities), Ethereum has been far ahead, even in the long bear market before. It is precisely because Ethereum has always promoted innovation that so many innovative projects have emerged in the fields of decentralized finance, non-homogeneous tokens and token issuance. As long as this momentum is maintained, Ethereum can gain greater influence in the market. Whether this impact is worth $ 10, $ 100, or $ 1,000 is not clear to me. The efficient market hypothesis and time will tell us the answer.

Conclusion

Although Ethereum has experienced many twists and turns along the way, I believe that the entire network has been improving. Maybe some people think that Ethereum has a false name, but it has never seen a chain like Ethereum that has ENS, decentralized finance, non-homogeneous tokens and ICOs. Ethereum and its community have a long way to go before Ethereum becomes mainstream. But when I was in contact with the Ethereum community and communicating with the Ethereum founders, I became more and more feel that this is very similar to Ubuntu / linux from 2007 to 2008 (just like my first contact with them. ). The learning process is difficult, but the community is very interesting. Although the product is incomplete, it has been updated slowly. Most importantly, I have a range of products for my daily use. I don't know if all this can add value to Ethereum. I think Ethereum (and tokens like Bitcoin) are still useful, even if they plummet by 90%. Not long ago, Ethereum fell all the way to $ 80. My focus has always been on practicality and how to get the end user as fast as possible. I know that this article does not include all the advantages of Ethereum, and I hope to write more details in the next few weeks.

(Finish)

Original link: https://www.decentralised.co/ethereums-numbers/

Author: Joel John

Source: Ethereum enthusiasts, original title "Viewpoint | Ethereum Development from Data over the Years"

Translation & Proofreading: Min Min & A Jian

This article was translated and republished by the original author with permission from EthFans.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Is Ethereum resistant to Asic mining? No, this is a rumor!

- Analysis of the main organizations in the Cosmos ecosystem: Agoric, Regen, Lunie, and Chorus One

- When the real crisis comes, the safe haven Bitcoin is forgotten

- Babbitt weekly election 丨 FCoin came to an abrupt end after a thunderstorm; "Mentougou" bitcoin whale lost thousands of bitcoins

- Data decreased slightly, rumors triggered a single-day net outflow of Binance

- Weekly | Central Bank issues technical specifications for financial distributed ledger, blockchain financial applications are expected to accelerate

- Interpretation | Five Misunderstandings of Ethereum 2.0