Watch | What are the similarities and differences between the Bank of England's digital currency plan to "abandon" blockchain and China

Source of this article: Interchain Pulse

Author: Yuan Shang

This month, the Bank of England (Bank of England) released a 57-page discussion report on Central Bank Digital Currency (CBDC) "Central Bank Digital Currency: Opportunities, Challenges and Design", which is a report closer to the ground.

After 6 years of thinking, this month, the Bank of England (Bank of England) released a 57-page discussion report "Central Bank Digital Currency: Opportunities, Challenges and Design", which is a report closer to the ground .

- Video: Exploration, Application and Prospect of Blockchain in Digital Marketing (Part 2)

- The Mentougou case triggered a panic of BTC selling. Is the market overreacting?

- International Securities Regulatory Commission: Global stablecoins may be subject to securities regulation

It is worth noting that this discussion paper clearly states that "Although many CBDCs are associated with distributed ledger technology (a technology used by blockchain), the UK's CBDC does not have to be based on this, and there is no reason to indicate that the center Institutions cannot build a CBDC. "The Bank of England began to study CBDC in 2014. This is the first time the Bank of England intends to abandon the blockchain.

This is in line with the concept of the digital currency DC / EP being developed by the People's Bank of China. According to the mutual chain pulse, the digital currency of the People's Bank of China is not based on blockchain.

In other respects, in the discussion draft, there are still many differences between the Bank of England's CBDC design and China's DC / EP.

Abandon the blockchain

In February this year, the Bank of Sweden started its experiment with CBDC, a project led by Accenture and built on Corda, the blockchain alliance R3. Prior to this, there were blockchain-based digital currencies issued by Uruguay, Venezuela, Ecuador, Tunisia, Senegal, and Iran. However, none of them became popular.

The Bank of England's earliest involvement in blockchain-based CBDC research. In 2014, the Bank of England released an important report, "Innovations in payment technologies and the emergence of digital currencies." This is the first time the global central bank has discussed digital currencies. In 2016, at the suggestion of the Bank of England, researchers at the University College London proposed and developed a legal digital currency prototype system, namely the Central Bank Cryptocurrencies-RSCoin system. Subsequently, the Bank of England began experimenting with the system.

However, the blow came one after another. In 2017, the Bank of Canada conducted experiments and believed that Corda based on distributed ledger technology did not meet the needs of the Bank.

In March 2018, the Bank of England experimented with RTGS (real-time full payment system) to 4 technology companies, only to prove that the Bank's RTGS can be connected to the blockchain system. The experimental results were published in July 2018. The participating teams only had two team systems that could connect to the RTGS system, and the systems of the other two teams were far from the central bank's RTGS system and could not be connected. The participating teams are Baton, Clearmatics, R3, and Token. This quiz is just a connection. If the operational requirements are to be met, none of the four teams can achieve it.

In March of that year, the Bank of England Governor Mark Carney stated that the Bank of England was "open" to the creation of a central bank digital currency (CBDC), but a reliable and reliable CBDC used in circulation cannot be achieved in the near future. "The main reasons are that distributed ledger technology is currently immature and that there may be risks in providing a central bank account for everyone."

The Bank of England's CBDC plan was progressing slowly, and it turned to private companies such as Fnality to advance. Until the launch of Libra and the advancement of China's digital currency, the Bank of England accelerated the construction of CBDC.

I do n’t know if it was inspired by the central bank ’s digital currency. For the first time, the Bank of England ’s March report stated that it is not necessary to use distributed ledger technology.

In the view of the Bank of England, the current financial payment system is based on a centralized basis, and the technology stack is mature. Why can't CBDC use centralized technology?

The Bank of England also believes that the related technologies of distributed ledgers can be completely disassembled, such as the cryptography and smart contract technologies involved.

The People's Bank of China has made in-depth research on what blockchain can and cannot do. In February of this year, the Blockchain Research Group of the Central Bank's Digital Currency Research Institute issued a clear statement: "The decentralized nature of the blockchain conflicts with the central bank's centralized management requirements. Payment services provided by the central bank cannot leave centralized account arrangements. It is built on a centralized system, which conflicts with the decentralized nature of the blockchain. Therefore, it is currently not recommended to transform traditional payment systems based on the blockchain. "

It can be said that China has created a road for central bank digital currencies to use no blockchain. The United Kingdom said, "I follow."

Double-layer structure vs single-layer structure

However, the Bank of England did not “follow” the People's Bank of China on the issue structure.

China's DC / EP uses a two-tiered framework, with central banks and commercial banks, respectively account-based and wallet-based. Users also need to open an account through an operating agency such as a commercial bank or a third-party payment company.

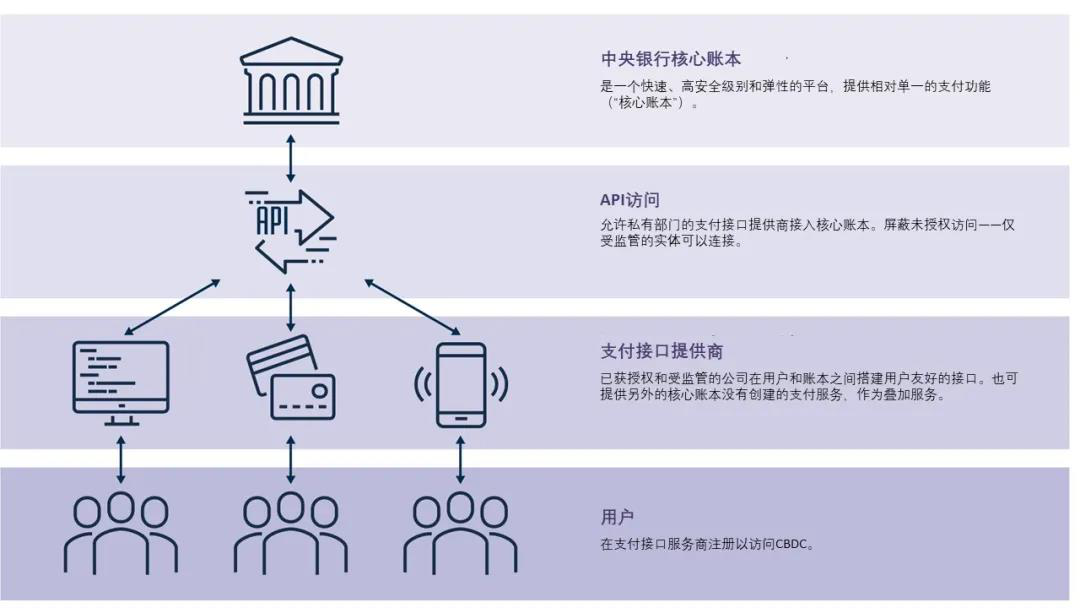

However, from the report "Central Bank Digital Currency: Opportunities, Challenges and Design", it can be seen that the Bank of England's model is that the central bank does the core ledger, and then opens the API to connect to any accessing private institutions to develop applications and provide payment services to users. Users directly use CBDC, and the central bank does the bookkeeping. -This is actually a single layer structure.

(Structure of the Bank of England report)

In fact, the Bank of England has followed this line of thought since it began researching digital currencies in 2014.

In this way, households and businesses use the central bank's currency directly for electronic payments. This change may affect the structure of the banking system and the central bank's main goal of maintaining monetary and financial stability.

First of all, commercial banks in the UK will be directly impacted by "disintermediation". The report gives an example. The user took out a £ 10 banknote from a commercial bank and exchanged it for a CBDC of £ 10. The balance sheet of the user has not changed, and the balance sheet of the central bank has not changed, but the commercial bank has lost £ 10.

Second, if the CBDC directly calculates interest, it will have a greater impact on commercial banks. At present, the interest rate is set by the central bank and implemented by commercial banks. However, with the CBDC central bank's ability to directly calculate interest for users' funds, a large amount of deposits will be directly transferred to CBDC, and commercial banks will face a liquidity crisis.

Fortunately, this is only a discussion draft, and it is unclear whether such a radical approach will be adopted in the end.

But the Bank of England did this to encourage innovation, hoping that private institutions could develop more CBDC applications. The report lists some possibilities. For example, a company is willing to apply for the API interface of the central bank account book, and then it can monitor the revenue and correspond to various categories of finance for paying wages and issuing invoices.

Other similarities

Compared with the digital currency of the People's Bank of China, another significant difference is the application of smart contracts. It is precisely because the Bank of England opened the digital currency API interface to the private sector, so the private sector can implement the deployment of smart contracts and realize the circulation of the CBDC. Moreover, you can trade with other digital currencies and other digital assets such as securities through smart contracts.

The current technical scheme of the Chinese central bank's digital currency does not support such operations.

In terms of technology implementation, the Bank of England has studied three methods:

1. Provided directly by the central bank's core account. But this requires a trade-off, both to be able to implement complex smart contracts and to achieve transaction performance. If smart contracts are applied on a large scale, it may overwhelm the centralized central bank digital currency system.

2. Develop an additional module dedicated to smart contracts. This module is responsible for processing the smart contract code, and only issues transaction instructions to the central bank's core account when payment is required. This method can reduce the pressure on the central bank system and has credibility.

3. Decentralized to suppliers that access the CBDC, but because the supplier's credibility is insufficient, only low-level permissions, such as locking funds and other functions, are delegated.

Because it was a discussion draft, the Bank of England did not specify which category it preferred.

There are also subtle differences between China and the UK in terms of regulation. The Bank of England report states that digital currencies in the UK must comply with three rules, including: the CBDC must comply with anti-money laundering (AML), the financing of terrorism (CFT) and sanctions, and compatibility with general data protection regulations (GDPR). Beyond that, there is no more expression on cracking down on crimes.

The Chinese central bank's digital currency must also comply with AML and its own privacy protection rules. But regulatory measures have also been designed to combat illegal activities.

Both Chinese and British digital currencies have requirements for offline payments. But it is unclear whether the Bank of England is single or dual offline. In this regard, China's DC / EP design is very advanced and supports dual offline.

Taken together, the central purpose of the Bank of England report is to improve the competitiveness of the British pound in the future global payment field. So the design ideas are bolder and encourage innovation.

Digital currency comparison table for China, Sweden and the Bank of England:

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- The founder of the Bitcoin Foundation: miss the early bitcoins, optimistic about the integration of China and the US market

- The most complete timeline of the MakerDAO Black Swan incident.

- Wu Jihan debuted on live broadcast: Bitcoin is hardly a safe haven in a volatile world

- President of the Beijing Internet Court: Black technology such as "Tianping Chain" provides advanced experience for the blockchain system of the court system

- What kind of blockchain project is worth investing in? Graph Network Data Tells You | Babbitt Industry Lesson

- Viewpoint | Ethereum 2.0 inspired by the Ethereum 1.0 upgrade

- Perspectives | Numerous entrepreneurial opportunities can be found through blockchain in the next decade