Chief analyst of the financial industry of Guosen Securities Economic Research Institute: Will the central bank's digital currency shake the banking business logic?

Source: Wang Jian's angle

The content of this article is from the reorganization of the old research results, the original text can be found in the text.

The information on digital currency in this paper comes from the current position of the central bank and may differ from the final plan.

- This weekend, the EOS network was blocked by an airdrop.

- Cai Kailong: Wuzhen World Blockchain Conference 10 points summary, my round table is so hot that "almost hit"

- Weekly data on the BTC chain: overall dull, Friday currency price jump triggers the net outflow of the coin over 4000BTC

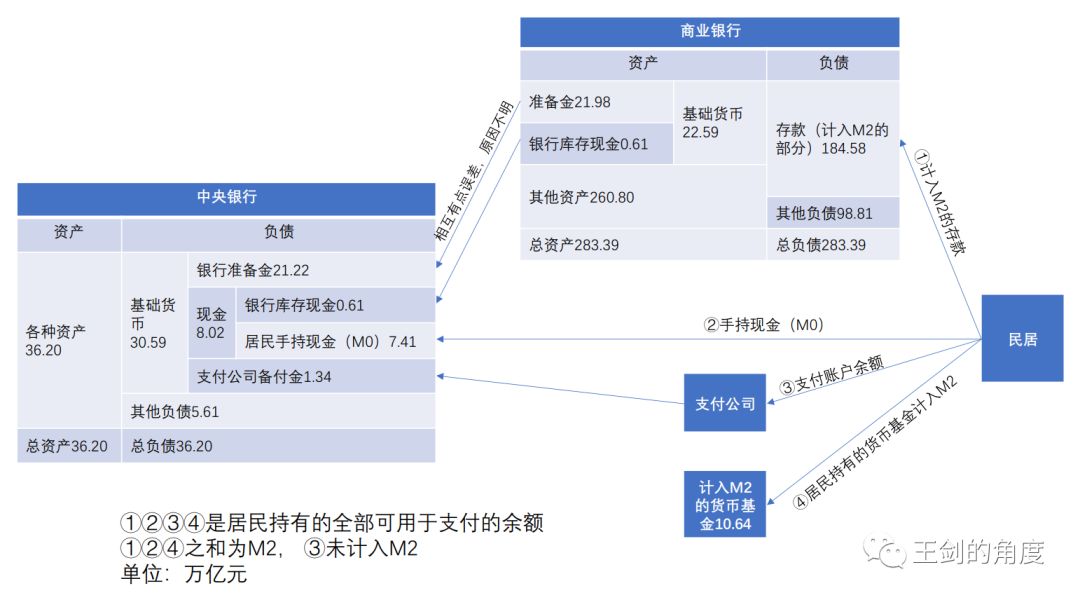

I. Existing monetary system

China's existing monetary system is a typical “central bank-commercial bank” secondary banking system , that is, the central bank issues the base currency to the bank, and then the bank uses the base currency as the reserve to the residents (that is, other than the bank). Industrial enterprises, non-bank financial companies, other institutions, individuals, etc.) issue broad money (the main body is the deposit of residents in the bank).

Note that when a bank issues a broad money, it does not issue the reserve (base currency) it holds to the residents, but issues the broad money out of thin air. As long as the deposit holders withdraw funds from the bank, the bank will use the reserve to deliver the reserve (base currency) to the residents.

Since not all depositors will withdraw money together, the broad money issued by the bank can be much larger than the bank's own real reserve. This is the "incomplete reserve system." For example, China's current bank has only 30 trillion yuan of base currency, but the broad money balance has been around 200 trillion yuan, up to 6 times. The central bank uses regulatory indicators such as reserve ratios to control this multiple.

For the introduction of the specific secondary banking system, please see our previous series of tutorials, "Financial and Monetary Balance Analysis Essentials of Financial Grand Cousins . "

However, in 2016, when the central bank required third-party payment companies (such as Alipay's Alipay, Tencent's Tenpay, etc.) to hand over the customer's reserve balance to the central bank, the second-tier banking system changed a little, that is, A party pays the company. The payment company is not allowed to take deposits, so the amount of the residents' deposits into the payment account is required to be transferred to the central bank in full. At this time, the payment company is currently a bank similar to the “complete reserve system”. At present, this part of the balance is 1.34 trillion yuan.

We use a map to present the structure of the above-mentioned entire monetary system:

The above 1234 is the balance held by the residents that can be quickly used for payment. However, 3 is not included in M2, so the sum of 124 is M2. For this, we believe that it is a statistical loophole, the balance of the payment account held by the resident, and the ability to perform the payment itself, should be counted in M2, and should be included in M0.

The above 1234 is the balance held by the residents that can be quickly used for payment. However, 3 is not included in M2, so the sum of 124 is M2. For this, we believe that it is a statistical loophole, the balance of the payment account held by the resident, and the ability to perform the payment itself, should be counted in M2, and should be included in M0.

It can be seen that the current base currency issued by the central bank is about 30 trillion yuan. This is the real legal currency of China. It has the legal capacity to pay off all debts in the country. No one can refuse to accept it. This is "compensatory." However, deposits issued by banks are not strictly renminbi, but a vouchers that can withdraw renminbi from banks. They are not legal. That is to say, if the payee and the creditor suspect that their bank of deposit will go bankrupt, he has the right to refuse the bank transfer payment of the customer. The payment company's payment account balance is the payment of the company's advance receipts to the residents. It is a commercial credit and a voucher for withdrawing the RMB. The credit level is even lower.

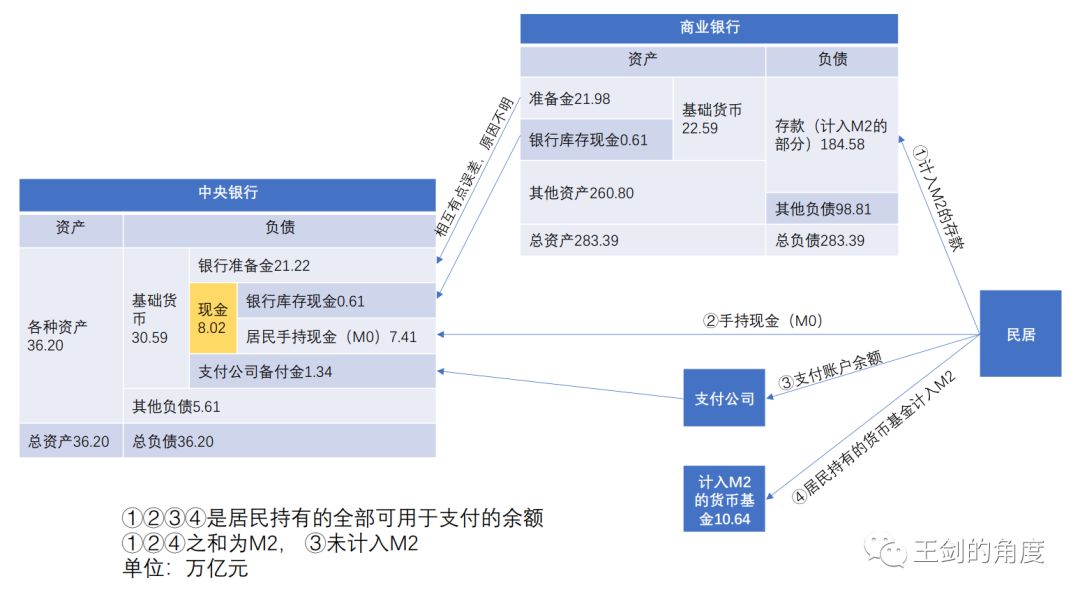

Second, the central bank's digital currency is part of the cash

According to the information about the digital currency disclosed by the central bank, this digital currency is not the same thing as bitcoin, but the digital renminbi, which is a new digital currency other than banknotes and coins. The "Cash" section in the image above. It is a real RMB, and it is legal. We think it is more accurate to call it digital cash, electronic cash, and digital M0 .

Therefore, this kind of digital cash has not changed the existing “central bank-bank” secondary banking system at all, but the cash component has a new existence carrier.

In fact, digital cash itself is not new, and now the UnionPay chip card with the Flash PayPass tag supports e-cash. The following sections may be a bit like advertising, but we really confiscate advertising costs.

The chip of the chip card can actually function as an electronic wallet , that is, the deposit in the bank is taken out, but not in the form of banknotes or coins, but in the form of electronic cash, which is stored in the chip. The electronic cash in the chip is the same as the banknotes. It is anonymous and not lost. When using it, the direct funds are transferred to the other's electronic wallet, which is very similar to the delivery of banknotes, but both parties need to store and read electronic cash. Equipment, such as this chip, and equipment for reading and writing electronic cash, called "card readers" (other devices that can read and write electronic cash include ATM, bank counter readers, etc.).

The above picture is from a report from the 2016 Mobile Payment Network, which shows a portable card reader, the “UnionPay Mini Pay” terminal. It can be seen that this thing is not new. It has been around for many years. Now the latest version is different from the above picture.

But I believe that except for practitioners like us, most of my friends have never seen this thing (in fact, I have never seen anything in kind). It can be seen that the market recognition and promotion effect of this thing is not good, so there must be some reason.

In fact, the biggest drawback is that this product requires the support of two major hardware: chip card (electronic wallet) and reading and writing equipment. Nowadays, the account can be paid directly on the mobile banking or payment company's APP. Even the physical bank card is not used, and no one will be willing to bring the reading and writing equipment. However, this shortcoming seems to be solved now, because after the cloud flash payment, it can solve the hardware problem, it can be operated directly on the mobile phone, and the mobile phone is regarded as an electronic wallet, and the electronic cash can be installed therein, eliminating the need for it. Trouble with hardware.

At this point, there is a more serious security issue, namely: the nature of electronic cash, which determines that it is stored in local hardware (chip or mobile hardware), unlike deposits recorded in bank accounts. Then, if the encryption technology is not hard and cracked, the electronic cash can be copied and pasted, thus achieving "double payment" (a sum of money is used for multiple payments). Today's bank card chips or other hardware certainly have top-level encryption technology, but the technology is progressing at any time, the bad guy's technology is also improving, no one can guarantee that it will never be cracked, and then copy the electronic cash inside. This is not the same as the counterfeit currency of the banknotes. The counterfeit currency is at least fake. The copied electronic cash is exactly the same as the original, and both are true, so there are major security risks.

Moreover, another advantage of traditional cash (banknotes, coins) is anonymity. Although the electronic cash is not registered, but because it is paid out from your chip card, it is really necessary to trace back to it, but there is still a way to anonymity.

In the end, for the above reasons, electronic cash has not been widely promoted.

These security, anonymity and other issues, after decades of pioneering efforts (mainly due to mathematics and computer technology), after the maturity of asymmetric encryption, distributed accounting, blind signature, etc. (blockchain is the technology of these Integration) is expected to be better resolved.

Therefore, the newly developed digital currency of the central bank, although still attributed to electronic cash, still belongs to M0 and bank cash, but due to the adoption of new blockchain technology (or, to be precise, it does not use blockchain technology itself) Rather, it uses asymmetric encryption, distributed accounting, blind signature and other technologies like blockchain technology, and it is expected to improve some existing security issues in the circulation. Therefore, it has the significance of its positive progress.

However, can it be promoted on a large scale? This point depends on the competition between the digital currency and the current popular bank and payment company account payment, to see which kind of payment is more convenient. We will wait and see.

Third, will it significantly affect the banking industry?

Then, we may have to consider a possibility: If the central bank's digital currency is greatly welcomed by the market and the liquidity exceeds expectations, then it is equivalent to taking a large amount of deposits from the bank. What impact will this have on the banks?

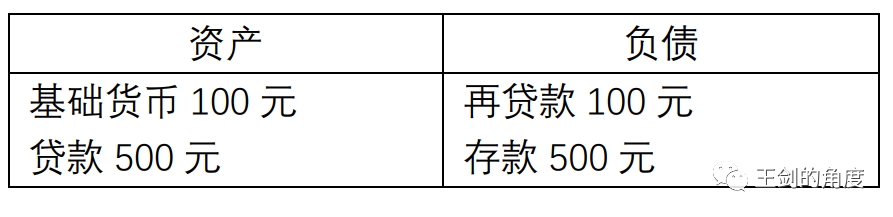

In the above-mentioned secondary banking system, the bank first obtains the base currency from the central bank. The way is generally to ask the central bank to borrow the loan:

Among them, refinancing is to pay interest, usually 2-3% (see different varieties, such as MLF, SLF, refinancing, etc.), and if the base currency is deposited in the central bank, the interest received is very low. If the central bank withdraws cash and becomes cash in stock, there is no interest income. Therefore, at this time, the bank is not making money, and it has to lose money.

The bank then deposited deposits (into M2) to the residential houses through loans and corporate bonds.

At this time, the bank is profitable. The interest rate charged by the bank from the loan is higher than the interest rate paid to the depositor, so the bank obtains the spread. This is the main business logic of the bank. Because China's current account payment is too convenient, residents have less and less money, and M0 accounts for a very low proportion of M2. Therefore, banks have maintained loans and deposits and are happy to earn spreads.

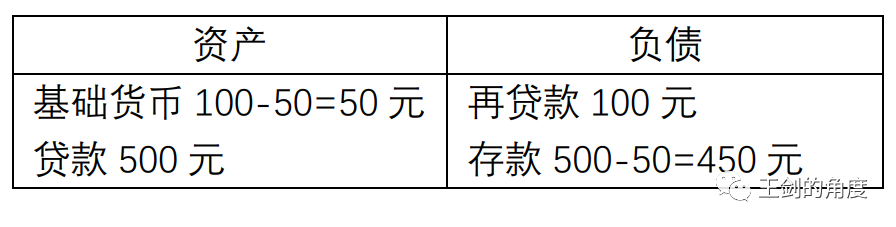

If a resident withdraws money, such as taking out cash (banknotes or coins) for 50 yuan, the bank will have to pay 50 yuan of the base currency obtained from the central bank to the residents. Then the report becomes:

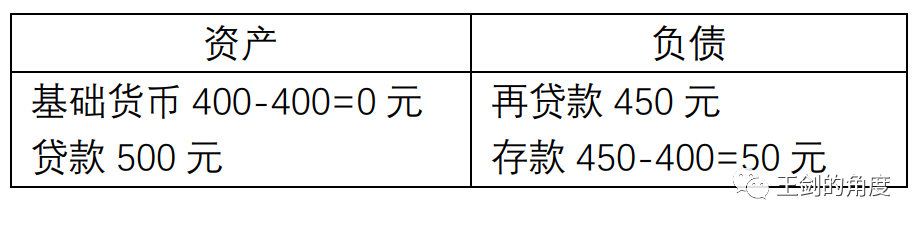

At this time, it seems that it does not affect the bank's profitability. After all, the scale of deposits and loans has not changed much. But if the digital currency is so popular that residents don't hold deposits, take them out, and hold digital currency for daily payments, then the situation is different. For example, after picking up the watch, the residents took another 400 yuan. At this time, the bank did not have a base currency of 400 yuan for the customer to withdraw, so it had to borrow 350 yuan from the central bank to refinance.

Then the residents took away 400 yuan:

At this time, the bank’s statements became mainly dependent on refinancing to support the loan, and the interest rate of the refinance was significantly higher than the deposit (the interest rate of some deposits was higher than the refinance, but since we discussed mainly the The settlement of deposits is mainly due to the current period, so the interest rate is very low. Therefore, the bank's spreads have been greatly narrowed, and the original business logic has been destroyed to some extent.

At this time, the bank’s statements became mainly dependent on refinancing to support the loan, and the interest rate of the refinance was significantly higher than the deposit (the interest rate of some deposits was higher than the refinance, but since we discussed mainly the The settlement of deposits is mainly due to the current period, so the interest rate is very low. Therefore, the bank's spreads have been greatly narrowed, and the original business logic has been destroyed to some extent.

At this time, the bank will also provide customers with e-wallets (in the past, chip cards, which may be APPs in mobile phones in the future), and will also generate certain costs (but save the cost of cash shipping inventory management). Of course, e-wallets enable customers who hold e-cash to still have a business relationship with the bank (if the customer holds the banknotes, it has nothing to do with the bank), increase customer stickiness, and increase marketing opportunities for other products and services, perhaps Come to other income. However, if the digital currency strictly protects the anonymity of cash to the bank, it may also make it difficult for the bank to grasp the customer information and lose the marketing opportunity. Then the bank only bears the cost in the whole process, and the enthusiasm is not high. Fortunately, the central bank officially stated that after the introduction of the digital currency, even if the residents withdraw a lot, the lending function is still in the bank, and the management will still try to protect the enthusiasm of the bank.

At the same time, the central bank also had to substantially increase the placement of the base currency. In the above example, 400 yuan was invested, which is because residents have too many cash withdrawals. In the end, in the secondary banking system, it is reflected in the substantial increase in the “cash” portion, and the currency multiplier has fallen sharply. Banks have weakened their position in the transmission of monetary policy, and their spreads have shrunk significantly. This is a bit of a return to the early years when the payment technology was underdeveloped. The residents used a lot of cash-carrying era. At that time, you can refer to Professor Huang Da’s early monetary studies.

Of course, we think this may not happen. Because this requires digital currency to be much more popular than account payments, and this seems unlikely in the short term. Moreover, the bank account and payment company's account payment can also introduce blockchain technology, and the experience and function of the payment link are also improved.

Therefore, digital currency is still only a part of cash, and cash is a small part of the total amount of money. The existing structure of the entire currency system will not change much.

About the author Wang Jian:

Guosen Securities Economic Research Institute, chief analyst of the financial industry

Researcher, International Monetary Research Institute, Renmin University of China

National Finance and Development Laboratory Banking Research Center Distinguished Research Fellow

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- China Securities Journal: Digital currency is conducive to the internationalization of the renminbi, the road to digitization is the right choice

- Coinbase: Safer to ASIC-friendly PoW coins, anti-ASIC will only lead to mining centering

- Wuzhen finale dialogue: the danger of domestic public chain? Da Hongfei, Shuai Chu, Chang Hao, Starry Sky… 7 guests talked with each other, what do they say?

- Cold Thinking on the Counter-attack of Blockchain——Meng Yan, Mr. Newton, Wang Wei Deep Dialogue

- Li Bin, CEO of Wuzhen·International Cultural Chain: Opportunities and Reflections on Chinese Cultural Digital Asset Chain

- Wuzhen How to dominate the transaction? Five senior investors explain the trend of blockchain investment in 2020

- Babbitt column | He left, leaving a flourishing