Coinbase will insure the $255 million encrypted hot wallet, which is the well-known insurance group Lloyd's

According to CoinDesk's recent news, Coinbase disclosed details of its insured on behalf of customers for the cryptocurrency held. In an opaque market, this move is rare.

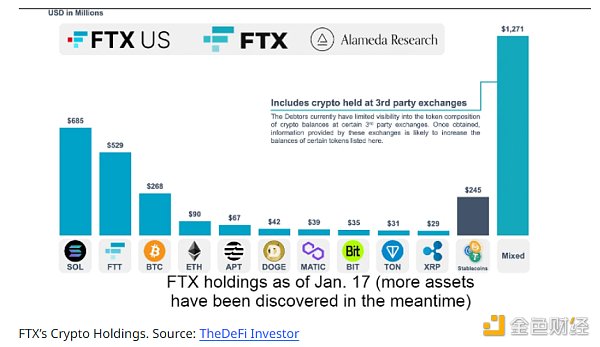

Image source: visualhunt

Philip Martin, the exchange's vice president of security affairs, confirmed in a blog post on Tuesday that the policy covers cryptocurrencies stored in its "hot wallet" worth $255 million. In other words, these assets are basically online and vulnerable to hackers. CoinDesk reported on Coinbase's policy for the first time last November.

- These file blockchain technologies will affect our food, clothing, housing and transportation.

- Is the non-transferable Token not a security? How does the SEC make a one-size-fits-all "lazy politics"?

- How hard is it to lose money on the exchange and how to recover bitcoin digital assets?

According to Coinbase, San Francisco-based Coinbase stores less than 2% of its customers in hot wallets, and the remaining 98% is stored in cold wallets. Its private key is offline to protect it from third-party attacks. In the heyday of the cryptocurrency bull market, Coinbase stored $25 billion in assets on behalf of its customers, but the company declined to disclose the latest data.

Martin's blog post says the policy was developed by Lloyd's registered broker, Aon, and is launched by a global group of US and UK insurance companies, including Lloyd's. Some consortiums of s of London). However, Martin did not disclose the name of the specific insurance underwriter.

Lloyd's covers a range of professional insurance markets that handle a variety of insurance businesses including crime, cyber attacks and natural disasters. Lloyd's received official recognition from the industry in terms of underwriting the potential loss of crypto assets.

Lloyd's previously used to disclose any information about digital asset insurance is quite vague, but now its openness is steadily increasing, at least for some customers in the encryption field.

For example, last month, security expert BitGo advertised that it would insure a $100 million crypto asset in a cold wallet, even named Lloyd's as the primary insurer of the insurance business.

In fact, as far as Martin Bowen is concerned, most of the content is a side-by-side attack on BitGo, as he talks about recent news and announcements about cryptocurrency insurance, suggesting that there is still a lot of "confusion". He then suggested that the company focus on the hot wallet instead of on cold storage, because the assets in the cold wallet are “stationary” and therefore less risky.

Comprehensive coverage

In addition to reporting Coinbase's insurance business more transparently, Martin also took the opportunity to write something on the blog about the emerging market of encryption insurance that bothered him.

He first wrote that, so far, for any cryptocurrency company, the most likely loss of customer assets comes from the loss of hot wallets caused by hackers. Martin pointed out that because of this, the insurance cost for hot wallets is much more expensive than the insurance for cold storage alone.

In addition, hot wallet insurance is provided exclusively by the criminal insurance market, which is different from the cold storage category covered by the item insurance market and is also separate.

The crime protection policy covers what he calls "assets in transit," which traditionally includes theft of ATMs and cash in armed escorts. In the area of cryptocurrency, such policies will cover losses caused by hacking, internal theft and fraudulent transfers. These include legal currency and hot wallet insurance, as well as physical damage or private key data stolen in cold wallets.

On the other hand, the insured market usually provides insurance for “quiescent assets” such as art, precious metals, and items in the vault or on exhibitions. Therefore, for digital assets, the current special insurance business on the market only focuses on physical damage or private key loss of cold wallets, including employee abuse or theft. Martin believes that it is more important to insure the risk of the former, he said:

"Companies should focus on insurance for asset flight. This means that exchanges and wallets should insure enough criminal protection to cover their hot wallets (including adequate buffers to cope with asset price spikes)."

Therefore, the custodian should insure sufficient criminal protection insurance to provide guarantees for the normal transfer of the customer. Or, if they don't use a cold wallet, they should also have enough insurance to cover any assets that can be accessed through the program.

The blog also pointed out that item insurance policies generally do not cover hacking in the traditional sense, and are unlikely to cover any blockchain-specific failures. For example, such a policy does not cover the loss of funds due to failures in the blockchain, such as the vulnerable signature multi-signature implementation of the vulnerable contract. Martin added:

“Properly insuring an item of insurance is a safeguard against major natural or local disasters, or preventing insiders from stealing/damaging private key materials.”

Insufficient capacity of cryptocurrency insurance market

Next, Martin pointed out that since the policy is denominated in French currency and the asset is cryptocurrency, there is a disconnect between the two. This means that in a bull market, it may be a challenge for companies that want to increase their policy caps as asset prices change.

He said the solution to the challenge was for insurance companies to hold digital assets in order to provide policy limits in cryptocurrency to avoid valuation differences. In addition, the policy is usually signed with the exchange or custodian, not directly with the cryptocurrency owner. Martin wrote:

“We need a world where the ultimate owners of cryptocurrencies can directly insure their cryptographic assets in a reliable, well-reviewed, transparent service provider.”

Coinbase claims that although the perceptions of insurance companies and brokers have improved, market capacity is still limited. Some of the larger crypto exchanges simply fill in the insurance gap by simply leaving thousands of bitcoins in place to prevent hackers.

Martin pointed out that the demand for cryptocurrency insurance is growing faster than the speed of new entrants. He concluded by summing up:

“In the cryptocurrency insurance market, we need more participants.”

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- What are the characteristics of the common identity in the securities pass and identity securities?

- The SEC first issued a "green light" to the tokens, and their lawyers taught you to get a "no objection" letter.

- Encryption technology: promoting the digital process

- What does Schnorr's upcoming multi-signature era mean?

- R3 history: from the most beautiful scenery in the past, to the current crisis

- Heavy! The SEC issued the first blockchain token supervision guide, whether it is a securities to see four major points

- Opinion: The non-exchange channel of the currency circle is essentially a brokerage and investment bank.