Exploration of Domestic Practice of STO——Generation and Circulation of Account Receivable Electronic Voucher (1)

Source: Weiyang Network

Author: Jansen Ma

With the development of blockchain bookkeeping, quantum computing and other technologies, all real rights, creditor's rights, intellectual property rights, equity and other property rights and other underlying assets can be confirmed in the legal sense to form a security token ( Security Token) , which becomes a certificate of civil rights with property attributes . Security token is a secure, continuous, and invariant chain-like data structure, and has significant features such as distributed, multi-node consensus, openness and transparency, and immutability.

STO (Security Token Offering) refers to the issuance of securitization tokens, and it issues securities tokens. Unlike the lack of oversight of ICOs, severe asymmetry in information between investors and project parties, and unclear rights and responsibilities, STO is supported by real underlying assets, making blockchain project investment more standardized and more sustainable. In terms of supervision, governments of various countries (especially the US government) have made many attempts to incorporate the existing token market into traditional financial supervision without introducing new supervision policies. This series of articles will explore and study the regulation of STO in French-speaking China.

In the supply chain of core enterprises, small and medium-sized suppliers of upstream and downstream companies often face difficulties such as long account periods and difficult capital turnover. However, banks and other financial institutions do not understand the risk information and financial status of SMEs, and are unwilling to provide financing services, resulting in difficulties in financing and expensive financing for SMEs.

- Data Monthly Report: Cryptocurrency price trend correlation A shares> US stocks Guangdong has the most blockchain companies in the country

- Taobao sells hardware wallets, "currency ban" is still on

- Qingdao Daily Special Edition | Grab the scene of the "window period", Qingdao blockchain industry in progress

In order to solve this problem, many innovative institutions have made a lot of explorations in receivables financing . For example, the simple remittance platform has created a receivable creditor's right certificate, a gold bill, which gathers 1-N suppliers through core enterprises, and introduces external financial institutions such as banks to form an online platform of a complete ecosystem. Another example is the circulable, financing, and splittable receivables creditor certificate “Yunxin” issued by the China Enterprise Cloud Chain platform. The core enterprise issues “class-like commercial tickets” for upstream suppliers. Yunxin ", upstream multi-tier suppliers can arbitrarily split and transfer Yunxin, and can also raise funds or hold due. In addition to core enterprises' self-built networks, some financial institutions, such as Zheshang Bank and Ping An Bank, have launched similar electronic accounts receivables.

Such platforms have a lot of value for financing based on accounts receivable. In terms of improving transaction security . The platform uses the distributed storage, immutability, and timestamp verification properties of technologies such as blockchain to fully record data and trace it at the same time, improving data reliability. In promoting capital flow . The platform involves participants from upstream and downstream suppliers, core enterprises, and banks in the supply chain to the blockchain network to achieve multi-level penetration of core corporate credit. Assets receivables and other assets are confirmed, transferred, and financed on the chain to ensure asset rights; at the same time, assets on the chain can be split and multi-level transferred to promote the movement of funds on the chain and resolve the end of the supply chain Financing dilemma for SMEs. In reducing financial risks . For investors such as banks, the data of the entire supply chain will help the bank to understand the entire supply chain and each of its enterprises more thoroughly. At the same time, the multi-level transfer of credit can help banks to obtain more secure high-quality assets and reduce NPL ratio. In terms of increasing the stickiness of supply chain enterprises . It can help solve the problems of difficult financing and full financing for multi-level suppliers and distributors. It can also increase the stickiness of supply chain owned enterprises and core enterprises and improve overall competitiveness. The integration of corporate information flow in colleges and universities is conducive to enhancing the ability of the industrial chain to cooperate and achieve overall benefits.

At the same time, this type of platform uses accounts receivables as the underlying asset, generates electronic vouchers (similar to tokens), and transfers them, forming a simple prototype of STO for domestic assets, which greatly improves the efficiency and authenticity of financial services in the supply chain. It basically solves the problem of information penetration of multi-level circulation of the underlying assets of small and medium-sized enterprises, and directly obtains the underlying asset information of small and medium-sized enterprises required for financing directly through the trusted DLT account book. significance. This article talks about in-depth analysis of this type of platform.

I. Generation of e-vouchers for accounts receivable

The platform relies on technologies such as blockchain, electronic signatures, etc., and forms an electronic creditor's right after initial confirmation by the core enterprise corresponding to the receivables. It records creditors, debtors (including direct debtors or credit enhancers), debt amounts, and claims Expiry date, etc., and form transaction data (including basic transaction data, online transaction data, etc.) into a creditor's rights data package, and store transaction data in a distributed accounting manner on the blockchain to form a secure, continuous, and invariant chain Data structure, with distributed, multi-node consensus, open and transparent, immutable and other significant features.

2. Transfer of e-vouchers for accounts receivable

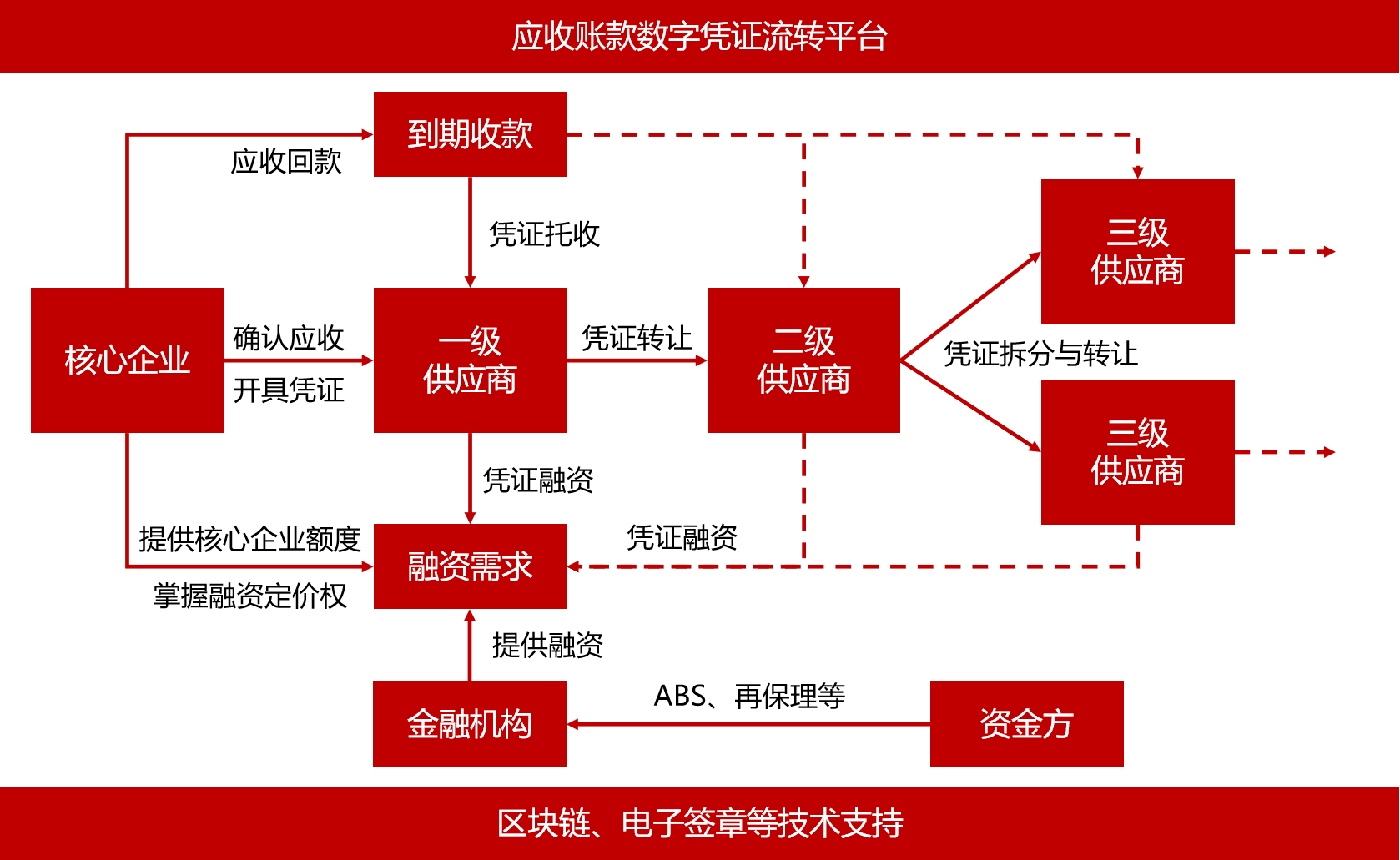

Core companies issue electronic accounts receivables for tier one suppliers, as shown in the figure below. There are three options for tier one suppliers:

The first is to choose to hold the digital voucher and obtain funds.

The second is to choose external financing and transfer accounts receivable to financial institutions (commercial banks, factoring companies, etc.); financial institutions can conduct ABS, re-factoring, etc., and can choose to hold due to obtain funds.

The third is to transfer (split) digital vouchers to secondary suppliers or offset debts. The second-tier supplier can also choose to hold the maturity, or carry out external financing, or transfer the digital voucher to the lower-tier supplier again.

3. Legal issues related to electronic voucher transfer

In the process of generating circulation, there are several legal issues worth paying attention to:

Legal effect of electronic voucher

The electronic voucher of accounts receivable records and reflects the relevant information of credits of accounts receivable (including but not limited to the names of creditors and debtors, the amount of debts of accounts receivable, the term of debts of accounts receivable), which are not independent of accounts receivable A class of property rights that exist (as opposed to instruments). The electronic voucher is a necessary means to apply information technology such as the Internet and blockchain to accounts receivable transactions. Its application is only based on the agreement between the platform participants and does not have a relatively independent basic transaction similar to a bill. Legal status and effectiveness, the underlying assets of such securitized products should still be defined as accounts receivable claims following the principle of substantive determination.

2. Legal Basis for Split Assignment

According to the provisions of Article 79 of the Contract Law, "Creditors may transfer all or part of the contract's rights to a third party, but not transferable according to the nature of the contract, Except. "It can be seen that the current law does not prohibit the division and transfer of the same creditor's rights. The supplier at the next higher level can choose to split the receivable electronic voucher and transfer it to the next one according to its transaction with the supplier at the next level. For a Tier 1 supplier, the essence of the transaction is the transfer of creditor's rights of receivables, and the split transfer is the split transfer of the same creditor's right. There are no legal obstacles to the split flow of accounts receivable.

3. Legal Basis of Settlement of Claims

Article 99 of the Contract Law of the People's Republic of China stipulates that "Each party may offset its own debt with the debt of the other party if the parties have debts due to each other and the type and quality of the underlying objects of the debt are the same. Exceptions are stipulated or cannot be set off according to the nature of the contract. If the parties claim to set off, the other party should be notified. Statutory offsets must not be accompanied by conditions or deadlines. "The supplier at the next level is based on the existence of real trade between the supplier and the supplier at the next level. Relationship, the supplier of the upper level enjoys the debt receivables; through the transfer of the creditor's right, within the amount of the account receivables held by the core enterprise, the creditor's debt elimination method is used to eliminate its debt to the next level. Supplier debt. There are no legal obstacles to debt offsets based on receivables.

4. Uniqueness of transfer of accounts receivable

The transfer of accounts receivable may have “single item over sale”. The platform can effectively prevent repeated transactions within the platform, but it is also necessary to prevent suppliers from using the electronic account receivable vouchers to conduct repeated transactions outside the platform.

About the author: Jansen Ma focuses on emerging technology and fintech compliance. He graduated from Tsinghua University and has worked for many years in national financial regulatory agencies and top fintech companies. Provide legal services and advisory services to financial institutions, investment institutions, technology companies, etc. on innovative products, compliance and licensing. WeChat public account: Fintech Legal Review.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Bank of Korea: No plans to launch central bank digital currency yet

- Bitcoin has become the darling of academia, with more than 13,700 related papers in 2019

- 2020 Outlook: A crucial year in the crypto space, what factors will drive the widespread adoption of blockchain?

- Crypto year review: what we went through in 2019

- Annual Inventory: Hacker Raves Behind the Crypto Market Boom

- "Premature" blockchain 50 index: 40% of companies are still in the research stage

- The path to breaking open finance in 2020