Interpreting DSR: Is DAI one step closer to real money?

Author: Jorge S

Source: Toku View

MakerDAO recently released the most important update since its launch, in addition to officially supporting Multi-Asset Mortgage (MCD), it also introduced DAI Deposit Rate (DSR). MakerDAO has high hopes for it, claiming that DSR will change the game rules of the DeFi ecosystem. Can it really release such a large amount of energy?

DSR as a risk-free return

The so-called DSR, DAI Saving Rate, which is the DAI deposit interest rate, is very easy to understand: MakerDAO provides a savings contract. Users only need to deposit their own DAI to get an annualized interest rate of 2%. It's not hard to speculate why MakerDAO introduced this feature, incentivizing users to buy and hold DAI.

- A few pictures take you to understand the new Nike patent "CrpytoKicks"

- Bitcoin hash value futures will be launched in 2020, how will it affect the mining industry?

- Foreign media: court documents show that New York Mellon Bank and Credit Suisse participate in Telegram's $ 1.7 billion token sale

Since the launch, compared to the creation of CDP to lend DAI, receiving and holding DAI has always lacked effective incentives. Mortgage ETH to lend DAI can meet the needs of users on the chain to increase leverage, and also provides a solution for many project teams that have raised ETH but need to use fiat currency to pay for expenses, but the other side of the transaction, that is, receiving and holding DAI People, but did not get any benefits, but may have to bear a certain loss of liquidity (compared to USDT, DAI's liquidity still has a very large gap).

The success of mortgage and lending platforms such as Compound and dYdX has undoubtedly helped MakerDAO find a solution. We can see that since their emergence, these mortgage lending platforms have effectively absorbed a large amount of savings by providing interest to deposit users.

It is to be expected that MakerDAO will adopt such a measure that has been proven effective by the market. However, compared with lending platforms such as Compound and dYdX, DSR has three significant differences:

First, there is no run risk . Lending platforms such as Compound will lend users' deposits to other users. In extreme cases, if the fund pool is emptied, deposit users will not be able to redeem their liquidity. The DSR does not lend the user's deposit, and the DAI received by the borrower does not come from the DSR deposit, which avoids the risk that the deposit user cannot redeem liquidity in real time.

Second, there is no counterparty risk . Similar to the previous point, because lending platforms such as Compound will lend deposits, changes in the mortgage status and solvency of loan users will also bring new risks to deposit users.

Third, there is no platform risk . When using lending platforms such as Compound, users not only bear the risk of holding DAI, but also bear the new risks introduced by the Compound platform itself. DSR is officially provided by MakerDAO, and users do not need to bear additional third party risks. In other words, the risk of using DSR is equivalent to the risk of holding DAI, and there is no new risk increase.

In a sense, we can think of DSR as the risk-free rate of return for DAI . This is similar to defining the yield of US Treasury bonds as the risk-free rate of return for the US dollar, because holding US Treasury bonds only needs to bear the risk of the depreciation of the US dollar, without having to bear additional new risks. From this point, we can say that DSR is a big step for DAI to real currency. If DAI can really become the de facto currency in the DeFi ecosystem, then DSR will undoubtedly become a very important market indicator.

DSR as a price stabilization mechanism

In the updated white paper, DSR is clearly described as a "price stabilization mechanism", that is to say, like the stable rate, DSR will also be used as a tool to regulate market supply and demand. If the price of DAI is higher than One dollar will reduce the DSR to curb demand. If the price of DAI is lower than one dollar, the DSR will be increased to drive demand.

Here we have to re-examine whether the price stabilization mechanism of DAI is effective enough. The stable currency can maintain relative stability with the price of the anchor currency, and its most basic logic comes from arbitrage. When the stablecoin price breaks away from the anchor price, an arbitrage opportunity will appear, and the behavior of the arbitrageur will pull the price back to the anchor price. Take USDT as an example, if its price is higher than one dollar, the arbitrageur will exchange USDT through the official channel and sell it on the market, thereby pulling the price back to one dollar, and if it is lower than one dollar, the reverse operation is performed. The arbitrage mechanism is very simple and effective, and the correction of the price deviation can be realized efficiently.

In contrast, when the price of DAI deviates from one dollar, arbitrageurs have no way to make immediate profits through operations such as borrowing, buying and selling. The arbitrage behavior must be completed until the price of DAI returns to one dollar. As for when the price will return to one dollar and whether it can return to one dollar, it is difficult to determine. Therefore, arbitrage risks and frictions are very large and cannot be used as the main means of stabilizing prices.

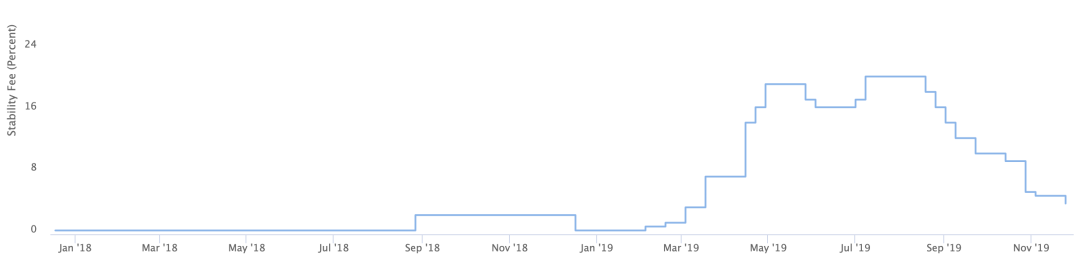

In fact, the price stability of DAI has always been achieved by adjusting the stabilization rate. Since the launch, the adjustment of the stable rate has occurred more than 20 times, ranging from 0.5% to 20.5%.

MakerDAO previously stated that in the early stage of going online, the stable fee rate will be adjusted through governance, and in this process, a reasonable adjustment mechanism will be gradually explored, and the adjustment of the stable fee rate will eventually be automated. However, from the current situation, automation is still difficult to achieve. For a long time, stable rates will continue to be adjusted by means of governance.

After increasing the DSR, MakerDAO will be able to adjust the deposit interest rate and loan interest rate separately. This flexibility will provide MakerDAO a huge advantage in competition with other platforms. At the same time, as the complexity of systemic regulation rises, automation becomes more difficult to achieve, and the quality and efficiency of governance actions will affect the health of the entire system to a greater extent .

Benefit structure change

Another issue worth considering is who gets the benefits of DSR. The income structure has not changed, and some participants have increased their profits, and the interests of others must have diminished. Intuitively, we may think that the holders of MKR are damaged. The interest (stability fee) paid by the borrower was allocated to the holders of MKR. Now it will be distributed to DSR deposit users, and the share of MKR will naturally It's small. But a closer look at the changes after this update reveals that this is not the case.

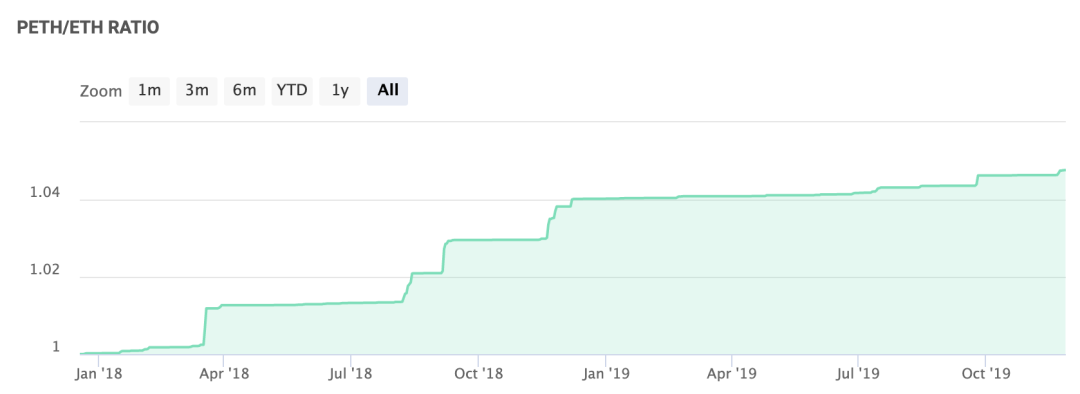

In the previous Single Asset Mortgage Version (SAI), before borrowing, you need to exchange ETH to PETH. With the occurrence of liquidation, the PETH used to pay the liquidation penalty will be destroyed, so the price of PETH relative to ETH has been rising. Therefore, when the borrower repays and leaves the market, it is profitable to redeem the PETH to ETH. This is equivalent to paying an interest to all users who collateralize ETH. After the new version is launched, this interest will no longer be paid.

As can be seen from the price change of PETH above, the annualized interest income is more than 2%, and its payment object is ETH in all mortgages, but DSR only needs to pay to the DAI in the savings. Therefore, compared to the previous version, the holders of MKR will not suffer any losses, but the borrowing costs of the CDP creators have really increased . It is foreseeable that this will lead to the use of PETH for financial management, and users who have only mortgaged but not borrowed will withdraw their mortgages, thereby reducing the overall mortgage rate of the platform and increasing system risk.

We can make a general summary, DSR will become a risk-free rate of return for DAI, and provide a relatively effective incentive for holding DAI. As a price stabilization mechanism, DSR will make MakerDAO more flexible in competition and also make governance work. It becomes more complicated and important; compared to the single asset mortgage phase, the launch of DSR will not harm the interests of MKR holders, but will cause the actual cost of borrowing to rise. DSR is an important and inevitable step in the development of DAI. We can wait and see if it can become a Game-Changer.

We will continue to update Blocking; if you have any questions or suggestions, please contact us!

Was this article helpful?

93 out of 132 found this helpful

Related articles

- Research Report | Guangzhou Blockchain Industrialization Policy Statistics, Investment Funds and Scenario Applications

- The secret of the "through" IPO of the A round was the issue of Equity Token?

- JP Morgan's blockchain payment network will run in Japan early next year, with more than 80 Japanese banks hoping to join the network

- Nike's "encrypted shoes" received US patents, can trace the authenticity, breed new shoes

- Xinhua News Agency Review: How will blockchain affect daily life?

- Long Baitao Recommendation | European Financial Sovereignty in the Digital World

- Ethereum public chain has achieved milestone application again! Bank giant Santander successfully redeems $ 20 million in bonds